Risk appetite is getting a boost after the US and China committed to the implementation of the phase one trade deal that was signed in January. The pledge was made via a phone call between China’s Vice Premier Liu He, US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin, after US President Donald Trump earlier this month raised the possibility of fresh tariffs against China.

Most major Asian stock indices are set to enter the weekend on a positive note as US equity futures point to further gains at the Friday open. Asian currencies are advancing against a softer US Dollar, while the Japanese Yen is also moderating against its Asian and G10 peers.

The last thing global investors need right now amid the global coronavirus pandemic is a one-two punch from spiking trade war risks. However, the fact that investors are being compelled to monitor these uncertainties on two major fronts set against a backdrop of a deep global recession, means safe haven assets like Gold and US Treasuries remain well bid.

There are enough potential downside risks still on the table, even without the injection of trade war uncertainties, that could trigger the unwinding of gains seen in risk assets since April. The catalyst for another dramatic decline could come by way of a second wave of coronavirus cases that triggers another round of lockdowns or the realisation that the trillions spent on support measures worldwide have fallen short in restoring more normal global economic conditions.

Even as global investors indulge in these bouts of optimism, evidenced by the MSCI ACWI Index’s 25 percent climb since March 23, it’s still too early to signal the all-clear. The risk of another selloff remains in play over the medium-term.

Dollar may flinch, but not surrender at heart-wrenching US non-farm payrolls

Today’s April US jobs data is set to unveil the devastation in the labour market caused by Covid-19. Markets are forecasting a fall in employment of 22 million jobs, its worst-ever showing on record, with the unemployment rate likely increasing nearly four-fold from the month prior to 16 percent. The US quarantine measures rolled out since March are expected to have laid waste to a decade’s worth of jobs growth, while crippling the primary driver of the world’s largest economy. Yet, markets have had ample time to consider such depressing premonitions and the confirmation of such forecasts is unlikely to prompt wild swings in the markets, barring a massive surprise.

Technically speaking, even if the Dollar index’s momentum appears ready to bring it past the lower end of its triangle pattern, it should remain within the 98.30-101 range. The fact that any break below its 50-day moving average since end-March has proven short-lived adds to the near-term rangebound feel of the Greenback. Such support is derived from the broader demand for safe haven assets, with King Dollar expected to continue holding court in the FX markets.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

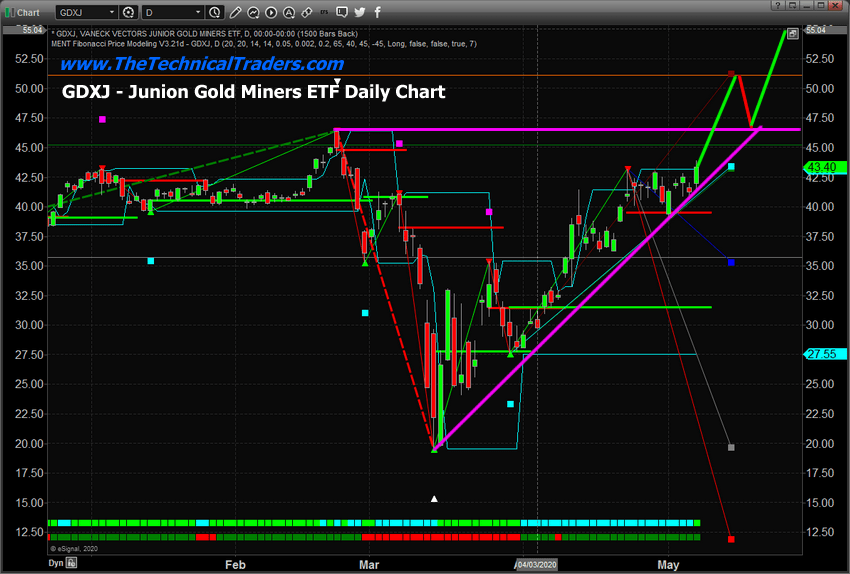

– Both Gold and Silver Futures have been struggling to rally above recent high levels since the start of the global stock market collapse related to the COVID-19 virus event. Yet, the Junior Gold Miners appear to be telling us the Precious Metals market is boiling hot.

Gold, the bell-weather safe-haven asset, initially collapsed when the US stock market started the massive selloff in late February 2020, then recovered to higher price levels near $1785 recently. Since reaching these levels, Gold has stalled into a sideways price flag near major resistance.

Silver, on the other hand, is trading near $15.60 and has yet to really recover to anywhere near the levels it had achieved in early January 2020 (near $18.60).

Well, GDXJ, the Junior Gold Miners ETF, is suggesting a very strong price rally is taking place that may push both Gold and Silver substantially higher. Key resistance exists near $46.50. Once broken we believe a very strong price rally will take place pushing GDXJ price levels to $51 or $52. After that, a brief downside rotation will potentially retest the $47 to $48 levels before an even bigger upside rally takes place. What is even more important is that we believe this big breakout move could start as early as next week, May 12th or after.

Before you continue, be sure to opt-in to our free market trend signals before closing this page, so you don’t miss our next special report & signal!

GDXJ Daily Chart

This GDXJ Weekly chart highlights the same price pattern and shows why we believe the upside price breakout could be a massive new trend. The Deep price low setup because of the COVID-19 virus event creates a very big price range for any future price advancements. That $24 price range, if applied to price levels before the breakdown event near $41, may suggest GDXJ could rally to levels above $65 over the next few weeks or months.

GDXJ Weekly Chart

Concluding Thoughts:

We believe the upside rally in both Gold and Silver recently is a very good indication that the sideways price channel that has plagued precious metals recently may be ending. If precious metals prices begin to rally, then GDXJ will break the upper $46.50 resistance level and begin a new upside price rally clearing the resistance setup before the virus event began.

