Most Asian assets are set to end the week on a risk-off note, with regional currencies now weaker against the US Dollar, while major stock indices tracked overnight losses on Wall Street. Chinese stocks are taking a breather from their rich vein of form of late, with the Shanghai Composite index and the CSI 300 unable to build on 8 consecutive days of advances. Still, the CSI 300 is trading around a 5-year high, while the Shanghai composite index remains at its highest levels since 2018. The two benchmarks have posted a month-to-date surge of around 15 percent respectively, which far exceeds the MSCI Asia Pacific index’s five percent climb so far in July. US futures are in the red at the time of writing.

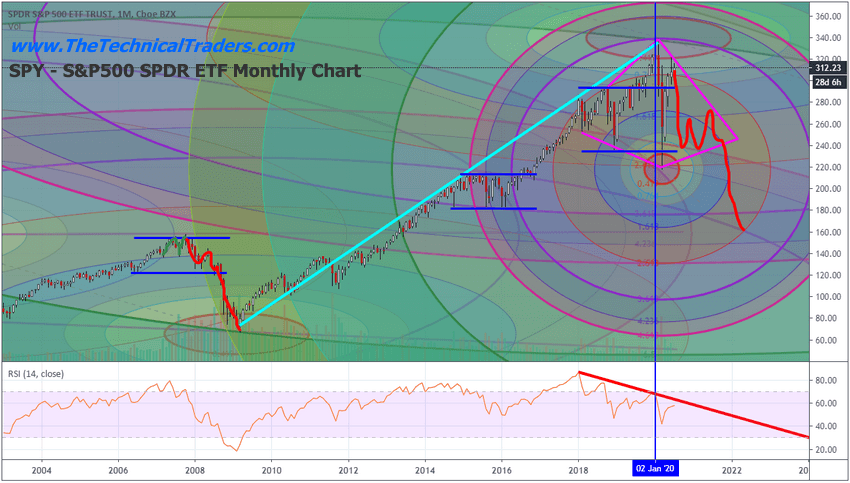

While global equities have blissfully ignored the deteriorating economic conditions around the world in the previous quarter, the moment of reckoning could arrive when the US earnings season kicks off next week. The second-quarter results are set to lay bare the pandemic’s impact to a greater extent compared to the previous quarter’s figures, and could prove to be one of Wall Street’s worst. It remains to be seen whether market participants have the stomach to digest such despairing data.

The forward guidance out of these companies however could have a more pivotal role in dictating the near-term market sentiment. After all, investors are desperate for further clarity, considering that four out of five S&P 500 listed companies withheld guidance during the last earnings season. That suggests that the 40 percent climb in the S&P 500 since March 23 has been largely fuelled by blind optimism.

Should greater clarity start feeding through over the coming weeks, that could be the catalyst to shake the S&P 500 out of its tight 230-point range that’s been adhered to since June. Still, given the unprecedented amount of stimulus measures already at work across major economies, one shouldn’t expect any pullback in risk assets to be overly drastic. On the flip side, should the upcoming earnings season bring with it greater optimism surrounding the post-pandemic recovery, that is set to give equity bulls the green light to chase further gains.

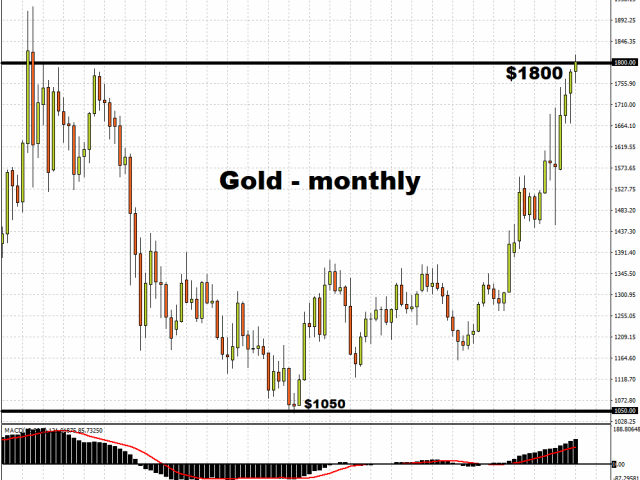

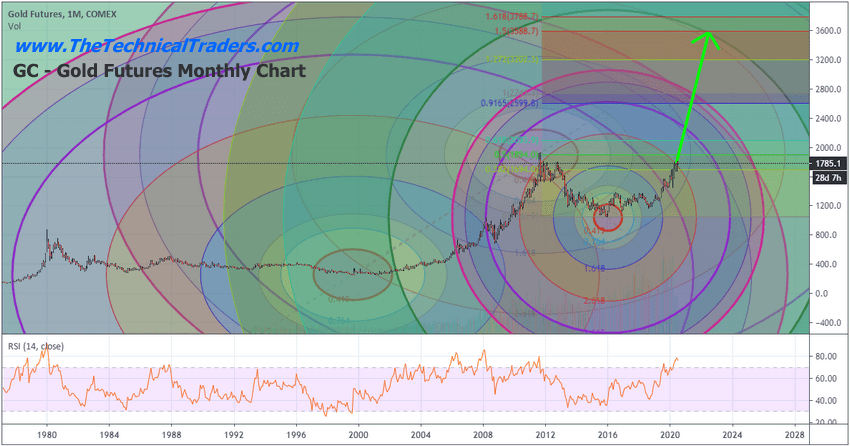

Gold remains at highest levels since 2011

Gold remains at highest levels since 2011

Meanwhile, investors are clearly hedging their exposures to risk, even though Gold prices have dipped below the psychologically-important $1800 level. With Gold on the cusp of five consecutive weeks of gains, the precious metal is reflecting the dynamics between hopes surrounding the global economic recovery and enduring concerns over the persistent nature of the pandemic.

Given the subdued US real yields and the stubborn risk aversion in the markets, this is clearly a supportive environment for Gold, with a repeat of the September 5, 2011 record closing price of $1900.20 in its sights.

Spot Gold could even set a new record high this year if another bolt of risk aversion courses through the markets, especially if the green shoots of the global economic recovery are snuffed out by another round of lockdowns across major economies, or if severe doubts are cast on global policymakers’ ability to support their respective economies. The threat of spiking geopolitical tensions is also lurking in the background, and if it materializes, could serve as another major tailwind for Bullion.

On the other hand, a vaccine would send the all-clear signal for risk assets at the expense of the yellow metal. More concrete signs that the global economy is set for a swifter-than-expected recovery could also pare some of Gold’s recent gains.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Equity markets are in red currently after a mixed session Thursday. US markets ended mostly lower yesterday after Labor Department data showed that 1.3 million Americans filed for first-time unemployment benefits last week.

Forex news

Currency Pair

Change

EUR USD

-0.5%

GBP USD

+1.2%

USD JPY

-0.36%

The Dollar strengthening is intact today ahead of inflation report scheduled for 16:30 CET today. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.3% Thursday as US Labor Department data showed 1.3 million Americans filed for first-time unemployment benefits when 1.4 new applications were expected. Both GBP/USD and EUR/USD reversed their climbing yesterday despite Germany’s statistics office report euro-zone’s largest economy’s trade surplus rose more than expected in May. AUD/USD joined USD/JPY’s continued sliding yesterday with both pairs lower currently.

Stock Market news

Indices

Change

Dow Jones Index

-0.77%

GB 100 Index

-0.92%

Nikkei Index

-1.21%

Hang Seng Index

-1.99%

Futures on three main US stock indexes are edging lower currently after ending mixed Thursday after 7-2 Supreme Court decision ruling that a New York prosecutor could have access to President Donald Trump’s tax returns. The three main US stock indexes recorded returns ranging from -1.4% to 0.5% as data showed 32.9 million Americans were receiving unemployment benefits in the third week of June. European stock indexes are pulling back today after ending higher Thursday. Asian indexes are all lower today led by Heng Seng as China’s regulators cracked down on margin financing and state funds said they would reduce equity holdings.

