Technical analyst Clive Maund discusses why he is upbeat about Tanzanian Gold.

Tanzanian Gold Corp. (TRX:NYSE; TNX:TSX) stock got clobbered by a big financing last December, and then it got beaten down further to a low in March when the entire market caved in, including gold stocks, so it has remained “under a cloud” since the financing, never really recovering with the sector in April, and it is only in the past week that it has started to perk up, as we can see on its latest 6-month chart below.

It is now clear that a base pattern has been building out since last December that has allowed time for sentiment to recover and for its moving averages to start to swing into a more positive alignment. An especially positive development is the improvement in the volume pattern that has led to a marked improvement in the Accumulation line in recent weeks. This, coupled with momentum (MACD) swinging positive, suggests that it is getting ready to break out of this base pattern at last.

It is thus encouraging to see that on the 18-month chart it has broken out of the downtrend in force from last July just over the past week. This chart also shows that, in addition to the nearby resistance level marking the upper boundary of the recent base pattern, there is another level of significant resistance on the way up centered on 75 cents, however, given how rapidly the outlook for gold is improving, it is considered unlikely that these resistance levels will prove to be much of an impediment.

On the fundamental front there have been a string of very positive developments for the company this year, which include:

Second was the Buckreef review which included discussion of the oxide plant start-up and imminent gold production, and new indications of a potential underground component in the larger sulphide mine plan.

Third was the work done by SGS Lakefields to give the company the ability to discuss a potential plan for a mining operation 3 times that described in our 2018 Pre-Feasibility Study with production of 150,000-175,000 ounces gold per year.

Zooming out again, the 6-year plus chart shows to advantage the entire giant base pattern that has formed in Tanzanian Gold at a low level since early 2015. This chart begins to make clear how historically cheap the stock is.

Finally, the 18-year chart makes the stock look even more cheap as we can see that it is now at a very low price compared to the heady days of the 2000s and going into 2011, when hope triumphed over reason. The ironic thing is that, now that the company is much closer to attaining its goals with respect to the development of its mines, against the background of a gold price that is headed to the moon, because of the impending hyperinflation which the Fed is already enthusiastically feeding, the stock price is historically at a very low level, way below where it was in the 2000s, implying that we should soon see the triumph of reason over despair.

Tanzanian Gold Corp. was mentioned as a most promising gold stock in the Precious Metals Sector Alert posted at 3.30 pm last Thursday and it was nice to see your buying drive a sharp move higher in the stock during the last half hour of trading.

The conclusion is that Tanzanian Gold is a strong buy here for all time frames, only qualified by the observation that we could see a minor dip over the short-term as it is a little overbought, although there may be no dip at all.

Tanzanian Gold Corp, TRX, TRX.ASE, trading at $0.62, closed at A$0.623 on 8th May 2020.

Originally posted at 1.50 pm EDT on CliveMaund.com on 8th May 2020.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Clive Maund: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. CliveMaund.com disclosures below. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Brien Lundin, sector expert and publisher of the Gold Newsletter, offers his perspective on the monetary ramifications of the COVID-19 pandemic in this conversation with Maurice Jackson of Proven and Probable.

Maurice Jackson: Today we will discuss the 2020 financial crisis and investment opportunities for your portfolio. Joining us for a conversation is Brien Lundin, the president of Jefferson Financial.

Mr. Lundin, investors are in a state of confusion and they’re looking for some sound guidance. These are truly unique times. For someone who says, “We’ve been here before, it’s going to be all right,” can you please share what are the primary differences between the global financial crisis of 2008 versus 2020?

Brien Lundin: Well, two things really. The primary difference, first off, is the degree of monetary accommodation and stimulus efforts. We always predicted this would happen to a greater degree this next time around. But the second big difference has been the rapidity of the move. We expectedand I had been predicting in Gold Newsletter for a couple of years nowthat the next crisis would come, they would find some excuse to demand more easing from the Federal Reserve, and the patient would demand more of the drug this time, so they would have to do more than they did before. But I expected all of this to play out over, say, five years. I did not expect it to play out over veritably five days, as it has. That’s been the big difference. Time has been compressed, everything’s on turbo, it’s all coming at us very quickly. That is why I believe that investors have to just really focus and leap ahead, and think ahead about all of the ramifications.

Maurice Jackson: Are you surprised at the responses from the Congress, the Treasury and the Fed?

Brien Lundin: No, not at all. As I mentioned, I had expected it to comereally this year at some point; I expected it later in the year. And more a function of the passage of time, because this market has been built on the adrenaline of easy moneyand by this market, I mean the stock market, which, in turn, now means the economy. It had all been built upon this foundation, a very shaky foundation of the historic accommodation from the Federal Reserve. And then, at some point, I predicted. . .the market was going to throw a hissy fit and start correcting and demand that the Fed come back and start this whole rate cutting cycle again.

And what I had been saying was that this time around, it would have to do more quantitative easinggo back to zero again on interest rates, but do more quantitative easingthan they had ever done before, and that this time around they would have to actually get into some fiscal measures, stimulus spending, direct aid and spending to the economy infrastructure and that sort of thing. So none of this came as a surprise. I knew the market was going to look for some excuse.

As it happened, COVID-19 was the excuse, it was the perfect excuse. It’s a very valid excuse in my mind. But all of this happened anyway, but later and at a much slower pace. So no, I’m not surprised at their reaction and I think it’s only the beginning. I think they’re going to do much, much more.

Maurice Jackson: All three of the aforementioned are going to be extremely resilient in their efforts to solve problems that they and their predecessors created. When you hear the Fed chairman state that now is not the time to worry about debt, but use the great fiscal powers of the U.S. to avoid deeper damage to the economy, does that signal to investors that everything is going to be OK?

Brien Lundin: Well, I think it signals to investors that it’s whatever it takesin that all of the rules, all of the restrictions have been thrown out the window; in that the Fed will overshoot, if anything, in its mitigation efforts.

So I think what that tells investors is that we’re going to see the Fed’s balance sheet soar to the sky. We’re going to see money printing of a degree we’ve never seen before out of war time, and probably even including that. And they’re not going to be restrained in any way. So I think that’s telling us that everything we expected is going to happen, but it’s going to be almost exponential to what we would have realistically expected.

Maurice Jackson: Speaking of the national debt, where do we currently stand and where do you think it’ll be by the end of the year?

Brien Lundin: Well, we were pushing $23 trillion, in terms of the gross federal debt before this crisis. And I think by the end of the year, or by the time this crisis runs its course, will be in excess of $26 trillion.

And when Donald Trump was elected, I made the remark that, judging on past history, every eight-year term, eight-year presidential administration, typically doubles the debt of the previous administration. And if that was going to happen, in this case, we would have a federal debt of $40 trillion. At the time I admitted that sounded absurd, but this was the pattern and I just wanted to bring to everybody’s attention. Now, it doesn’t seem so absurd anymorethat by the time we get out of this, we’ll be approaching a federal debt of $40 trillion.