Get ready, this could be a very big move higher for Junior Miners and it could align with our May 8th through May 12th global market inflection point prediction.

If you are using our free public research for your own trading decision-making and/or using it as an opportunity to find and execute successful trades, please remember you are the one ultimately making the decisions to trade based on our interpretation and free research posts. We, as technical traders, will continue to post new research articles and content that we believe is relevant to the current market setups.

If you want to improve your accuracy and opportunities for success, then we urge you to visit TheTechnicalTraders.com to learn how you can enjoy our research and our members-only trading triggers (see the first chart in this article). If you are managing your retirement account or 401k, then we urge you to visit www.TheTechnicalInvestor.com to learn how to protect your assets and grow your wealth using our proprietary longer-term modeling systems. Our goal is to help you find and create success – not to confuse you.

Our researchers will generate free research on just about any topic that interests them. As technical traders, we follow price, predict future price moves, tops, bottoms, and trends, and attempt to highlight incredible setups that exist on the charts. What you do with it is up to you. Visit www.TheTechnicalTraders.com/FreeResearch/ to review all of our detailed free research posts.

In closing, we would like to suggest that the next 5+ years are going to be incredible opportunities for skilled traders. Remember, we’ve already mapped out price trends 10+ years into the future that we expect based on our advanced predictive modeling tools. If our analysis is correct, skilled traders will be able to make a small fortune trading these trends and Metals will skyrocket. The only way you’ll know which trades to take or not is to become a member.

Arcturus Therapeutics Holdings’ arrangement is explained and commented on in an H.C. Wainwright & Co. report.

In a May 4 research note, H.C. Wainwright & Co. analyst Ed Arce reported that Arcturus Therapeutics Holdings Inc. (ARCT:NASDAQ) formed a partnership with Catalent Inc. (CTLT:NYSE), which “raises the profile of LUNAR-COV19 as a leading vaccine candidate.”

Arce reviewed Catalent’s contribution to the partnership. The global contract development and manufacturing organization is to manufacture Arcturus’ messenger RNA (mRNA) LUNAR-COV19 for protection against SARS-CoV-2 to be used first for human clinical trials and potentially, eventually commercially.

As for timing, Arce noted, San Diego, Calif.-based Arcturus intends to transfer its vaccine technology to Catalent this month and expects Catalent to manufacture the first batches of LUNAR-COV19 by June 2020. “Critically, Arcturus continues to anticipate initiation of Phase 1 testing of LUNAR-COV19 in the summer of 2020,” Arce highlighted.

Catalent is to produce the vaccine at its biomanufacturing facility in Madison, Wisc. “This facility utilizes Catalent’s flex-suite, a current good manufacturing practice manufacturing suite, that can produce batches at multiple scales and support Arcturus’ proprietary mRNA manufacturing process,” explained Arce.

Obtaining the vaccine from one facility domestically versus multiple entities worldwide should result in several benefits, Arce continued. They include easy development and production, accelerated delivery and improved costs. Arcturus believes Catalent can produce millions of doses of LUNAR-COV19 mRNA in 2020 and, if need be, hundreds of millions of doses each year subsequently for use globally.

Arce pointed out that LUNAR-COV19 differentiates itself from other similar vaccine candidates in that the technology and delivery platform behind it deliver an “extraordinarily low dose (perhaps 2 micrograms)” in “a potential single shot.”

H.C. Wainwright has a Buy rating and a $62 per share price target on Arcturus, the stock of which is currently trading at about $42.12 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosures from H.C. Wainwright & Co., Arcturus Therapeutics Holdings Inc., First Take, May 4, 2020

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Ed Arce, certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of Arcturus Therapeutics Holdings Inc. (including, without limitation, any option, right, warrant, future, long or short position).

As of April 30, 2020 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of Arcturus Therapeutics Holdings Inc.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The firm or its affiliates received compensation from Arcturus Therapeutics Holdings Inc. for non-investment banking services in the previous 12 months.

The Firm or its affiliates did receive compensation from Arcturus Therapeutics Holdings Inc. for investment banking services within twelve months before, and will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

H.C. Wainwright & Co., LLC managed or co-managed a public offering of securities for Arcturus Therapeutics Holdings Inc. during the past 12 months.

The Firm does not make a market in Arcturus Therapeutics Holdings Inc. as of the date of this research report.

H.C. Wainwright & Co., LLC and its affiliates, officers, directors, and employees, excluding its analysts, will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives (including options and warrants) thereof of covered companies referred to in this research report.

Oats are among the healthiest grains on earth with studies indicating eating oats and oatmeal contributes to lower blood sugar levels, a reduced risk of heart disease and weight loss. The advent of the coronavirus once again brought into the focus the importance of adequate healthcare and healthy lifestyle. It is expected to reinforce the trend in consumer preference shift towards consuming healthy food, which is likely to increase the demand in the global oats market. Rising demand expectations are bullish for oats. At the same time in Canada, the top world exporter of oats, farmers intend to plant 3.8 million acres of oats in 2020 – 6.3% more acres from a year earlier, according to Statistics Canada’s Principal field crop areas, March 2020 survey. And in US, the top world importer and sixth largest producer of oats, the Department of Agriculture National Agricultural Statistics Service ( NASS ) estimates oats planted area for 2020 at 3.01 million acres, up 7 percent from last year, according to Prospective Plantings report released March 31, 2020. Higher supply estimates are a downside risk for oats price.

