UK Prime Minister, Boris Johnson, on Sunday announced his plans for restarting the UK economy, with the easing of lockdown measures set to kick in as early as Wednesday. The government also announced its fewest Covid-19 deaths since March, which is offering greenshoots of hope that the worst of the outbreak has passed.

Such expectations are pushing the Pound higher against most Asian currencies as well as its G10 peers, including the US Dollar, Japanese Yen, and the Euro.

Yet, Brexit risks loom

Although the Pound is getting a slight lift to kick off the week on hopes that the UK economy can return to some form of normality in the not-too-distant future, that narrative may give way to the Brexit theme that has been an ever-present driver for Sterling in recent years. Brexit talks are set to resume this week between UK and EU negotiators, which leaves the Pound exposed to possible bouts of volatility which markets aren’t yet preparing for.

The Pound-Dollar risk-reversal spread between the one month and nine month contract appears flat at the time of writing. This suggests that markets are underpricing the prospects of Brexit-related volatility in Sterling, even as key deadlines loom.

The UK government has until June 30, which is less than two months away, from changing its mind on the end-2020 date for this Brexit transition period. Should the UK enter 2021 without a deal with the EU, the economic ramifications on the UK could severely hamper its attempted recovery from the coronavirus pandemic.

Such downside risks, if realized, are likely to add to the Pounds woes, potentially exacerbating GBPUSD’s 6.22 percent year-to-date decline.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The Government of Argentina intends to raise export duties on soybeans

Argentina is the third largest soybean producer in the world after the United States and Brazil. It is the world’s main exporter of soybean meal and oil. Note that, according to forecasts, in the 2019/20 agricultural season, the soybean crop in Argentina will drop by 5.8 million tons to 49.5 million tons, compared with the previous season. Global consumption may increase. FutureBridge Consulting Company expects growth in the global vegetable protein market by 20% in 2020-2022. The United States Department of Agriculture (USDA) forecasts an increase in soybean demand in China in 2020 up to 89 million tons, which is 7.8% more than in 2019.

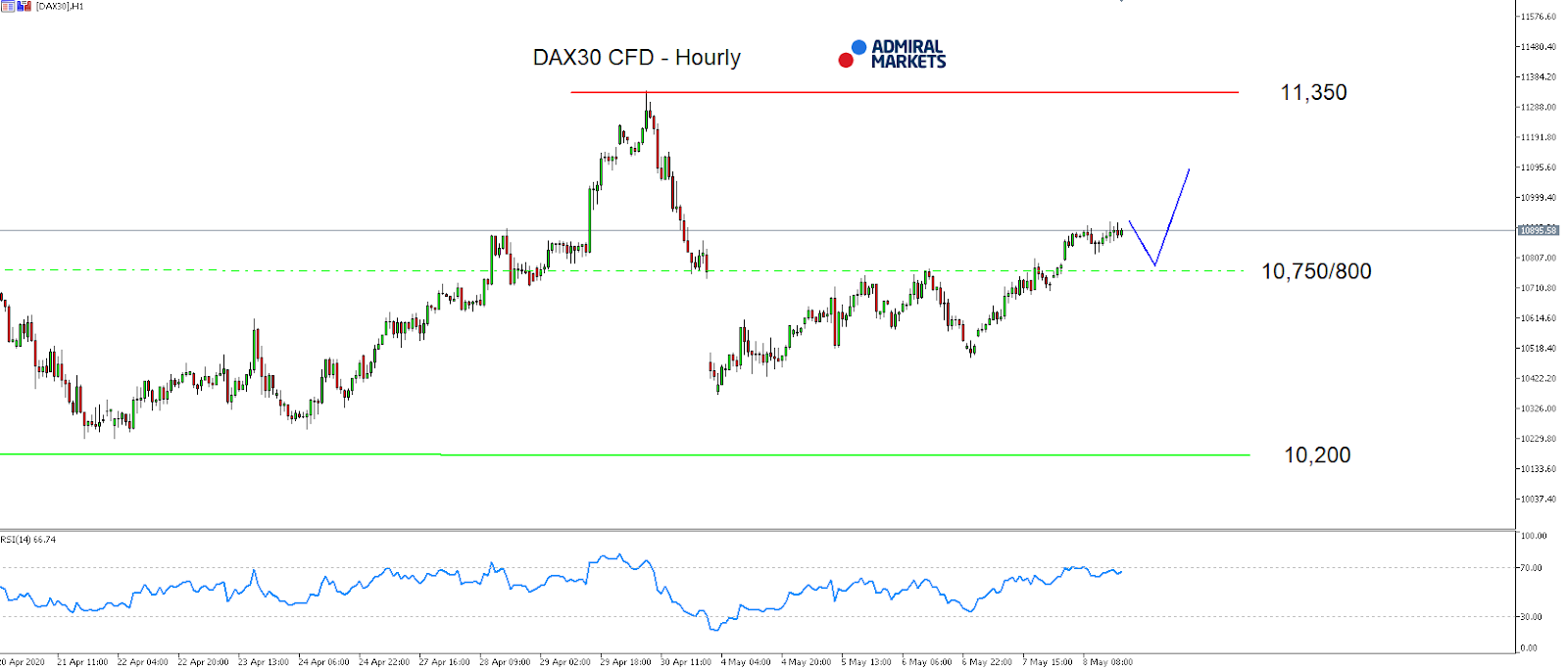

The DAX30 shrugged off the initial shock of Tuesday’s German Constitutional Court’s ruling last Tuesday, deciding that some ECB actions in regards to asset purchases regarding the QE are unconstitutional and thus not valid in Germany since ECB decisions are not backed by the EU treaty, and brought the mark of 11,000 points into focus for the DAX30 into the last weekly close.

The driver probably came from not only increases in optimism in regards to the reopening efforts of the Corona lockdown, especially in the US.

But also that recent built trade tensions between the US and China eased a little. Beijing and Washington discussed their Phase 1 trade deal in a telephone call, with China agreed to improve the atmosphere for its implementation and the US promising both countries expected obligations to be met.