But at some point it doesn’t much matter anymore because we’ve already reached the point of no return. We’ve already reached a level in the federal debt where we can no longer have real interest rates, at least above zero. Now that is interest rates adjusted for inflation. And the debt is so large now that it must be depreciated away more quickly than the debt service costs are being paid on that debt, otherwise, the federal budget would collapse.

There’s no way we can’t afford to pay, and no way politically that I think American citizens would agree to pay a trillion dollars or more on debt service costs every year. And that’s where we’re getting to, that’s where we would be if we had interest rates at any appreciable level, so we simply cannot have interest rates at those levels. Again, the debt will have to be depreciated away, moreover through the devaluation of the dollar, and that’s going to happen, I think, to greater effect and at a greater speed than we expected before or that we’ve seen before.

Maurice Jackson: The big elephant in the room that many investors may be overlooking, is GDP (gross domestic product). How does GDP factor into this discussion?

Brien Lundin: Well, in terms of this crisis, it’s going to take a big hit. It already took a big hit, down 4.54.8%, I believe, in the first quarter. The second quarter is going to be absolutely abysmal. I mean, there are economists predicting 2030% declines in GDP for the second quarter, and that’s going to be shocking.

I think that may be the impetus for that second dive down in the stock market that everybody’s talking about. So we may see all of that play out.

But again, I think that the policy response, which you’ll see from the Fed, which you’ll see from Congress and the administration, is a redoubling of their efforts to rescue the economy, to stimulate the economy. And we’ll see the money printing, we’ll see the fiscal spending, the stimulus programs, the infrastructure spending. Really, it’ll be a blank check mentality.

Maurice Jackson: Our government representatives must not be students of monetary history, as they appear to have no regard for the unprecedented inflation of our currency. When do you foresee the effects of inflation to begin impacting us all?

Brien Lundin: Well, it’s going to happen. First off, this time I think we need that. In 2008, post-2008, we did not see much, we didn’t see all of that money printing translated into retail price inflation, which is what the general public and the general investing public perceives as real inflation. We didn’t see that because it was all encapsulated within the financial system and, of course, the rescue efforts back then were aimed more toward rescuing the financial system.

So this time around. it’s a bit different. It’s not a crisis within the financial system and a lot of the rescue efforts, a lot of the stimulus, is being aimed more at Main Street rather than Wall Street.

So I think we’re going to see is more real-world effects of this monetary stimulation. We’re going to see inflation perk up this time around. I think. . .to keep gold on a bull market path this time around, we’ll actually have to see that kind of inflation.

But the good news for gold bugs is I think we will see it. I think it’s, at this point, unavoidable, because there’s so much. . .helicopter money this time around, checks being sent to American citizens directly. With that kind of monetary stimulus, I think inflation is unavoidable.

Maurice Jackson: Turning our focus to the stock market: With the declining currency, what kind of impact do you foresee in the general equities? Is this the time to get out?

Brien Lundin: Well, I haven’t been a big stock bear. I don’t think that you can look at, say, gold and the stock market as being contra-cyclical. I think everything right nowthe metals, commodities, the stock market, the bond marketeverything’s being driven by central bank stimulus. It has been to great degree since 2008, and really over the decade or so before that, as we’ve seen the Fed become more and more involved in trying to manage the downturns in the economy. We’ve had these boom-and-bust cycles over and over again, but with all of this liquidity being thrown into the market, all of these typical inverse correlations or uncorrelated assetsall those correlations tend to go toward one.

So what happens is this kind of monetary stimulus is bullish for not only gold and precious metals, but also equities, also the bond market. So I don’t think that the stock market necessarily will falter in the days ahead, I don’t think it has to. Now, I think initially, all of this stimulus will be bullish for the stock market.

Maurice Jackson: And I’m assuming that includes mining and junior mining companies. Is that correct, sir?

Brien Lundin: Oh, absolutely. Absolutely. Because they’re going to be supported by two big trends, by a bullish environment for equities in general, and by a bullish environment for the precious metals.

Maurice Jackson: And I guess oil would also factor in that discussion as well, lower oil prices, correct?

Brien Lundin: Yeah. Oil prices for the producers help tremendously, because energy is one of the primary input costs into gold production. Not only that, but we’re going to see the CPI [consumer price index]the public, the readings of inflationdrop a bit because of lower energy prices over the next few months.

But as we see supply destruction on oil, and we see the CPI get to lower levels because of lower oil prices, when oil prices do rebound, it’s a lot easier to see a rebound in oil from say, $15 to $25 a barrel, and that’s a tremendous. On a percentage basis, that’s a tremendous increase. So we’re going to see, once we get some economic recovery and some demand recovery in oil, we’re going to see oil prices bounce, not to necessarily the $45, $50, $55 level, but to a significant degree, to where it will really boost the inflation readings. And I think that’s going to come as a shock to the markets.

Maurice Jackson: Speaking of mining and junior mining companies, which ones have your attention at the moment and why?

Brien Lundin: Well, a lot of them, Maurice. I tell my readers that they need to buy the companies that are either in production or getting ready to get into production, and or have large established resources, because these kinds of optionality plays will be the first to benefit.

So that’s the general advice I’ve been giving my readers. I haven’t necessarily been taking that advice personally, because I know a lot of these companies very well. They have great exploration programs and great drill targets, and I’ve been pecking away at that myself and recommending them to my readers, at some of these very low levels.

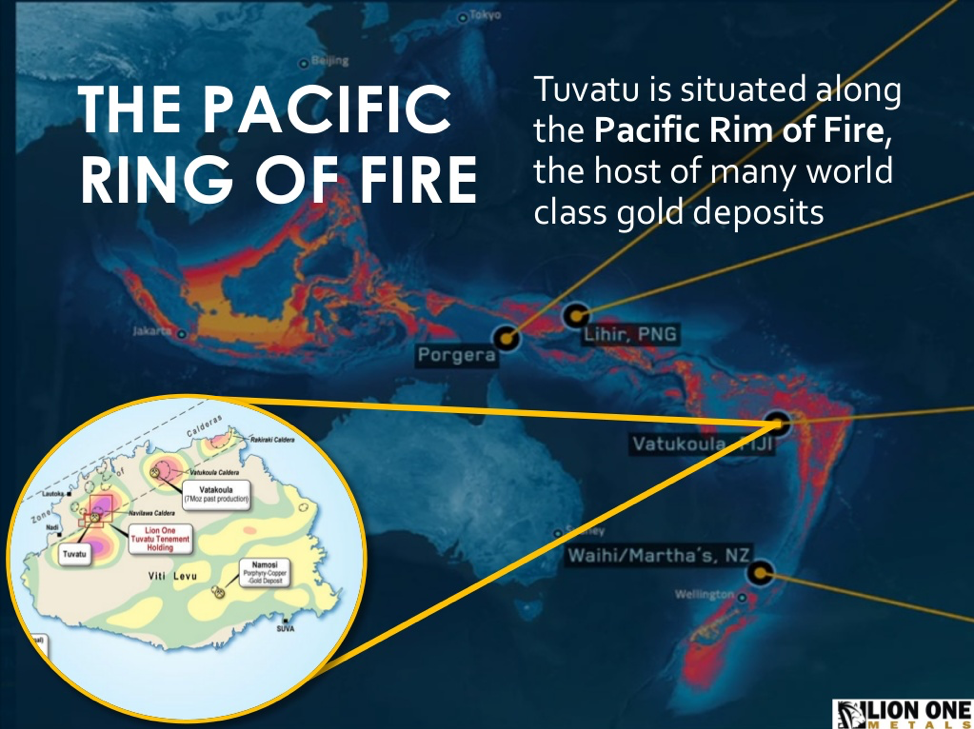

Some of the companies I like out thereI had a chance recently to talk with the management of the geologic team of Lion One Metals Ltd. (LIO:TSX.V; LOMLF:OTCQX) and I really liked their project in Fiji, in particular the Caldera target. I think it’s one of the most spectacular exploration targets you’ll find in the world today.