For many forex traders, whether experienced or amateur, the risk is inevitable and comes in different forms. Many factors affect the trading market.

Not many people expect that a health crisis will affect the forex and financial market. However, Coronavirus has taken the world by storm and influenced the financial market across the globe.

The virus, also called COVID-19, was first reported in December 2019. To date, the virus has claimed over 2,100 lives. It has been estimated that more than 75,000 people are now infected with this deadly virus.

The Coronavirus was first reported in the Chinese city of Wuhan in December 2019. It is officially known as COVID-19. People infected with the virus exhibit various symptoms, including a cold or pneumonia. The mortality rate is estimated at 2%, while China is trying to contain it. Some cities, such as Wuhan, are isolated while patients are quarantined.

Although Coronavirus mainly affects the Chinese population, it is spreading to other parts of the world. On January 20, 2020, more cases were reported outside of China, including in Thailand, South Korea, and Japan.

Subsequently, on the 30th of that month, the World Health Organization declared the virus a global health crisis. Therefore, what does all this have to do with the Forex market?

The Impact Of The Coronavirus On Trading

The impact of Coronavirus on the forex market can be viewed from different angles. China is probably one of the world’s economic giants. The value of the Coronavirus in the national economy still cannot be ignored.

Financial experts warn that the number of scam attacks has escalated significantly. In such conditions, one should take extra precautions when trading. It is advisable to read reviews and study all of the information carefully. Honest reviews on brokers might be hard to find, even on well-known ones such as Nadex, Finmax, or IQ Option. You can read a trustworthy review on IQ Option here.

According to several economists, including a survey by Reuters, in the first four months of 2020, the country’s annual economic growth will decline. It has been estimated that this has indeed happened, with figures ranging from about 6.0% to 4.5%. After the change, some sectors also experienced negative changes, such as Apple stock prices, which went down after the Coronavirus outbreak.

Although the spread of the virus is expected to be kept to a minimum, the economic impact may be more tangible if the virus continues to spread. There are concerns that after China’s protracted trade war with the U.S., doubled with the spread of Coronavirus, the economy will probably not survive.

As this virus continues to spread to other Asian countries, it is expected that they, too, will suffer adverse consequences for their economies.

China’s Financial Market

China closed its markets during the Lunar New Year, and this period was extended until February 2 this year. However, after the extension, the market was reopened, and before that happened, the Central Bank of China announced an injection of 1.2 trillion Chinese yuan as liquidity. The market experienced further changes, including the suspension of over-the-counter trading to avoid forced selling. The Shanghai index fell to 10%.

Against the background of cancellation and suspension of flights to China by such significant airlines as Lufthansa and British Airways, China’s economy plunged into an abyss. Many major companies, such as Hyundai, have suspended some of their operations because of the problems they face.

Hyundai, for example, could not get spare parts from China, as a result of which some plants in South Korea were shut down.

In connection with these events caused by the outbreak of the epidemic, experts estimated a decrease in GDP by 0.5-1% in case the Coronavirus would peak in February or March.

The impact of these events on Chinese financial markets should not be underestimated. USD/CNH is trading higher and is expected to move even higher. It is anticipated that USD/CNH might face a holding of 7.0000 if the virus is contained.

Impact On Global Value Chains

During the past two decades, China has played a crucial role in the world economy. China’s growing importance in the world economy is not only due to its status as a producer and exporter of consumer goods.

China has become a significant supplier of intermediate resources for manufacturers abroad. Today, about 20% of world trade in intermediate products is produced in China (compared to 4% in 2002).

It is believed that any significant supply disruption in China in these sectors has a significant impact on producers throughout the rest of the world.

Indeed, many companies around the world fear that the measures introduced to curb COVID-19 (i.e., restrictions on economic activity and on the production of intermediate goods) are being implemented.

Impacted Countries

A reduction in China’s supply of intermediate inputs may affect the production capacity and therefore, exports of any country, depending on how dependent its industry is on Chinese suppliers.

For example, some European car manufacturers may face a shortage of critical components. Japanese companies may also find it challenging to obtain the parts needed to assemble digital cameras.

For a lot of companies, the limited use of inventories as a result of a lean and timely production process will lead to shortages that will affect their production capacity and total exports.

In general, the countries most affected will be the European Union (engineering, automotive and chemical), the United States (engineering, automotive and precision instruments), Japan (engineering and automotive), and the Republic of Korea (communications equipment and facilities), as well as Taiwan Province of China (communications equipment and office equipment).

Other Markets

While the financial markets of China and other Asian countries are becoming disorderly, some markets are winning. Safe currencies, including the Japanese yen, Swiss franc and U.S. dollar, continue to thrive.

These currency markets continue to gain support, while the Euro is slightly behind, with limited assistance. The commodity market is the worst hit. Commodity currencies like the Australian dollar are in danger, while the sterling pound is becoming vulnerable at a slower rate, especially if the global economy eventually slows down.

The influence of Coronavirus is felt not only in China but also indirectly, in other markets. Looking at light crude oil, one can see the influence.

While crude oil prices fell after Iran attacked U.S. bases in Iraq, it is clear that after the Coronavirus outbreak, about three weeks later, prices fell from an estimated 65.65 to a low of 52.13.

We cannot ignore the fact that China and the U.S., which signed the deal, kept the price of crude oil at 58.00 for a while. However, Coronavirus is slowly gaining momentum. If the outbreak continues, especially in China, the demand for crude oil is predicted to decline and then decline further.

Although Norway has not reported any deaths or infections from Coronavirus, it has been affected by the value of its Coronavirus infection. Since December, the prices of U.S. dollars for Norwegian Krone have fallen, and this was due to the demand for crude oil.

