The demand for the US currency is still high despite weak economic statistics. Thus, the number of people employed in the nonfarm sector decreased by 20.236K in April, while experts forecasted a decrease by 20.050K. Today, financial market participants expect the next report on the initial jobless claims in the United States. Also, investors are focused on relations between Washington and Beijing. US President Donald Trump said on Wednesday that he was closely monitoring how China fulfilled its obligations under the “phase one” trade agreement signed earlier. The US dollar index (#DX) closed in the positive zone (+0.37%) yesterday.

The European Commission presented the Spring Economic Forecast, according to which the pace of economic recovery in the Eurozone would be uneven. As the European Commission expects, the EU unemployment rate will rise from 6.7% to 9% this year. Eurozone GDP is likely to fall by a record 7.75%, and in 2021 will recover by 6.25%.

The British pound has fallen in expectation of the Bank of England meeting, which will be held today. Since the start of the COVID-19 pandemic, the regulator has adopted a wide range of measures to support the country’s economy, including lowering lending rates and expanding the quantitative easing program to £645 billion. Taking this into account, investors do not expect new incentives to be announced today. Still, they will closely monitor the macroeconomic forecasts and comments of the Bank of England regarding a likely further increase in the quantitative easing program.

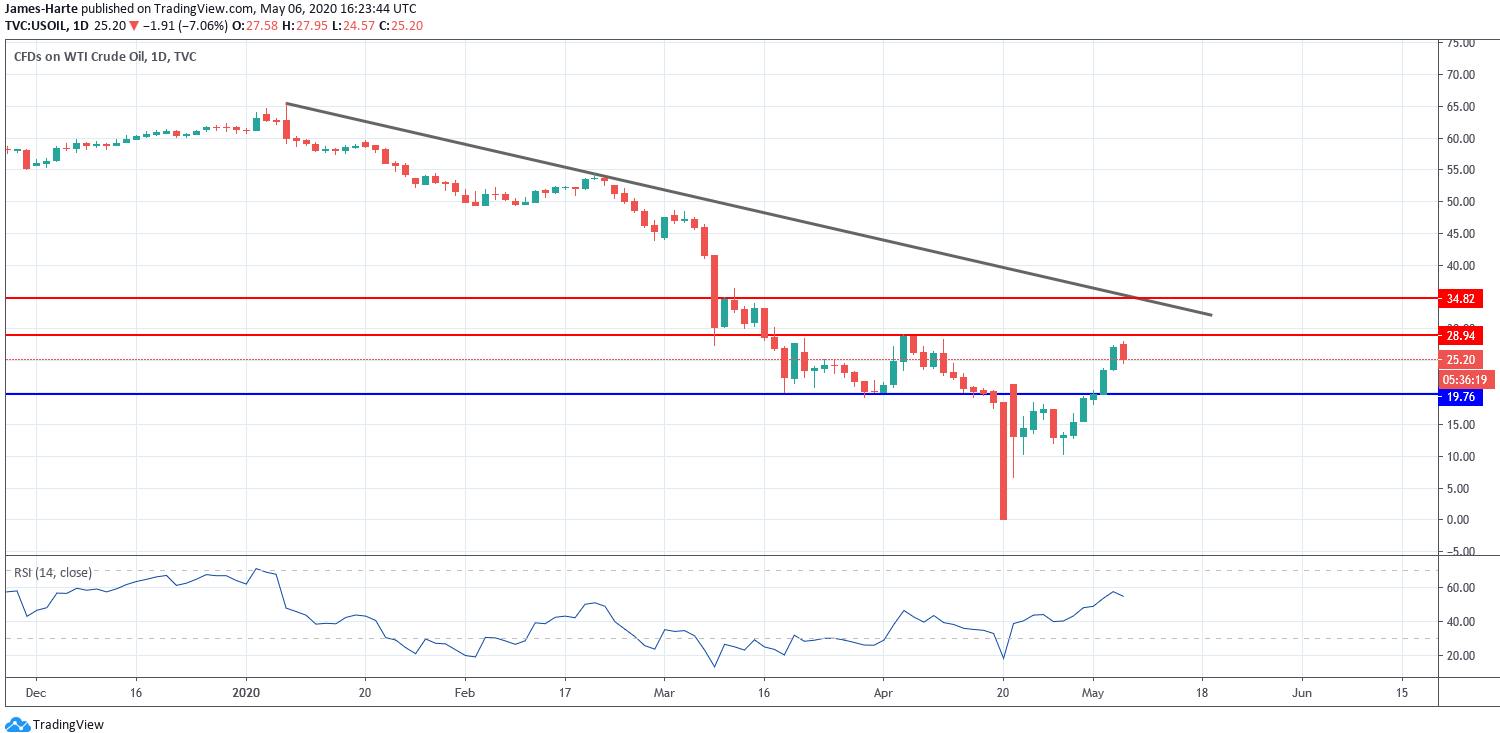

The “black gold” prices continue to recover. Currently, futures for the WTI crude oil are testing the $23.85 mark per barrel.