If the break above 10,800 points now proves sustainable, a test of the psychologically relevant region around 11,000 points seems likely, probably even a run as high as 11,250/300 points.

A solid support and potential long trigger can be found around 10,800 points, while a drop back below 10,800 and thus back into the neutral zone between 10,200 and 10,800, identifies the push back above 10,800 points as a fake out:

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Hourly chart (between April 20, 2020, to May 8, 2020). Accessed: May 8, 2020, at 10:00pm GMT

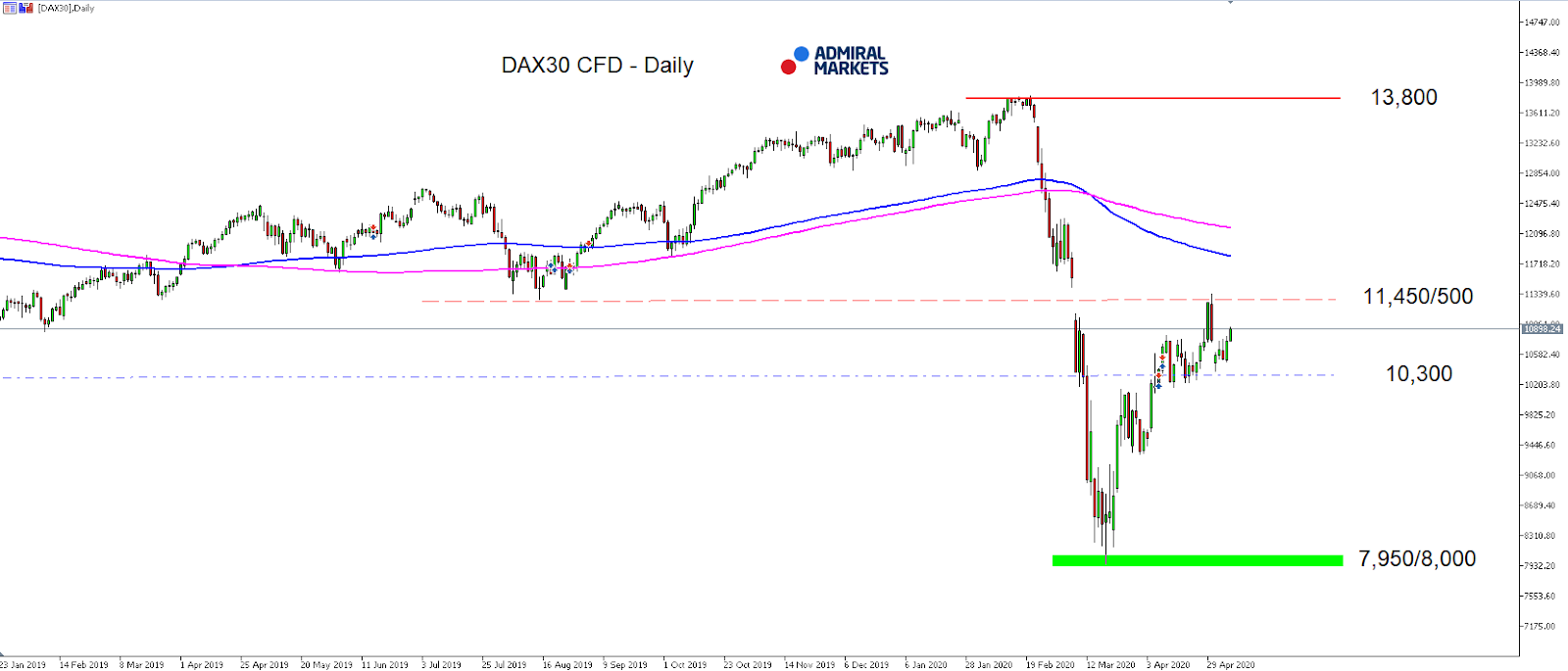

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Daily chart (between January 23, 2019, to May 8, 2020). Accessed: May 8, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the DAX30 CFD increased by 9.56%, in 2016, it increased by 6.87%, in 2017, it increased by 12.51%, in 2018, it fell by 18.26%, in 2019, it increased by 26.44% meaning that after five years, it was up by 34.2%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

Investors in Asia kicked off the week in an upbeat mood, with most major equity indices trading in positive territory. The upside momentum seems to be a continuation from Friday’s Wall Street session which saw the S&P 500 adding 1.7% and the Nasdaq Composite erasing all losses for the year following a 37.5% rally from its March trough.

Charts of US major indices are already reflecting a V-shaped recovery with the Nasdaq Composite only 7.9% short of its record high and the S&P 500 15.8% below its peak.

For many investors, the divergence between Wall Street and Main Street does not make a lot of sense especially as it seems to be widening. No figures in history match Friday’s non-farm payrolls report, which showed a record 20.5 million jobs losses for April and unemployment reaching 14.7%. According to US Treasury Secretary Steven Mnuchin, the unemployment rate may now be closer to 25%.

While we all know that financial markets are forward-looking and much support has been received from monetary and fiscal policies, what we are experiencing now is investors falling into a behavioural bias known as ‘Narrative Fallacy’. Narrative fallacy limits our ability to evaluate information objectively, hence we make irrational decisions. Humans can easily fall into this bias as we love stories, and the great story right now is economies are gradually restarting with lockdowns being lifted.

While we all hope that we swiftly return to pre-Covid19 economic activity, the facts will most likely prove us wrong. Today we are starting from an incredibly low activity base. Tens or possibly hundreds of millions of jobs are already lost globally, and many will not return in a matter of months. Even for those who are still on payrolls, there is a high likelihood of elevated levels of savings curbing demand. That is still not taking into consideration a second coronavirus wave that could lead to new lockdowns if no proper treatment or vaccine is discovered yet.