And I’m also very familiar with Fiji and I think that’s because I’m the chairman of Thunderstruck Resources Ltd. (AWE:TSX.V; THURF:OTC.MKTS), which is a exploration company with a drilling program ongoing in Fiji. I’m very familiar with that regime and I think a lot of investors aren’t familiar with it. It’s a blossoming new frontier for mining and metals exploration.

Maurice Jackson: And if I may interject there, with Lion One Metals, the CEO there is Walter Berukoff and their flagship project is the Tuvatu, and it’s an alkaline deposit (VRIFY). That’s what’s very interesting hereit’s an alkaline deposit, so we’re looking at some significant tonnage and grade here, potentially.

Brien Lundin: Gold deposits, specifically alkaline deposits of that sortthe list of those kinds of deposits that have not become world-class mines approaches zero. The odds dramatically increase if it’s a major discovery. So yeah, you bring up a very good point for that deposit. That’s why I like it a lot; that’s why I’m a shareholder personally.

Maurice Jackson: And was there another company you were about the reference? I’m sorry I interrupted you.

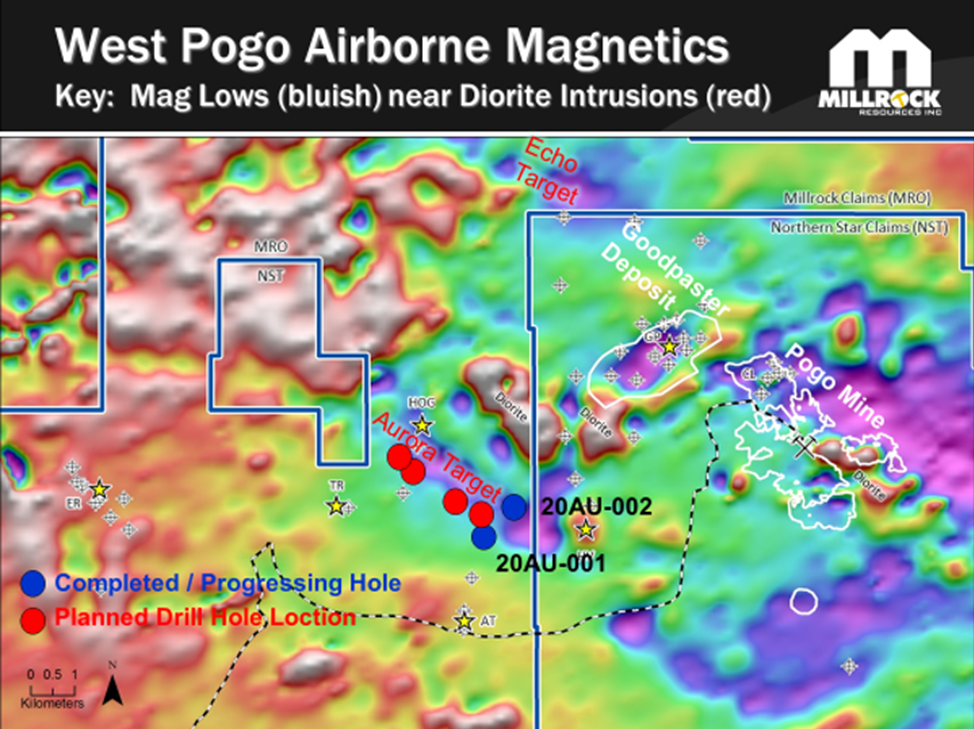

Brien Lundin: I’ve been recommending Millrock Resources Inc. (MRO:TSX.V; MLRKF:OTCQB), because their project adjacent to, on trend with, and surrounding the Pogo deposit in Alaska, is just amazing. They did an extraordinary joint venture agreement with an Australian company, where they will have $5 million of drilling accomplished this year.

They were just cut off by the COVID crisis and had to halt drilling after one-and-a-half holes. Now they got the results back from that first one and a half holes and they were disappointing.

And, in fact, the second hole didn’t reach the targeted depth, so it was really just one of the holes, and it didn’t turn up with good gold grades at all. So the stock has taken a hit.

But the key here is that the Pogo depositthe new drilling on the Pogo deposittrends onto their ground in two directions, and with $5 million of drilling upcoming, the chances that they’re going to vector into what could be a world-class deposit are very good. So, I still like that one and I think it’s a bargain right now.

Maurice Jackson: And likewise, the CEO there is a Gregory Beischer. You were discussing the 64North Project and the Aurora targets and yes, they only got about 25% completed there, but you couldn’t be in a better location. And again, the gold wasn’t high, correct, but the indicator minerals, they’re there, that’s what’s remarkable. It was identical, basically, to the Pogo mine, which is Northern Star Resources Ltd. (NST:ASX) by the way, that’s their neighbor there. But they’re within walking distance of that mine. Strategic location, you couldn’t beat it.

Brien Lundin: And the drilling of Northern Star kept going, progressing step by step closer to their property boundaries and essentially reached the property boundaries. And yes, the indicator minerals are there. The geology is just what they were looking for. The gold grades are barely anomalous at this point.

But with $5 million of drilling being done, they can vector in to where the higher grades are potentially, where you hope the higher grades and a deposit would be. It’s hard to vector, though, with one drill hole, because it’s just a point. But with $5 million worth of drilling, again, I have great confidence that they’ll be able to find what they’re looking for.

Maurice Jackson: And they have two strategic partners, Resolution Minerals Ltd. (RML:ASX) and EMX Royalty Corp. (EMX:TSX.V; EMX:NYSE.American) and they’ve done their due diligence.

Brien Lundin: And they always do: some of the smartest people in business.

Maurice Jackson: Absolutely. All right. Germane to this conversation, if the U.S. currency is going to lose purchasing power, how does moneyi.e., gold and silverfactor into one’s portfolio?

