By Jameel Ahmad, Global Head of Currency Strategy and Market Research at FXTM

The Pound is suffering with another negative start to the week against the USD, with the GBPUSD opening the week with two days of successive declines. The economic data from the United Kingdom followed a similar undesirable pattern to expectations given the global pandemic and subsequent weakness the world economy is facing.

The GDP data release showed a 2% quarter-on-quarter decline for the UK economy, however this has offered no end to recent nail-biting economic readings with it also being announced that the UK economy in March alone contracted by -5.8%. The latter represents the worst reading on record for UK GDP and given that the UK entered the pandemic somewhat latter than its peers, it presents a major warning sign that the Q2 GDP reading will not be pretty.

On a fundamental basis for the UK only, the Pound should remain weak. The United Kingdom is still in a very fragile state with coronavirus disease infections, as well as no clear indication in sight for when lockdown restrictions could be noticeably eased.

Should this bleak landscape remain unchanged and as long as the USD remains resilient (a big if) there is an argument to be made that the GBPUSD could potentially return to 1.20 at some point before the second quarter of 2020 concludes. Again, the USD will have a pivotal say in this and how the Dollar has traded in recent weeks has been anything but predictable.

On the Daily charts, support marginally above 1.22 could be seen as a near-term floor for GBPUSD. This would represent roughly the lows for the Daily candlesticks on April 6, April 3 and as far back as March 16. If this level were to break, the Weekly low from August 25 2019 just above 1.2138 might become an area of interest.

(GBPUSD Daily FXTM MT4)

EURGBP on the Daily charts continues to trade in a tight range. For a potential breakout to the upside, hypothetical buyers might wait to see if the EURGBP can break higher than 0.8862. Otherwise the continuation of a range that has been in place since early April remains on the cards.

(EURGBP Daily FXTM MT4)

The GBPJPY could be the pair to watch, if the right combination is in place. Pound weakness as well as a stronger JPY due to safe haven demand for the Yen would be monitored to see if the pair can possibly break below 130.48.

(GBPJPY Daily FXTM MT4)

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Increased global wheat supply estimates bearish for wheat price

The US Department of Agriculture World Agricultural Supply and Demand Estimates May report forecast larger supplies, increased trade, greater consumption and higher ending stocks for 2020/21. Foreign supplies are projected to increase 2.4% over year to 984.2 million tons due to higher production in 2020/21. And 2020/21 world ending stocks are estimated to increase 5 percent to a record 310.1 million tons – with China accounting for 52 percent of the total. And yesterday Rabobank lowered its 12-month Chicago Board of Trade wheat price down 6 per cent from last month into the range $5.25 – $5.34 a bushel, citing positive production outlook. Higher supply estimates are bearish for wheat price.

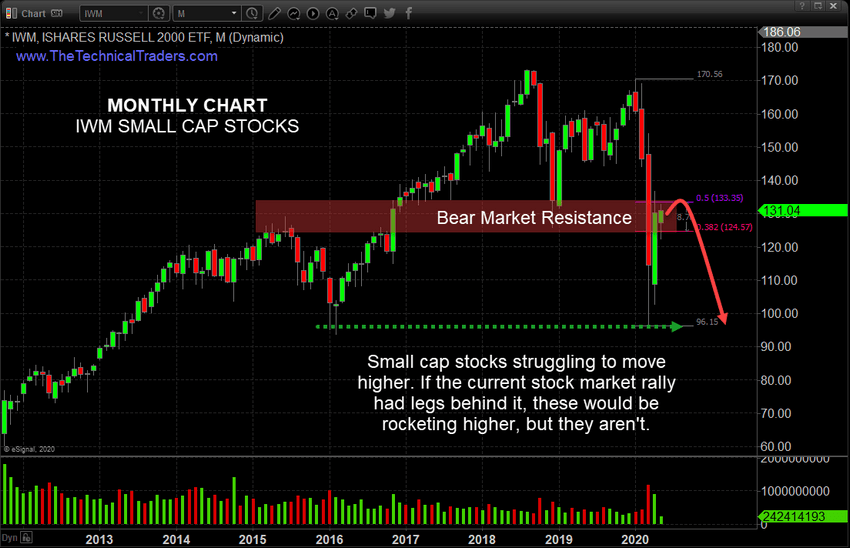

– Our research team believes the Russell 2000 is leading the way in terms of technical analysis and future expectations. While the NASDAQ has rallied as a result of US Fed stimulus and foreign investor activity, the Russell 2000 has set up a very clear price resistance level near $131~132 that presents very real potential for a double-dip downward price trend in the near future.

Monthly IWM ETF Chart

The resistance level near $131~132 suggests the IWM may rotate downward, creating a right-shoulder, and likely attempt to move down to the $96 previous lows. If this resistance area can’t be breached by further upside price activity, then the price will likely attempt to rotate lower and rests multiple levels as price collapses back below $100 again. The lack of upward price activity in the Russell 2000, and other market sectors, suggests the rally is isolated to the NASDAQ and certain other symbols – not broad-based.

