G10 currencies may bully the Japanese Yen this week as growing optimism over a swift economic recovery from the pandemic boost appetite for riskier assets at the expense of safe-havens.

The Yen has already lost ground against major currencies over the past 36 hours, with the most noticeable losses versus the Euro and Swedish Krona. As investors place their hopes in an economic recovery fueled by unprecedented central bank support and handsome fiscal stimulus packages, the Yen and other safe-haven assets may remain in the direct firing line.

EURJPY finds comfort above 121.00

The EURJPY remains in an uptrend on the daily charts with support at 121.00. An intraday breakout above 122.00 should encourage an incline towards 122.80 and 123.70. Should 121.00 proves to be an unreliable support, the currency pair may retest 119.70.

USDJPY remains in 100 pip range

A breakout opportunity is forming on the USDJPY with a weakening Yen potentially pushing prices towards the 108.00 resistance. A solid breakout above this point may open the doors towards 109.40 and 110.20. If prices end up tumbling below 107.00, expect the USDJPY to challenge 105.90.

GBPJPY approaches 135.00

It has been the same story for the GBPJPY for the past three weeks. Prices remain in a wide 340 pip range with support at 131.600 and resistance at 135.00. A solid close above the 135.00 could trigger a sharp move towards 137.00. Lagging indicators like the 20 and 50 SMA in addition to the MACD are in line with the bullish setup.

AUDJPY slips after RBA decision

We see some weakness in the Australian Dollar after the Reserve Bank of Australia left interest rates unchanged at 0.25%. The AUDJPY may weaken towards 72.80 in the short term if an intraday breakdown below 74.40 is achieved. Alternatively, a softer Yen could provide enough support for the currency pair to test 76.50.

Commodity spotlight – Gold

Since we are discussing safe-haven assets, it does not hurt to speak about Gold which is just over $16 away from the $1800 level.

The precious metal may struggle to push higher in the near term amid the improving mood with the next key level of interest around $1765.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Global markets are mixed currently after the rally continued on Monday as US markets reopened following July 4 holiday. US equities advanced Monday led by financial and technology shares.

Forex news

Currency Pair

Change

EUR USD

-0.51%

GBP USD

+1.76%

USD JPY

+0.28%

The Dollar weakening has halted today . The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, lost 0.4% Monday despite the Institute for Supply Management report services sector recorded sharpest recovery in June since the survey was created in 1997. Both GBP/USD and EUR/USD continued rising Monday as Eurostat reported retail sales in euro-zone rebounded sharply in May. Both pairs are lower currently. USD/JPY continued sliding yesterday while AUD/USD accelerated its climbing with both pairs reversing their dynamics currently as the Reserve Bank of Australia kept interest rates unchanged at ultra-low 0.25%.

Stock Market news

Indices

Change

Dow Jones Index

-1.08%

GB 100 Index

-0.69%

Nikkei Index

-0.58%

Futures on three main US stock indexes are in red currently. Stock indexes in US rallied Monday: the three main US stock indexes posted gains ranging from 1.6% to 2.2% as the Institute for Supply Management non-manufacturing index jumped to 57.1 in June from 45.4 in May. Readings above 50.0 indicate industry expansion, below indicate contraction. European stock indexes are edging lower currently after a rebound on Monday led by bank shares. Asian indexes are mixed today after China on Monday accused the US of undermining stability in the South China Sea as US Navy conducted exercises in the area with two aircraft carriers and accompanying vessels.

Commodity Market news

Commodities

Change

WTI Crude

-1.07%

Brent Crude Oil

-0.87%

Brent is edging lower today. Oil prices ended higher on Monday against the background of Saudi Arabia’s decision to raise the premium of its benchmark grade crude, and all other grades, by $1 a barrel. The US oil benchmark West Texas Intermediate (WTI) for August slipped however 0.05% Monday. September Brent crude climbed 0.7% to $43.10 a barrel on Monday.

Gold Market News

Metals

Change

Gold

-0.39%

Gold prices are retracing lower today. August gold gained 0.2% to $1793.50 an ounce on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

The has Dollar stumbled into the new trading week with a nasty NFP hangover despite enjoying a holiday extended weekend.

There is a strong sense of optimism in the air despite rising coronavirus cases in the United States, and this risk-on mood is boosting appetite for equities at the expense of safe-haven assets like the Dollar.

Expect the Greenback to remain depressed over the next few days if economic data continues to improve and market players repeatedly shrug of rising coronavirus cases in the United States and some other countries.

Given how the migthy Dollar was treated without mercy by every single G10 currency on Monday, the week ahead could rough and rocky if the current themes remain intact.

Technical traders will continue to observe how the Dollar Index (DXY) behaves below 97.15 on the daily timeframe. Prices are currently trading under the 20 Simple Moving Average while the MACD points to the downside. If the risk-on remains the name of the game this week, the Dollar Index may sink towards the 96.00 support level. A breakdown below this point could encourage a decline lower towards 94.70.

Dollar bulls can still regain some control above 97.15, which could re-open the gates towards 97.80 as illustrated on the four-hourly timeframe.

Euro enjoys Dollar induced sugar rush

Over the past 18 hours, the EURUSD has jumped over 100 pips to hit a fresh two week high at 1.1340.

Given how the primary driver behind the Euro’s aggressive appreciation was based around a tired and vulnerable Dollar, the upside may face some obstacles down the road. Fundamentally, sentiment towards the European economy remains shaky thanks to rising coronavirus cases, mixed economic data and EU leaders being divided over the €750bn pandemic fiscal plan.

Technically, the EURUSD certainly has the potential to push higher…but that will depend on whether the upside momentum is sufficient enough to secure a solid daily close above 1.1300.