Commodity Market news

Commodities

Change

Brent Crude Oil

-1.1%

WTI Crude

-1.18%

Brent is edging lower today. Oil prices fell yesterday after Energy Information Administration reported that US crude inventories rose by 5.7 million barrels for the week ended July 3. The US oil benchmark West Texas Intermediate (WTI) futures ended lower yesterday: August WTI fell 3.1% and is lower currently. August Brent crude closed 2.2% higher at $42.35 a barrel on Thursday.

Gold Market News

Metals

Change

Gold

-0.06%

Gold prices are extending losses today . August gold ended 0.9% lower at $1803.80 an ounce on Thursday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Updates on Sorrento Therapeutics’ two coronavirus-related products are provided in an H.C. Wainwright & Co. report.

In a July 6 research note, H.C. Wainwright & Co. analyst Ram Selvaraju reported the status of Sorrento Therapeutics Inc.’s (SRNE:NASDAQ) vaccine and antibody test for COVID-19.

“We continue to believe that Sorrento may be positioning itself as a leader in addressing the pandemic, with multiple potential therapeutic approaches in its pipeline,” he commented.

As for its coronavirus vaccine T-VIVA-19, the California-based therapeutics developer published initial preclinical study results that Selvaraju described as “encouraging.” In the trial, mice were injected intramuscularly or intravenously once with Sorrento Therapeutics’ vaccine and three weeks later, received a follow-up booster shot.

The initial immunization created antibodies against the SARS-CoV-2 protein in all mice within the first week of administration, and the booster enhanced those antibodies. The antibodies that developed wholly prevented virus infection, as determined via cell cultures, in 80% of the subjects.

Regarding Sorrento Therapeutics’ COVID-19 antibody test COVI-TRACK, Selvaraju reported that it is currently being evaluated for emergency use authorization, which it is expected to be granted in the coming weeks. Subsequently, the biopharma will make it available for distribution to clinical testing sites around the world, leveraging its existing relationships, such as with Cardinal Health, in doing so. At the start, Sorrento expects to manufacture up to 5 million test kits per month.

Selvaraju presented five reasons why COVI-TRACK is a competitive testing solution. It produces results quickly, in about eight minutes, and detects immunoglobulin G and immunoglobulin M antibodies. The test’s specificity, the ability to not generate false positives, and its sensitivity, the ability to not generate false negatives, exceed the 95% and 90% standards, respectively, when many of the existing tests “are woefully inaccurate,” the analyst noted. Lastly, Sorrento has savvy and experience with antibodies, Selvaraju wrote.

The need for COVI-TRACK “is likely to be healthy” and “persist for the foreseeable future,” indicated Selvaraju. As such, in the U.S. alone, the vaccine could generate $50 million-plus a year for Sorrento Therapeutics.

Selvaraju pointed out that in other recent news, the company completely prepaid both of its outstanding term loans, one for $100 million and another for $20 million. Now debt free, the biopharma should be better positioned going forward for “operational flexibility and potential strategic combinations.”

H.C. Wainwright has a $24 per share 12-month price target on Buy-rated Sorrento Therapeutics; today, the stock is valued at about $7.31 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from H.C. Wainwright & Co., Sorrento Therapeutics Inc., Company Update, July 6, 2020

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Raghuram Selvaraju, Ph.D., certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of Sorrento Therapeutics, Inc. (including, without limitation, any option, right, warrant, future, long or short position).

As of May 31, 2020 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of Sorrento Therapeutics, Inc.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The firm or its affiliates received compensation from Sorrento Therapeutics, Inc. for non-investment banking services in the previous 12 months.

The firm or its affiliates did receive compensation from Sorrento Therapeutics, Inc. for investment banking services within twelve months before, and will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

H.C. Wainwright & Co., LLC managed or co-managed a public offering of securities for Sorrento Therapeutics, Inc. during the past 12 months.

The Firm does not make a market in Sorrento Therapeutics, Inc. as of the date of this research report.

Alvopetro Energy’s “important milestone” and expansion potential are covered in a Mackie Research Capital Corp. report.

In a July 7 research note, Mackie Research Capital Corp. analyst Bill Newman reported that Alvopetro Energy Ltd. (ALV:TSX.V; ALVOF:OTCQX) “achieved an important milestone” by connecting Brazil’s Caburé to Bahiagás’ distribution network and commencing its first physical sales production from the natural gas field.

“This is an important milestone as the company is now generating free cash flow that can be reinvested into other growth opportunities. We expect the stock to trade up on the news,” Newman stated.

“Natural gas and revenue are flowing,” Newman added. “With the production facilities in place, new discoveries can be quickly monetized.”

The analyst noted that Alvopetro ramped up its natural gas production on July 6 to 10.6 million cubic feet per day (10.6 MMcf/d). For each million British thermal units of gas it sells, it will receive US$5.13 this month.

Revenue of US$5.9 million is expected in H2/20, Newman highlighted, with a near tripling to US$16.7 million in 2021. The Calgary-based firm is expected to use the cash flow for other growth opportunities its portfolio of assets presents.

Newman also pointed out that Alvopetro intends to expand production to 17.6 MMcf/d, the total capacity of its transfer pipeline and gas treatment facility. To do so, the company plans to start a drill program, perhaps in late 2020.

Mackie has a Speculative Buy rating and a CA$1.65 per share target price on Alvopetro. In comparison, the stock is now trading at CA$0.78 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Alvopetro Energy. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Mackie Research, Alvopetro Energy Ltd., Update, July 6, 2020

RELEVANT DISCLOSURES APPLICABLE TO COMPANIES UNDER COVERAGE 1. None Applicable. 2. Relevant disclosures required under Rule 3400 applicable to companies under coverage discussed in this research report are available on our web site at www.mackieresearch.com.

ANALYST CERTIFICATION Each analyst of Mackie Research Capital Corporation whose name appears in this report hereby certifies that (i) the recommendations and opinions expressed in this research report accurately reflect the analyst’s personal views and (ii) no part of the research analyst’s compensation was or will be directly or indirectly related to the specific conclusions or recommendations expressed in this research report.

With a promising hit and the rise in prices for both gold and copperand indications of more to comePeter Epstein of Epstein Research believes this explorer has potential for “an exciting outcome.”