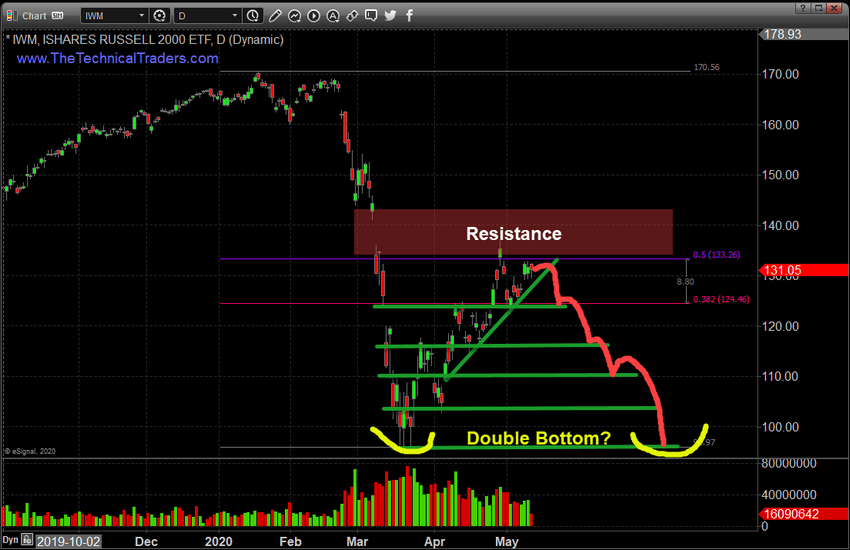

Daily IWM ETF Chart

This Daily IWM chart highlights the multiple levels of support below the current price levels. Each of these may act as some form of a soft floor in price as price attempts to move lower. Again, the lack of price to attempt to rally above the RED Resistance level on this chart suggests the Russell 2000 may have found a top and may begin to “rollover” as momentum diminishes.

If stocks are set to fall something else should start to rally. Check out my trade idea on silver!

Before you continue, be sure to opt-in to our free-market trend signals before leaving this page, so you don’t miss our next special report & signal!

Concluding Thoughts

Technical Traders watch for these types of patterns because they provide an A or B type of scenario for profits. Either, A, upper Resistance will be broken and the IWM will really past $140 and attempt a further upside price rally.. or, B, this resistance level will hold price below $140 and present a very real downside price opportunity where price may attempt to fall well below $110.

Our concern is that the initial downside price move in the markets, as a result of the COVID-19 virus event and global shutdown event, was followed by a Fed-induced “relief rally” that may be ending. Most of the time, these big impulse moves result in a “relief recovery” before further trending takes place. We believe the relief recovery is nearly over and the global markets may be setting up for a much bigger trending move.

If you are using our free public research for your own trading decision-making and/or using it as an opportunity to find and execute successful trades, please remember you are the one ultimately making the decisions to trade based on our interpretation and free research posts. We, as technical traders, will continue to post new research articles and content that we believe is relevant to the current market setups.

If you want to improve your accuracy and opportunities for success, then we urge you to visit TheTechnicalTraders.com to learn how you can enjoy our research and our members-only trading triggers (see the first chart in this article). If you are managing your retirement account or 401k, then we urge you to visit www.TheTechnicalInvestor.com to learn how to protect your assets and grow your wealth using our proprietary longer-term modeling systems. Our goal is to help you find and create success – not to confuse you.

Our researchers will generate free research on just about any topic that interests them. As technical traders, we follow price, predict future price moves, tops, bottoms, and trends, and attempt to highlight incredible setups that exist on the charts. What you do with it is up to you. Visit www.TheTechnicalTraders.com/FreeResearch/ to review all of our detailed free research posts.

In closing, we would like to suggest that the next 5+ years are going to be incredible opportunities for skilled traders. Remember, we’ve already mapped out price trends 10+ years into the future that we expect based on our advanced predictive modeling tools. If our analysis is correct, skilled traders will be able to make a small fortune trading these trends and Metals will skyrocket. The only way you’ll know which trades to take or not is to become a member.

Tanzania’s central bank lowered its benchmark interest rate and reserve requirement to “cushion the economy from adverse effects of COVID-19” and provide additional liquidity to banks, safeguard the stability of the financial sector, and continue facilitating the financial intermediation process. The Bank of Tanzania (BOT) said in a statement from May 12 that its monetary policy committee on May 8 approved a 200 basis point cut in the discount rate to 5.0 percent, providing additional space for banks to borrow at a lower cost and thus signaling lower lending rates. The Statutory Minimum Reserves (SMR) requirement was cut 100 basis points to 6.0 percent, as of June 8, while the haircut on government securities was lowered to 5.0 percent from 10 percent for government securities and to 20 percent from 40 percent for Treasury bonds as of May 12. “This measure will increase the ability of banks to borrow from the Bank of Tanzania with less collateral than before,” BOT said in a statement. BOT said it would also provide regulatory flexibility to banks and other financial institutions that carry out loan restructurings to borrowers that are experiencing financial difficulties due to the virus. Lastly, BOT said it wanted banks to incentivize their customers to increase the usage of digital payment systems, such as online banking and point of sale systems, and raised the limit on transactions for mobile money operators to reduce congestion in banks. Mobile money operators will be allowed to increase their daily transaction limits to 5 million Tanzanian shillings from 3 million and their daily balance can now run to 10 million shillings, up from 5 million. “The Bank of Tanzania said it would continue to monitor the impact of the COVID-19 virus on the economy and “take appropriate policy actions to limit the impact.” Tanzania’s shilling was trading at 2,314 to the U.S. dollar today, down 0.7 percent this year.