Should this level prove to be reliable resistance, the EURUSD is seen sinking back towards 1.1270 and 1.1200 with a longer-term target around 1.1100.

Gold welcomes weaker Greenback

Can you believe Gold is trading only $16 away from $1800.

The precious metal remains bullish on the daily charts as there have been consistently higher highs and higher lows. For as long as $1765 proves to be reliable support, Gold has enough backing to attack $1800. Lagging technical indicators like the 20 Simple Moving Average and MACD support the bullish bias.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

More new people may have made their first purchase of physical gold or silver in the past 4 months than in any four-month period in history. This sort of data isn’t reported and tracked. But if our experience as one of the nation’s largest precious metals dealers is representative, we believe that’s the case.

We’ve never seen so much retail demand, and a big portion of the buyers are first timers.

With the new wave of people entering the market comes a fundamental question lots of them have before they get started: What do I do with the metal after I buy it?

Physical gold and silver are useful both as an investment and crisis insurance, but it takes a bit of explaining.

Some folks wonder how they might go about actually realizing profits. It will be different than logging into a brokerage account and hitting the “sell” button.

Others have heard precious metals are a form of emergency money they can use to buy groceries should the U.S. dollar fail, but they have trouble picturing exactly what that could look like.

Here are some ways to think about how metals can work both as an investment and as money if our fiat currency outright dies…

Gold and silver are ideally positioned to capitalize on a couple of powerful trends which will dominate markets in the coming years: price inflation and declining confidence in institutions including government, the Federal Reserve Note dollar, and Wall Street.

Investors have an excellent chance of buying metal today and eventually selling it for a healthy profit – measured in both Federal Reserve Notes AND in real terms.

Investors in an ETF, such as GLD or SLV, might be right on the money about the trends and find out their investment failed anyway. It could turn out the ETF was stuffed with paper IOUs which weren’t honored, rather than actual metal.

When the time comes to sell metal and cash in, new investors should know there is a ready and liquid market for their coins, rounds, and bars. They will have plenty of places to go.

Dealers are buying bullion products from customers literally all day long.

Selling bullion can be as easy as buying it. You can walk into a local dealer, call Money Metals Exchange, or go online to sell instantly at the current market price. Just lock a price, deliver your metal, and receive payment. It’s as easy as that.

When it comes to how precious metals might be used in the midst of a currency crisis, the truth is none of us knows exactly what to expect.

If confidence in fiat (paper) money collapses, perhaps the government will finally reform the dollar by resuming a gold standard.

Maybe a crypto currency will become a medium of exchange. The tokens could even be backed by physical metal to enhance trust.

Or, it’s possible merchants will price goods and services directly in grams of gold or silver. In that scenario, people will once again take silver to the grocery store.

There are lots of ways things could unfold. However, a few things are certain based on thousands of years of history. Fiat currencies always fail in the long run. Physical gold and silver are trusted, and even more so during uncertain times.

Meanwhile, they are always valuable in exchange for local currency. Today, there is a price for gold in virtually all of the world’s currencies and that will be true tomorrow.

The beauty of owning gold and silver bullion is that you don’t have to guess what people will be using as money in the future. Whatever it is, people will be eager to exchange it for your precious metal.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

– One thing is very certain right now – we live in very interesting times. As the world rushes head-first into the 21st Century, it appears one of the most pressing issues before all of us is to navigate the risks and opportunities that continue to stack up ahead of us. Within the first 20 years of this century, the global markets have experienced many shifts and big price rotations. Emerging markets, Oil, Technology, Bio-Tech, Miners, Metals, Currencies, Cryptos – we can look at all of these on a longer-term basis and see a boom cycle and a moderate bust cycle event.

The current trends suggest global investors are pouring capital into the US technology stocks which is what is driving the NASDAQ to new all-time highs. We published this article in late June suggesting a parabolic top pattern may be setting up in the global markets – which may be very similar to the DOT COM peak in 1999~2000 explained here.

Our researchers believe the global shift away from risk and into hot sectors are driving capital investments into a frenzy right now. It reminds us of the frenzy in the US in the late 1990s when housing, technology stocks, and credit expansion rolled into a frothing expansion phase – then burst suddenly in 1999. There were plenty of signs in 1997 and 1998 that the frenzy buying was a huge risk – but traders and consumers simply ignored the risks and kept buying.

Similarly, this same type of bubble mentality happened in 2017 with Bitcoin. In less than 24 months, Bitcoin rallied from $370 in early 2016 to $19,666 near the end of 2017 – a massive 8000%+ rally. The similarities of the Bitcoin rally and the rally of the US stock market in the late 1990s is the mentality of the investors throughout these bubbles – the “no fear” mentality that it will keep going higher and higher. The same type of mentality appears to be happening in the US stock markets right now and the data suggests something vastly different is really taking place.