Brien Lundin: As you can imagine, I’ve gotten a lot of inquiries, and people are generalist investors, and we’re publishing a newsletter called Gold Newsletter that really is the preeminent, the longest-lasting, the first of the precious metals advisories out there. I get a lot of people coming to me and asking, “How do I get started?” And I tell them all the time, “You have to start with a physical allocation of precious metals, physical metals, either in your possession or accessible to you.” And you can build on that later and you can store more elsewhere, but you need to ensure your wealth with physical precious metals holdings.

You can then look into other ways to leverage these things we’re talking aboutof higher rising prices for gold and silver, which seem inevitable, and those are investmentsbut I tell them they need to have insurance for their wealth, insurance for everything they’ve worked for all their life, by holding physical gold and silver.

Maurice Jackson: Very, very responsible words. Thank you for sharing that. What does the current spot price of gold suggest to you, as the number of golden investors have been expecting a more robust response in the price?

Brien Lundin: When I began writing our May issue of Gold Newsletter, I was thinking, gold’s really got to get moving. And then I started reading the previous month’s issue, and then looked at the gold price. And said, “Damn, gold was $100 cheaper a month ago.”

And it’s $100 higher today, but it doesn’t seem like it’s really got that momentum and that’s because it had a really torrid run the first two weeks of April, and spent the last two weeks of April and now early May, just digesting those gains. It hasn’t fallen, it hasn’t really resumed the rally yet, but it’s been bouncing around that $1,700/ounce level.

I think it’s completely normal. I think gold’s waiting for the next shoe to drop, and the next indication that we’re going to have more and more of the stimulusand it’s going to get that because, as I said, the second-quarter GDP numbers are going to be absolutely horrendous. And Congress just has to get back to trying to fill the trough once again.

And they’re going to do that. We’re going to have more and more stimulus programs, the most accommodative Federal Reserve we’ve probably seen in history, and we’ve only just begun.

Maurice Jackson: I’m not a big fan of the big banks, but Bank of America recently shared that they expect the gold price to reach $3,000/ounce. So it’s not just you sharing this.

Brien Lundin: Yeah, yeah. And that’s a very staid, credible institution. They tend to be a little bit more dramatic than the other banks and the other big institutions. But still, that’s something that I’m even loath to say in interviews, without sounding crazy.

But that said, I fully expect it at some point and I think their logic is absolutely accurate and impeccable.

Maurice Jackson: We all have our favoritesgold, silver, platinum and palladium. May I ask, what are you buying right now and why?

Brien Lundin: I am buying more silver than gold. I am buying silver because it has not caught up to gold yet. It typically takes a while to catch up to gold in a long-term monetary-based gold bull market, which is what we’re in. It typically takes silver longer to respond, but then it outperforms gold. We haven’t really gotten to that outperform process yet, or stage yet, and I think we’re going to get there. So I’m buying physical silver; have been buying physical silver. And in general the mining stocks, I’m buying the exploration plays that I know a lot about.

Maurice Jackson: Can you share your outlook on all four of the metals referenced?

Brien Lundin: Yeah, I’m very bullish of gold. I tell people, if you like gold, you have to love silver, so they are one in the same, as far as the big drivers.

Platinum and palladium, I’m bullish on them but for different reasons. I think that there are genuine supply-demand dynamics in play for both of those metals that are inescapable. Right now. . .those precious metals had been abated a little bit, because a lot of the demand is driven by automobile demand and catalytic converter demand. So that will take a while to come back. But in the meantime, there are real supply issues with both of those metals, and I can tell you that the major producers are very bullish for the long term, and they’re looking to invest in new projects.

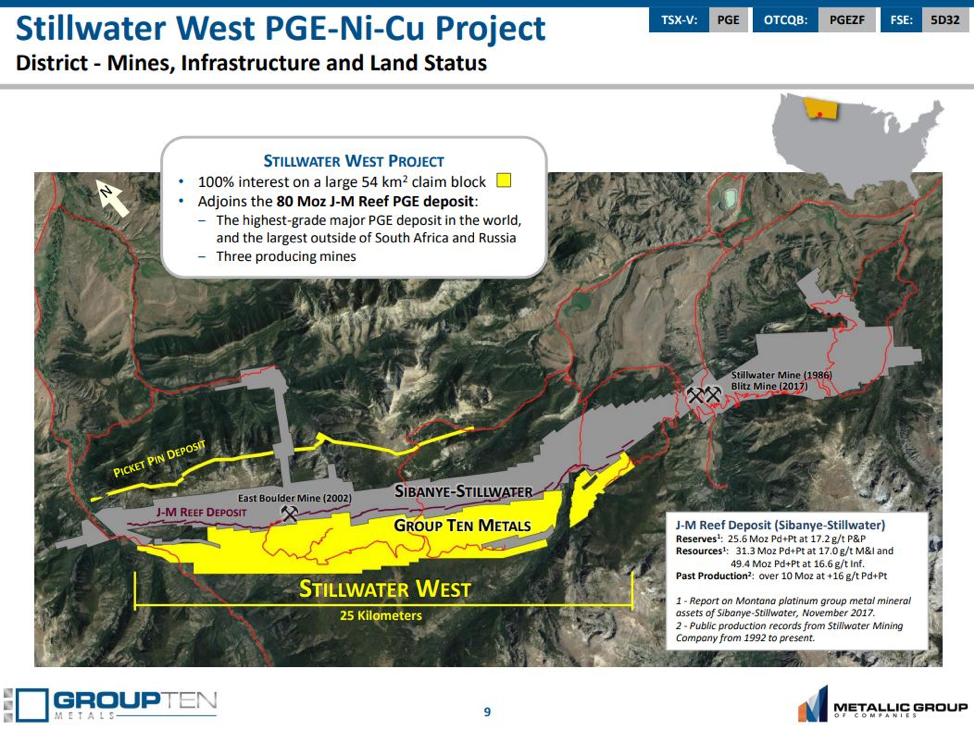

I just recommended Group Ten Metals Inc. (PGE:TSX.V; PGEZF:OTCQB; 5D32:FSE) recently. It’s another one of my platinum-palladium plays, and I think the majors are going to be aggressive. Over the next couple of years, there’s a window of opportunity for some of these PGM [platinum group metal] juniors are going to be taken out. And I know that those juniors are working toward that opportunity.

Maurice Jackson: And the CEO for Group 10 Metals is Michael Rowley. We had an opportunity to do a live webinar with him two weeks ago (click here). And the flagship project is the Stillwater West, located in Montana.

Switching gears, sir: you’re the host of the New Orleans Investment Conference, the world’s greatest investment event. For someone new, can you please introduce us to the New Orleans Investment Conference?

Brien Lundin: The New Orleans Investment Conference is the original retail investment conference, or really investment conference of any stripe. It was started in 1974 by Jim Blanchard, to teach American citizens how to invest in gold, and that right to invest in gold was something that Jim was instrumental in helping get back to American citizens. It had been taken away by Roosevelt in the 1930s.

So the modern gold bull market. . .has to thank the New Orleans conference for bringing that market to the populace, and showing retail investors how to buy gold, how to buy precious metals.