Market indicators

Yesterday, there was a variety of trends in the US stock market: #SPY (-0.68%), #DIA (-0.81%), #QQQ (+0.62%).

The 10-year US government bonds yield has risen again. At the moment, the indicator is at the level of 0.70-0.71%.

The news feed on 2020.05.07:

– Bank of England inflation report at 09:00 (GMT+3:00);

– Bank of England interest rate decision at 09:00 (GMT+3:00);

– Initial jobless claims in the US at 15:30 (GMT+3:00);

The euro lost the 1.0818 handle as it extended declines from the previous session.

However, prices are now trading near the trend line form the daily chart.

Overall, the EURUSD is consolidating into an ascending triangle pattern.

However, this will depend if the common currency can stall further declines. If the trend line breaches strongly, then we expect the downside to continue.

Alternatively, if EURUSD posts a reversal near the trend line, we expect price action to retrace the declines. This will see a potential move back to the 1.1000 handle.

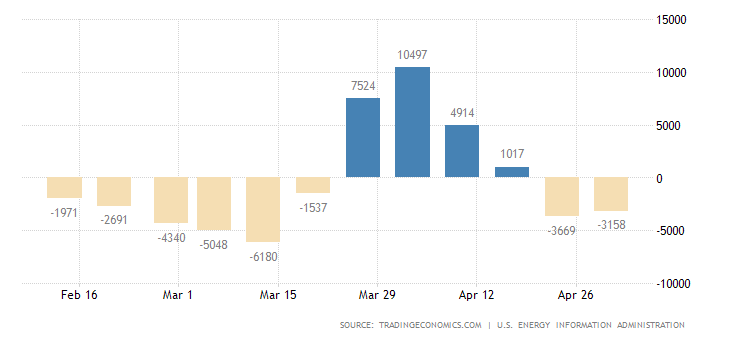

The latest data from the Energy Information Administration this week revealed a further surplus in US crude inventories, which have now risen for 15 straight weeks.

The EIA reported that in the week ending May 1st, US crude stores rose by a further 4.6 million barrels. The increase was a little less than the 7.8 million barrel increase forecast, which reflects some bounce back in demand.

That said, US crude stores are now just shy of the 535 million barrel all-time highs at 532.2 million barrels.

Storage Concerns Growing

The US Gulf Coast refining and export hub has now seen its crude levels rising to fresh record highs of 282.7 million barrels on the back of this latest increase. At the Cushing delivery hub in Oklahoma, crude stocks rose by a further 2.1 million barrels to 65 million barrels, the highest level in three years.

Refinery crude runs were up again last week, rising by 215k barrels per day as refinery utilization rates increase by 0.9% back up to 70.5% of capacity.

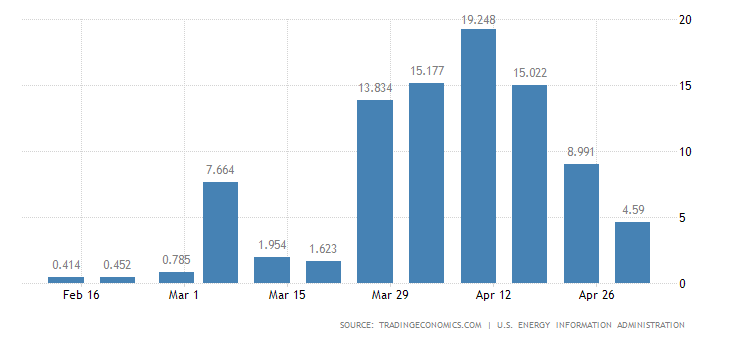

Elsewhere, the report showed that US distillate stockpiles, including diesel and gasoline, were higher by 9.5 million barrels last week. This was over three times the 2.9 million barrel increase forecast.

This latest increase brings the total distillate inventories level to 151.5 million barrels.

Gasoline Demand Bouncing Back

The report was not totally bearish, however. Gasoline stocks bucked the trend again last week.

Gasoline inventories fell by 3.2 million barrels over the week, despite expectations for a 43k barrel increase.

This is the second consecutive week of declines in gasoline stocks, reflecting a pickup in demand as lock-down measures begin to ease in places and more people take to the roads.

US Crude Production Falls Again

There was further good news for crude bulls as US crude production fell by 200k barrels per day to 11.9 million.

This is the lowest level of production since July 2019 and marks an extension in the recent trend of declining production levels.

However, given the heavily subdued state of global demand, US crude production levels still have a long way to come off before they can fuel any meaningful upside.

Is Crude Due A Reversal Higher?