Norway exports crude oil and, therefore, changes in oil prices directly affect the price of the Krone.

With lower demand for oil, it looks like USD-NOK will rise, and if held down, oil rates will rise, and therefore USD-NOK will move even lower than at present in the market.

While there is still uncertainty regarding the impact of COVID-19 on China’s productive capacity, recent statistics indicate a significant decline. The full implications of COVID-19 on global value chains will become more evident in the coming months.

One crucial question, however, is how interruptions in the supply of intermediate inputs from China will affect the rest of the world.

The Coronavirus has also affected financial markets around the world, and it remains to be seen how much damage can be done or avoided.

It all depends on whether this virus is in the body or not. If governments can stop an outbreak like SARS, the expected extreme negative impact on trade can be avoided.

The central bank of the Czech Republic cut its benchmark interest rate for the third time this year, saying the outlook for economic activity had “deteriorated substantially” and this required an even greater easing of monetary conditions. The Czech National Bank (CNB) cut its 2-week repo rate by a further 75 basis points to 0.25 percent and has now cut it by 2 percentage points since it made a sharp U-turn after the outbreak of the coronavirus and cut its rate twice in March after raising it the month. CNB also lowered its Lombard rate to 1.0 percent while its discount rate was maintained at 0.05 percent. The new interest rates take effect May 11. While 5 members of the bank’s board voted for the 75 basis point cut, 2 voted for a 50 point cut. Although the Czech government is gradually lifting the quarantine measures that caused a shutdown of most of the economy, CNB said the negative impacts of subdued external demand and “the very unfavorable perception of the economic situation among Czech households and firms will persist.” Noting an extremely high uncertainty surrounding the outlook, CNB forecast the country’s economy will contract 8 percent this year, sharply down from its previous forecast of 2.3 percent growth, before bouncing back to 4.0 percent growth in 2021, up from 2.8 percent. Although economic activity will gradually bounce back, it will not return to pre-pandemic levels before the end of 2021, CNB said, mainly because fixed investments will be dampened by the deep decline in external demand associated with the significant deterioration in global economic sentiment. Exports are also expected to drop sharply while household consumption will fare better. The forecast of inflation is unchanged for consumer prices to rise 2.1 percent in the second quarter of 2021 and the same in the third quarter, implying significantly lower interest rates this year and next year, and a weaker koruna-euro exchange rate than the previous forecast, CNB said. Inflation, which fell to 3.4 percent in March from 3.7 percent in February, will be restrained from weaker domestic demand, which will outweigh any temporary inflationary effect of a weaker koruna along with the drop in fuel prices and slower growth in administered prices. In addition to rate cuts, many central banks have been providing liquidity to the banking system but CNB said it didn’t see any need right now to intervene. However, lawmakers have amended the central bank act to allow the CNB to provide liquidity and it is now preparing instruments to aid non-bank entities through short-term loans agains securities, mainly government bonds. CNB said it was also working on broadening the range of eligible collateral for banks and planning on providing liquidity though 3-month operations.

The Czech National Bank issued the following statement by its board:

“At its meeting today, the Bank Board of the Czech National Bank lowered the two-week repo rate by 75 basis points to 0.25%. At the same time, it lowered the Lombard rate to 1.00%. The discount rate remains unchanged at 0.05%. Five members voted in favour of this decision, and two members voted for lowering the repo rate by 50 basis points.

The decision adopted by the Bank Board is underpinned by a new macroeconomic forecast. After the sharp fall in domestic market interest rates recorded in March, consistent with the forecast is a further decline in 2020 Q2. It must be stressed that the situation during the preparation of the forecast was exceptional owing to the ongoing coronavirus pandemic. The uncertainty regarding the external and domestic assumptions of the forecast and the way they are captured by the model system is thus extremely high.

The impacts of the coronavirus pandemic and the related measures will lead to a significant decline in global economic output this year. According to the forecast, euro area economic activity will drop markedly in the first half of this year. The situation will stabilise gradually in the second half of the year and the Czech Republic’s main trading partner countries will return to economic growth next year. Producer prices are expected to fall substantially this year, owing to the aforementioned drop in economic activity and the collapse of oil prices. Consumer price inflation in the euro area will slow considerably this year. The European Central Bank has launched massive securities purchases. The outlook for short-term euro area interest rates remains negative over the entire forecast horizon.

The price of oil dropped by almost two-thirds during the first quarter of this year. According to the forecast, it will stabilise close to USD 40 a barrel. The euro will appreciate slightly against the dollar.

The quarantine measures adopted by the government and firms caused the shutdown of a large part of the domestic economy in March. The restrictions are gradually being lifted and most sectors are gradually starting up again during Q2. However, the negative impacts of the subdued external demand and the very unfavourable perception of the economic situation among Czech households and firms will persist. GDP will therefore fall significantly this year and, despite a gradual return to growth, economic activity will not return to the pre-pandemic level before the end of next year. This will be due chiefly to fixed investment. Its return to growth will be dampened by the deep decline in external demand associated with the significant deterioration in global economic sentiment. Exports can also be expected to drop sharply. Following an initial decline, household consumption will fare somewhat better, supported by decreasing but still positive wage growth and massive stabilising fiscal policy measures. In addition to programmes to support the liquidity of households and firms hit by the pandemic, government expenditure will rise owing to a previously approved increase in pensions and non-market sector wages and continued investment activity in the public sector. The labour market will cool quickly in the first half of the year owing to the contraction of the economy and will continue to do so next year despite an economic recovery. Employment will decline appreciably until almost the end of next year. The unemployment rate will increase rapidly, peaking at the start of next year.