It’s not your typical conference. We cover all of the sectors, all of the asset classes, but we do have a golden thread that runs through our event, or golden theme that’s run through it over the decades, and we feature a lot of conservative/libertarian speakers. We feature a lot of big-name speakers that you won’t find at other events.

And the camaraderie of our attendees, and the intelligence that they’re willing to share, because they’re all generally very successful investors in their own rightit’s just an experience that you have to be there to really understand it. And we encourage anyone interested, whatever level of interest or experience they may be, if they’re interested in preserving their wealth and building it during uncertain times, they really do need to attend the New Orleans Conference.

Maurice Jackson: And speaking of attendance, what are the dates this year?

Brien Lundin: October 14 through 17, and we’re planning for a live event down here in New Orleans. It’s always a lot of fun. And we’re hopeful and actually expecting that all of this pandemic crisis and nervousness will be behind uswell behind usby then.

Maurice Jackson: Who are some of the featured speakers this year and the discussion topics?

Brien Lundin: Well, we’re featuring the best of the experts in gold, silver and alternative investments, and how to protect your wealth, and again, how to build it during these uncertain times. We’ve invited most of the major newsletter writers and commentators on the economy and on precious metals and mining stocks, because I really feel like this is an opportunity that only comes around once or twice in our investing careers. We’ve been very fortunate to be on the cutting edge of every bull market in the metals, and the results have just been stupendous for investors who come to our conference, who get the hottest picks from the world’s top experts and get to meet a lot of the companies in our exhibit hall.

Maurice Jackson: I’ve had the opportunity to attend five years at the New Orleans Investment Conference, and I must say it is very welcoming experience. No matter what your background is or level of investment experience is, you are welcome there with open arms and you have the opportunity to learn, not just from the speakers but from fellow investors, to share intellectual ideas and take them back home. The relationships that I’ve created in these last five years I still have today, and I thank you for that, sir.

Brien Lundin: Yes. And these attendees are my clients, but they grow to be, over the years have grown to be close friends, and it’s like an old-home week. Every year everybody gets together and makes new friends and greets old friends, and everyone is so willing to share their ideas and thoughts and strategies.

And I tell people every year, as we open the conference: “Y’all going to be looking at the stage, going to see some extraordinary speakers come up to the podium and give you their ideas over the next three, four days, but look around you in the audience. There’s just as much to be gained from the people that come to this event.” Because by coming to the New Orleans conference, they’ve already identified themselves as very smart, very active, intellectually curious, successful investors and there’s so much to be learned and shared amongst all of us.

Brien Lundin: Jefferson Financial is essentially the holding company that operates both the Gold Newsletter and the New Orleans Investment Conference, and publishes our very special reports and other special projects.

So Gold Newsletter is the first precious metals advisory. We’re now in our 50th year of helping investors navigate gold. In the first few years, Gold Newsletter was primarily involved in advocating for the legalization of gold ownership. That’s how long we’ve been around. The New Orleans Conference, as we’ve just said, is where we all get together every year and share ideas and our predictions for the future.

And I can tell you that in times like we’re in right now, it is not only not unusual, it’s expected for us to find companies and get stock recommendations of companies that go on to go up four or five, 10, 20 or more times in value. This is where you find opportunities like that. This is where you find investors that have that kind of potential.

Maurice Jackson: Before we close, sir, what keeps you up at night that we don’t know about?

Brien Lundin: Oh, well, lately maybe the pandemic, but really nothing keeps me up at night these days.

In regards to the economy, et cetera, I think that what we’re seeing play out right now in the economy has been inevitable for some time. And if I do have any worry, I guess it’s that not more investors know how to protect themselves through gold and silver.

You buy fire insurance, but you don’t really expect your home to catch on fire. But gold and silver are the insurance for an event that you know is going to happen, that you know the dollar is going to be depreciated over time. It’s insurance you only have to pay the premium one time, to get some protection. So it’s a thing that more people need to know about, and they need to do, and they need to do it now. We’re still in the very early stages of this game and we have literally years to come, of watching these trends play out and people really need to own gold and silver now, while they still can.

Maurice Jackson: And we’re proud to have an affiliation with the Gold Newsletter. Mr. Lundin, I think, are we not in the Gold Newsletter as a licensed representative for Miles Franklin?

Brien Lundin: Yes, actually we have an investor’s guide to gold and silver that tells people every way to invest in the precious metals, from physical metals, through mining stocks, even futures and options and more. But we also list the best dealers, the best conferences to go to, the best newsletters to subscribe to. So it’s all there in one stop shop, a 30-page special report that explains it all, and which also lists you, Maurice Jackson, as a recommended dealer.

Maurice Jackson: Well, we’re honored to be part of that elite team, sir. Last question. What did I forget to ask?

Brien Lundin: Well, I guess you forgot for me to give you a specific price prediction over a specific timeframe, which I would not have done anyway. But a lot of people try, a lot of people try.

Maurice Jackson: No, I think that’s responsible, because we don’t know where the currency is going to go and we don’t know the government’s response. So that’s a moving target.

But I think you said the most responsible thingthe prudent thing to do as a cornerstone for your investment portfolio is to own some physical precious metals. It’s insurance, and that’s the most responsible way I can approach it and I think you’ve covered well, sir.

Brien Lundin: Yes. It gives you peace of mind, so you can sleep at night knowing that you have that working for you.

And again, these trends are undeniable, they’re inevitable. People have gone through them throughout human history. It’s going to happen againthe dollar will be depreciated, so people need to own gold and silver.

Maurice Jackson: Mr. Lundin, for someone listening that wants to get more information on your work, please share the contact details.

Maurice Jackson: And as a reminder, I am licensed representative for Miles Franklin Precious Metals Investments, where we provide a number options to expand your precious metals portfolio, from physical delivery, offshore depositories and precious metals IRAs. Call me directly at (855) 505-1900 or you may e-mail maurice@milesfranklin.com.

Brien Lundin of Jefferson Financial, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Group Ten Metals, Millrock Resources, and Lion One Metals. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Group Ten Metals, Millrock Resources, and Lion One Metals are sponsors of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Lion One Metals, Group Ten Metals. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Group Ten Metals. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Millrock Resources, EMX Royalties and Group Ten Metals, companies mentioned in this article.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Small-cap UGE International boasts a $50 million project backlog and a $250 million pipeline.

Difficulties facing solar industry operators have been highlighted in recent reports, including by Bloomberg and the Washington Post; among the issues cited are decreasing demand among homeowners, disruptions in supply, and capital shortages.

But not all parts of the solar industry are equal, and while the industry as a whole may be facing headwinds, UGE International Ltd. (UGE:TSX.V; UGEIF:OTCQB) is thriving during the coronavirus-induced downturn. The firm, which focuses on project development in the commercial and community solar sector, announced at the end of March its largest project ever, a 6.6 MW solar installation in Westchester County, New York. The project will feed electricity into the grid and provide savings to community subscribers by selling them energy credits at a discounted rate.