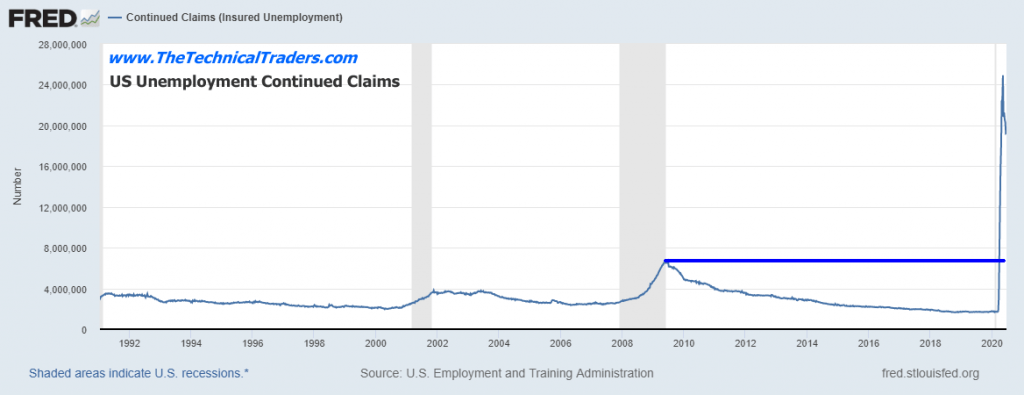

Unlike what happened throughout recent history, the globe has recently experienced a massive disruption event – the COVID-19 virus. This disruption has displaced economic output and consumer earnings on a massive scale – and we are just starting to learn how disruptive these economic factors may be. One item we believe is severely under-estimated is “consumer earning capabilities”. The number of jobless in America has risen to well over 35 million (over 10% of the population). If the COVID-19 virus continues to disrupt consumer’s ability to earn income and engage in the economy over the next 6+ months or longer, there is a very real possibility that the V-shaped recovery everyone believes is happening will simply not happen at all.

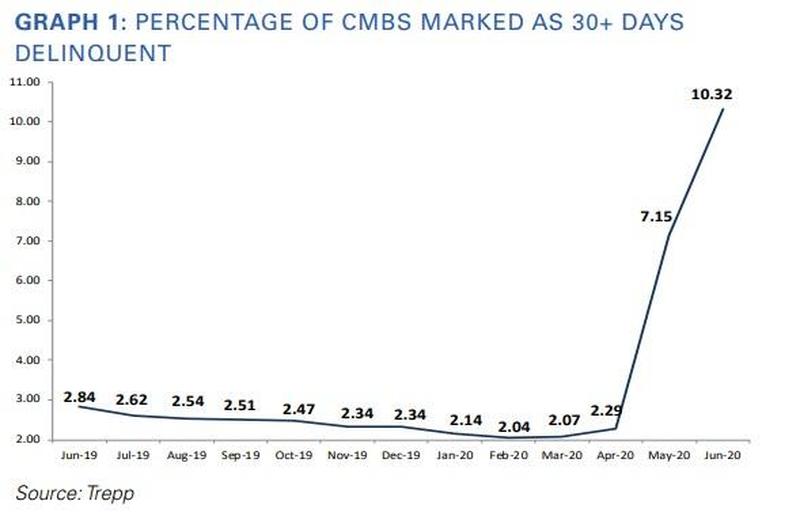

One of the most ominous signs of a broader consumer and commercial contraction happening in the US markets is the skyrocketing delinquency rates for commercial real estate. Trepp recently published new data suggesting the commercial real estate market is experiencing a massive increase in delinquencies of 30+ days which may lead to a wave of high-value defaults. Other research suggests US Banks may face $48+ Billion in commercial real estate loan losses.

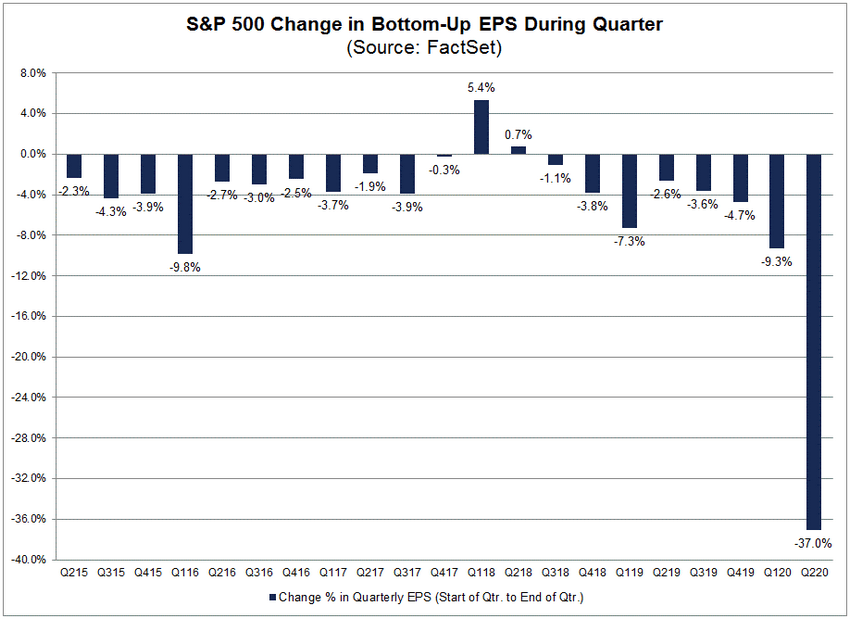

The Q2:2020 earning estimates have decreased by such a large amount that all investors should prepare for a shocking series of data over the next 30+ days. Nike surprised everyone with a nearly $800 million loss for their Q4 ending May 31, 2020. We just read that PizzaHut parent, NPC, filed for bankruptcy recently. This recent Bloomberg article suggests a massive wave of US corporate bankruptcies could continue throughout 2020 and well into 2021 and extended economic pressures erode the foundations and operations of hundreds or thousands of US businesses ().

What is happening in the US markets right now is that foreign and US investors are piling into this deep price rotation expecting the US Fed to do whatever is necessary to support the markets throughout the COVID-19 virus event. We believe the risks for investors have never been higher as the global markets teeter on the edge of a partial recovery while the COVID-19 virus surges again throughout the US.

We’ve kept our clients actively protected from the risks within the markets and continue to advise them on how to identify profitable trades within the current market trends.