How long risk assets supported by unconventional policies can defy the real economy remains an open question for now. But from where valuations are standing, it seems a lot of the good news is already priced in, and in my opinion, the best-case scenario is to see some sort of consolidation around current levels. Until confidence returns to the real economy, the rally in risk assets will not be sustainable and investors will need to reconsider their positions at some point soon.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Equity markets’ rising is intact today after Sunday reports President Trump’s administration was holding discussions with Republicans and Democrats in Congress on potential aid to states after April jobs report indicated unemployment jumped to 14.7% due to US job losses unseen since the Great Depression of the 1930s. The White House is “absolutely” pushing for a payroll tax cut, Treasury Secretary Mnuchin said, despite little congressional support for the proposal.

Forex news

Currency Pair

Change

EUR USD

-0.02%

GBP USD

-0.59%

USD JPY

+0.05%

AUD USD

+1.45%

The Dollar weakening reversed today ahead of inflation report due later in the afternoon. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, edged down 0.1% to 99.75 Friday as Labor Department reported unemployment rate jumped to 14.7% from 4.4% in previous month. Both the EUR/USD and GBP/USD continued rising Friday despite report German exports plunged above expected 12% in March, the steepest drop in since 1990. Both pairs are lower currently. USD/JPY and AUD/USD continued climbing on Friday with the dynamics intact for both pairs currently.

Stock Market news

Indices

Change

Dow Jones Index

+0.11%

Nikkei Index

+2.68%

Hang Seng Index

+0.6%

Australian Stock Index

+0.29%

Futures on three main US stock indexes are advancing currently after closing sharply higher on Friday. More companies including Uber, Mitsubishi Electric and Hitachi will report quarterly results today. Stock indexes in US ended higher on Friday : the three main US stock indexes recorded gains ranging from 1.6% to 1.9%. The SP500 currently trades at more than 22 times expected 12-month earnings, according to FactSet. That is a level not seen in roughly 20 years while companies are unwilling to provide guidance on future performance due to heightened uncertainty. European stock indexes are extending gains currently. Asian indexes are mostly rising today with Hong Kong’s Hang Seng index ahead gaining 1.6% currently.

Commodity Market news

Commodities

Change

Brent Crude Oil

-0.78%

WTI Crude

-2.45%

Brent is edging lower today. Oil prices ended higher last session as the Organization of the Petroleum Exporting Countries and its allies, collectively known as OPEC+, have started cutting production by 9.7 million barrels a day in May and June. The US oil benchmark West Texas Intermediate (WTI) futures ended higher Friday: June WTI gained 5.1% but is falling currently. July Brent crude closed 5.1% higher at $30.97 a barrel on Friday, booking a 17.1% gain for the week.

Gold Market News

Metals

Change

Gold

-0.25%

Gold prices are extending losses today. June gold lost 0.7% to $1713.90 an ounce on Friday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

This week – May 10 through May 16 – central banks from 5 countries or jurisdictions are scheduled to decide on monetary policy: Moldova, New Zealand, Belarus, Egypt and Mexico.

Romania’s central bank was originally scheduled to decide on monetary policy on May 12 but its board decided on March 20, when it cut the rate 50 basis points at an emergency meeting, to suspend scheduled monetary policy meetings “given the high degree of uncertainty” surrounding economic and financial developments.

Instead, the central bank’s board will meet to decide monetary policy when necessary.

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

Shares of ION Geophysical traded higher after the company reported Q1/20 financial results that included a 53% year-over-year increase in revenue.

Oil and gas technology services and solutions company ION Geophysical Corp. (IO:NYSE) yesterday afternoon announced financial results for Q1/20 ending March 31, 2020.

The firm reported total net revenues of $56.4 million in Q1/20, which represented a 53% increase over $37.0 million in Q1/19. The company advised that the increase was due primarily to an increase in 2D multi-client data library sales.

For Q1/20, the firm additionally reported operating income of $6.3 million, compared to an operating loss of $15.9 million in Q1/19. The company further indicated that in Q1/20, it posted a net loss of $2.3 million, or ($0.16) per share, compared to a net loss of $21.4 million, or ($1.52) per share in Q1/19.

The company’s President and CEO Chris Usher commented, “We achieved the best first quarter performance in six years despite challenges from both coronavirus and oil price volatility…Our strong revenues of $56 million generated positive operating income and $23 million in Adjusted EBITDA, and, as a result, we expect our liquidity position to improve as revenues are collected in the second quarter. Our first quarter results reflect the value of our offshore data library and validate the combined effectiveness of our strategic refocus and over $20 million cost reductions. Our team creatively closed a number of large multi-client contracts, some of which were delayed from the fourth quarter, even after E&P market dynamics changed. I remain confident in ION’s value proposition to cost-effectively support customers’ data-driven decision-making in this lower-for-longer exploration and production environment.”

The company indicated that it has maintained a strong liquidity position in the face of energy market turmoil and the COVID-19 situation. The firm stated that as of March 31, 2020, it had total liquidity of $53.8 million, which consisted of $42.7 million in cash and $11.1 million remaining available balance under its $50.0 million revolving credit line.

ION Geophysical Corp. is a technology-focused company headquartered in Houston, Tex. that provides geophysical technology, services and solutions to the global oil and gas industry. Its products and technical services are designed to help oil and gas exploration and production companies obtain images of the earth’s subsurface.

ION Geophysical started off the day with a market capitalization of around $25.1 million and an enterprise value of $115.7 million with approximately 15.03 million shares outstanding and a short interest of about 6.40%. IO shares opened more than 100% higher today at $3.37 (+$1.70, +101.80%) over yesterday’s $1.67 closing price. The stock has traded between $2.84 to $4.36 per share today and is currently trading at $2.88 (+$1.21, +72.46%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

A recap of Parsley Energy’s Q1/20 performance and projections for this year and next are given in a Raymond James report.

In a May 5 research note, analyst John Freeman reported that Raymond James increased its target price on Parsley Energy, Inc. (PE:NYSE) after it posted its Q1/20 numbers.