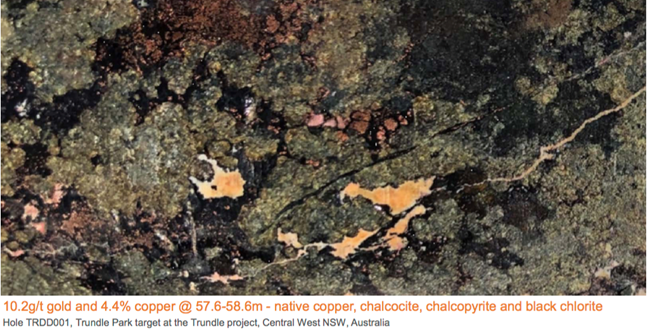

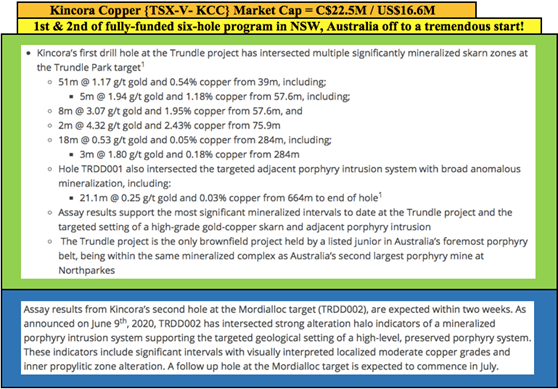

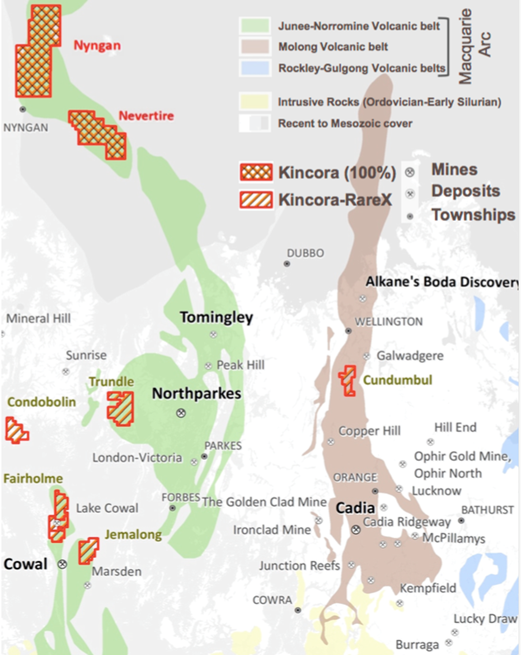

Investors in Kincora Copper Ltd. (KCC:TSX.V) have had to be patient in allowing management to explore for really big prizes in Mongolia and New South Wales, Australia. This week we learned that it was well worth the wait. On July 6, the company announced an excellent drill result intersecting multiple mineralized skarn zones at its Trundle Park target in Australia’s foremost porphyry region [see July corporate presentation].

The results are noteworthy for at least three reasons: there’s considerable near-surface, high-grade mineralization; as the first of six holes, even better assays could follow (leveraging knowledge gained from this result); and further evidence of an adjacent porphyry system was found.

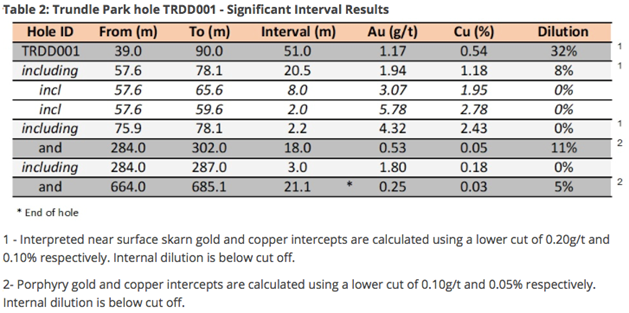

By far the best mineralization is from 39 meters (39m) to 90m depth. This 51m interval hit 1.17 g/t Au + 0.54% Cu. Included in the 51m is one meter, from 57.6m, of 10.4 g/t gold (Au) + 4.4% copper (Cu). See image below.

51m, less than 90m deep: Very good grades + a porphyry teaser at depth

At current gold and copper prices of US$1,793/ounce and US$2.78/lb., this is an in-situ rock value of ~US$100 = ~CA$135.5/tonne. In gold terms, it’s 1.75 g/t Au equivalent (equiv.). In copper terms, 1.64% Cu equiv. Note: these strong grades will not be indicative of the overall deposit. However, this hole suggests the potential for a nearer-term, standalone open pit.

That’s the sexy part of the assay, the hole also intersected a targeted adjacent “porphyry intrusion system” with broad anomalous mineralization. This assay delivered the most significant intervals to date. Management notes that Trundle is the only brownfield project held by a listed junior in Australia’s foremost porphyry district, the Lachlan Fold Belt (LFB).

John Holliday, technical committee chair, and Peter Leaman, senior VP of Exploration commented: “We are extremely pleased and excited by the results of this first hole. It’s not often one sees such high grades near surface within a porphyry environment. Assay results prove previously announced visual interpretations of multiple zones of significant gold and copper mineralization. This supports the skarn being a standalone target at depths and intervals often mined by open cut and underground methods. . .

“. . .These results from this first hole at the Trundle target, plus visual indications from the second hole 8.5 km north at the Mordialloc target, are very encouraging. The Trundle project appears to sit within the interpreted Northparkes Intrusive Complex, placing Kincora in a unique global setting as the only listed junior exploring a large system in a brownfield field setting.”

Breaking: Dr. Copper says “reports of my death are greatly exaggerated”

The timing of the press release could hardly be better. Copper has bounced back strongly from US$2.10/lb. in mid-March to US$2.78/lb., +32%. Dr. Copper has spoken loud and clear. He/she believes that, even if temporarily slowed, the global electric transportation and green energy revolutions are alive and well.

Dr. Copper is leaning toward a V-shaped recovery. Others seem to agree, look no further then Tesla’s >CA$300 billion valuation for evidence of market sentiment on electric vehicles!

In addition to copper’s irreplaceable role in electric transportation and renewables, copper demand will increase if/when the world’s major economies embark on infrastructure massive spending sprees. Giant infrastructure builds/rebuilds(bridges, tunnels, airports, stadiums, etc.) are highly copper-intensive.

Even if copper demand is tepid, the supply response to the pandemic has been dramatic. Reduced production from countries such as Chile, (where per capita COVID-19 cases are among the worst in the world), Peru, the Democratic Republic of Congo and others, will last several more quarters. Chile is by far the largest producer, larger than the next three copper-producing countries combined in 2019.

It took three paragraphs to sound off on copper, but just one on gold. For years, gold bugs have pointed to fiat currencies, deficit spending, debt issuance, money printing, imminent inflation, etc., pushing gold to US$5,000 or US$10,000/oz. “next year!!” Next year has finally arrived. I’m not predicting US$5,000+/oz. anytime soon, but gold fundamentals are as strong as ever. Bull markets in precious metals last years, not months. Gold is up 31% from its US$1,368/oz. low of March.

A single hole, but a tonne of de-risking as exploration models validated

Turning back to this hole at Trundle, it is the first of two each at three targets in an ongoing 3,800m program. This single assay delivered meaningful de-risking of the Kincora story. Positive visual inspection of the core was verified by strong results that largely confirmed the team’s targeted geological model and exploration strategy. This is critical, because a fear investors have with junior miners is that even talented management teams will run out of money before finding anything promising.

That risk has been moderately reduced (but not eliminated). If results from hole #2 at the Mordialloc target, 8.5 kilometers north of hole #1, are as good or better, Kincora’s valuation might look undervalued compared to peers such as Magmatic Resources (MAG:ASX), Sky Metals (SKY:ASX) and Stavely Minerals (SVY:ASX) that have an average market cap of ~CA$80 million (CA$80M) versus ~CA $25M for Kincora.

To be clear, none of these companies measure up to Alkane Resources Ltd.’s (ALK:ASX; ANLKY:OTCQX) CA$700M market cap, but one cannot rule anything out at this early stage. So far there are just two winners of six holes, but we now know there’s smoke at Trundle. Will any of the next four holes find fire?

Let’s take a step back to revisit the bigger picture. High-grade, near-surface skarn mineralization is exciting, but the pot of gold/copper at the end of the rainbow is one or more porphyry deposits. Results from the first hole, and anticipated results from hole #2, represent a meaningful step closer to the pot of gold/copper.

Director John Holliday has said on the record that he thinks after Alkane’s Boda project, Kincora has the best porphyry play in the district. Likewise, CEO Sam Spring believes Kincora is the leading pure-play porphyry explorer in Australia’s LFB. Make no mistake, they’re biased!

Still, unlike many junior gold/copper districts around the world, there are relatively few juniors active in the area. I mentioned three, there are about a dozen with meaningful flagship projects in the region. By contrast, Canada’s Golden Triangle has three dozen, or more.

Readers are invited to view Kincora’s July corporate presentation. On pages 29 and 30, management places their drill result into context. While the first drill hole at Trundle did not contain the highest grades or widest intercepts, its high-grade mineralized zones are closer to surface than some peers. And, this is just the first hole!