In the next part of this article, we’ll explore more data facets related to the Q2:2020 and the future expectations of the US and global markets. Our biggest concern is the destructive capabilities of the general consumer. At some point, we have to understand the consumer drives 85% of the US GDP and future expectations. If this event destroys the consumer, then it will destroy future expectations.

Keep in mind, we do not trade or invest on fundamentals or economic cycles because we know they can lead or lag stock prices by several months at times. Our focus as technical traders is to follow the price trend and trade accordingly. Stay tuned for part II.

Get our Active ETF Swing Trade Signals or if you have any type of retirement account and are looking for signals when to own equities, bonds, or cash, be sure to become a member of my Passive Long-Term ETF Investing Signals which we are about to issue a new signal for subscribers.

Chris Vermeulen Chief Market Strategies Founder of Technical Traders Ltd.

NOTICE: Our free research does not constitute a trade recommendation or solicitation for our readers to take any action regarding this research. It is provided for educational purposes only. Our research team produces these research articles to share information with our followers/readers in an effort to try to keep you well informed.

As governments around the world begin to reopen their borders, it’s clear that efforts to revive the economy are redrawing the lines between who will prosper, who will suffer and who will die.

Emerging strategies for restoring economic growth are forcing vulnerable populations to choose between increased exposure to death or economic survival. This is an unacceptable choice that appears natural only because it prioritizes the economy over people already considered marginal or expendable.

The management of borders has always been central to capitalist economic growth, and has only intensified with neoliberal reforms of the last several decades. Neoliberal economic growth has increasingly become tied to opening up national borders to the flow of money and the selective entry of low-wage labour with limited access to rights.

Nation-state borders regulate this flow, and in so doing, reconstitute the borders between people: those whose lives must be safeguarded and those who are considered disposable.

COVID-19 has brought heightened visibility to these border-making practices, with the pandemic intensifying the decisions between economic and social life.

Anxious to avert the potential loss of as much as 95 per cent of this year’s vegetable and fruit production, temporary farm workers were deemed the essential backbone of the agri-food economy. For the health and safety of Canadians and seasonal farm workers, farmers required the farm workers to self-isolate for 14 days in order to prevent the spread of the virus.

But the deaths of two farm workers in Windsor, Ont., and serious outbreaks of COVID-19 infections among migrant workers on farms across the country, have revealed systemic forms of racism that reveal the priority given to profit maximization over the health and safety of Black and brown migrant farmers.

With worker welfare left largely to the discretion of employers, it is not altogether surprising that reports of crowded and unsanitary housing, an inability to socially distance, delays in responding to COVID-19 symptoms and threats of reprisals for speaking out have become rife throughout the agri-food economy. Even as COVID-19 cases soar in Ontario, provincial guidelines make it possible for infected farm workers to continue working if they are asymptomatic.

It is a tragic irony that the quest for a better life among migrant workers should be one that demands levels of exposure to abuse, threats, infection and premature death that few citizens are likely to face.

Choosing between health and the economy

Now, as governments speak of opening borders more widely due to the economic costs of COVID-19, countries are beginning to make new, challenging decisions between public health and economic growth.

For example, across the Caribbean, the abrupt closure of international borders decimated the region’s tourism industry overnight. Estimating a contraction of the industry of up to 70 per cent, Standard & Poor has already predicted that some islands will experience significantly deteriorated credit ratings.

For example, with tourism accounting for half of Jamaica’s foreign exchange earnings and more than 350,000 jobs, it is not entirely surprising that the tourism minister has justified re-opening as “not just about tourism. It is a matter of economic life or death.” It’s also not surprising that resort chains like Sandals and airlines alike have been eager to resume business as usual.

But assurances that “vacations are back,” even as new cases emerge, ring hollow given that most Caribbean countries have long struggled with overburdened health-care systems. And even with new protocols for screening, isolating or restricting the mobility of infected visitors, it is likely that the region’s poorer citizens — many of whom are women in front-line hospitality services — will bear the brunt of the costs of new infections.

Unequal dependencies

The dependence of Caribbean and Latin American governments on tourism and remittance dollars, and Canada’s dependence on Black and brown people to carry out low-paid essential work, are unequal dependencies that are intimately tied. For the most vulnerable, these dependencies mark the stark overlap between economic life and COVID-19 death.

Yet COVID-19 has also presented us with a unique opportunity to rethink the border inequalities that have governed our lives and the primacy of the economy within it.

It forces us to ask: Who does “the economy” serve? What types of activities are valued or dismissed when we prioritize economic growth? Whose life is valued, and whose continues to be expendable?

Prioritizing the economy over the lives of the poorest and most vulnerable should never be an acceptable fix.

About the Authors:

This is a collaborative article written by members of the Global Economies and Everyday Lives Lab at Queen’s University, Canada. Nathalia Ocasio Santos, Grace Adeniyi Ogunyankin, Priscilla Apronti, Hilal Kara and Tesfa Peterson co-authored this piece.

Slowing euro-zone business activity contraction bullish for EURUSD

Euro-zone’s business activity contraction slowed in June: the PMI Composite index rebounded for a second successive month to 48.5 from 31.9 in May, when an increase to 47.3 was expected. Readings above 50.0 indicate industry expansion, below indicate contraction. This is bullish for EURUSD.

The pound sterling’s latest rebound could be short-lived for the lack of new development on the Brexit front. Unexpected cancellation of last Friday’s talks could only put fresh strain on an already tight schedule.

As both parties meet up this week, the prospect of resolving their differences seem to be rather dim. Traders can expect short-term volatility at the UK’s GDP release. Unless there is substance to the trade deal with the EU, Sterling is likely to underperform in the coming days.