Inflation will rapidly return to the upper boundary of the tolerance band around the target in the coming months, mainly due to the generally anti-inflationary impacts of the coronavirus crisis amid a deep decline of the domestic economy. Appreciably weaker domestic price pressures will outweigh the temporary inflationary effect of a weaker koruna. Inflation will therefore decline towards the 2% target at the end of this year. The decline in inflation will also be fostered by a drop in fuel prices stemming from the collapse of world oil prices and slower growth in administered prices. By contrast, food price inflation will remain high this year. The decline in inflation will also be slowed this year and the next by the price impacts of changes to indirect taxes. As a result, inflation will be close to the CNB’s 2% target next year.

Monetary policy-relevant inflation will be slightly lower than headline inflation, as the first-round effects of changes to indirect taxes will be slightly positive.

The koruna weakened sharply at the end of Q1 following the outbreak of the pandemic. The exchange rate will remain close to its current level over the entire forecast horizon due to the worse foreign and domestic economic outlook and narrower interest rate differential.

After the sharp fall in domestic market interest rates recorded in March, consistent with the forecast is a further decline in 2020 Q2 followed by broad stability. This decline in rates reflects the effects of government quarantine measures on the domestic economy as well as the significantly worse external outlook. As already stated, these facts will have significant anti-inflationary consequences. By contrast, the decline in rates will be slowed by the recent sharp weakening of the koruna, which is contributing to an easing of the overall monetary conditions.

The outlook for domestic economic activity this year has deteriorated substantially by comparison with the previous forecast. The inflation forecast at the monetary policy horizon is unchanged. The new forecast implies significantly lower interest rates this year and the next and a weaker koruna-euro exchange rate than the previous outlook.

The Bank Board assessed the risks to the forecast in the current extraordinary situation as being unprecedentedly high and requiring an even greater easing of the monetary conditions compared with the baseline scenario of the forecast. In the current situation, the risks are naturally connected with the course of the pandemic and especially with the duration and size of the impacts of the quarantine measures on the global and Czech economy.

At the moment, the CNB does not see a need to intervene immediately in financial markets by providing liquidity to financial institutions. Nonetheless, following an amendment of the Act on the CNB, it is for preventive reasons preparing a liquidity-providing instrument for some non-bank entities licensed by the CNB. These institutions will newly be able to obtain liquid funds in the form of short-term loans from the CNB. Such loans will be secured on the part of these financial institutions by the same securities that are used as standard collateral by credit institutions in liquidity-providing CNB repo operations, i.e. above all Czech government bonds.

In addition, for credit institutions (banks, foreign bank branches and credit unions), the CNB is working on broadening the range of eligible collateral used in existing liquidity-providing operations to include mortgage bonds. Liquidity-providing operations with three-month maturity will also be introduced for credit institutions.

The specific parameters of these operations will be published on the CNB website in the coming days. The Bank Board expects these operations to be announced regularly from 18 May 2020. At the same time, the Bank Board expects the relevant institutions to conclude the necessary contractual documents with the CNB or adjust their balance sheets so they are able to fully cover their liquidity needs themselves.

The CNB views these new instruments as additions to the range of monetary policy and macroprudential measures contributing to an environment on the Czech financial market that will enable Czech financial institutions and, in turn, the entire Czech economy to better deal with the current economic situation.

In its conduct of supervision, the CNB is continuing to take a flexible approach to how the individual supervised entities are to comply with certain regulatory duties. This is in line with the approach of the European supervisory authorities. The aim is to reduce the regulatory burden and thus create room for the individual supervised entities to react more flexibly to changes in the overall economic situation.

These steps enable, in particular, credit institutions to use their good capital position to support and finance the real economy while maintaining a prudent approach to risk management. This balanced approach of credit institutions to funding their clients may help reduce the contraction of the real economy and, as a result, lower the credit losses credit institutions may face in this crisis.”

ProMIS is harnessing its unique technology platform to develop a more error-free antibody test.

Testing has been an Achilles heel of the coronavirus pandemic, but ProMIS Neurosciences Inc. (PMN:TSX; ARFXF:OTCQB) has partnered with Dr. Hans Frykman and the BC Neuroimmunology Lab to use its unique technology to create a more accurate antibody test for SARS-CoV-2, the virus that causes Covid-19.

Two main types of tests exist for Covid-19: one that detects the presence of the virus that causes Covid-19, which indicates a person has an active infection, and another that detects antibodies, showing that a person has been exposed to the virus.

The first test that was developed, a test for the presence of the virus, is used mainly to confirm diagnosis of Covid-19 in people who are showing symptoms such as a fever, a dry, persistent cough, difficulty breathing, a sense of restriction in the chest. “They are typical signs of Covid-19, but we would want to know if these are signs of the common flu or a bad cold or Covid-19. We know that Covid can progress really significantly very quickly, especially in individuals with underlying conditions,” ProMIS CEO Dr. Elliot Goldstein told Streetwise Reports. “The number of tests is limited, but it’s not actually the tests themselves but the reagents and systems you need to run the test that are in short supply.”

“Anytime you conduct a test for the virus and get a negative response, the test indicates only that on that day at that time, the person does not have the virus. The person could have had Covid and recovered, or might have had an asymptomatic or very mild case. Or that person could get the virus tomorrow or in three days,” Dr. Goldstein explained. “At any point in time the virus test helps indicate the prevalence of the virushow many people are actually infectedif you test broadly, and at the time you do it, you can determine whether an individual is currently infected or not.”