Raymond James’ new target price on Parsley is $12 per share, up from $11. The Texas-based energy company’s stock is trading now at about $9.38 per share.

Freeman reviewed and commented on Parsley’s Q1/20 results. The company “delivered modest EBITDA and earnings per share beats relative to the Street” due to oil pricing,” Freeman pointed out.

Production was relatively in line at 126,600,000 barrels of oil per day (126.6 MMbbl/d), which was 1% higher than consensus’ forecast but 1% below Raymond James’ estimate. Total production was 1% above the Street’s projection but 3% below Raymond James’ forecast.

“The performance on the quarter was encouraging, however, the highlight from earnings was the significant reduction in 2020 capex (down from about $1 billion to less than $700 million),” Freeman commented.

Capex, “a welcome surprise,” Freeman wrote, came in 5% and 7% lower than the investment bank and the Street’s estimates, respectively. Opex was 3% under Raymond James’ projection

Moreover, Parsley’s related maintenance capital needs were greatly below expectations as well, indicating that Parsley made capital efficiency gains during the period.

“We were pleasantly surprised that Parsley is able to maintain in line Q4/20 oil volumes (about 115 MMbbl/d) on a capital program that’s about $300 million/30% below the Street,” added Freeman.

Looking forward, Raymond James modeled a base case, or stable scenario for Parsley, that implies a West Texas Intermediate oil price of about $30 a barrel and Parsley having four to five rigs and one to two crews operating. In that scenario, Parsley would produce about 117 MMbbl/d in 2020 and 115 MMbbl/d in 2021.

Capex would amount to about $678 million in 2020, dropping to $598 million in 2021.

Free cash flow would be about $300 million in 2020, which coincides with Parsley’s guidance of $300M plus, and increasing to $370 million in 2021.

Raymond James has an Outperform rating on Parsley Energy.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Raymond James, Parsley Energy Inc, May 5, 2020

ANALYST INFORMATION

Analysts Holdings and Compensation: Equity analysts and their staffs at Raymond James are compensated based on a salary and bonus system. Several factors enter into the bonus determination, including quality and performance of research product, the analyst’s success in rating stocks versus an industry index, and support effectiveness to trading and the retail and institutional sales forces. Other factors may include but are not limited to: overall ratings from internal (other than investment banking) or external parties and the general productivity and revenue generated in covered stocks.

The analyst John Freeman, primarily responsible for the preparation of this research report, attests to the following: (1) that the views and opinions rendered in this research report reflect his or her personal views about the subject companies or issuers and (2) that no part of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views in this research report. In addition, said analyst(s) has not received compensation from any subject company in the last 12 months.

RAYMOND JAMES RELATIONSHIP DISCLOSURES Certain affiliates of the RJ Group expect to receive or intend to seek compensation for investment banking services from all companies under research coverage within the next three months.

Raymond James & Associates, Inc. makes a market in the shares of Parsley Energy, Inc.

Additional Risk and Disclosure information, as well as more information on the Raymond James rating system and suitability categories, is available here.

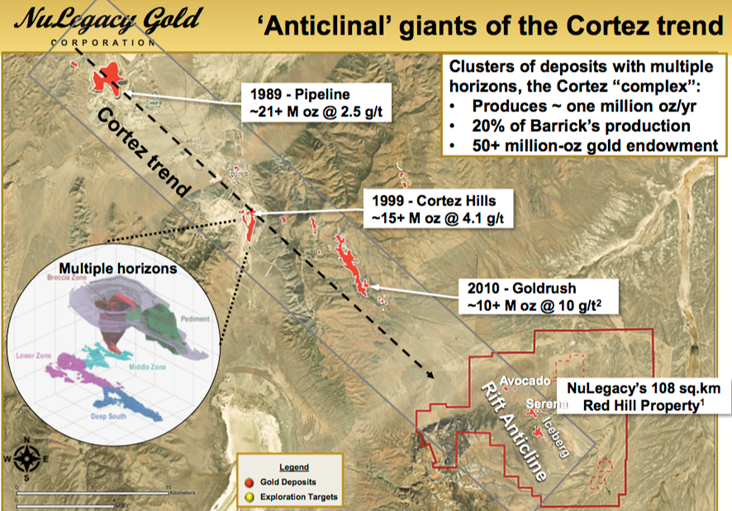

Peter Epstein of Epstein Research looks into the Gross Overriding Royalty that just changed hands on the company’s flagship Red Hill project, and discusses what it means for the firm.

In late April, Metalla Royalty & Streaming acquired two royalties, one of which was a Gross Overriding Royalty (GOR) on NuLegacy Gold Corporation (NUG:TSX.V; NULGF:OTCQX) flagship Red Hill project, a Carlin-style deposit in Nevada’s world-famous Cortez trend.

To be clear, this was a transaction between Metalla and a private company; no cash or other remuneration flowed to NuLegacy. However, this news is still exciting and thought provoking as it pertains to a potential (implied) valuation of Red Hill. So much so, thatCEO/director of Finance and MarketingAlbert Matter put out this press release highlighting it. {corporate presentation}

Metalla’s news is applicable to NuLegacy for a number of reasons. Let me start by saying I know the Metalla team, I’ve written about the company several times (although not recently).

This is a smart, hard-working, market-savvy group, with global experience, integrity and expertise. When dealing in streams and royalties, it’s all about industry connections, market knowledge and deal flow. Metalla has that and is up to its eyeballs in deal flow (deals it can make or pass on).

Takeaways on implied valuation of NuLegacy’s Red Hill project?