If you are new to the world of day trading, the one thing you’ve probably noticed is that everything seems to happen at the speed of light! With so much to keep in mind, and so much going on at the same time, you may be at a loss as to how to keep track of what you have already traded and how to improve your trading style. Someone may have suggested that the best course of action may be to use accounting software. Not only will this help you track your trades, but it will also come in handy in several other areas as well. So, do day traders need accounting software? The best answer is probably yes. Here is why.

Staying Ahead of the Taxman!

Many people have asked whether or not day trading is legal and that, too, is easy to answer. Yes, day trading is most definitely legal, however, staying ahead of the taxman might not be as easy! Bear in mind that all your trades happen so rapidly that to omit one gain or one loss can upset your taxes immensely. If you want to keep track of literally every trade to keep your gains/losses up to date, you would certainly benefit from the best accounting software on the market used by savvy day traders. You can do a comparison of various software platforms suitable for day traders on the piesync.com website. Here they compare two extremely popular programs – FreshBooks and QuickBooks – so that you can see which is easier for you to use and has the necessary features to keep your trades current. You will certainly want one that allows for seamless integration with your day trading software!

More Time to Trade

Also, you may want to consider using accounting software because the right platform will give you more time to focus on learning to trade. Some accounting software packages are so difficult to use that you will spend more time figuring out the program than you spend trading. With day trading, this can be your worst nightmare. Remember, you need to track all your trades, especially for the IRS, but to spend a long period of time recording them would be counterproductive. With the right software, you will have more time to spend analyzing the market because it will be able to pull outcomes as they occur. So, here again, yes, you need accounting software. However, you need the right accounting software for day traders.

When Less Is More

What all this boils down to is that the less time you can spend on bookkeeping, the more time you will have to focus on your trading style. New day traders find that they are better able to focus on trading when they do not also need to work on keeping records. Remember, in terms of time for day traders, less is always going to be more – and so much more! From having accurate figures come tax time to allowing you to focus more on trading, accounting software can be the missing link you have been searching for. Do you need accounting software? You absolutely do.

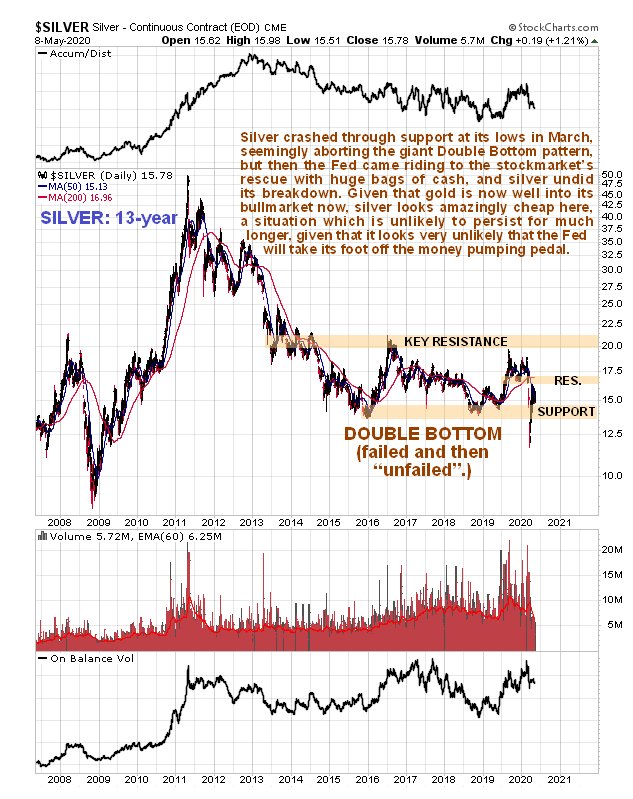

The way you see silver now depends on whether you see a glass that is half empty or half full. If you are a pessimist by nature you will be grumbling about its underperformance relative to gold up to this point, but if you are an optimist, as we certainly are with regards to silver, you will see it as maintaining the opportunity to pick it up cheap before it really takes off higher in a big way, which as we will now proceed to see is a fast growing probability.