The rally in crude has seen price trading back up to just shy of testing the 28.94 level resistance before coming off a little. However, while price holds above the 19.76 level, focus will be on further upside.

A test of the 19.76 level could prove to be the right-hand shoulder of a large inverse head and shoulder pattern, suggesting higher prices in the medium term. The key topside level to break will be the 34.82 mark where we also have trend line resistance.

The short-term economic outlook is looking terrible and it is likely to become even worse as more data gets published. Wednesday’s US ADP labour market report showed a record 20.24 million jobs were lost in the private sector last month due to business closures. While these numbers were anticipated, given that more than 30 million people filed for unemployment benefits over the past six weeks, this still represents an extreme shock to the world’s largest economy.

When analysts and strategists try to forecast the future of asset prices during such shocks, they tend to compare it to previous past patterns or economic cycles to draw conclusions and recommendations. Unfortunately in our lifetime, we have never experienced such a pandemic nor a contraction of this size and speed in the economy. Even many of the tools used by monetary and fiscal policymakers are brand new. Hence, predicting how this will turn out is going to be more of a guessing game than by using existing modelling and statistical methods.

Right now, the optimistic V-shaped recovery does not look like a realistic scenario for several reasons. An upturn of this type means that most of America and the world needs to get back to work soon, but that does not seem at all reasonable when looking at trends in Covid-19 infections. Even with lockdowns easing in many US states and across the globe, many sectors will not recover for several years, particularly airlines, leisure, auto and possibly oil.

Many questions related to the virus are still not being answered yet, especially the ones related to when and if a vaccine or treatment will be developed. Will the warm weather help contain the infections? Will the virus mutate into a different form requiring new medical trials? Will easing lockdowns lead to a new and stronger wave of infections? Until we get answers to these questions among several others, we cannot predict the shape and speed of the recovery.

Of course, the longer we stay at home, the more progress there should be in containing the deadly virus. However, this comes at the cost of more economic damage and it is this trade-off between health and the economy which is the most awkward question leaders across the globe are having to deal with. Even if we assume life returns to near normal, are we going to behave in the same way we did before Covid-19? Will we have the courage to appear in crowded places? Will all parents send their children back to school? Will we travel to places where infections are still on the rise? Are we going to follow old spending habits? In my opinion, it will take several months if not years to return to normal and that’s why even if economies open up, the recovery will be slow.

Currently the stock market is not a true representation of the economy’s weakened status. Investors are taking their cue from the Federal Reserve and Congress which are implementing unprecedented measures to ensure that the economic pain does not get reflected in financial markets. However, I believe there will be many long-term consequences which will be talked for many years to come.

The forward earnings multiple on the S&P 500 is currently standing at a 19-year high of 25, while the cyclically adjusted earnings multiple is still above the 2008 peak, despite falling from 31 in January this year to approximately 26.7 today. This suggests that valuations are still extraordinarily rich despite the vast amount of companies providing negative guidance, if in fact they are giving any at all. At current levels, I think investors are betting on a best-case economic recovery scenario supported by further easing measures. But as I mentioned earlier, predicting how asset prices play out during this pandemic is more of a guessing game than any form of true analysis.

Let’s hope that markets are right in predicting the best-case scenario.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Global markets are mostly advancing currently ahead of US Labor department report expected to indicate the total number of US unemployed hit 33 million. The bullish sentiment was boosted by unexpected rise in China’s exports in April.

Forex news

Currency Pair

Change

EUR USD

-0.05%

GBP USD

-0.55%

USD JPY

-0.76%

AUD USD

+0.46%

The Dollar strengthening has reversed today ahead of expectations data will show 33 million Americans likely sought unemployment benefits over the last seven weeks. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.4% Wednesday. It is lower currently as US Treasury said it would borrow $2.999 trillion during the June quarter, five times more than the previous single-quarter record. Both GBP/USD and EUR/USD continued sliding yesterday with both pairs higher currently. Pound got a boost after Bank of England kept the policy steady and stated UK demand has generally stabilized at very low levels in recent weeks. USD/JPY continues falling while AUD/USD has resumed declining.

Stock Market news

Indices

Change

Dow Jones Index

+0.99%

Nikkei Index

+0.98%

Hang Seng Index

+0.32%

Australian Stock Index

+0.38%

Futures on three main US stock indexes are higher currently after mixed session on Wednesday. The earnings season continues with companies including Verizon, Bristol-Myers Squibb and AMD scheduled to report quarterly results today. Stock indexes in US ended mixed on Wednesday : the three main US stock indexes recorded returns ranging from -0.9% to +0.5% with technology shares leading Nasdaq’s advance. European stock indexes are advancing currently following a pullback Wednesday after the European Commission forecast euro-zone economy will contract 7.4% this year in worst economic shock since 1930s. Asian indexes are mixed today. Shanghai Composite is ahead after gaining 0.5% as the General Administration of Customs reported China’s exports rose unexpectedly 3.5% in April from a year earlier, after falling 6.6% in March.