The euro is supported by the trend line above 0.8950 and is positioned to rally to the previous high above 0.9400.

AUDJPY Rises Amid Bullish Commodity Prices

Regardless of news of a potential second wave of COVID, the Australian dollar’s V-shaped recovery is a testimony that there is firm optimism that the world’s economy might have bottomed out.

Rising prices of iron ore and copper, supported by returning Chinese demand, have contributed to a recovery in Australia’s trade balance. The combination of reopening and bullish commodity markets offer the Aussie a lead against less growth-sensitive currencies.

The pair has found solid buying interests along the 30-day moving average above 72.50. The recent top of 76.60 is the next target in sight.

USDCHF Drifts Lower on Virus Surge

Record surge in new infections in the US is posing a serious challenge to the much-anticipated economic recovery. So much so, that the latest uptick in employment was received with mild enthusiasm. 4.8 million new jobs were added against a consensus of 3 million, though the back-pedaling on reopening across several states dampened hopes of a definite U-turn.

As a result, the greenback is likely to stay muted against its safer Swiss counterpart as investors stick with a cautious mind. The US dollar is heading toward 0.9250. Any meaningful rebound will need to lift the key resistance of 0.9650 first.

CADJPY Inches Higher on Improved Sentiment

The Canadian dollar is trying to catch its breath after a stellar recovery against the Japanese yen back in June. Overall, market sentiment has improved since, and that could argue for a continuation of the bullish reversal.

Prices of oil, Canada’s biggest export, have been grinding higher and offer a strong positive correlation to the movement. Should Friday’s jobs data paint a less-than-gloomy economic picture, as last week’s GDP number did, the Loonie may see more of the upside in the coming days.

As long as the pair stays above 78.00 the bullish bias stays. 81.80 is a key resistance to lift for an extended reversal.

The latest manufacturing data from the United Kingdom for the month of June created some optimism. After a disastrous drop in the early months of this year, manufacturing is showing some stabilization.

Data from IHS Markit saw the UK’s Purchasing Manager’s Index rising from 40.7 in May to 50.1. A reading above 50 indicates expansion in the sector.

The rebound came as UK factories re-started operating after the lockdown due to the global pandemic.

Fed Minutes Reveal Discussions on Yield Curve Control

The US Federal Reserve bank released the meeting minutes from the June monetary policy meeting. As interest rates remain near zero, the minutes saw policymakers discussing the various tools available for monetary policy.

The minutes showed that policymakers were discussing the idea of yield curve control, something similar to what the Bank of Japan does currently.

Members also indicated support for outcome-based forward guidance, with some in favor of the forward guidance being anchored to the inflation data.

Retail Sales in Australia Rebound in May

The latest economic reports from Australia indicate that perhaps the worst is over. The retail sales data form the Australian Bureau of Statistics showed that retail sales grew 16.9% in May on a month over month basis.

This follows a 17.7% decline just the month before. Food retail grew 7.2% while personal accessories grew 129%. Restaurant and take away services accounted for about a 30% increase on the month.

US Labor Market Recovers for a 2nd Consecutive Month

The latest figures from the Labor Department showed another solid month in the jobs market. Payrolls grew 4.8 million in June following up on a 2.7 revised increase in May.

Economists were forecasting an increase of just 3 million during the month. The labor department noted that despite the second month of increase, it is still far off from the 22.2 million jobs that were lost in the months of March and April.

The US unemployment rate eased from 13.3% in May to 11.1% in June. Meanwhile, the average hourly earnings grew by 1.2% on the year in June.

Upcoming Economic Events

ISM Non-Manufacturing PMI to Recover in June

The Institute of Supply Management will be releasing the non-manufacturing data for June. According to the preliminary estimates, non-manufacturing or services activity is forecast to rise from 41.9 in May to 44 in June.

While this indicates a modest recovery, the fact that non-manufacturing activity is still below 50 suggests contraction. However, the estimates might be conservative. This comes following last week’s manufacturing PMI report which saw a rebound in the index from 43. in May to 52.6 in June.

Reserve Bank of Australia to Stay on the Sidelines

The RBA will be kicking off a new month with its monetary policy meeting. According to the general estimates, the RBA will not be making any changes to interest rates.

The RBA cut rates in March this year responding to the pandemic crisis. While the Australian economy has also been hit, there is evidence building up that the economic recovery is underway. This could mean that the RBA will remain on the sidelines but maintain a dovish outlook to support the markets.

Germany Factory Orders to Rebound in May

The latest figures from Germany will likely show an improvement in the factory orders. After falling nearly 36% in April, the data for May suggests a more modest decline of just 28%.

With the ECB and the European Commission injecting stimulus into the markets, there is evidence of recovery already. This could potentially mean that investors will shrug off the data. Later in the week, Germany will also be releasing data on industrial production for May.

China’s Inflation Set to Improve in June

The latest inflation figures from China will likely show that consumer prices are rising steadily. Forecasts show that headline inflation will rise from 2.4% in May to 2.7% in June on a year over year basis.

Meanwhile, the producer price index is forecast to see a modest improvement from a 3.7% decline previously to a 3.3% decline in June. Consumer prices in China hit a high of 5.4% in January before easing steadily since then.