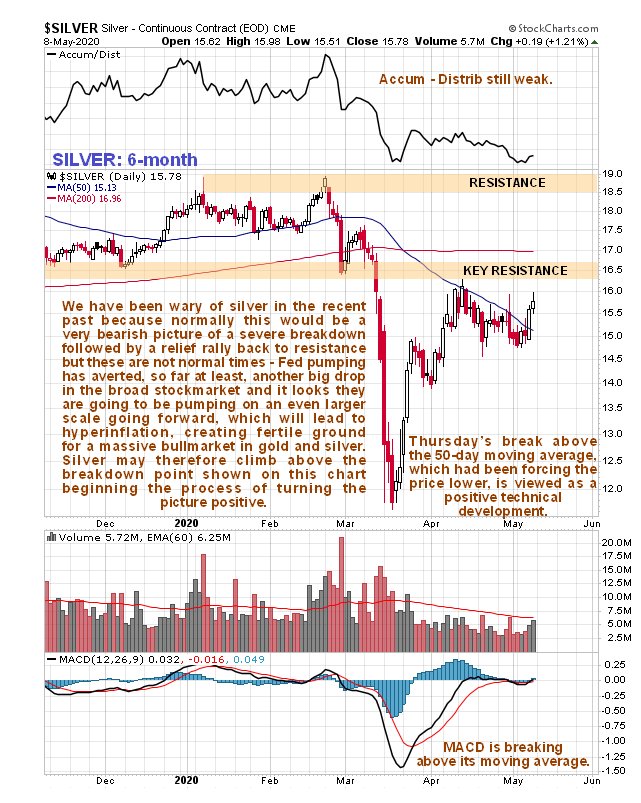

We have been wary of silver and silver investments in the recent past with good reason, because if another deflationary downwave hit, silver was in position to get really beaten back down into the dust, as we can see on its latest 6-month chart below. After being smashed in March when the stock market tanked, it staged a recovery, but started looking decidedly timorous as it approached a zone of heavy resistance in April and its unfavorably aligned moving averages. It was set up to take another severe beating in the event of the stock market tipping into another downwave, especially as it has been forced gradually lower by its falling 50-day moving average over the past several weeks.

But during this period the Fed has been creating money at a stupendous rate to throw at the credit markets and the stock markets to prop them up, and there appear to be no limits to how far they will go in pursuit of this objective. Needless to say this action is hugely inflationary in its implications and will lead eventually to hyperinflation, although it won’t start to kick in until the velocity of money increases, and we can expect gold and silver to anticipate this. Right now there is no velocity of money because the economy is dead, but we can expect them to keep pumping money until they get things moving.

The ongoing money creation by the Fed is the reason that the stock market hasn’t tipped into another downwave, and the reason that gold has held up well in recent weeks. If it continues we can expect silver to take on the key resistance in the $16.50 area that it gapped below in March. If it should overcome it, it will change the trend from the current neutral 7 down to neutral, paving the way for a major uptrend to begin.

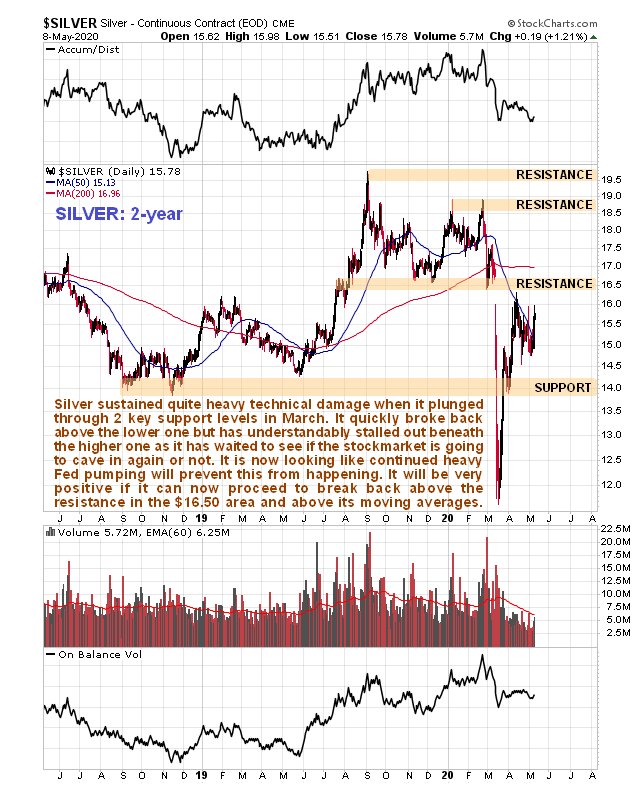

On the 2-year chart we can see why, at this juncture, we continue to have to classify the trend as neutral/down because of the quite strong resistance at the failed support in the $16.50 area and the still negatively aligned moving averages. A break above this resistance and the 200-day moving average just under $17.00 will improve the picture significantly

On the 13-year chart we can see how the breakdown in March caused by the stock market plunge broke silver down below the lows of a potential giant Double Bottom, and the fact that it has risen back into the pattern is positive, provided that it can hold recent gains and build on them. Volume indicators look positive relative to price, which is a good sign.

Silver’s latest COT looks much more positive than gold’s, which rather suggests that we can look forward to silver outperforming gold for a change before too much longer. This chart certainly indicates that there is plenty of room for silver to advance from here.