Commodity Market news

Commodities

Change

Brent Crude Oil

-0.14%

WTI Crude

+1.25%

Brent is extending losses today following the US Energy Information Administration report Wednesday that US crude oil inventories rose a slightly lower than expected 4.6 million barrels last week, the 15th consecutive weekly rise. The US oil benchmark West Texas Intermediate (WTI) futures retreated yesterday: June WTI lost 2.3% snapping a five-session streak of gains and is falling currently. July Brent crude closed 4% lower at $29.72 a barrel on Wednesday.

Gold Market News

Metals

Change

Gold

+0.56%

Gold prices are rebounding today. June gold lost 1.3% to $1688.50 an ounce on Wednesday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Shares of Portola Pharmaceuticals traded 130% higher after the company reported that it has received an $18 per share buyout offer from Alexion Pharmaceuticals.

The acquisition is said to provide a key addition to Alexion’s diversified commercial portfolio. The report indicated that the merger agreement has already been unanimously approved each of the company’s boards of directors.

The report explained that “Portola’s commercialized medicine, Andexxa® [coagulation factor Xa (recombinant), inactivated-zhzo], marketed as Ondexxya® in Europe, is the first and only approved Factor Xa inhibitor reversal agent, and has demonstrated transformative clinical value by rapidly reversing the anticoagulant effects of Factor Xa inhibitors rivaroxaban and apixaban in severe and uncontrolled bleeding.”

Portola’s President and CEO Scott Garland commented, “In developing and launching Andexxa, Portola has established a strong foundation for changing the standard of care for patients receiving Factor Xa inhibitors that experience a major, life-threatening bleed. Andexxa rapidly reverses the pharmacologic effect of rivaroxaban and apixaban within two minutes, reducing anti-Factor Xa activity by 92 percent…Given their enhanced resources, global footprint and proven commercial expertise, we look forward to working with Alexion to maximize the value of Andexxa. With their commitment to commercial excellence, together, we will be able to drive stronger utilization of Andexxa, increase penetration and accelerate adoption in the critical care setting.”

Ludwig Hantson, Ph.D., CEO of Alexion, remarked, “The acquisition of Portola represents an important next step in our strategy to diversify beyond C5. Andexxa is a strategic fit with our existing portfolio of transformative medicines and is well-aligned with our demonstrated expertise in hematology, neurology and critical care…We believe Andexxa has the potential to become the global standard of care for patients who experience life-threatening bleeds while taking Factor Xa inhibitors apixaban and rivaroxaban. By leveraging Alexion’s strong operational and sales infrastructure and deep relationships in hospital channels, we are well positioned to expand the number of patients helped by Andexxa, while also driving value for shareholders.”

The firms advised that “under the terms of the merger agreement, a subsidiary of Alexion will commence a tender offer to acquire all of the outstanding shares of Portola’s common stock at a price of $18 per share in cash.” Alexion plans to fund the purchase with existing cash on hand and the transaction is expected to close in Q3/20. The purchase is subject to approval by a majority interest of Portola’s common stockholders tendering their shares along with ordinary closing conditions and regulatory approvals. The company noted that “following successful completion of the tender offer, Alexion will acquire all remaining shares not tendered in the offer at the same price of $18 per share through a merger.”

Alexion is a global biopharmaceutical company based in Boston, Mass., with offices in 50 countries worldwide. The company states that it has been “the global leader in complement biology and inhibition for more than 20 years and that it has developed and commercializes two approved complement inhibitors to treat patients with paroxysmal nocturnal hemoglobinuria and atypical hemolytic uremic syndrome, as well as the first and only approved complement inhibitor to treat anti-acetylcholine receptor antibody-positive generalized myasthenia gravis and neuromyelitis optica spectrum disorder.”

Portola is headquartered in South San Francisco, Calif., and is a commercial-stage biopharmaceutical company focused on treating patients with serious blood-related disorders. Specifically, the company is engaged in developing and commercializing novel therapeutics in order to advance the fields of thrombosis and other hematologic conditions. The firm listed that its first two commercialized products are Andexxa® and Bevyxxa® (betrixaban), and that it is also advancing and developing cerdulatinib, a SYK/JAK inhibitor for use in treatment of hematologic cancers.

Portola Pharmaceuticals started off the day with a market capitalization of around $609.0 million with approximately 78.5 million shares outstanding and a short interest of about 23.0%. PTLA shares opened 130% higher today at $17.85 (+$10.09, +130.03%) over yesterday’s $7.85 closing price. The stock has traded today between $17.71 and $17.91 per share and is currently trading at $17.83 (+$10.07, +129.77%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

The junior gold explorer with a nascent exploration breakthrough could soar on the back of a gold bull market, writes Peter Krauth.