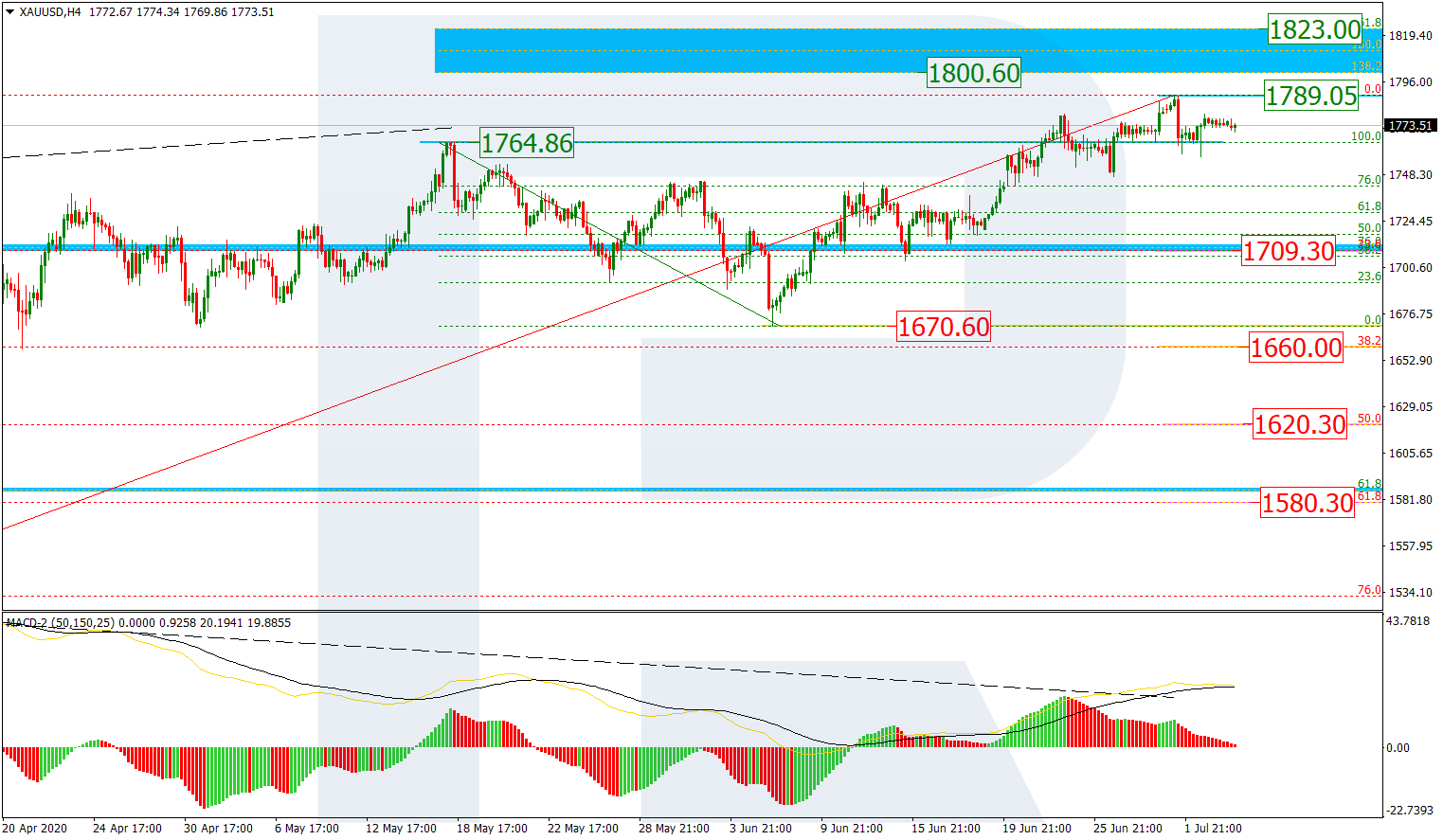

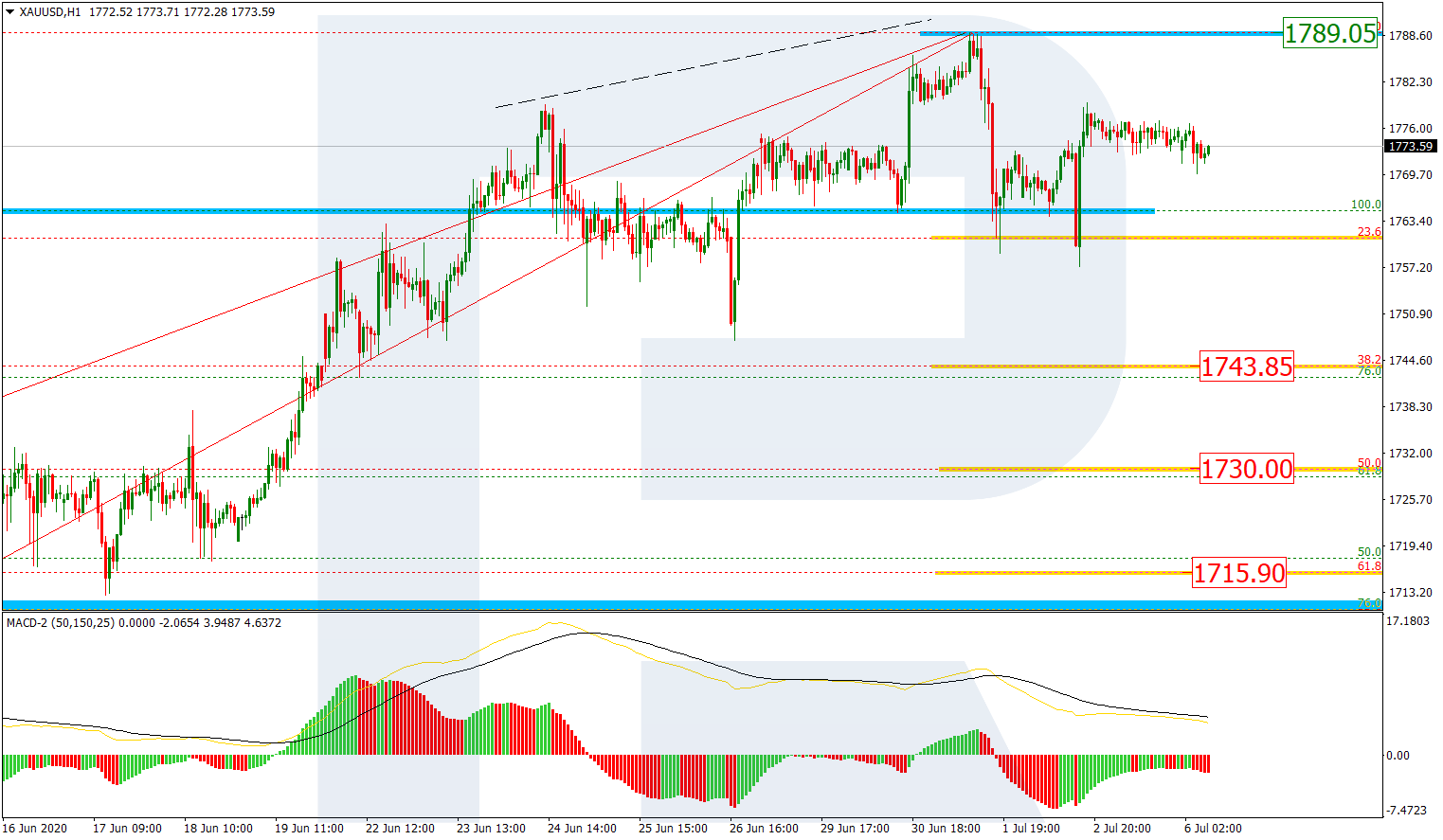

From the technical point of view, the H4 chart shows that XAUUSD is moving above the broken high at 1764.86. This situation means that the pair has fixed above the high at 1789.05 in order to continue the ascending tendency towards the post-correctional extension area between 138.2% and 161.8% fibo at 1800.60 and 1822.70 respectively. However, a divergence on MACD and low market volatility indicate a possible reversal or pullback. The key support is at 1670.60. The first correctional target may be 23.6% fibo at 1709.30, while the next ones are 38.2%, 50.0%, and 61.8% fibo at 1660.00, 1620.30, and 1580.30 respectively.

As we can see in the H1 chart, there was a local divergence on MACD, which made the pair start a new decline that has already tested 23.6% fibo. Later, the decline may continue to reach 38.2%, 50.0%, and 61.8% fibo at 1743.85, 1730.00, and 1715.90 respectively.