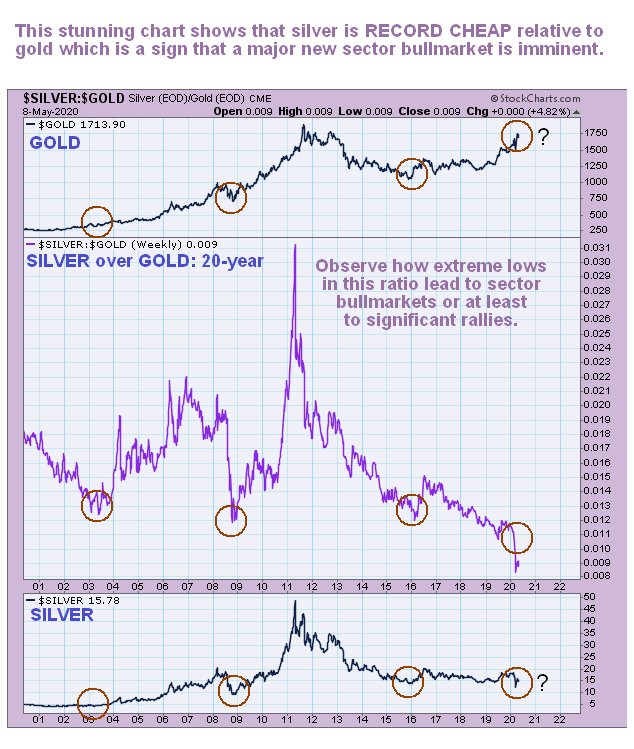

Just how undervalued silver is relative to gold is made dramatically clear by the 20-year chart for silver over gold shown below. Every time this ratio has dropped to a really low level it has led to a major sector bull market, but now it is much more extreme suggesting both that the looming bull market will be big and that it is likely to start soon.

With respect to silver’s relatively rotten performance compared to gold in the recent past, this is a good point at which to draw your attention to an excellent article by Jeff Clark on the subject entitled Why Is Silver Stagnant and When Will It Start Moving? I’m sure you will agree that this is most encouraging article for silver investors.

In addition to silver being very cheap relative to gold, there is now a big difference between the paper price for silver and the physical price for silver, which, as with gold, is viewed as a very auspicious development. IT IS VERY IMPORTANT NOT TO LET THIS LARGE PREMIUM PUT YOU OFF BUYING PHYSICAL SILVER IF YOU ARE MINDED TO, because this premium is likely to get even bigger, and if silver starts to take off higher again, physical silver could very quickly become impossible to obtain. Use the cloak of recent weakness to get it on board as fast as you can. Even if a worst case scenario eventuates and the stock market drops despite Fed pumping and silver drops back towards recent lows, so what? When the hyperinflation hits silver could easily end up at $100 or $200 an ounce, and maybe much higher, so why quibble about a possible $3 or $4 drop from here, which is any case is considered much less likely now?

Originally posted on CliveMaund.com on May 10, 2020.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

The deflation and depression is right here, right now, and if you don’t believe that, try asking some of the 30 million people who just lost their jobs in the U.S., or those who (used to) work in the catering and tourism industries.

The Federal Reserve is reacting to this situation by working to create hyperinflation, because it finds it preferable to a deflationary implosion. There are two reasons for this. One is that it enables the Fed to continue to fulfill its time-honored role, which is to transfer wealth from the rest of society to the 1%, and the other is it defers complete systemic collapse for a little longer.

The Fed has created a staggering amount of new money since this crisis started a few months ago to feed the debt monster. Its balance sheet has gone exponential and is expanding vertically, guaranteeing hyperinflation, which will begin the moment the velocity of money starts to pick up. Currently there is no velocity of money because the economy is dead, but if you print enough money to throw at it, as in countless trillions, you can get things moving again.

At the risk of sounding old-fashioned, I want to point out here, for the benefit of those who perhaps have a hard time understanding certain basic truths, that creating more money does not actually create wealth. If you, say, triple the amount of money, all that happens is that you have three times the amount of money competing for the same amount, or a reduced quantity, of goods and services, which inevitably drives prices up, hence the trend to hyperinflation.

The manic money creation by the Fed has already driven stocks back up, so they have recovered most of their losses triggered by the virus scare, and the Fed will keep on pumping until it gets things moving again, in order to banish the specter of deflation.

But no matter how much they create to satisfy the immediate cravings of the debt monster, it will never be enough, and it will continue to threaten to jack up rates unless it is fed ever greater quantities of cash. Money creation has already gone into the vertical blow-off phase, and the quantity of money will continue grow at an accelerating rate until it becomes worthless.

Thus, it is no surprise that gold is starting to power up for an advance that will take it to the stratosphere, or more likely the moon. Silver hasn’t “got the memo” yet, or maybe it did just last Friday, judging from its price action.