The skarn and porphyry intrusion system setting intersected is common among large porphyry systems. For example, in the Macquarie Arc, the Big and Little Cadia skarns at Cadia were important to the discovery of multiple adjacent “causative intrusions and deposits” that make up the largest porphyry system in Australia. Kincora’s strategy is to drill to depths at which porphyries at Cadia, Northparkes, Cowal and Boda are situated.

Management, Board and Technical Team: Now the hard part

The management, board, technical team and advisers share in this initial exploration success. But, where does this leave the company? I think the considerable strength of Kincora’s team will be amplified in coming months as it leverages the valuable knowledge gained from the first six holes. Kincora found smoke at Trundle, it’s now trying to locate the porphyry fire.

CEO Spring provided me with this exclusive quote: “What we intersected near-surface in hole #1 is a skarn. What we’re testing for in hole #2, and at the bottom of hole #1, is a porphyry (the presumed source of mineralization in the skarn). At the Mordialloc target, hole #2, we don’t see a skarnwe knew that only a porphyry was the target. What we intersected in hole #2 suggests that we’re closer to the core of a porphyry system (which, if you hit, can easily be a company maker) than in hole #1, without yet hitting it.”

While some investors are rightfully congratulating the team, I suggest that their jobs have only just begun. Now that we know there’s probably something meaningful (although not necessarily economic) at Trundle, the pressure is on to advance the project efficiently and cost effectively. This is where tremendous experience and skill sets come into play.

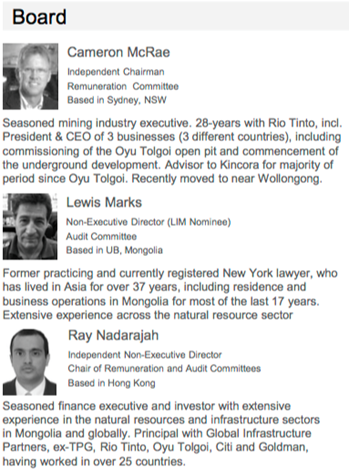

In looking at the bios, we have Mr. McRae, with nearly 30 years’ at Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK), president and CEO of three of Rio’s segments. Mr. Lehman has >40 years’ experience, mostly with BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK), including Tier 1 discoveries under his belt. He’s a world-renown expert in copper and gold deposits. Mr. Holliday, based in New South Wales (NSW), has >30 years’ with BHP and Newcrest Mining Ltd. (NCM:ASX)a principal discoverer of the world-class Cadia copper-gold porphyry in NSW. Very few, if any, are better suited to lead Kincora’s technical team.

CEO Sam Spring has been a senior exec at Kincora for eight years. Prior he held a number of positions including lead mining/metals analyst at Goldman Sachs and various roles evaluating, advising or negotiating merger and acquisition (M&A) activities in multiple jurisdictions. Readers are encouraged to also review the bios of other highly talented contributors above and below. This is a group who have done this before; discovered, developed, permitted, constructed, funded and commissioned mines.

I doubt Kincora is going to ride this horse across the finish line, but the experts working on Trundle, and Kincora’s other high-profile targets in NSW, understand exactly what potential acquirers are looking for. They’ve created vast shareholder wealth in past endeavors. With continued successes they’re on track to potentially deliver another exciting outcome for Kincora Copper stakeholders.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Epstein Research Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Kincora Copper, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Kincora Copper are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Kincora Copper was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events and news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Sri Lanka’s central bank lowered its key interest rates for the fifth time this year as it seeks to lower lending rates further and encourage the financial system to “aggressively” lend to productive sectors of the economy to boost activity at a time of subdued inflation. The Central Bank of Sri Lanka (CBSL) cut its two key interest rates, the standing deposit facility rate (SDFR) and the standing lending facility rate (SLFR), by 100 basis points each to 4.50 percent and 5.50 percent, respectively. It is CBSL’s fifth rate cut this year and the deposit rate has now been cut by 250 basis points following earlier cuts in January, March, April and May. Todays rate cut is also the central bank’s 7th cut since May 2019, with the rate cut by a total of 350 basis points since then as it continues to stimulate the take-up of credit by businesses that were first hurt by the 2019 Easter Sunday bombings and then the COVID-19 pandemic. The central bank said it would continue to monitor domestic and global economic conditions and “take further measures to ensure that the intended outcomes of already implemented policies are realized.” Although the central bank expects an economic rebound in the second half of the year, after the economy was “severely affected” during the second quarter, it said it was imperative to introduce growth promoting and confidence enhancing structural reforms to foster high and sustainable growth in the medium term. Sri Lanka’s gross domestic product slowed to annual growth of 2.0 percent in the first quarter of this year from 2.4 percent in the previous quarter and in the month of May the country had no tourist arrivals, as in April, as all passenger arrivals were terminated from mid-March to prevent the spread of the coronavirus. As in previous months, the central bank called on financial institutions to fully pass on the cumulative cuts of 250 basis points interest rates, adding it also expects banks to use the additional liquidity freed up by its cut to the reserve ratio of a total of 300 points to boost lending to productive sectors of the economy. “However, further space remains for market lending rates to adjust downwards commensurate with the series of easing measures taken by the central ban thus far during the year,” CBSL said. Reflecting authorities’ measures to stem the outflow of currency, Sri Lanka’s rupee has strengthened since mid-April after falling in March and was trading at 185.9 to the U.S. dollar today, down 2.3 percent this year. Sri Lanka’s reserves were US$6.7 billion at the end of June, enough for 4.2 months of imports. Sri Lanka’s inflation rate eased slightly to 3.9 percent in June from 4.0 percent in May.

The Central Bank of Sri Lanka issued the following statement:

“The Monetary Board of the Central Bank of Sri Lanka, at its meeting held on 08 July 2020, decided to reduce the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) of the Central Bank by 100 basis points each, to 4.50 per cent and 5.50 per cent, respectively. The Board arrived at this decision with a view to inducing a further reduction in market lending rates, thereby encouraging the financial system to aggressively enhance lending to productive sectors of the economy, which would reinforce support to COVID-19 hit businesses as well as to the broader economy, given conditions of subdued inflation. The spread of the COVID-19 pandemic has significantly impacted near term growth prospects globally, while available indicators for Sri Lanka also suggest that economic growth is likely to have been severely affected during the second quarter of 2020. Although a rebound is expected during the second half of the year with the support of monetary and fiscal stimulus measures, the introduction of growth promoting and confidence enhancing structural reforms is imperative to foster high and sustainable economic growth over the medium term. On the external front, the trade deficit is estimated to have narrowed during the first five months of 2020, with the contraction in imports outweighing the contraction in exports. Reflecting the impact of measures taken to stem foreign currency outflows, the Sri Lankan rupee, which remained volatile briefly from mid-March to mid-April 2020, recorded a notable appreciation thereafter. Gross official reserves stood at US dollars 6.7 billion by end June 2020, sufficient to cover 4.2 months of imports.