The second type of test, called serological tests or assays, is also known as an antibody test. “When a person is recovering from a viral infection, the immune system makes antibodiesalso called immunoglobulinsthat are specific to the virus. They neutralize the virus and help clear it out; that’s part of the mechanism of why you get better,” Dr. Goldstein explained.

One way to see if a person has had Covid is to test for antibodies. “A positive test means you’ve been exposed to the virus because, in the absence of a vaccine, that’s the only way you would have the antibodies. While it’s not 100% certain that antibodies neutralize the virus, based on experience with other coronaviruses, it is likely,” Dr. Goldstein said. Having the virus neutralized should offer at least some protection against future re-infections.

People who have had positive virus tests know that they have Covid or had Covid and recovered, but many people are asymptomatic or may have had what felt like a light cold, and they want to know if they are at risk, or if they have some protection against the disease. “This is really important for frontline healthcare workers, people working 8-10 hours a day in intensive care or the emergency room with patients known to be very sick with Covid-19; even with protective equipment, they have significant exposure to the virus,” Dr. Goldstein explained. “If someone has been through the disease and has natural antibodies, they can’t infect someone else. What you want to know on an individual level is am I safe from infection and am I safe for other people.”

Generally, antibody testing is a fairly common procedure, Dr. Goldstein explained. When you spin blood in a centrifuge, it separates into three parts: red blood cells, plasma and serum. Serum is where you find antibodies. “ELISA (enzyme-linked immunosorbent assay) is a standard test that looks for antibodies, but it is not specific enough for the Covid-19 virus.”

The challenge is there are multiple coronaviruses. “Four different coronaviruses are responsible for the common cold, and then there are others like SARS and MERS. They all have the same sort of halo or corona of protein around the outside of it,” Dr. Goldstein said. “They look like the old naval mines used in war. The whole family of coronaviruses look like that. The amino acid sequences of different coronaviruses are not identical but very similar; they share a lot of common structures. There are only really small differences and you can’t really pick them up using the usual physical methods.”

Studies have shown that up to 90% of individuals in Western countries have been exposed to one or more of the common cold coronaviruses and have antibodies against them. “They look very similar to the coronavirus causing Covid-19. So in Covid-19 antibody tests, the most important thing is it has to be highly specific for the Covid-19 antibodies and doesn’t test positive when it identifies a common cold antibody. That is a false positive,” said Dr. Goldstein. “It’s actually much safer not to have a test that has a lot of false positives because you could base a behavioral decision on faulty information.”

Dr. Goldstein cited an example. “If you are testing 1,000 people and there is a 90% prevalence for the cold virus, that means around 900 people have antibodies to the common cold. If the prevalence of the Covid-19 virus is 2%, roughly 20 of the 1,000 would have antibodies to the Covid-19 virus. Let’s say the serology test has 95% specificity. That means five times out of 100, it will give a false positive, indicating the presence of Covid-19 antibodies when it is really picking up antibodies against the cold virus. What this means is 5% of 900, or 45 people, will test positive for Covid when they have not had it, and are making decisions based on incorrect information. The consequences of being wrong are dramatic and highlight the need for a very good, high-quality serological test.”

How does this relate to Alzheimer’s and other neurological diseases that are ProMIS’ core competency? “In Alzheimer’s, ALS, frontotemporal dementia, Parkinson’s disease and other neurological disease, we’ve been able to use our proprietary, unique technology to identify sites on misfolded proteins that are driving these diseases. Our core technology is the capability to understand what’s special about the bad proteins that are causing these diseases and then we can make antibodies highly selective against them. Our technology allows us to identify a region, an epitopes target, which is a series of four to six amino acids where the protein has misfolded. Not only do we know where this target site is located, importantly we also determine the shape (conformation) of this site. Proteins like amyloid and alpha synuclein and TDP 43 misfold and when these proteins misfold they become toxic, they kill neurons, resulting in disease,” Dr. Goldstein explained.

ProMIS has transferred that thinking to the virus causing Covid-19. “The corona is composed of the spiky protein. Remember, we want to be able to distinguish between the coronavirus causing the common cold and the coronavirus causing Covid-19,” Dr. Goldstein said. “If we can distinguish between the two, we can have an antibody test that’s specific for Covid-19. We are looking at a region of the virus called the receptor binding domain, the RBD, that is part of the spike protein and how it attaches to cells. We have a core competency that allows us to identify sites, and not just the location of the sites, but the shape of the sites on complex protein molecules. That allows us then to use that knowledge to create either antibodies or to create serum tests, or even quite frankly, we can use those targets to create vaccines.”

Using ProMIS’ proprietary technology, the company has been able to “identify a site that we believe is only present on the Covid-19 virus and not on other coronaviruses. We are now initiating the synthesis of several different forms of that site; it’s a small area,” Dr. Goldstein stated. “That would then transfer to Dr. Hans Frykman’s lab at University of British Columbia, a world-class serology lab. Then we will see if the targets we’ve identified are specific and selective antibodies against Covid-19.”

When you test the serum of an individual, if they’ve been exposed to the virus and have the antibodies, “those antibodies should bind selectively and specifically to the target. So if the antibodies from the patient’s serum are binding to the target site, we know it’s a Covid-19 virus because that site is only visible in that shape on the Covid-19 virus and not the others. For the validation of our test, only in patients known to have had Covid-19 should we see binding of antibodies against Covid-19 to our target. The second validation is based on testing in serum from subjects known to have never been exposed to Covid-19 virussuch subjects have antibodies only from cold or other coronaviruses, and therefore the antibody test should be negative; there should be no binding. So we should only see binding in serum from a patient known to have recovered from COVID-19, and we should not see binding in serum from an individual known not to have been exposed to COVID-19,” Dr. Goldstein explained.