Gold has the wind in its sails. Its price in U.S. dollars is up an astounding 62% since late 2015, with a 33% gain in just the past year, outpacing all major assets.

And investors are only just starting to get interested.

The Covid-19 pandemic and its economic impact is a major catalyst. More than $8 trillion in global fiscal stimulus has already been committed to alleviate unemployment and support struggling businesses. But it’s almost certainly not enough.

“That sets up the perfect storm for X-Terra, making it a Strong BUY. With its outstanding initial drill results at the Grog property and the remarkable potential at Troilus East, I can easily see XTT double its market cap in the next 6-12 months, perhaps sooner.”

Near-zero interest rates combined with unprecedented money-printing are creating ideal conditions for the ultimate inflation hedge: gold. And that’s making junior gold equities the go-to sector as the metal rapidly approaches its all-time high.

Amidst all this, one junior gold explorer with a nascent exploration breakthrough could soar as the gold bull market moves into its next phase.

New Brunswick Could Host Large New Gold System

Bona fide new discoveries with district potential are rare. Participating early in one could be a life-changing event.

Its top two projects are in neighboring Canadian provinces, both among the highest-ranking gold mining jurisdictions globally.

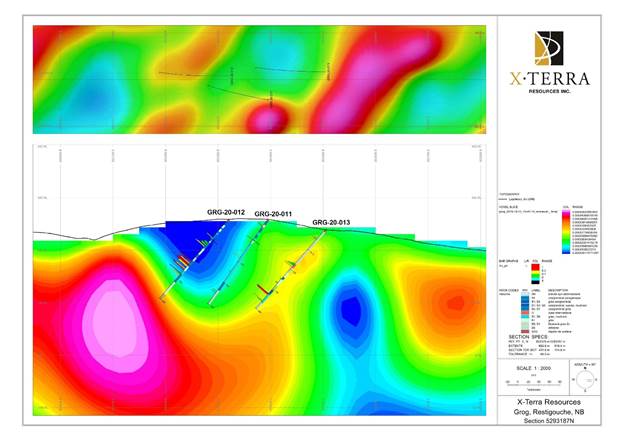

In early March, X-Terra completed its inaugural drill program over the Grog and Northwest Properties in the province of New Brunswick along the McKenzie Fault. It comprised 1,904 meters over 16 holes.

Hole GRG-20-012 identified gold mineralization over a significant width. One interval averaged 0.41 g/t gold over 36 meters, including 0.46 g/t gold over 31 meters and 7.59 g/t gold over 0.6 meters. The company points out that 6 of the remaining holes returned mineralized intervals between 0.1 g/t gold and 0.35 g/t gold.

X-Terra President and CEO Michael Ferreira said, “This is a significant exploration breakthrough, and reinforces our expectations that a large epithermal system is present. While more in-depth geological work, which includes drilling is needed, it remains evident that the 11 holes (1570 metres drilled) only covered a very small fraction of the targeted environment. Reaching a significant mineralized interval this shallow (From 107 metres to 143 metres, in GRG-20-012) is a milestone we were relentlessly pursuing after completing the limited field exploration programs based predominately on roadside trenching. The information obtained in this program will allow the detailed follow up on the Grog Target but also allow the company to refine and generate more high priority targets carrying the same geological characteristics to that of the Grog target. This provides a monumental shift moving forward.”

HIGHLIGHTS FROM HOLE GRG-20-012

Hole ID

From

(m)

To

(m)

Length

(m)

Au

(g/t)

GRG-20-012

107.00

143.00

36

0.41

Including

107.00

138.05

31.05

0.46

Including

114.50

117.50

3.00

1.01

Including

125.00

128.00

3.00

0.72

Including

137.45

143.00

5.55

0.92

The beauty of this impressive drill hole intercept is its signature, which contains a wide alteration halo associated with sulfidation and quartz veining. Based on the geophysical data, they will be able to track the gold bearing system at depth using an advanced data processing approach combined with their geological knowledge.

The exploration team can now use the signature to formulate similar drill targets elsewhere on the property, with the potential for similar results.

Clearly, X-Terra’s diligent, methodical and scientific approach has begun to pay off. Experience combined with a skilled overlay of induced polarization, magnetic surveys, sampling and trenching helped achieve this recent success.

Back in 2017, the company discovered high grade gold occurrences. That was followed up with further work, which delivered extensive anomalies scattered over roughly 30 km along the McKenzie Gulch regional Fault.

Their geologists then engaged a quick exploration cycle over the next 18 months, starting with an orientation geophysics survey, followed by trenching and drilling. They now have an initial model in progress, which involves an extensive magmatic hydrothermal system, and the targets generated so far are pluri-kilometric.