That’s why this news is so interesting. It represents a reliable, unbiased vote of confidence in NuLegacy’s Red Hill project. I was able to track down the president, CEO and a director of Metalla, Mr. Brett Heath, to ask him about his team’s view of NuLegacy, their management and technical teams, and the Red Hill project,

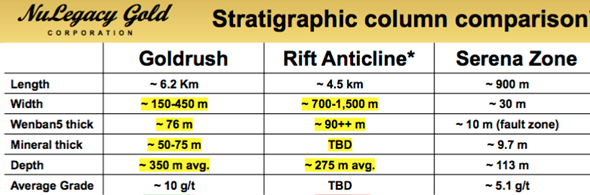

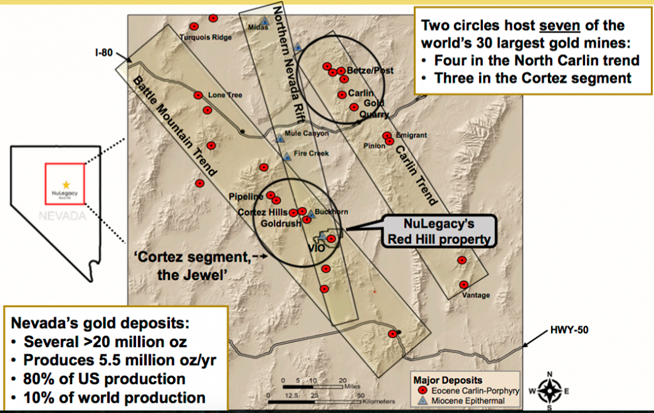

“The Red Hill project is very interesting due to its location & position within the Cortez trend of Nevada that hosts globally significant mines & projects, specifically Cortez Hills, Pipeline & Goldrush. Although many near-surface deposits have been discovered, several blind deposits similar to Goldrush have yet to be found.

“NuLegacy’s Rift Anticline is a promising new drill target, a chance to discover a large, high-grade deposit. The close proximity of Red Hill to Goldrush heavily influenced our understanding of the geology at Red Hill. Specifically, it allowed us to better understand that the Rift Anticline has similar stratigraphy to Goldrush, and similar mineralization events nearby.”

Investors, shareholders and analysts are trying to figure out what (if any) read-throughs there are in terms of the valuation of the Red Hill project.

From the press release:

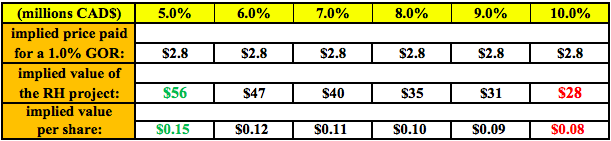

“Valuing Gross Overriding Royalties (“GORs”) is a complicated business made easier in this instance by the straightforward nature of the [transaction] . prorating the US$4 million purchase price for the total of 2% GOR that was acquired . values a 1% GOR in the Red Hill project at ~US$2 million.”

What this valuation exercise boils down to is how does the value of a 1% GOR compare to a conventional working interest in the same project? GORs are highly case specific, so I will give a range of possibilities. Many factors make GORs unique, but a rule of thumb is that a 1% GOR equates to a 5% working interest.

However, due to the unknown terms of this particular GOR, let’s assume that the 1% GOR is equal to between a 5% and 10% working interest. By extending the range higher than 5%, more conservative valuations for Red Hull are obtained. In the chart below one can see that the implied ~US$2 million paid for a 1% GOR equals C$2.8 million at the current exchange rate.

Therefore, Red Hill’s indicative valuation could be viewed as C$28 million to C$56 million, or C$0.08 to C$0.15 per share. Currently, the stock’s trading at C$0.07. The company has a cash balance of C$4.5 million. {see corporate presentation}. I believe the C$0.08 to C$0.15/share range is conservative because Metalla’s purchase of the GOR had a built-in profit expectation. The true ascribed value of a 1% GOR on the Red Hill project might be higher than C$2.8 million.

A true vote of confidence in NuLegacy Gold

Perhaps more important than an implied (subjective) valuation of Red Hill are the following takeaways. First, Metalla not only likes Red Hill, it must also feel good about the long-term prospects for Nevada and the U.S. Metalla looks at hundreds of deals a year from all over the world. Management can, and does, invest in dozens of jurisdictions.

Yet, in April 2020, it chose the U.S., . Nevada . the Cortez Trend . Second, it chose a project that’s pre-maiden resource. Remember, Metalla has paid out ~C$2.8 million, but doesn’t make a penny of that back unless it re-sells some or all of the GOR it acquired, or Red Hill reaches commercial production. Therefore, I argue that investing at this relatively early stage is a stamp of approval in the extensive work done to date at Red Hill.

That Metalla chose to deploy capital in a gold asset rather than a silver asset, despite the gold-silver ratio being near an all-time high (over 110 to 1) seems promising. Finally, it chose the U.S. at a time when the currencies of Mexico, Australia, Canada and others have weakened considerably vs. the U.S. dollar, making exploration cheaper in those countries. One must have conviction to choose Red Hill over dozens of public and private, pre-maiden resource, projects around the globe.

In the end, a good project in a great jurisdiction is only as prospective as its technical/management teams. NuLegacy has prudently advanced Red Hill in good times and bad. For most of NuLegacy’s existence, the gold price traded between about $1,050 and $1,400/oz.

Gold price at $1,730/oz. is a game-changer .

Now gold is hovering around $1,730/oz after almost touching $1,800/oz in March. This is a game-changer for juniors like NuLegacy that have tremendous blue-sky potential, (look at neighboring mines and development projects, some of the best on the planet) but like most juniors, have limited funding to conduct aggressive drill programs in a strong gold price environment.

A savvy company betting on the Red Hill project is yet another indication that the time has come for precious metal players to become more active in M&A.

The day that Barrick commits its deep experience (and deep pockets!) to NuLegacy’s Red Hill, all royalties held on that project would soar in value. Why? The timeline to potential production would be shortened, perhaps by years, (more drilling, less investor hand holding, perhaps skipping a PEA or a PFS). The scope of the project would become largermore drilling across a wider footprint (a 108 sq. km land package).

The value of the royalties could double, triple, quadruple . who knows? The share price at which NuLegacy gets taken out could also be meaningfully stronger. After all the company has been through, I don’t think the Board would sell the company below C$0.30/share. At least not with the gold price at $1,730/oz (or higher). Readers are reminded that C$1.5 billon OceanaGold Corp. & giant natural resources fund Tocqueville own a combined 21.5% of the company.