“The project is approximately 12-15 times the size of UGE’s average project and, when completed, will produce power for an estimated 1,000 homes for the duration of the system’s lifetime,” the company stated. The company also has the option of installing battery storage, “which would provide a further boost to project revenue and returns.”

The project in Westchester may be just the tip of the iceberg for UGE. The firm currently has a committed project backlog valued at approximately $50 million, consisting of more than 40 projects, and a pipeline in excess of $250 million. The firm’s global solar experience has exceeded 400 MW.

Several macro factors are working in UGE’s favor. Large real estate owners are clamoring to rent UGE their rooftops, happy to have cash flow during the recession. “There has been a shift in the thinking of real estate owners; they are prioritizing finding ways to earn more revenue,” UGE’s CEO Nick Blitterswyk told Streetwise Reports. “Community solar allows real estate owners to boost revenue by receiving lease payments for their empty rooftops and open land, which is especially attractive during a time when their revenue may otherwise be decreasing.”

Under the community solar model, UGE rents a location, designs, constructs and, in most cases, finances the project, retaining ownership, selling the electricity to community members for less than the price the regional utility is charging. The company is maintaining ownership of many of its projects, allowing it to capture recurring revenue and boosting its gross margins. “The company’s gross margins jumped to 27% in 2019 as it transitioned to this model, from 10-20% in the years prior,” Blitterswyk noted.

UGE also believes it could benefit from the slowdown in construction that has accompanied the pandemic. “We should see more competitive costs for subcontractors and other expenses,” Blitterswyk said. “You could argue that costs of equipment are probably going to go down too.”

Interest rates have tumbled. “To the degree that interest rates are low, that helps us as well,” Blitterswyk explained.

While construction has been restricted in hard-hit areas, such as New York, even that has not affected UGE in a major way. “It may take nine months to fully mobilize, engineer and install a project. So from that perspective, the process is spread out anyway. We are definitely losing a couple of months, but construction is one of the first things opening up as restrictions ease,” Blitterswyk noted. The company “will focus on accelerating schedules once such local restrictions are lifted,” the company announced, and expects to be on-site in most regions that it operates in by the end of May.

Supply lines appear to be intact. “We’ve actually been seeing a surplus of panels. Most of the panels are made in Asia, and Asia seems to have the virus somewhat under control, and factories are producing,” Blitterswyk explained.

The firm notes that “new project development continues at a rapid pace, as demonstrated by the significant number of new projects won in recent weeks. UGE expects to move several of these new projects into the construction phase before the end of the year.”

“Of our $50 million backlog, we expect about one-quarter will be fulfilled in 2020 and the remainder in 2021, so we are looking at 80 to 100% growth in both 2020 and 2021,” Blitterswyk stated, “just based on the projects we already have under contract.”

UGE has around 24 million shares outstanding, and around 27.6 million fully diluted; management and insiders own 55%. The company’s market cap is around CA$6.7 million.

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: UGE International. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of UGE International, a company mentioned in this article.

North Macedonia’s central bank lowered its policy rate for the third time this year to support the economy by lowering the cost of financing and trimmed the amount of Treasury bills that will be auctioned to provide additional liquidity in the banking system that can be used to increase lending activity and mitigate the effects of the negative shock from the coronavirus. The National Bank of the Republic of North Macedonia cut its policy rate by another 25 basis points to 1.50 percent and has now cut it by 75 points this year following cuts in January and then at an emergency meeting on March 16. The bank’s operational monetary policy committee trimmed the amount of treasury bills, which together with the reduced offer in April, will release a total of 15 billion denars, and expanded the scope of instruments through which it can provide liquidity to the banking system. The central bank will now accept domestic government bonds with the longest maturities (15 and 30 years) as well as Eurobonds when purchasing securities as part of monetary operations. Although external and domestic risks to the economy continue, the central bank said moderate inflation and a stabilization of expectations and recent confidence, evidenced by the foreign exchange market, and deposits in the banking system, provided room for further monetary easing. Recent data for the first quarter of this year show continued but slower economic growth and average inflation in the first four months of the year was 0.4 percent, with inflation expectations around zero percent for this year. Foreign exchange reserves remain in what the central bank said was “a safe zone,” with net inflows from private transfers in the second half of April slightly lower than expected. The central bank’s intermediary policy objective since 1995 has been to target the denar’s exchange rate due to its significance in a small, open economy, the need for a nominal anchor to maintain credibility, the high level of use of the euro and the transparency of the exchange rate policy. The Macedonian denar rose in response to the rate cut to trade at 61.5 to the euro, but is unchanged on the year.

The progression of mass emotions in financial markets “tends to follow a similar path each time around”

By Elliott Wave International

The Wave Principle’s basic pattern includes five waves in the direction of the larger trend, followed by three corrective waves.

In a bull market, the pattern is five up, followed by three down. In a bear market, the pattern unfolds in reverse: the five waves trend downward and the correction trends upward.

Each of these waves sports its own characteristics.

As the Wall Street classic book, Elliott Wave Principle: Key to Market Behavior, by Frost & Prechter, says:

The personality of each wave in the Elliott sequence is an integral part of the reflection of the mass psychology it embodies. The progression of mass emotions from pessimism to optimism and back again tends to follow a similar path each time around.

For example, strong price advances on high volume typically happen during wave 3 in a bull market. Of course, in a bear market, the strong price action is downward.

Returning to Elliott Wave Principle:

Third waves usually generate the greatest volume and price movement and are most often the extended wave in a series.

Let’s review an instance of a third wave in a downturn from recent financial history.

Here’s a chart and commentary from Elliott Wave International’s Aug. 21, 2015 U.S. Short Term Update:

This week’s sharp decline is clearly a third wave. It sports a steep slope with strong downside breadth and volume.

During the next trading session (August 24, 2015), the Dow fell nearly 1,100 points at the open.

As you might imagine, it would be highly helpful to learn how to anticipate third waves so one can prepare.

Indeed, Elliott Wave International has just made the 1-hour course, The Wave Principle Applied, free through May 15 for free Club EWI members. Club EWI membership allows you to get Elliott wave insights on investing and trading, the economy and social trends that you will not find anywhere else.

The Wave Principle Applied normally sells for $99, so you are encouraged to take advantage of this limited-time offer to access the course for free.

As the Wall Street classic book, Elliott Wave Principle: Key to Market Behavior, by Frost & Prechter says:

Without Elliott, there appear to be an infinite number of possibilities for market action. What the Wave Principle provides is a means of first limiting the possibilities and then ordering the relative probabilities of possible future market paths. Elliott’s highly specific rules reduce the number of valid alternatives to a minimum.

This article was syndicated by Elliott Wave International and was originally published under the headline Why This Wave is Usually a Market Downturn’s Most Wicked. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

The coronavirus pandemic is devastating small businesses across the U.S. because of shelter-in-place orders that have forced millions to temporarily close.

So far, Congress has devoted more than US$375 billion to helping restaurants, retailers and other small companies endure the crisis, and lawmakers are currently discussing spending hundreds of billions more.