X-Terra is contemplating that it could be onto a brand new regional gold trend.

Such outstanding recent drill intercepts make for an even more exciting outlook. That’s because future exploration targets will be chosen with a better understanding of the geological sequence. And that should improve the odds of more successful drill results.

But perhaps the biggest takeaway from hole GRG-20-012 is the suggestion that it demonstrates real potential for a large epithermal system. And that could mean a whole lot of gold lies beneath, something further exploration will answer.

Quebec Offers Huge Promise Near Large Developing Gold Mine

Despite the exciting outlook offered by the Grog area located in New Brunswick, X-Terra is far from being a one-trick pony.

Also bursting with massive untapped potential is the Troilus East Property, located in north-central Quebec.

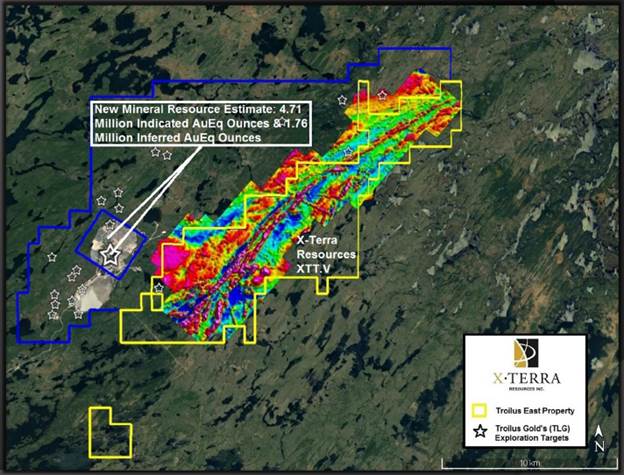

X-Terra’s Troilus East project is immediately adjacent to Troilus Gold Corp.’s former producing gold-copper mine. Even after 15 years of historic production, the Troilus Gold Project currently boasts 4.71 million ounces of gold equivalent in the Indicated category, plus 1.76 million ounces of gold equivalent in the Inferred category.

Early last year, X-Terra announced the completion of a high-resolution magnetic survey on the Troilus-East property. Management continues to advance the project, using the same diligent and methodical scientific approach that has brought success to the Grog discovery. XTT will be using magnetic signatures to perform follow-up work, looking to identify geological contexts with characteristics similar to those of the Troilus gold-copper mineral deposit.

Since tripling its land position, X-Terra has locked up the largest adjacent land claims to Troilus Gold of any public company.

That’s exciting, as Troilus Gold is considered by some as the largestor at least one of the largestundeveloped gold deposits in North America. And that could well make X-Terra a future target should Troilus Gold or other players look to lock up more of the adjacent land.

People and Projects Offer Massive Potential

As is often the case, people are as important to a junior explorer’s success as its properties. As a former professional motorcycle racer, X-Terra President and CEO Michael Ferreira saw the potential of resource exploration to create immense value for shareholders. Now living full-time in the Quebec mining town of Rouyn Noranda, Ferreira has judiciously curated a winning team.

Dr. Michael Byron, Ph.D., P.Geo. and a company director, has thirty years of field work, research and senior management positions across gold, base-metals, diamond and gemstone exploration. He was instrumental in re-discovering Falco Resources’ leading asset, the Horne 5 deposit.

A testament to the quality of management is XTT’s rare combination of tight share structure and quality projects. On a fully diluted basis, there are just 80 million shares outstanding, with management’s skin in the game representing 6% of ownership.

As I see it, X-Terra’s combination of quality management with exceptional high potential projects is starting to bear fruit. Its New Brunswick-located Grog and Northwest project, along with its Troilus East project located in Quebec, are highly prospective.

Given that the global fiscal and monetary response to the coronavirus has generated a tsunami of money printing, the gold market is kicking into high gear.

That sets up the perfect storm for X-Terra, making it a Strong BUY. With its outstanding initial drill results at the Grog property and the remarkable potential at Troilus East, I can easily see XTT double its market cap in the next 612 months, perhaps sooner.

In my view these are the early days of a string of successful exploration results, making XTT.V radically undervalued, for now.

Peter Krauth is a former portfolio adviser and a 20-year veteran of the resource market, with special expertise in energy, metals and mining stocks. He has been editor of a widely circulated resource newsletter, and contributed numerous articles to Kitco.com, BNN Bloomberg and the Financial Post. Krauth holds a Master of Business Administration from McGill University and is headquartered in resource-rich Canada.

Disclosure: 1) Peter Krauth: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: X-Terra Resources. My company has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: X-Terra Resources. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with X-Terra Resources. Please click here for more information. An affiliate of Streetwise Reports is conducting a digital media marketing campaign for this article on behalf of X-Terra Resources. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of X-Terra Resources, a company mentioned in this article.