One of the key points to understand is that this crisis will not end until all the gargantuan debts that have built up, and associated derivative positions, are written off as worthless. Corporate debt, government debt, municipal debt, junk bonds and all bonds, right up to Treasuries, are intrinsically worthless, and are going to be forcibly marked to market by one of two methods: default; or hyperinflationas in, “Here’s your money backoh, I’m awfully sorry, it’s now worthless.”

If you own any of this garbage, you should move swiftly and resolutely to get rid of it, before its value declines to a big fat zero. The crisis cannot end until the overhang of this atrophying sludge, which is like a huge ball and chain hanging around the neck of the world economy, is eliminated. The creditors will end up with nothing. One of the main reasons for the recent huge money creation by the Fed is to backstop the credit markets in order to stop rates rising, which would cause debt to compound at a catastrophic rate. They seem to be alright, however, with the idea of eliminating the debts by taking the hyperinflationary route.

The Fed is to other central banks around the world what the Corleone family was to the Mafia in the “Godfather” series, which is to say that they had better follow the Fed line unless they want to get “wasted.” Thus, we can expect them to engage in the same manic money creation.

With fiat around the world now heading at an ever-rapid rate toward its intrinsic value of $0, the choices for those wanting to preserve their wealth are rapidly narrowing down toward just two things: gold, which is real money; and silver. While various scarce collectibles like old cars and paintings hold their value and increase in price during periods of high inflation, they are not a very practical means of exchange. You cannot imagine wandering around a street market with a painting and stopping at a stall and saying, “I’ll swap this old Rembrandt for that cabbage and a couple of parsnips,” and that’s assuming that you get that far without being mugged.

Gold and silver are more transportable and more practicalsilver especially for more minor transactions, which makes its recent poor performance relative to gold somewhat puzzling. Not that we are complaining, since it is giving us more time to load up before it does take off.

With respect to silver’s relatively rotten performance compared to gold in the recent past, this is a good point at which to draw your attention to an excellent article by Jeff Clark on the subject entitled Why Is Silver Stagnant and When Will It Start Moving? I’m sure you will agree that this is most encouraging article for silver investors.

A reason why we have been rather “backward with coming forward” to make investments in the precious metals sector in the recent past was the serious risk that markets would tip into another severe bear market down-wave, but this danger is now believed to be passing due to relentless and massive money pumping by the Fed designed to backstop the credit markets and pump the stock market, especially the darling FAANG (tech) stocks, which are now “organs of the state.”

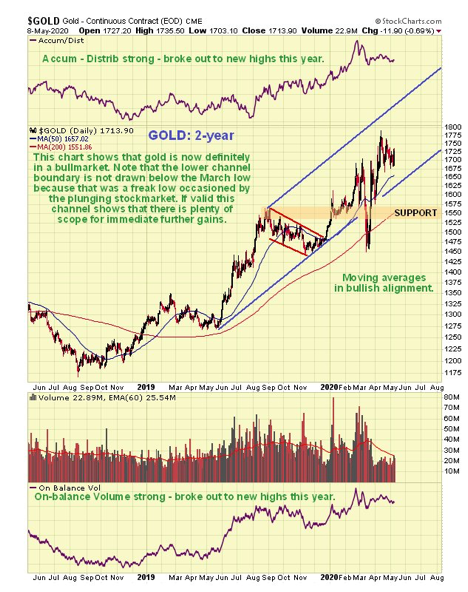

We can see on gold’s latest 6-month chart that the recent pattern could have been a top following its arrival at a trendline target, but now it is looking increasingly like a bull pennant.

On the 2-year chart, we can see that gold is definitely in a bull market. There are a couple of interesting points to observe on this chart. One is that the quite strong advance in the middle of last year broke gold out of the multiyear base pattern that we can see on the 10-year chart lower down the page. Another is that the action into mid-March this year demonstrates that if the stock market crashes it will take gold down with it, although as set out above, rampant Fed pumping is greatly reducing this risk. Although it looks like gold could further medium term on this chart, we can equally see that the rate of rise could now accelerate, especially the accelerating rate of money creation.

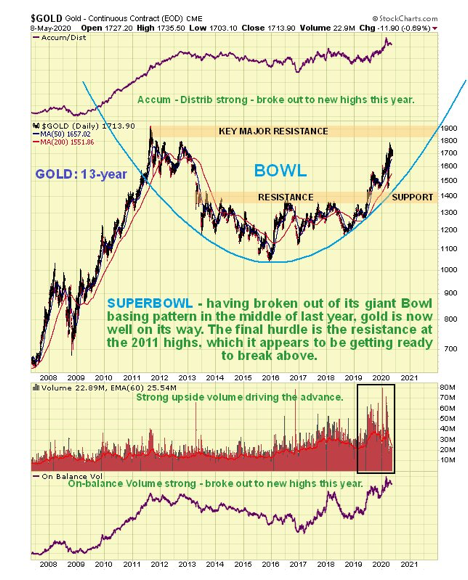

On the long-term 13-year chart, we can see the big bowl base pattern that formed between 2013 and last year, and how, following last year’s breakout above the upper boundary of this pattern, it is forging ahead in readiness for a breakout to new highs. Of course, gold has already broken out to new highs against most major currencies. A strongly bullish point to observe, which bodes well for the future, is the strong upside volume driving the advance, which has taken both volume indicators shown to new highs.