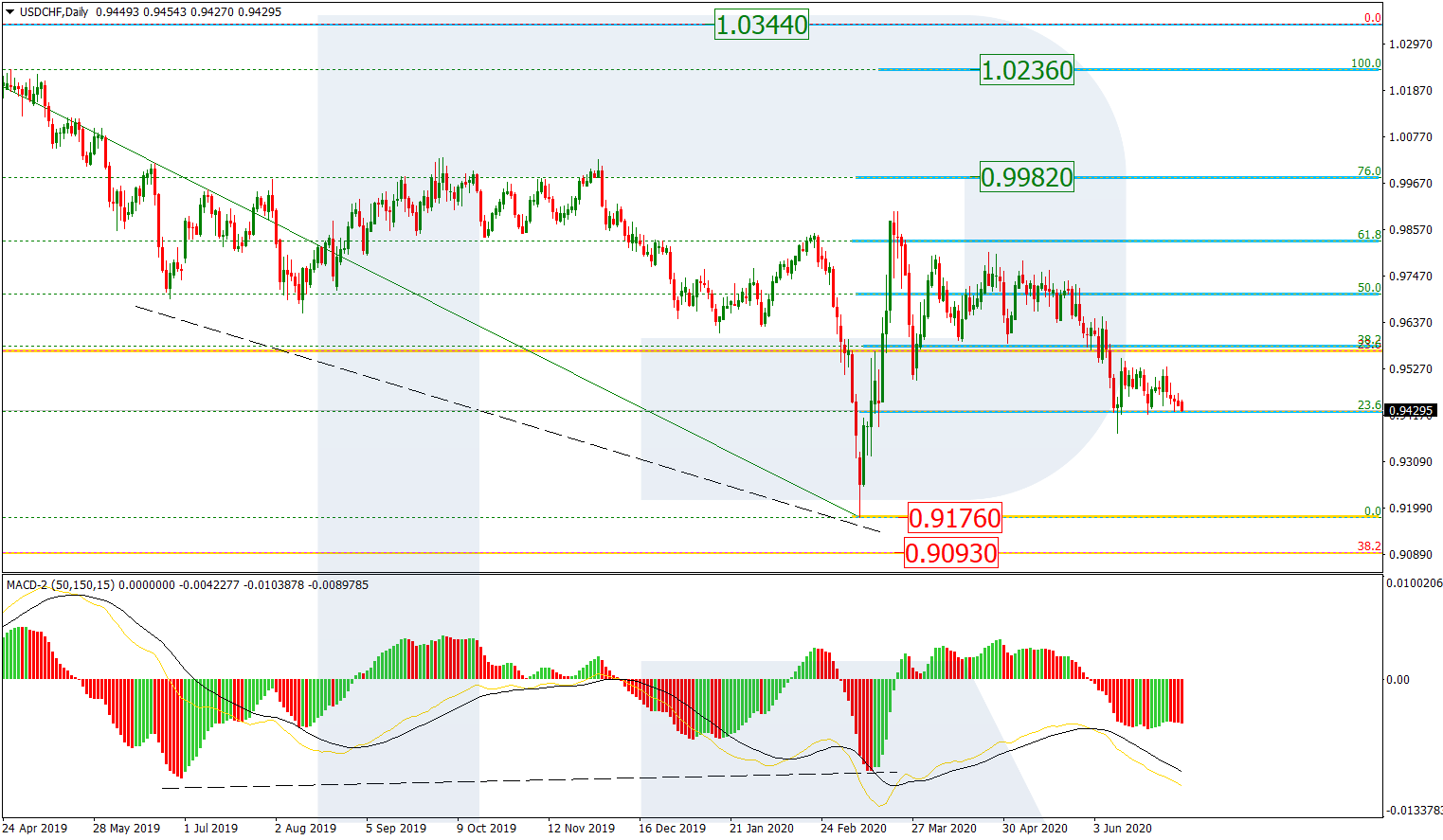

USDCHF, “US Dollar vs Swiss Franc”

As we can see in the daily chart, after quickly reaching 61.8% fibo, USDCHF has returned to 61.8% fibo. Although the current dynamics is descending, the previous divergence may not be over yet, which means that the pair still has a chance to form a new rising impulse towards the mid-term 76.0% at 0.9982 and then the fractal high at 1.0236.

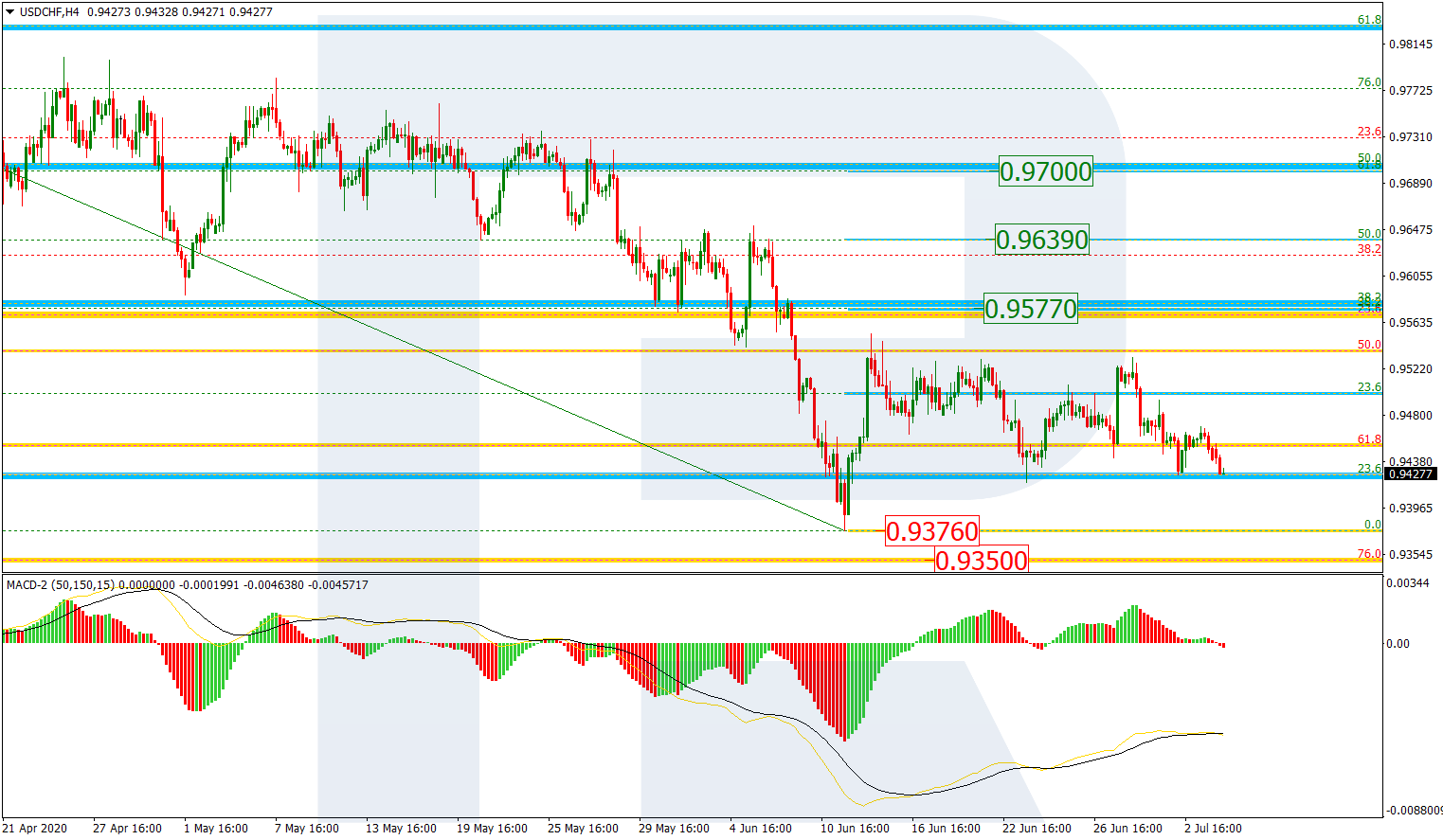

The situation in the H4 chart hasn’t changed much over a week. The chart is still showing attempts of the price to break a short-term correctional Triangle pattern to the downside, which means that the market wants to continue the bearish tendency towards the mid-term 76.0% fibo at 0.9350 after breaking the low at 0.9376. However, as usual, one shouldn’t exclude another scenario, according to which the instrument may form a new rising impulse after finishing the correction and testing the low. In this case, the asset may move towards 38.2%, 50.0%, and 61.8% fibo at 0.9577, 0.9639, and 0.9700 respectively.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.