Market interest rates continued to decline, reflecting the impact of policy rate reductions and the surplus liquidity in the domestic money market. However, further space remains for market lending rates to adjust downwards commensurate with the series of easing measures taken by the Central Bank thus far during the year. Despite high levels of surplus liquidity available to banks, credit extended to the private sector contracted significantly in May 2020. However, credit extended to the private sector is likely to pick up in the period ahead, supported by the expected sharp reduction in lending rates and highly concessional credit schemes introduced to support COVID-19 hit businesses. Meanwhile, the notable increase in credit to the public sector drove the increase in domestic credit as well as the overall monetary expansion during the first five months of 2020. In consideration of the need to support a rapid recovery of the economy, the Monetary Board, at its meeting held on 08 July 2020, decided to reduce the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) of the Central Bank by 100 basis points each to 4.50 per cent and 5.50 per cent, respectively, with effect from 09 July 2020. The Monetary Board wishes to strongly reiterate that all financial institutions led by licensed commercial banks (LCBs) must pass on the full benefit of the cumulative reduction of 250 basis points in policy interest rates thus far during the year without delay. LCBs are also expected to release to the private sector borrowers the enhanced levels of liquidity effected by the reduction of the Statutory Reserve Ratio (SRR) by 300 basis points thus far during the year, which has also reduced the cost of funds of banks. Such additional liquidity must be used to lend to productive sectors of the economy, along with concessionary credit schemes already announced by the Central Bank to help needy sectors of the economy. The Central Bank will continue to monitor domestic and global macroeconomic and financial market developments and take further measures to ensure that the intended outcomes of already implemented policies are realised.” www.CentralBankNews.info

Is everyone familiar with the bet between Julian Simon and Paul Ehrlich? Ehrlich wrote a book titled The Population Bomb. He held a pessimistic view of the future, in which population growth would outstrip resources (essentially the same as Thomas Malthus).

Simon disagreed. So in 1980, they made a famous bet. Ehrlich thought that the real cost of commodities would be higher in 10 years. Simon said they would be lower.

They picked a group of five metals, to watch their prices. And made their bet, just at the end of the cycle of rising interest rates and rising prices that had begun after WWII.

The majority of the decade occurred under the falling cycle which still prevails today. It is likely that neither of them were aware of the correlation between interest rates and prices observed by Gibson 57 years prior to their bet. In any case, in 1980, all they had experienced for decades was the relentless rise of both. So Paul Ehrlich would seem to have taken a very conventional view. And Simon would be the bold contrarian.

Between 1980 and 1990, three of the metals fell in price. But the bet was not based on what people call the nominal price. This is, you know, the actual price paid by actual buyers to actual sellers who actually mine and smelt actual metal. It’s something else.

Primer in Monetary Pseudoscience

The value of the dollar is falling, and therefore economists seek a way to adjust the dollar. If such a way could be found, then one could compare the inflation-adjusted 1980 dollar to the inflation-adjusted 1990 dollar. Or the 1900 dollar. Or the 2020 dollar.

It seems a simple idea, as pseudoscience often does. It’s tempting and convenient. You just have to design a basket of consumer good. You just presume that these goods are a proper and representative measure of the things people buy.

Never mind that even the advocates of this approach do not agree on which goods should be included and which excluded.

Also, you ignore when, say, horse-drawn buggies are replaced by cars and hence there is no more need for buggy whips. Plus don’t mention improvements in the goods themselves. A 1980 car is not remotely comparable to a 2020 car. The 1980 car was before even that beacon of mediocrity known as the “K Car”.

Anyways, pay no need to this cognitive mess. And heed not your third grade math teacher, who said that you cannot add apples to oranges. Instead, be mesmerized by modern monetary magicians who insist that you absolutely can, if you’re making an index which includes apples and oranges and fuel and cars.

You just need to take a weighted average of the prices of the arbitrarily-chosen goods. Oh, by the way, you have to assume that consumer goods have constant real value. This is necessary to make the next Grand Canyon leap to the notion that consumer goods prices can be used to adjust the unit of measure of value itself.

Oh. Sorry. We forgot one more assumption: that monetary debasement is a scalar; that is, there is only one dimension. One way that debasement affects the dollar. And therefore we need only look at one variable. Consumer prices.

Don’t worry, boys and girls, we are doing science!

With those unwarranted assumptions and bogus inferences behind us, we have a consumer price index (CPI). We’re ready for the part of the science experiment that is guaranteed to amaze the parents and younger siblings of any 8-year old with a science experiment kit. He dips a white strip of paper into a glass containing clear liquid, and… presto chango abracadabra… the strip turns blue!

We look at the year-on-year change of the CPI, and adjust the dollar accordingly. For example, if CPI doubled between 2021 and 2022, then the 2022 dollar is adjusted to be worth half of the 2021 dollar.

The Cash Value

There are two reasons why people promote junk science. One is that it’s easier than doing real science. The other is that it promotes a view they arrived at non-scientifically. They use pseudoscience to bolster their financial interests or political policies.

While it is certainly true that this attempt to adjust the dollar is easy and tempting, that does not fully explain the prevalence and vehemence of this approach. It would be even easier to measure the dollar in gold (but that is the One Thing That Must Not Be Done).

Our monetary central planners—and their court-economists—prefer to redirect everyone’s attention away from the grave harms that come from their relentless counterfeiting of credit, and their endlessly falling interest rate. So monetary criticism is channeled into the relatively harmless pastime of consumer price obsession.

The Switcheroo

The Simon-Ehrlich bet hinged, not on the nominal prices of their selected commodities (metals), but on their real prices. That is, fictitious prices that no one buys or sells, based on the adjustment to the dollar which is based on changes in the CPI.

All five metals dropped in real terms. Simon won the bet. And everyone assumes the bet settled the debate between the two men. Not quite.

In the haste to find an easy way to adjust the dollar, those who would perform monetary science have overlooked a subtle but profound flaw in their methodology. And it fatally undermines the Simon-Ehrlich bet.

To see the mistake, let’s look at how consumer goods are manufactured. A major ingredient is commodities. Another major ingredient is energy—and the major ingredient in energy production is a commodity (e.g. oil). Consumer prices are heavily dependent on commodity prices.

To calculate the real prices of commodities, they are:

Starting with the nominal prices of commodities

adjusting these nominal prices

by adjusting for inflation the unit of measure itself, the dollar

which is done by measuring changes in the prices of consumer goods

that depend heavily on commodity prices!

Let that sink in. They want to calculate the real price of each commodity. So they adjust the dollar. The adjustment is based on the price of the goods made from the commodity.

It’s a self-referential calculation.

It should be clear that if you used a commodity price index to adjust the dollar (instead of the consumer price index), then it would show that real commodity prices are not changing at all.

This is because the dollar would be adjusted by precisely the amount that the nominal prices of the commodities changed, and therefore the new real price would be the same as the original nominal price.

With CPI used as the adjustor, real commodity prices do change. They change because commodities are not 100% of the cost of consumer goods. Generally, manufacturers become more efficient as they keep optimizing their businesses. Parts that were once made of metal, are replaced with plastic. Plastic parts can be made lighter, by making them thinner where strength is not needed.

Manufacturers are also improving their products, adding more features. Just compare a 2020 car to that 1980 car. The 2020 car does not weigh any more (it probably weighs less), so by this rough measure the present-day car does not use more commodities than the 1980 car. However, a much greater quantity of other ingredients go into it, such as engineering labor and manufacturing tools.

Meanwhile, regulators and taxinators are fighting this relentless drive to reduce ingredients and hence costs, by force the inclusion of more and more useless ingredients.

These are ingredients that consumers do not value, and often do not even know about. For example, expanding employee bathrooms to be ADA-compliant. Or the legal fees related to audits, licenses, and regulatory inquiries.

Economists blithely say that the dollar has lost purchasing power, but the dollar is actually buying more than ever before. It’s just buying different things, such as compliance officers.

The Simon-Ehrlich bet hinged on the proportion of the cost of consumer goods that comes from the raw commodity ingredient cost relative to the other ingredients including useless ingredients.

In other words, if useless ingredients forced onto retailers and manufacturers grow into a larger and larger percentage of the consumer price of the goods, then by definition raw commodities are a smaller percentage of the consume price.

And as an artifact of this shift in proportion, the inflation-adjusted price of commodities is reduced from what it would be.

Julian Simon vs Paul Ehrlich

This is not what Julian Simon and Paul Ehrlich believed they were betting on. They thought they were betting on the ancient zero-sum fallacy. They thought they were settling the question of whether man’s reason increases productive capacity at a faster or slower rate than his libido increases the population.