Canadian foreign policy has long embraced both a deep continental relationship with the United States and a devotion to liberal internationalism. In light of the COVID-19 pandemic, the time has come to re-evaluate our approach.

While Canada has been able to manage the coronavirus crisis so far, our ability to continue to keep the pandemic at bay and successfully rescue the economy will likely be even more difficult.

If the U.S. cannot get a handle on the virus, and if its leadership chooses a protectionist route to economic recovery, Canada’s return to normalcy will be that much harder. That’s especially true if the Canadian government is not able to secure exceptions from Washington’s protectionist measures, as it has recently.

Similarly, if international trade and movement are slow to re-establish themselves, and if protectionism becomes a worldwide response, Canada can expect a cumbersome recovery.

Canada and the United States share a border and other geographical ties. But the coronavirus has underscored the need to ease our dependence on the U.S. Niagara Falls, Ont., is seen from the American side of the falls. (Pixabay)

Mostly benign

Canada’s dependence on the United States has been mostly benign. Yes, American decisions on softwood lumber and steel/aluminum tariffs, and limitations on other free trade agreements found in the USMCA hurt Canada, but Canada also greatly benefits from its commercial relationships with its neighbour.

But as COVID-19 radicalizes the already radical presidency of Donald Trump, Canada may be forced to confront its dependence on the U.S. more directly and with greater urgency.

Short-lived tensions — including Trump’s unsuccessful attempt to halt exports of masks to Canada and his musings about stationing troops near the border — may be harbingers of longer term restrictions, disagreements or spillover effects that slow or stifle Canada’s attempt to rebound from the current crisis.

Worse, the rise of nationalism and geopolitical competition points to the likelihood of a fragmented international order built around a handful of large protectionist or self-sufficient power blocs. Liberal principles of free trade and movement may come under increasing pressure, leaving Canada particularly vulnerable to the whims of protectionist powers.

The ‘Third Option,’ COVID-19 edition

So, what, if anything, can be done? In 1972, following the shock to the world economy brought about by former U.S. president Richard Nixon’s decision to effectively end the Bretton Woods system of fixed exchange rates, Pierre Trudeau’s government introduced a policy idea called the “Third Option.” It was essentially a call for more self-sufficiency at home and stronger ties with the rest of the world to lessen dependence on the United States.

Though the Third Option dissipated after a few years, the idea behind it never quite died off. COVID-19 renders Third Option thinking not only respectable but also responsible again.

Whether general or issue-specific, multilateral or “plurilateral,” ties with partners in Africa, Asia, the Americas and Europe are in Canada’s best interest, simply because they constitute a counterweight to the United States. True, some of these ties will always be shallow, others short-lived, and still others both. Yet, some ties might well lead to the establishment of deeper and closer strategic relationship with the rest of the world.

More diverse trading relationships will be essential to ensure Canadian resilience. In light of the recently concluded Comprehensive Economic and Trade Agreement, the European Union, for all its shortcomings and uncertainties, is one good candidate for such a relationship.

No heavy reliance on allies

The principal challenge of the COVID-19-era Third Option, though, is not finding new partners. Rather, it’s Canada’s ability to do things on its own without relying on too heavily allies and partners.

Canada needs to break free of its dependence on the United States if it’s to soar. (Dennis Larsen/Pixabay)

We may see Canada invest in national manufacturing of medical goods as a result, akin to the munitions supply program that ensures the Canadian military has the ammunition it needs.

But the pandemic has also highlighted that Canada’s COVID-19 response has arguably been too reliant on international assessments. Canada will need to strengthen its own ability to assess and craft effective responses to global crises, not only in the area of public health, but finance, security and defence, climate change and migration, among others.

While global problems require global solutions, the pandemic has highlighted that national responses remain vital and should not be overly dependent on allies and international bodies.

Building the capacity to pursue the Third Option will take time, money and, most importantly, a political culture willing to reconsider the fundamentals of Canadian foreign policy. To get there, Canadians must be willing to think harder about Canada-U.S. relations and an increasingly fractured international order.