“Our technology basically allows us to zero in with sniper-like precision on the structure of a protein and understand it, not only the structure overall but the shape of the regions on that protein and then that allows us to identify what is specific to that protein, in this case the spiky protein on the virus causing COVID-19,” said Dr. Goldstein.

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: ProMIS Neurosciences. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of ProMIS, a company mentioned in this article. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

With the FDA approving Gilead’s Remdesivir as an emergency use treatment for the most acute cases of COVID-19, many people are wondering what type of a drug it is.

Remdesivir is a member of one of the oldest and most important classes of drugs – known as nucleoside analogue. Currently there are more than 30 of these types of drugs that have been approved for use in treating viruses, cancers, parasites, as well as bacterial and fungal infections, with many more currently in clinical and preclinical trials.

I am a medicinal chemist who has worked in design and synthesis of these important drug treatments for over 30 years. I have written numerous reviews over the years about these drugs and their structure and function, and as a result have had many inquiries lately from friends, family and others not in the field asking me to explain what exactly is it about Remdesivir that makes it so effective, but also why it is so interesting. Understanding why means digging into the biochemistry of this class of drugs.

Fake genetic building blocks

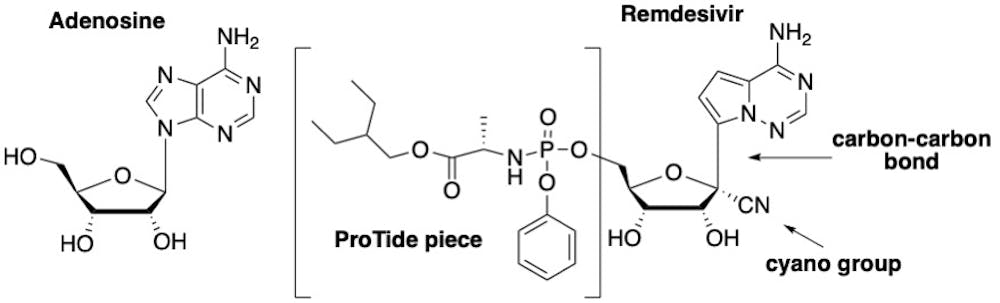

The reason nucleoside analogues and a similar group called nucleotide analogues are so effective is that they resemble the naturally occurring molecules known as nucleosides – cytidine, thymidine, uridine, guanosine and adenosine. These are the essential building blocks for the DNA and RNA that carry our genetic information and play critical roles in our body’s biological processes.

Slight differences in the chemical structure of these analogues from naturally occurring compounds make them effective as drugs. If an organism like a virus incorporates a nucleoside analogue into its genetic material, rather than the real thing, even small changes to the structure of these building blocks prevent the regular chemistry from happening and ultimately foils the ability of the virus to replicate.

The basic structure of a nucleoside includes a sugar group and a base (A, C, G, T or U), and in the case of a nucleotide, a group containing a phosphate which is a collection of oxygen and phosphorus atoms.

The first nucleoside analogues were approved for medicinal use in the 1950s. The early nucleosides had only simple modifications, typically either to the sugar or the base, while today’s nucleosides, such as Remdesivir, typically have several modifications to their structure. These modifications are essential to their therapeutic activity.

How does Remdesivir work as antiviral therapeutic?

This activity occurs because nucleoside/tide analogues mimic the structure of a natural nucleoside or nucleotide such that they are recognized by, for example, viruses. Due to those structural modifications, however, they stop or interrupt viral replication, which stops the virus from multiplying and infecting more cells in the body.

As a result, they are known as direct-acting antivirals, and this is the case for Remdesivir, which works by blocking the coronavirus’s RNA polymerase – one of the key enzymes that this virus needs to replicate its genetic material (RNA) and proliferate in our bodies. Remdesivir works when the enzyme replicating the genetic material for a new generation of viruses accidentally grabs this nucleoside analogue rather than the natural molecule and incorporates it into the growing RNA strand. Doing this essentially blocks the rest of the RNA from being replicated; this in turn prevents the virus from multiplying.

The drug Remdesivir is basically an altered version of the natural building block adenosine – which is essential for DNA and RNA. Comparing the structure of Remdesivir with adenosine, one can see there are three key modifications that make it effective.

The first is that Remdesivir, as it is administered, is not the actual active drug; it is actually a “prodrug,” meaning it must be modified once in the body before it becomes an active drug. Prodrugs are used for many reasons, including protecting a drug until it reaches its site of action. The active form of Remdesivir contains three phosphate groups; it is this form that is recognized by the virus’s RNA polymerase enzyme.

A naturally occurring nucleotide (left) which is a building block of RNA and DNA and Remdesivir (right) which is a variation on its natural counterpart. Katherine Seley-Radtke, CC BY-SA

The second important modification on Remdesivir is the carbon-nitrogen (CN) group attached to the sugar. Once Remdesivir is incorporated into the RNA growing chain, the presence of this CN group causes the shape of the sugar to pucker, which, in turn, distorts the shape of the RNA strand such that only three more nucleotides can be added. This terminates the production of the RNA strand and is what ultimately sabotages the replication of the virus.

The third important structural feature which makes Remdesivir differ from adenosine is the change of one particular chemical bond on the molecule. Rather than a bond linking a carbon and nitrogen atoms, chemists replaced the nitrogen with another carbon, creating a carbon-carbon bond. This is critical to the success of this drug because coronaviruses have a special enzyme that recognizes unnatural nucleosides and clips them out. But by changing this chemical bond, Remdesivir cannot be removed by the enzyme, allowing it to stay in the growing chain and block replication.