Might there be a bidding war for NuLegacy?

In a best case example then, there could be multiple bidders for NuLegacy. This is not nearly as crazy as it sounds, especially if the gold price keeps going up, or if the next (fully funded) drill program hits the mark. If Barrick were to make a move, OceanaGold, Newmont, or even Tocqueville (they could hold out for higher price) might have something to say about it.

Those entities, and/or other mid-tiers/majors in Nevada or around the world would keep Barrick honest. Over the years NuLegacy has been in touch with several well-known names, but I never know who they’re talking with at any given time. Make no mistake, Barrick is best positioned by virtue of having the most synergies with Red Hill, so it can afford to pay several more pennies per share if need be. That’s how a share price of C$0.30+ becomes possible.

Bottom line, NuLegacy Gold (TSX-V: NUG) / (OTCQX: NULGF) is a high-risk exploration play, but I believe a good speculation. There’s no better time to be buying high-risk exploration than when the prices of the metals being explored for are moving up.

As more attention is drawn to NuLegacy, its team, the undisputed safety of Nevada, the prolific nature of the Cortez Trend, etc., I think there’s compelling relative and absolute value here that readers should consider investigating further.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about NuLegacy Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of NuLegacy Gold are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, NuLegacy Gold was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Metalla Royalty & Streaming and Newmont Goldcorp, companies mentioned in this article.

While the broader markets have seen sharp declines, Frank Holmes, CEO and chief investment officer of U.S. Global Investors, homes in on gold, gold stocks and bitcoin, and gives his prognosis for the airlines.

Streetwise Reports: Let’s start with gold, which has seen an impressive rise in the last few months as the broader markets have declined on the back of the coronavirus pandemic. What do you think is ahead for the metal?

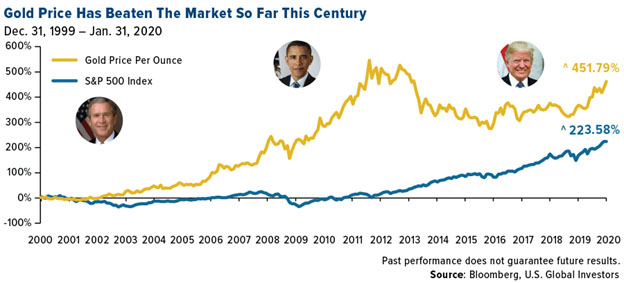

Frank Holmes: There is a short-term view and a long-term view. What’s really hard for so many investors and asset allocators to recognize is that gold bullion since 2000 has far outperformed the S&P 500. In fact, of the last 20 years, in 16 of those years gold has been positive. So if we look at the numbers, it’s double what the S&P 500 has done for the past 20 years.

With gold, there’s the fear trade and the love trade. The love trade is 60% of the demand and it is long-term demand. The fear trade is short-term demand, and it’s about 40%. Right now, we’re living with fear that’s really dominating the markets. The two factors that go with that are negative real interest rates and the amount of debt being printed by the government. So whenever you have the combination of a rising Fed balance sheet with Quantitative Easing 1, 2 and 3, buying junk bonds, whatever they’re doing in the stock markets to try and provide liquidity, as that flows dramatically so does the price of gold.

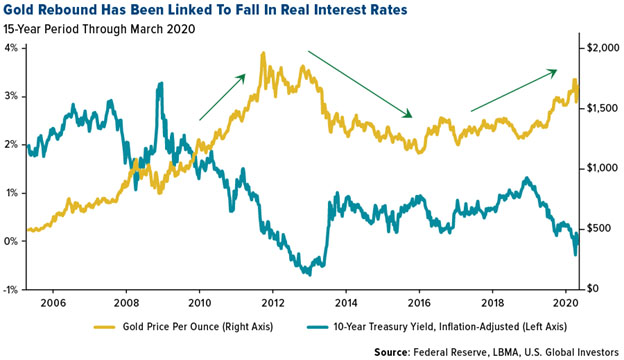

Typically and most significant, in every country in the world we have found that when you have negative real interest rates, gold goes up in that country’s currency. Take the yield on 10-year government bonds and subtract the monthly Consumer Price Index (CPI) number; if it’s a positive return, gold is not attractive as an asset class. But if it’s a negative real rate of return, gold appreciates in that country’s currency.

When gold went to $1,900 in September of 2011, the 10-year government bond had a negative real rate of return of -300 basis points. Then five years later, the price of gold went down to $1,100 and real interest rates were +2% over the CPI number. So you had a variant swing from -3 to +2, which is 500 basis, and that’s why gold corrected. Since then, we’ve had these periods now, and particularly in the past year, of negative real interest rates in America. That’s how gold started staging a rally, which started about this time last year, peaked in August, sold off and now it’s coming back again.

The Federal Reserve said recently it’s going to keep rates basically at 0. The CPI is still running more than 1%. In fact, we could get big food inflation, the way it looks, for beef, chicken, etc. Inflation could have a big impact on negative real interest rates, and gold is moving higher.

So short term, it’s all about real negative interest rates. As long as they stay negative, then we’re going to see gold go up in the U.S. dollar. It could go up against the euro, against any country’s currency.

I mentioned earlier that 60% of gold demand is love, and it predominantly comes from China and India. China and India are 40% of the world’s population, and if you throw in the Middle East and Southeast Asia, we’re now talking about 50% of the world’s population. They give gold for weddings and for birthdays, and there’s a strong correlation of rising gross domestic product (GDP) per capita in those countries for the past 20 years, and rising gold consumption.

China and India comprise approximately 50% of the world’s gold demand GDP per capita. Indian women wear six times the amount of gold on their bodies than what is in Fort Knox, and they predominantly wear 24 karat, minimum 22 karat, gold jewelry. It’s protected them from bad governments and bad government policies.

SR: What do you see happening with silver?