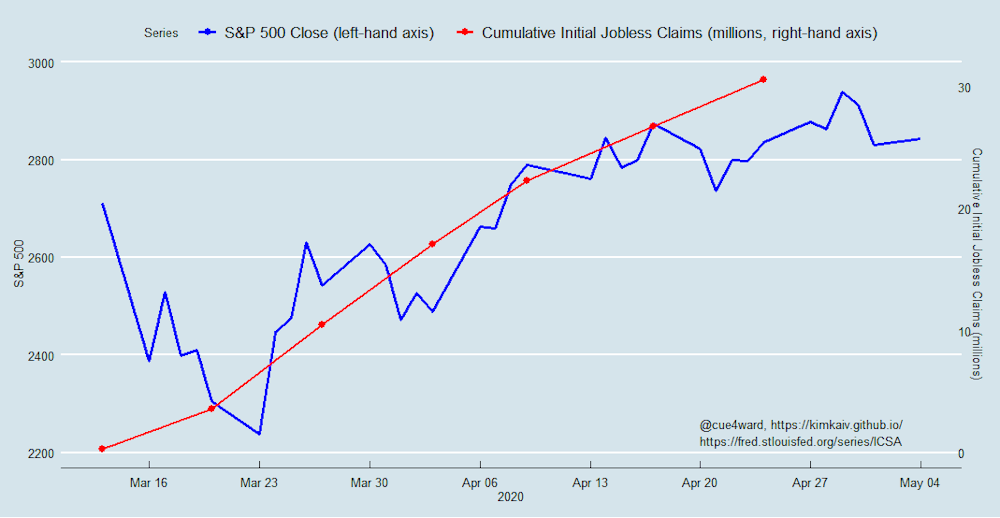

At times the contrast between the real economy and the stock market is striking. For US stocks, April was their best month since 1987, while at the same time real economic indicators – such as employment, manufacturing, services, trade, commodities and GDP – tanked. It seems that in April, the stock market caught the tail end of spring break spirit.

Some suggest this shows investor sentiment is free of any anchor in the real economy. Either this or rampant speculative flows “buying the bottom” have become a self-fulfilling force. I argue that market sentiment in April was informed by twin-howitzer policy deployments of overriding force and clarity, but which are ultimately of finite holding power.

During economic contractions, stock prices generally react negatively to unanticipated increases in unemployment. Research shows that a rise in unemployment portends reduced earnings and dividend growth for companies. This relationship is especially strong during economic contractions. So when unemployment increases unexpectedly, stock prices fall – usually.

Yet the big step-change increase in initial jobless claims in the week ending March 21 coincided with an extraordinary sequence of dramatic response measures by the US central bank, the Federal Reserve. The stock market’s bounce began on the following Monday and continued throughout April, despite mounting unemployment-insurance claims, which have now crossed the 30 million mark.

One particularly cynical reason for this is that furloughed and laid-off employees relieve businesses of costs. Of course, the wider economy is deprived of their spending as well. But from the third week of March, the trajectories for unemployment and spending were firmly set and known to market participants.

From that time onward, the subsequent rise of unemployment and the associated fall in spending were no longer “unanticipated”. The cascade of furloughs and lay-offs were predictable and so this information was built into both sentiment and stock prices at the time. Hence, the weeks of increasingly dire real-economy figures didn’t move the market in a big way.

Jobless claims tracked with the S&P 500 stock index. Kim Kaivanto, Author provided

Government intervention

But the more important factor for this month-long rise of the US stock market in the face of consistently dismal real-economy news was the unprecedentedly large, double-barrelled federal response – of financial-sector liquidity programmes and real-sector stimulus programmes – which was also emulated by governments around the world.

The US Federal Reserve’s extraordinary policy measures – and subsequently the nearly US$3 trillion authorised by the US Congress in the form of the CARES Act – provides firms and markets with emergency liquidity support to stave off an avalanche of defaults. Despite curtailed consumer and business spending, these government programmes offer businesses a means of avoiding immediate defaults – hopefully until the lockdown policies can be lifted. Think of this as an emergency transfusion and cauterisation of the wound.

The economic historian Niall Ferguson has suggested that the sheer scale of this state intervention is distorting the signals we are getting from the financial markets. But the breadth and scale of the intervention has an effect of its own, which is just as important as the support itself. It sends a credible signal that under the Trump administration, business will get all the support it needs to weather this pandemic. The US president sees buoyant markets as the key to his re-election, and he is dedicated to using all means at his disposal to that end.

Long-term debt issues

Buried in the weeds of this global crisis, seeds of destruction are sprouting. Much of the CARES Act emergency support for business consists of lending programmes. Of this, the US treasury received US$500 billion to support hard-hit big businesses like airlines, as well as states and cities – with loans, loan guarantees, and other investments.

But already in the autumn of 2019, the debt burden of US corporates approached a whopping US$10 trillion. As a ratio of GDP, the debt of nonfinancial firms in the US is at an all-time high. Some calculations place the proportion of “zombie firms” – companies whose earnings are so low that they must issue new debt just to cover the interest-payment obligations on their existing debt – at 16% among US public companies. Not only is lockdown pushing this figure higher, but so are the very loan programmes which were created to serve as emergency lifelines.

For large firms, refinancing continues to be viable, albeit with shortened maturities. Stress-test analysis of S&P 500 firms reveals a shift: fewer strong firms and more weak and vulnerable ones. So even with further top-ups to CARES Act programmes, the eventual recovery is likely to be subdued, at least until an effective COVID-19 vaccine becomes widely available.