For what it’s worth, we believe that reason wins hands-down. There is no question today that the quality of life is better in 2020 than it was in 1980. Perhaps we do not consume more commodities, or maybe we do, but we eat more and we have better-made and better-functioning products.

We have got to get monetary science out of its Medieval period. Today, most thinking about money is as scientific as thinking about astronomy was prior to Copernicus. In the five centuries since he taught the heliocentric model, the methods of science were developed. They desperately need to be applied to money and credit.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Having broken the $1800 level, the yellow metal continues to push higher this afternoon. The Dollar has recovered from hitting near one-month lows but is subdued with risk appetite fairly mixed. Initial jobless claims and continuing claims came in better than expected, but the former still remain above the one million level for the sixteenth straight week.

Chinese markets continued their march ever higher overnight, while German stocks are showing a healthy gain on decent earnings data. The greenback’s negative correlation with equities remains with stocks well supported on dips. Rising infections and now fatalities in the US are seemingly ‘white noise’ to markets pumped up on monetary and fiscal steroids.

Speaking of which, Sterling has taken a liking to yesterday’s new fiscal support from UK Chancellor Sunak and is the leading major on the day. The total was more than expected, even if we doubt it will get to the £30 billion headline figure. However, Brexit talks loom large as a major headwind going into the Autumn, although the bar is very low to some kind of agreement.

GBP liking ‘Rishi dishy’

Price action is king right now with momentum firmly upwards as cable pushes into its fifth consecutive day in the green. We are currently trading just above the two April highs in the mid-1.2640s, so need to consolidate above here ahead of the next resistance around the 200-day moving average at 1.2686. This may slow gains if prices can get anywhere nearer to the June high north of 1.28.

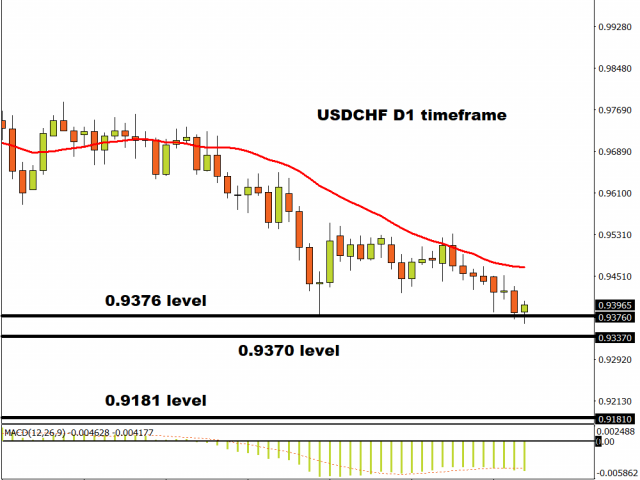

USD/CHF pushing lower towards cycle low

The Swissie is one of the top performing major currencies this month and USD/CHF broke sharply lower again yesterday on its way towards the 0.9376 June low.

A close below this level should see more downside as the June ‘hammer’ candle is a significant pivot. Next major support is at 0.9337 with the five-year low resting below at 0.9181.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

– Yes, we certainly live in interesting times. This, the last segment of our multi-part article on the current Q2 and Q3 2020 US and global economic expectations, as well as current data points, referencing very real ongoing concerns, we urge you to continue using common sense to help protect your assets and families from what we believe will be a very volatile end to 2020. If you missed the first two segments of this research article, please take a moment to review them before continuing.

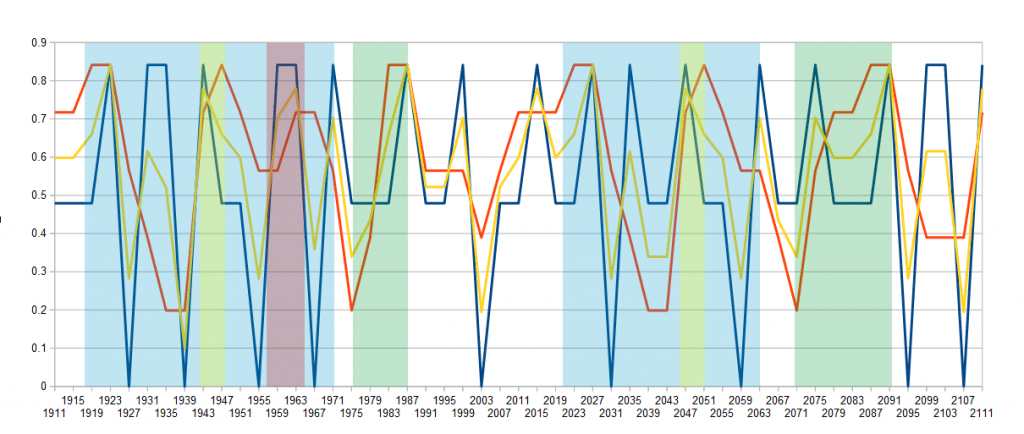

On May 24th, 2020, we published this research article related to our super-cycle research. It is critical that you understand what is really happening in the world as we move through these major 21 to 85+ year super-cycles and apply that knowledge to the data we have presented in the first two segments of this research post. Within that article, we quoted Ray Dalio from a recent article published related to his cycle research.

“In brief, after the creation of a new set of rules establishes the new world order, there is typically a peaceful and prosperous period. As people get used to this they increasingly bet on the prosperity continuing, and they increasingly borrow money to do that, which eventually leads to a bubble. As prosperity increases the wealth gap grows. Eventually, the debt bubble bursts, which leads to the printing of money and credit and increased internal conflict, which leads to some sort of wealth redistribution revolution that can be peaceful or violent. Typically at that time late in the cycle, the leading empire that won the last economic and geopolitical war is less powerful relative to rival powers that prospered during the prosperous period, and with the bad economic conditions and the disagreements between powers, there is typically some kind of war. Out of this debt, economic, domestic, and world-order breakdowns that take the forms of revolutions and wars come new winners and losers. Then the winners get together to create the new domestic and world orders.”

That rather chilling statement suggests one thing that we all need to be aware of at this time: what the current and future economic cycles will likely present and how the world will navigate through this process of a cycle transition.

In our opinion, the massive cycle event that is taking place may not disrupt world order as Mr. Dalio suggests. There is a very strong likelihood that credit/debt processes may become the “collateral damage” of this cycle transition, but not much else changes. The world order and powerful nations across the globe are keenly aware that starting WWIII because of a credit/debt crisis is not in anyone’s interest. The world has enough capability to address these concerns without blowing the planet to pieces in the process.

Our super-cycle research suggests we have entered a period that is very similar to 1919~1920 – a “roaring good time” most likely has already extended beyond reasonable levels. Our research suggests a massive peak in cycle events near 2023~24 after an already substantial support cycle from 2007~08 to 2023~24. This span of time, roughly 17 years, is very likely to be a blend of the Unraveling & Crisis phases of the super-cycle. We believe the broader Crisis phase will continue to transition throughout a span of time lasting well into 2031~2034. This suggests we may have another 11 to 15+ years of a massive unwinding cycle throughout the globe.

SUPER-CYCLE RESEARCHER DATA FROM OUR RESEARCH TEAM

Our research team believes the COVID-19 virus event sent these super-cycles into Warp-Speed recently. The US stock market was poised to rally early in 2020 and may have experienced a multi-year rally had it not been for the COVID-19 disruption that took place in Mid-February. The destruction of the economy related to the COVID-19 shutdown is still playing out. Recent news suggests 41% of businesses that closed on Yelp have shut down permanently. Now, consider that this means for consumers and local governments related to earning and revenue capabilities? Workers have been fired and have completely lost earnings capabilities. Business owners now face credit/debt issues and possible bankruptcies. Local governments have lost revenue from taxes, payroll, sales, and fees and permits. This destructive cycle continues until the economy has shed the “excess” within all segments of core economic function.