The Small Business Administration is at the center of these efforts. But early reports suggest the agency is struggling with the flood of requests it’s received for loans – more than 70% of U.S. small businesses have reportedly already applied for assistance – leading to a lot of frustration among owners desperate for support.

From 2010 through 2014, I worked as general and then-chief counsel to the U.S. Senate Committee on Small Business and Entrepreneurship, where I helped write laws to aid small businesses recover from the Great Recession.

Congress’ quick actions are encouraging, but I believe the SBA needs to do more to ensure aid goes to those most in need – including the more than 13 million small businesses owned by women that have challenges accessing capital even under normal circumstances.

Image by Free-Photos / Pixabay

An advocate for small business

The Small Business Administration was established in 1953 as an independent agency dedicated to counseling and advocating for small businesses. It replaced existing lending and contracting programs established during the Great Depression and World War II.

Over time, the SBA’s mission has grown to include a suite of lending programs, contracting and entrepreneurial development initiatives.

Its roots in helping small businesses compete for government contracts has resulted in a range of definitions as to what constitutes a small business. SBA itself has different definitions depending on industry, which can range from 100 to 1,500 employees or $750,000 to $38.5 million in annual sales.

One of the SBA’s main duties is providing aid to small businesses to help them recover following natural disasters such as hurricanes or tornadoes and other crises.

For example, the SBA dispensed $3.59 billion in disaster loan assistance in fiscal year 2018 following the devastation caused by hurricanes Harvey, Irma and Maria in 2017.

But the SBA has never done anything on the scale it’s being asked to do to help small businesses survive the coronavirus pandemic.

The first piece of legislation Congress passed in response to the crisis in early March included $20 million in emergency supplemental funding for SBA’s economic injury disaster loan program, which offers loans of up to $2 million.

Realizing that small businesses that were being forced to shut down in droves would need significantly more aid, Congress added hundreds of billions more funding in the $2 trillion CARES Act, which was signed into law on March 27.

The law gave $10 billion more to the SBA’s Economic Injury Disaster Loan Program to allow the SBA to hand out up to $10,000 grants immediately to applicants who are eligible for the program – even if they are ultimately denied.

In addition, it created the $349 billion paycheck protection program in an effort to encourage companies to continue to employ their workers during the pandemic. The program allows companies with fewer than 500 employees to receive as much as $10 million. Money used for “allowable” expenses such as payroll and rent doesn’t have to be paid back as long as a few other conditions are met.

Lawmakers are considering ways to provide small businesses with more support – perhaps another $250 billion or more – in another bailout package.

Unprecedented need

But the unprecedented size of the need has led to many stumbling blocks in rolling out the programs.

The New York Times reported that applicants are waiting weeks for approval, while others are being told they will get a fraction of what they expected.

In addition, other reports have found that the $10,000 emergency grants that were supposed to be available within three days haven’t gone out to at least some applicants. An SBA official said the agency has already received over 3 million applications for the grants, which would cost $30 billion, triple the amount originally set aside.

And there was confusion over the rules companies must follow. On April 3, the SBA issued an interim final rule that said 75% of the proceeds of the paycheck protection program loan must go to payroll costs, which wasn’t in the CARES Act. Retailers, restaurants and other companies with high rents and other overhead complain that they won’t be able to meet that threshold.

Challenges for women-owned businesses

The situation is urgent as research shows that about half of small businesses typically have cash on hand to last 15 days. At the same time, loans are distributed on a “first-come, first-serve” basis.

And for businesses owned by people of color or women, things can be even more acute. My own research, for example, found that women-owned businesses tend to lack access to capital and often don’t benefit from tax breaks and other support intended for small companies. And because they are less likely to have banking relationships with the lenders the SBA traditionally works with, women business owners may need special attention to ensure they get the support they need to weather this crisis.

While getting money out the door fast is critical, it’s equally important it gets to the companies that need it most.

Trade talks between the UK and US have officially begun. Both parties are working towards a free trade agreement – a full deal, as opposed to something like the recent China-US “mini deal” that focuses on certain export targets to manage trade between the two countries. Like a lot of relationships at the moment, this one is being negotiated over video.

There are doubts over the timeline of when these talks will come to a conclusion. As well as the coronavirus pandemic, the picture is further complicated by the ongoing EU-UK talks. But at the outset of this process there are some things we know about what each side is looking to get out of a deal.

What the UK wants

The US is already the UK’s biggest destination for goods, sending 13% of its exports there in 2018. The UK wants better access for these US-bound exports, particularly food and agricultural products, though those only account for 5% of its US exports overall.

Improving market access relies on an array of factors, starting with tariffs. For example, ceramics face a particularly high tariff of 28%, as do some categories of textiles, at 32%.

Agreement must also be reached on rules of origin, where there is a joint understanding as to how the origin of each product will be decided. This is very important since 70% of trade involves global value chains, so most goods have value added by producers from more than one country. This means that deciding on a single origin for each product is tricky and may have an impact on the costs of trading, since various duties depend on the origin of the product. Further issues involve technical barriers to trade, standards, and agreements on testing procedures.

As well as goods, trade in services is also on the agenda. The UK is keen to see improved market access for UK services in accountancy, architecture and finance, as well as freedom of movement and mutual recognition of professional qualifications.

What the US wants

The US already has lower tariffs than the UK for most categories of goods, so it would expect more concessions from the UK side in this regard. For instance, US tariffs on imported cars are 2.5%, while UK tariffs are 10%.

The UK currently meets EU regulations for environmental, fuel efficiency and safety standards for cars. A comparison of EU and US regulations shows numerous differences: the US directly sets minimum fuel efficiency, while the EU does not; the EU and US have different emission standards. Even seatbelt regulations differ. This has important implications for how cars are built, making it more difficult and expensive to export cars to both markets.

The US team will also push for US products to be traded more freely in the UK market – hence, chlorinated chickens and other agricultural and food products produced according to US standards.

When it comes to services, the US will want to better access for its healthcare and pharmaceutical companies. So even though the UK government says that the NHS is not on the table, we can expect US negotiators to try and gain access to it.

EU looms large

These UK-US negotiations cannot be separated out from those between the EU and UK, since US demands are bound to clash with some EU rules and regulations. This will lead to a painful trade-off for the UK, which will have to choose between closer economic ties to either the EU or US.

The fact that the US is a much smaller trade partner than the EU means potential gains from the UK-US deal are quite small. When you add the issue of regulations to this – the UK and EU are already much more closely aligned, whereas the US has a much more liberal policy environment – the UK has a lot to lose from worsened access to EU markets.

We show in our research that even if the UK manages to secure preferential trade arrangements with the US and the Commonwealth countries combined, it will not offset the negative impact of Brexit. Because the EU is the UK’s biggest trade partner, the UK will benefit the most from securing a full free trade deal with the EU.

Negotiating tactics

The UK is using an interesting negotiating tactic of launching simultaneous trade talks with the EU and US. The idea is that if it achieves good progress in its trade talks with the US, it can use this as leverage to influence negotiations with the EU.