Gold’s latest COT shows readings in middling groundnot low enough to be decidedly bullish, but not high enough to preclude further advance. This is in marked contrast to silver’s latest COT, which looks much more positive.

A final point worth making relates to the now big gap between the paper price of gold and the prices for physical metal, which is becoming increasingly hard to obtain. This is viewed as a very positive sign, and it is hardly surprising considering what is going on in the world. If you are interested in buying physical metal you should not less this put you off, because the gap is likely to widen much more as the price advances before physical metal becomes unobtainable except at very high prices.

Originally published on CliveMaund.com on Sunday, May 10, 2020.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Shares of MyoKardia traded 60% higher, setting a new 52-week high price, after the company reported that it met all primary and secondary endpoints in the Phase 3 EXPLORER study of mavacamten in treatment of obstructive hypertrophic cardiomyopathy.

Clinical-stage biopharmaceutical company MyoKardia Inc. (MYOK:NASDAQ), which is focused on developing targeted therapies for the treatment of serious cardiovascular diseases, today announced it achieved “positive topline data from the company’s Phase 3 pivotal EXPLORER-HCM clinical trial of mavacamten for the treatment of patients with symptomatic, obstructive hypertrophic cardiomyopathy (HCM).” The firm further stated that MYK-461 (mavacamten) demonstrated a robust, well-tolerated and safe treatment effect and that it met all primary and secondary endpoints in the study that produced statistically significant results including reduction or elimination in obstruction of the left ventricle in treated patients.

Iacopo Olivotto, M.D., of Careggi University Hospital and lead clinical investigator for the EXPLORER-HCM clinical trial commented, “The extraordinary data from the EXPLORER pivotal trial confirm mavacamten’s ability to relieve dynamic outflow obstruction, control symptoms and improve quality of life in patients with hypertrophic cardiomyopathy…HCM is the most common inherited cardiovascular disease, and patients face an uncertain journey that all too frequently includes debilitating symptoms, as well as serious complications, such as heart failure, stroke and cardiac arrest. Mavacamten is the first drug developed to target the specific molecular defect of the disease. EXPLORER represents a major achievement toward a precision-medicine approach in cardiomyopathies and should provide great hope to a community painfully aware of the lack of disease-specific treatment options.”

The company’s CEO Tassos Gianakakos remarked, “The resoundingly positive data from EXPLORER bring us a significant step closer to improving the lives of people with serious cardiovascular conditions, starting with HCM, a debilitating disease estimated to affect one in every 500 people…The activity and tolerability profile observed for mavacamten in this pivotal study underscores the profound impact and potential for therapeutics that target the underlying biology of disease. We look forward to the submission of MyoKardia’s first New Drug Application and, importantly, to serving the many patients that stand to benefit from mavacamten.”

The firm indicated that the EXPLORER-HCM clinical trial enrolled a total of 251 patients and is part of MyoKardia’s pivotal program studying mavacamten as a treatment for symptomatic, obstructive hypertrophic cardiomyopathy. The company stated that it plans to submit a New Drug Application to the U.S. Food and Drug Administration (FDA) in Q1/21.

The company explained that “HCM is a chronic, progressive disease in which excessive contraction of the heart muscle and reduced ability of the left ventricle to fill can lead to the development of debilitating symptoms and cardiac dysfunction and it is estimated to affect one in every 500 people.” The firm noted that the most frequent cause of HCM is mutations in the heart muscle proteins of the sarcomere; however, it has additionally been linked to increased risks of atrial fibrillation, stroke, heart failure and sudden cardiac death.

MyoKardia is a clinical-stage biopharmaceutical company based in Brisbane, Calif., that concentrates on developing targeted therapies for cardiovascular diseases. The firm stated that “its initial focus is on small molecule therapeutics aimed at the proteins of the heart that modulate cardiac muscle contraction to address diseases driven by excessive contraction, impaired relaxation, or insufficient contraction.”

MyoKardia began the day with a market capitalization of around $2.9 billion with approximately 46.68 million shares outstanding and a short interest of about 10.6%. MYOK shares opened nearly 67% higher today at $101.91 (+$40.82, +66.82%) over Friday’s $61.09 closing price and reached a new 52-week high price this morning of $104.26. The stock has traded today between $98.02 to $104.26 per share and is currently trading at $100.06 (+$38.97, +63.79%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

(Following item updated with State Bank of Pakistan, which said its monetary policy committee would meet on Friday, May 15 to decide on monetary policy.

Pakistan’s central bank has cut its policy rate three times this year by a total of 425 basis points following cuts on March 17, at an emergency policy meeting on March 24 and April 16.)

This week – May 10 through May 16 – central banks from 7 countries or jurisdictions are scheduled to decide on monetary policy: Moldova, New Zealand, Belarus, Egypt, Mexico, Ghana and Pakistan.