MORE DATA & MORE PREDICTIONS

Within the first two segments of this article, we’ve highlighted numerous data points and charts to more clearly illustrate the current global market environment. We have to consider the reality of what is happening on the ground throughout the world and, in particular, what is happening in the US and most major economies right now. If 30 to 40%, or more, of local businesses, are closing permanently, this suggests that 30 to 50% of tax revenues for local governments will also vanish. It also suggests that these displaced workers and business owners will need to find new sources of income/revenue over the next 12+ months.

As much as we would like to think a “V-shaped” recovery is highly likely, it’s not going to happen is 30 to 50% of the US economy is suffering at levels being reported currently. Yes, you could have investors pile into the US stock market because they believe the US economy is the most likely to develop a strong recovery in the future, but that will likely happen after the excess has been processed out of the economy through a business/credit contraction phase. The current stock market valuation levels seem to ignore the fact that consumer and business activity has likely collapsed by a minimum of 25 to 45% (or more) over the past 90+ days – and may not recover to levels anywhere near the early 2020 economic activity levels.

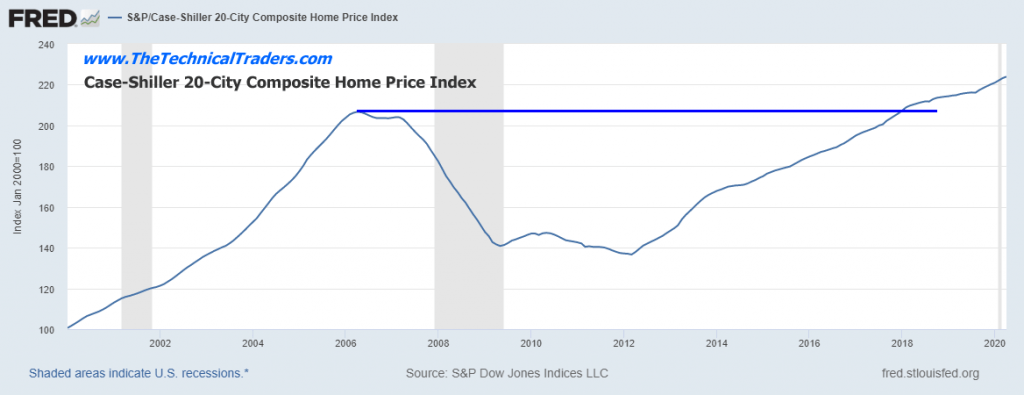

Still, if you listen to the news and watch the data related to the real estate market, you would think there has been no disruption in the US economy. Supposedly, homes are still selling quickly and the market is very robust. The Case-Shiller 20 city home price index is well above 220, the highest levels ever reached for this index. This suggests home prices have risen to levels that are likely 15% to 30% higher than the peak levels in 2006-2007 – yet we’ve just experienced a massive economic disruption across the globe where 25% to 45% (or more) of our economic earning and income capability has vanished. Read between the lines if you must – something doesn’t seem to be reporting valid data at the moment.

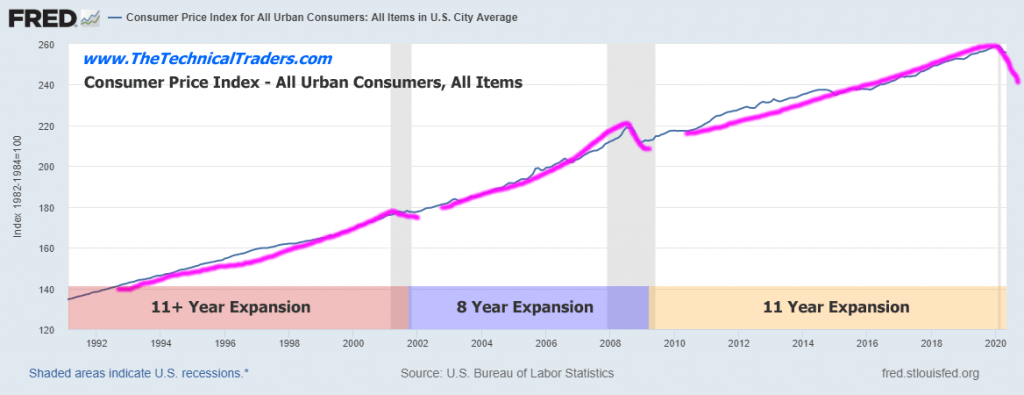

The Consumer Price Index has recently started falling. The only times in history where the CPI level has initiated substantial downward trends are throughout major recessionary or contraction economic phases. It is very likely that the decrease in the CPI level is reflecting a supply glut pricing effect as a result of the COVID-19 shutdown process. When consumer activity drops dramatically while supply channels continue as normal, a supply glut happens. When this happens, price levels must adjust and address the over-supply of goods and raw materials stacking up in warehouses, containers, and ships.

If the consumers earning and spending capabilities are disrupted long enough, the manufacturing and supply side of the equation can’t react fast enough to the immediate decline in demand. Therefore, the supply glut continues for a period of time as manufacturers attempt to scale-down the production levels to address for proper demand levels. Obviously, lower demand equates to lower sales volumes and lower-income levels for manufacturers and sales outlets. This translates into layoffs at the factories, sales outlets, and all levels in between. The cycle continues like this until an equilibrium is reached between supply and demand.

This translates into lower-earning expectations for much of the US and foreign markets compared to previous expectations. While the S&P 500 stock price levels have recovered to nearly the early 2020 price levels, it seems rather obvious to us that Q2 earnings data will likely shock the markets with dramatically lower results and forward expectations – in some cases these numbers may be disastrous.

When Nike released their Q4 (May 2020) earnings and showed a nearly $800 loss because of the early COVID-19 shutdown, this should have presented a very real understanding of how all levels of retail, manufacturing, and consumer services would also likely show a dramatic economic contraction taking place. Currently, we are watching for news of new US businesses entering the bankruptcy process. This recent article suggests business bankruptcies are skyrocketing higher – yet are still below the 2008~09 levels. Please keep in mind that we are only 90+ days into this COVID-19 virus event – so this data is still very early reporting.

Still, the numbers are very telling…

“US filings totaled 3,427 on June 24, according to data from Epiq seen by the Times. The reading also closes in on the financial-crisis reading of 3,491 companies entering bankruptcy in the first half of 2008. “

If you are reading the same data I read from that statement, the difference between the 2008 levels and current levels is only 64 additional bankruptcies in the US – less than a 2% difference in total bankruptcies.

The reality of the current market conditions is that we are only 90+ days into this processing of all this new data and attempting to understand what is likely to become a new operating norm for global economies. In 2008-09, the unwinding process took place over a full 12 to 16-month process. The recovery process too much longer – more than 5+ years. Currently, the unwinding process of the COVID-19 collapse took less than 30 days and the recovery process took a little over 90 days.

If our research team is correct, the speed at which the current recovery took place is nothing more than a reactionary recovery to a problem that was sudden and full of uncertainty. The Q2 data will likely solidify the uncertainty and unknowns into very real economic values (losses) and may shock the US stock market into a downward price reversion phase.

We believe one of the best hedging tools any skilled technical trader can use right now is Gold and Silver (Precious Metals). We continue to urge our friends and followers to maintain a portion of our portfolio in precious metals as a hedge against risk and unknowns throughout most of 2020 and beyond. If the Q2 data does what we believe it will do, shock the markets, then a moderately violent and volatile downside price move is pending. Simply put, you can’t destroy 25 to 45% of an active economy and displace millions of workers while sustaining high price valuations – unless you have a bubble-like euphoric investor mentality. That, ladies and gentlemen, is exactly what we believe is happening right now.