FH: Silver has more industrial applications than gold, so silver is like a warrant on gold. If a stock takes off and there’s an option or a warrant in the money, it explodes and goes up much more percentage-wise. It has greater volatility. Every 10% move in gold usually translates to a 15% move in silver, up or down. And with this fear that’s been taking place with negative interest rates and the calamity of money printing around the world, what we see now is that silver didn’t move at first. Silver has always lagged.

SR: Do you recommend that the individual investor hold gold bullion?

FH: Yes. I think the easiest way is the SPDR Gold Trust (GLD). Or if you want to buy the physical gold insured, go to a reliable site like Kitco, and you can take physical delivery.

There is a company called Mene Inc. (MENE:TSX.V; MENEF:OTCMKTS) at mene.com. It sells 24-karat gold jewelry with only a 10% markup. And it will buy back your gold jewelry at a 10% discount to the price of gold if you ever want to sell it back. That’s the business model. It will deliver throughout the U.S., I think using Brinks for delivery of simple gold jewelry.

SR: Let’s talk about bitcoin for a moment and how that fits into a portfolio.

FH: I am the chairman of HIVE Blockchain, which became the first real cryptomining company. We are mining using green energy, surplus energy in Iceland, Sweden and now Quebec, which sells electricity to New York state. Quebec has a surplus of it. So we started mining these coins.

What I found is that the Bitcoin is very different than Ethereum. Bitcoin is going to become, to me, like Andy Warhol’s art. If you look at the original paintings of Marilyn Monroe or Elvis Presley, when he came out with his prints in different colors, they came out at $1,000, went up to $10,000, fell, went up to $50,000, fell, went up to $100,000 and went to $125,000because there are just more people, widened GDP, over time, and then they become art collectors. I think that if you have an original Bitcoin that’s never been traded, it’s going to be in that space.

The other part is that cryptocurrency is very new, and digital money is going to only grow. Blockchain technology is a superior piece of technology. What we saw was that Bitcoin bottomed a little over a year ago. Then it rallied, it went up to $14,000. All the central banks got worried. They knocked it down, and it’s making a comeback.

Bitcoin, in mid-May, is going to halve production. There’s a limited number of Bitcoins allowed to be ever created. The methodology when you mine them is you get new Bitcoins. They’re called genesis or virgin coins. The number of coins you get every time you mine is going to halve. So the supply is going to shrink dramatically. A thought process with that is that Bitcoin will trade higher, probably above $10,000. Bitcoin is very speculative, just like buying Andy Warhol’s art early.

I think that anyone who looks at Bitcoin or Ethereum must recognize that the daily volatility is four times the S&P 500 and gold. Thirty percent of the time gold or the S&P can go up or down 1%. For Bitcoin and Ethereum, it’s 45%. Cryptocurrency is a huge secular trend, but it’s going to be volatile.

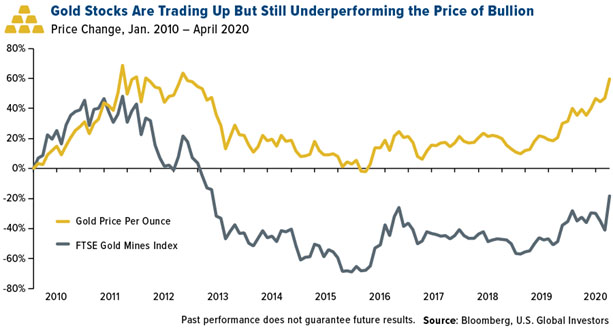

SR: How do you feel about gold stocks? Are you looking at seniors or juniors or both? What should investors be looking at?

FH: For the first time in a long time, I’m becoming very bullish on gold stocks. I’ve been very negative on gold mining companies for over a decade now, for raising capital and actually destroying value per share. But over the decade, new boards of directors and new chief executive officers have come on, and there’s become a greater discipline on cash flow returns rather than on cash flow, revenue per share growth, cash flow per share growth, rising dividends, all the normal things you buy a Starbucks or any great company for. It’s the capacity to have revenue growth. Mining companies did a lot of silly mergers and acquisitions work, with which they destroyed capital, but that has changed.

Franco-Nevada has a royalty on Newmont Goldcorp Corp. (NEM:NYSE) and Barrick Gold Corp.’s (ABX:TSX; GOLD:NYSE) joint venture assets in Nevada. The revenue per employee at Franco-Nevada is over $20 million. For Barrick or Newmont, it’s $500,000 of revenue per employee. Goldman Sachs has $1 million of revenue per employee. So these royalty firms are very efficient companies. If you look at the past decade, Franco-Nevada has far outperformed Berkshire Hathaway. It has far outperformed any gold stock. It’s because it’s showing revenue per share growth, cash flow per share growth, over the rolling one year over three years on a consistent basis.

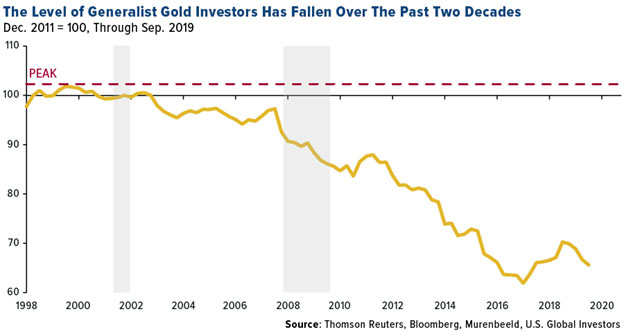

What’s now happening is we have new management for these other gold stocks. The big move in gold stocks occurs when the generalists start to buy the sector. They’ve not been owning the underweight gold stocks because of the bad discipline by management and boards or silly acquisitions. Now what we’re seeing, for the past three years, through the end of March, we’re going to see the one year revenue growth over two years strong. Now you get 36 months of a strong growth in revenue and cash flow from the industry, and all of a sudden, generalists show up. When you start seeing more and more of the stocks in that industry showing free cash flow, the generalists start to show up.