Romania’s central bank was scheduled to decide on monetary policy on May 12 but its board decided on March 20, when it cut the rate 50 basis points at an emergency meeting, to suspend monetary policy meetings given the high degree of uncertainty surrounding economic and financial developments.

Instead, the central bank’s board will meet to decide monetary policy when necessary..

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

– As China’s economy is rebounding, the belated COVID-19 mobilization in the United States and Europe has resulted in huge human and economic damage. New policy plunders could make the situation much worse globally.

My new report, “The Tragedy of Missed Opportunities,” focuses on the huge COVID-19 human costs and economic damage. Released by a global think-tank, Shanghai Institutes for International Studies (SIIS), it identifies the missed opportunities in the virus battle and its consequent human and economic costs ” [link and here].

In the United States, the Trump administration’s futile effort to “protect the economy” (read: the markets) has had disastrous repercussions. Yet, the White House continues to suppress science-based medical policies.

The European Union was more willing to battle the virus but was unable to do so proactively because it lacks the needed common institutions for effective response.

Despite several major opportunities to initiate early mobilization, the major advanced economies did not opt for preemptive action.

Missed opportunities

Between the first recorded case (Dec 30, 2019), and the WHO’s announcement of the international emergency (Jan 30, 2020), the epicenter of the outbreak was centered in Wuhan, Hubei, and nearby Chinese provinces. The first cases were also recorded in some 20 other countries, including the US and major EU states.

That’s when China, Hong Kong, Singapore and later South Korea mobilized against the outbreak. The White House and the EU had the same virus information as these early mobilizers in the first week of January, yet both chose not to mobilize. That’s how they missed the first opportunity for proactive mobilization.

The second opportunity to contain the virus was between the WHO’s international emergency (Jan 30) and global pandemic alert (Mar 10), when the epicenter moved to Europe and then to the US. Yet full mobilization in both began only 1-2 weeks after the pandemic warning – 6-8 weeks later than in China and Hong Kong.

During this period, inadequate preparedness was reflected by faulty test kits and long testing delays; shortages of protective equipment (PPE), which US trade wars made worse, endangering frontline healthcare professionals; failed responses adding to health risks (rejection of medical policies, failed quarantines); misguided media coverage causing an “infodemic” and an odd battle against the WHO.

That’s how the second major opportunity for mobilization in February and much of March was missed. In cumulative terms, it covers the entire 1st quarter of the year.

As escalation continued in Europe, the epicenter moved to the US, while quarantines and lockdowns diffused worldwide. While China started social distancing measures in January, they were widely introduced in the West only in April. As a result, the outbreak will linger far longer worldwide, while new virus waves and residual clusters are more likely and premature lockdown exits will add to human and economic costs.

That’s how the third major opportunity to battle the virus failed in February-March. In cumulative terms, it comprises the first half of the year.

Next, the epicenter will move to developing countries with weaker healthcare systems. Without external support, that could push 265 million people into poverty, as the UN food relief agency has already warned.

That’s how the fourth major opportunity against COVID-19 would be missed.

Massive human costs, historical economic damage

In January, there were over 7,700 cumulative confirmed cases in China, but only a dozen in Europe and half a dozen in the US. Since China mobilized against the outbreak then, cumulative cases are likely to stay below 90,000 at the end of June.

In contrast, Europe and the US could each have some 3 million cumulative cases and hundreds of thousands of deaths. Belated mobilizations have horrible costs.

Struggling to deflect responsibility for its disastrous COVID-19 plunders, the Trump White House is fabricating pretexts to target China as a politically expedient scapegoat, while trying to recruit EU NATO allies to a still another Cold War.

Without vaccination and therapies, the human costs will continue to climb until the epidemic curves normalize, earliest by 2021. The economic carnage will start with the 2nd quarter coronavirus contraction casting a dark shadow over the early 2020s.

Even in the current baseline case (IMF, Apr 2020), the cumulative loss to global GDP over 2020 and 2021 could amount to $9 trillion. That’s more than the world’s third and fourth largest economies Japan and Germany combined – or three times more than the 2003 Iraq War, still another misplaced tragedy.

New trade wars could cause global depression

But there could be much worse ahead. The current IMF baseline still downplays the dire economic landscape – from the 2008/9 global crisis to US tariff wars – that preceded COVID-19. Also, the epidemiologists assume there might be a longer outbreak in 2020, a new outbreak in 2021, or both.

Since the Trump White House wants to reignite the trade war, it could cause what I call the Great Power Conflicts scenario. In this case, the coronavirus contraction and lingering pandemic risks would result in new trade wars and geopolitical conflicts causing a multi-year global depression. This is the current path of the White House.

What is needed to avoid such a calamity is the Great Power Cooperation scenario, which would have to cope with lingering pandemic risks would, but deals in trade and technology and diplomacy-driven geopolitics could foster global economic recovery. This appears to be the preferred path of China, most of the EU and US opposition against the Trump White House.

After the tragedy of missed opportunities, only international, multilateral cooperation can offer a way out.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

A version of the commentary was released by China Daily on May 12, 2020.