The super-cycle event that took place between 1920 and 1929 was nothing more than a euphoric bubble-like event where investors and traders had “no fear”. Everyone was leveraging everything they could to try to jump into the markets because they believed nothing could stop the rally. Keeping this in mind, you may want to read this recent research post about parabolic bubbles we published on June 23, 2020.

When bubbles burst, most commonly done when investors suddenly come to their senses in terms of real valuation expectations, the downside price moves can be extremely distressing. We urge you to properly understand that may happen with Q2 earnings data and new announcements. We also urge you to understand the COVID-19 virus event may have moved the super-cycles into some type of “warp-speed”. If our research is correct, we could be speeding towards a massive unwinding/crisis cycle phase very similar to 1929~1945.

Please read all the previous segments of this article and please properly position your portfolio to protect your assets. There will be lots of other trades in the future for all of us. These bigger price moves are not suddenly going to end because of Q2 or Q3 data. Be patient and stay protected. Q2 data is almost here and we are about to see some realization of the COVID-19 economic destruction process.

Get our Active ETF Swing Trade Signals or if you have any type of retirement account and are looking for signals when to own equities, bonds, or cash, be sure to become a member of my Passive Long-Term ETF Investing Signals which we are about to issue a new signal for subscribers.

Chris Vermeulen Chief Market Strategies Founder of Technical Traders Ltd.

NOTICE: Our free research does not constitute a trade recommendation or solicitation for our readers to take any action regarding this research. It is provided for educational purposes only. Our research team produces these research articles to share information with our followers/readers in an effort to try to keep you well informed.

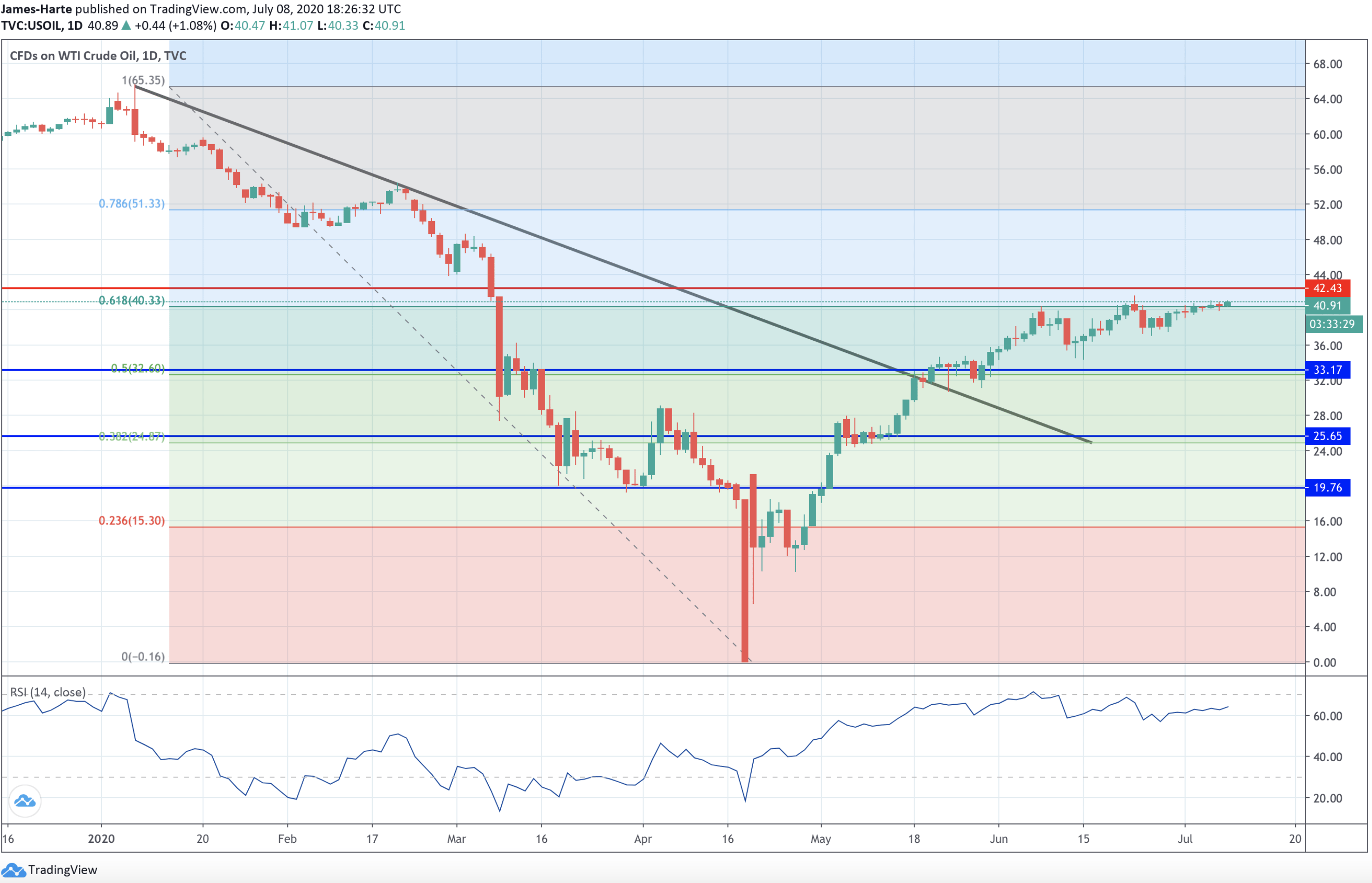

Crude oil prices have managed to remain near recent highs this week. This is despite the latest report from the Energy Information Administration highlighting a further rise in US crude inventories.

The EIA reported that in the week ending July 3rd, US crude inventories increased by another 5.7 million barrels. This is a wildly different result to the 3.1 million barrel decline the market was looking for.

Imports Rise Again

Regionally, crude levels in the Gulf Coast region rose the most. Levels there moved to record highs of 309 million, creating fresh fears over storage capacity in the US.

A great deal of this build was attributed to a fresh increase in imports. Net crude US imports jumped by 2.13 million barrels per day last week. Imports rose to 5.01 million barrels, hitting their highest level since the summer of 2019.

In the Gulf Coast specifically, imports jumped by 1.8 million barrels per day to 3.2 million barrels per day, marking their highest level since summer 2018.

Gasoline Demand Bouncing Back

However, despite news of an increase in the headline inventories number, oil prices remained supported amidst news of a strong drop in US gasoline stocks.

Fuel stores fell by 4.8 million barrels over the week, far outstripping analyst expectations for only a slight decline.

Despite the easing of lockdown measures over recent weeks, gasoline stocks had remained elevated up until the decline reported last week. This is encouraging evidence of the pickup in activity as people return to work and begin moving around again.

The summer is typically the highest period of demand for gasoline, dubbed “the summer driving season.” Hopefully, this latest report will help assuage fears that gasoline demand might remain low all summer.

However, despite the drop in gasoline stocks, distillate inventories, which include diesel and heating oil, were higher over the week by 3.1 million barrels.

This latest increase, which stands in stark contrast to the 75k barrel drop expected, takes inventory levels up to 177.3 million barrels, their highest level since the early 1980s.

Risk Sentiment Remains Supportive

Oil prices have been broadly supported over recent weeks. This is due to the resilience seen in equities markets.

Traders appear to be looking beyond fears of a second wave of the virus currently. Instead, they seem to be focusing on the tentative, post-lockdown recovery.

They’re also looking to the wave of central bank easing in response to the virus. This, for now, is keeping oil prices supported.

Oil Rally Running Out of Steam

The rally in crude oil continues to stagnate around the 61.8% retracement of the decline from 2020 highs.

However, while price holds above the 33.17 level, focus remains on further upside and an eventual break above the 42.43 level.

However, should price break back below the 33.17 level, focus will turn to deeper support at the 25.65 mark.