Remdesivir trials

Remdesivir originally was found during a drug discovery program at Gilead to search for inhibitors of the hepatitis C virus, which is another RNA virus. Although Gilead ultimately selected a different nucleoside analogue for treatment of hepatitis the company tested the drug to see if it was effective against other RNA viruses. Remdesivir exhibited potent activity against Ebola and Middle Eastern respiratory virus, among others.

According to the NIH, patients who received Remdesivir had a faster recovery compared to those who received placebo; 11 days compared with 15 days for those who received the placebo. “Results also suggested a survival benefit, with a mortality rate of 8.0% for the group receiving Remdesivir versus 11.6% for the placebo group,” according to the NIH press release.

While these results are preliminary, there are a plethora of clinical trials underway across the world. Regardless, a certain amount of caution is still needed. As noted by Dr. Anthony Fauci on NBC’s “Today” show, “the antiviral drug Remdesivir is the first step in what we project will be better and better drugs coming along” to treat COVID-19, but cautioned, “This is not the total answer.”

I share this view with many other scientists in the field. No matter what those results ultimately show, Remdesivir will mostly certainly be part of a cocktail of drugs, just as is standard for treating other viruses such as HIV and hepatitis C.

A combination, or cocktail, of drugs will provide a more effective and more complete therapy that blocks the virus from replicating. The other benefit of such a drug cocktail is that it lowers the chance the virus will develop resistance to the therapy. In the meantime, these early results for Remdesivir are proving to be an important source of hope for many of us across the world as we wait for this pandemic to subside.

But with coffee shops closing worldwide, the coronavirus crisis is testing Rwanda’s top export.

COVID-19 and coffee in Rwanda

Rwanda appears to have been successful in keeping COVID-19 at bay so far. The Central African country of 12 million reported just over 250 cases as of early May.

To analyze the effects of COVID-19 restrictions on Rwanda’s coffee industry, we drew on information from our five-year research project funded by the U.S. Agency for International Development and interviewed local collaborators and international industry experts.

As a critical sector of the Rwandan economy, coffee is a sensitive topic in the country, so our contacts in Rwanda preferred to speak anonymously. The quotes included here are drawn from our interview notes and their accuracy checked with our sources.

Our analysis finds that health restrictions are increasing coffee production costs in Rwanda and introducing delays to the global supply chain that consumers halfway across the world may eventually feel.

Open but restricted

Rwandan coffee farmers must adhere to social distancing guidelines during the May harvest, keeping coffee pickers one meter apart. As a result, according to two Rwandan coffee sector experts who work with farmers, they are hiring fewer workers. That may increase the time it takes to pick the same acreage.

Since not all workers in the coffee sector are considered essential, Rwanda’s strict travel restrictions are also slowing coffee’s journey from farm to cup.

“I cannot even legally drive out to our roastery, even though it is just a few kilometers away,” the manager of one Rwandan coffee roasting facility told us.

To avoid contact between buyers and farmers, some processing mills – which prepare fresh coffee beans, or “cherries,” for export and roasting by removing the skin and pulp – are asking farmers to deliver their harvest themselves, rather than send trucks for pickup.

Few farmers in Rwanda own cars or motorcycles – less than 3%, based on our research. So they must deliver their coffee on foot, traveling on average 3.5 miles. A round trip that normally takes minutes may now take two hours.

Once the coffee reaches the mill, hurdles to processing arise.

“My company has two agents who are allowed to travel to mills to oversee operations, but they must be tested for COVID-19” at police checkpoints when entering a new district, a Rwandan coffee buyer told us.

Sorting and milling of coffee is also likely to take substantially longer due to decreased staffing in compliance with social distancing regulations.

To keep on-site workers safe, mills are setting up hand washing stations and distributing hand sanitizer, but many are struggling to get required protective equipment like face masks, which have surged in price due to increased demand.

Vista of Rwandan coffee country. Andrew Gerard, CC BY

“We are preventing the economic activity that can reactivate the economy of coffee-producing regions,” warned Roberto Vélez Vallejo of Colombia’s National Federation of Coffee Growers – which sells coffee under the brand Juan Valdez – via Tweet.

To overcome such challenges, Rwanda’s coffee farmers are turning to mobile technology.

Now, co-op leaders are using text messaging to share information about coffee prices, social distancing protocols and other coronavirus-related topics with members.

Shifting demand

Neither technology nor unions can solve what is perhaps the biggest problem facing Rwandan coffee’s industry: a global coffee market in upheaval.

Across the United States and Europe – which together import over 60% of the world’s coffee – COVID-19 containment measures have shut down cafes, shifting where demand is located.

In the U.S., which has a US$47.5 billion coffee shop industry, about a quarter of coffee consumption normally takes place away from home. Recently, this figure has come close to zero.

To serve coffee drinkers stuck at home, roasters must pivot to online and grocery sales – a difficult transition, especially for small players competing with chains like Starbucks.

International uncertainty is trickling down to Rwandan farmers in the form of broken contracts. One major Rwandan coffee exporter told us several buyers had either reduced or delayed finalizing their planned purchases.

Ruth Church, of the U.S.-based Artisan Coffee Importers, which specializes in Rwandan coffee, said she worried her clients would reduce orders too, but has since gotten confirmation that they will maintain last year’s purchasing levels.

“That comes from the relationship they’ve been able to form with the farmer,” she said of her buyers. “They know producers are vulnerable.”

But, Church warned, “Others may be forced to cancel or reduce.”

Rwandan coffee is adapting to get coffee to market. Now they hope someone will buy it.

Bridget Vuguziga, an independent consultant based in Kigali, Rwanda, contributed to this analysis.