The coronavirus this past quarter hurt the S&P 1500 stocks because the majority of them had free cash flow yields of about 4%, and they got evaporated, obliterated, because of this global shutdown. But the gold stocks didn’t. They actually have rising free cash flow. They’re going to show this quarter the price of gold is up, some of them had shut-ins for very temporary periods of time but their revenue, their cash flow, as a whole is going to truly outshine the overall industry. And when the quants and the fundamentalists start looking at where their growth is, these stocks are going to show up.

I did an analysis of only looking at free cash flow and picked the 10 gold stocks every quarter that had the highest free cash flow yield. And I sold them and bought them every quarter. I far outperformed any gold index. So that discipline shows up as a key metric to attract the quant fund or the generalist. When I look at my datathe two-year number is so importantI’m becoming very bullish on gold stocks.

When we talk about the names, my bias is U.S. Global GO GOLD and Precious Metal Miners ETF (GOAU). I launched this several years ago as a smart quant approach to picking gold stocks. It has three royalty companies that we talked about, Franco-Nevada, Wheaton Precious and Royal Gold. They’re 30% of that ETF. They rebalance every quarter.

Then all the other names, they go down to a $200 million market cap but they have to be able to show the highest cash flow returns on invested capital. Once they do something silly or stupid, they’re thrown out. Back testing, that model has outperformed the VanEck Vectors Gold Miners ETF (GDX) and the VanEck Vectors Junior Gold Miners ETF (GDXJ) just on a basket of 60 gold stocks. This only has 28 names. Since I launched it, it’s far outperformed on a rolling 12-month basis. It’s smart data, and it dynamically recalibrates every quarter.

If you want to buy the individual names, then I would focus on those three big royalty companies. Thereafter, I would focus on those companies that have this metric I talk about, free cash flow yields. Out of the 100 gold stocks in the world that we follow, there are only about 14 of them that really have attractive free cash flow yields. What’s interesting is that Barrick and Newmontand Newmont’s part of the S&P 500does have a free cash flow yield that is positive, so you’re seeing it has really done exceptionally well this past quarter because it has an attractive free cash flow yield and has not been hurt by the coronavirus.

SR: Let’s switch gears for a moment. U.S. Global Funds runs the Jets ETF, an airline ETF. Obviously, the airlines have been battered. Do you see them coming back? Do you see bankruptcies?

FH: I think that the government agencies and the politicians have learned a lot from two big corrections: the 9/11 correction and 20082009. When you look at this industry, the Federal Aviation Administration says that 1 in 15 people is associated with the airline industry. That’s huge. When you look at the multiplying effect of the airline industry, it’s massive, just as housing is. One dollar for housing is worth $16 approximately. So when it comes to airlines, we’re talking a double digit number of multiplying effect.

What’s happened is that the government has been very smart this time to say we must make sure that we don’t unwind this industry as we’ve done in previous times. So I think there’s going to be a faster turnaround from the bailout policies.

What’s happened with the airlines is they have ancillary revenue that has been very significant in the past five years. Some $20 billion of revenue then went to $100 billion of revenue, which covers a lot of costs. It aggravates you and me when we fly: change fees, baggage fees, but all these fees have let the airlines not be victimized by the price of oil because every time the price of oil went up, airline stocks fell. Every time oil went down, airlines went up. It was this inverse relationship that took place. Oil has represented less and less of ancillary fees. Now what’s happened on this correction is not only the ancillary fees and everything have fallen, but oil has crashed. So airlines’ biggest cost is way, way down. That means when they turn, and they come out of this correction, they have huge upside. Not only do they have the support of the government, they have the ability to start adding on these fees.

Because of the bailouts, airlines are not going to be able to buy back their stocks and they’re not going to be increasing their dividends in this process. But that doesn’t matter. Their revenue capacity per share is explosive. So I think that that’s a very big difference.

SR: Anything else that you would like to talk to our readers about in this period of extreme volatility and uncertainty?

FH: Yes, bad news is good news. There’s the optimism of trying to find who’s going to be the solution to the problem. Had the U.S. Food and Drug Administration and the Centers for Disease Control and Prevention used Google and Amazon technology, they probably could’ve adapted faster to this coronavirus. Amazon hired 100,000 people. It’s amazing that in all that negative news, it adapted the fastest. It’s trying to understand how capital markets morph. There are certain industry leaders. I love Clorox. I don’t think that stock is going to be given away. I think it’s one of those just steady dividend payer and growing dividend stocks. So it’s in the negative news where you can find opportunities besides airlines, besides gold. You can turn around and find these other pockets.

SR: Thank you, Frank. I appreciate your time today.

Frank Holmes is CEO and chief investment officer at U.S. Global Investors, which manages a diversified family of funds specializing in natural resources, emerging markets and gold and precious metals. In 2016, Holmes and portfolio manager Ralph Aldis received the award for Best Americas Based Fund Manager from the Mining Journal. In 2011 Holmes was named a U.S. Metals and Mining “TopGun” by Brendan Wood International, and in 2006, he was selected mining fund manager of the year by the Mining Journal. He is also the co-author of The Goldwatcher: Demystifying Gold Investing. More than 30,000 subscribers follow his weekly commentary in the award-winning Investor Alert newsletter, which is read in over 180 countries. Holmes is a much sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg, BNN and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications.

Disclosure: 1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or members of her immediate household or family own, shares of the following companies mentioned in this article: None. She is, or members of her immediate household or family are, paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this interview are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Frank Holmes: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: N/A. I, or members of my immediate household or family, are paid by the following companies mentioned in this article: HIVE Blockchain Technologies. My company has a financial relationship with the following companies mentioned in this interview: N/A. Funds controlled by U.S. Global Investors hold securities of the following companies mentioned in this article: Mene Inc., Franco-Nevada Corp., Royal Gold Inc., Wheaton Precious Metals, Newmont Mining, Barrick Gold Corp. I determined which companies would be included in this article based on my research and understanding of the sector. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. 4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Franco-Nevada and Newmont Goldcorp, companies mentioned in this article.