This approach has been criticised by some trade experts because it spreads the UK negotiating capacities too thin and creates difficulties in coordinating these talks. The fact that the negotiations must now be carried out remotely makes it even more difficult due to the logistical constraints of talking over video.

The US-Japan Trade Agreement came into effect this year after six months of negotiations and using a fast-track approvals process in the US. However, this was really only another mini-deal concentrating on tariffs and digital trade. This suggests that a comprehensive UK-US deal will take much longer and would need a vote in Congress.

In between dealing with the COVID-19 outbreak and the associated economic fallout, as well as the US elections, it may take a while before we see any results from these virtual negotiations. And we must remember that the UK government’s own modelling suggests that a deal will bring limited economic gains for the UK.

New Zealand’s central bank kept its key policy rate steady at a record low of 0.25 percent and said negative interest rates were a future option but for now it would boost its purchases of government bonds as further stimulus is needed to support a recovery in economic activity, employment and inflation. The Reserve Bank of New Zealand (RBNZ), which slashed its benchmark Official Cash Rate (OCR) by 75 basis points to their current level on March 16, said it would expand its Large Scale Asset Purchase (LSAP) program to $60 billion from an earlier limit of $33 billion as the “economic situation has deteriorated since the previous policy meeting” in light of the global efforts to contain the spread of the COVID-19 pandemic. Although measures to contain the virus in New Zealand have limited its spread and the number of new cases had declined, this has severely disrupted manufacturing, tourism, hospitality and construction sectors. It has also reduced global and domestic demand as the income of both households and businesses has fallen, uncertainty has risen and business investment is lower. “The sharp contraction in activity is expected to reduce inflation and employment below the Bank’s objectives for several years,” RBNZ said, forecasting a 22 percent plunge in economic output in the second quarter of this year. Although RBNZ said the government’s $52 billion spending is the main method for supporting the economy at this time, the balance of economic risks remain to the downside and members of its monetary policy committee agree that a “least regrets monetary policy approach is needed, delivering stimulus sooner rather than later, and thus minimizing the risk that the stimulus delivered turns out not to be enough.” The central bank will do its part in supporting economic activity by keeping interest rates low for the foreseeable future, RBNZ said, forecasting OCR will remain at its current level through March 2021 and expects a fall in retail interest rates as lower borrowing costs for banks are passed on. “The Monetary Policy Committee is prepared to use additional monetary policy tools if and when needed, including reducing the OCR further, adding other types of assets to the LSAP program, and providing fixed term loans to banks,” RBNZ said. The asset purchase program was expanded to include NZ Government Inflation-Indexed Bonds in addition to New Zealand government bonds and local government funding agency bonds (LGFA). RBNZ has cut OCR by 150 basis points since it first began cutting in May 2019 and said a negative rate is an option in the future though presently financial institutions were not operationally ready for such a move so any further rate cut now would not achieve the objective of reducing borrowing rates for New Zealanders. However, it added that discussions with financial institutions about preparing for a negative OCR were ongoing but expanded asset purchases was the most effective way to deliver stimulus at this time and this can be scaled as needed. Given the uncertainty surrounding the spread of the coronavirus, the monetary policy committee discussed three economic scenarios based on the government’s containment measures. Under the baseline scenarios, which was the most optimistic of the three, annual gross domestic product growth among New Zealand’s key trading partners declines 4 percent this year but then gradually rises from 2021, while inflation averages just over 1.8 percent due to spare capacity and oil prices recover to around US$35 per barrel over the next two years. New Zealand’s economy, which already slowed sharply last year to the lowest since 2013, is seen slowing to growth of 1.3 percent this year and then contracting 8.4 percent in 2021. In 2022 GDP will bounce back and expand 9.6 percent and then grow 3.3 percent in 2023. Inflation, which rose in the first quarter to 2.5 percent, the highest since 2011, from 1.9 percent in the fourth quarter of 2019, is forecasts to average 2.5 percent this year before declining 0.4 percent in 2021 and then rising to 0.9 percent in 2022 and 1.6 percent in 2023.

The Reserve Bank of New Zealand issued the following statement:

“Tēnā koutou katoa, welcome all.

The Monetary Policy Committee has agreed to significantly expand the Large Scale Asset Purchase (LSAP) programme potential to $60 billion, up from the previous $33 billion limit. The LSAP programme includes NZ Government Bonds, Local Government Funding Agency Bonds and, now, NZ Government Inflation-Indexed Bonds.

The global economic disruption caused by the COVID-19 pandemic is expected to persist and lead to lower economic growth, employment, and inflation both in New Zealand and abroad. Even if New Zealand successfully contains the spread of disease locally, reduced world activity will mean lower demand for many of New Zealand’s exports.

The Monetary Policy Committee is committed to achieving its employment and inflation objectives. The main support for the economy in this environment is appropriately being provided through increased fiscal spending. However, monetary policy will continue to provide significant support through keeping interest rates low for the foreseeable future.

The balance of economic risks remains to the downside. The expansion to the LSAP programme aims to continue to reduce the cost of borrowing quickly and sharply. This is preferable to delivering a smaller amount of stimulus now, only to risk later realising more should have been done.

We expect to see retail interest rates decline further as lower wholesale borrowing costs are passed through to retail customers. It remains in the best long-term interests of the banking sector to promptly maximise the effectiveness of our LSAP programme.

The Official Cash Rate (OCR) is being held at 0.25 percent in accordance with the guidance issued on 16 March. The Monetary Policy Committee is prepared to use additional monetary policy tools if and when needed, including reducing the OCR further, adding other types of assets to the LSAP programme, and providing fixed term loans to banks. The Committee’s decisions are guided by the Reserve Bank’s mandate and our decision making principles on the use of alternative monetary policy instruments.

Meitaki, thanks.

Summary Record of Meeting – May 2020 Statement

The Monetary Policy Committee noted that the economic situation has deteriorated since the previous policy meeting. The COVID-19 pandemic is affecting economic activity throughout the world. The unprecedented health crisis has led many countries to introduce measures to contain the spread of disease. In New Zealand, activity has fallen sharply as a result of the pandemic and containment measures. The sharp contraction in activity is expected to reduce inflation and employment below the Bank’s objectives for several years.

Members discussed the significant uncertainties surrounding the economic outlook. The pandemic and restrictions on the movement of people are uncharted territory for modern economic policy. Here, and overseas, there is uncertainty about the impact of containment measures on economic activity. Monetary policy is using tools which have not been deployed before in New Zealand, and their degree of success is something that will become evident over time.

To help understand the uncertainties, the Committee discussed several different scenarios for the economic outlook. Members agreed that the situation is too uncertain to allow any one scenario to be treated as a central projection. Three scenarios were discussed, including what could happen if extended containment measures are required. Members noted that the baseline scenario was the most optimistic of the three. All three scenarios involved a significant and unprecedented decline in economic activity and employment.

The Committee noted that more stimulus is needed to support a medium-term recovery in economic activity, employment, and inflation. Members noted that the main thing needed to support the economy is fiscal stimulus, given that fiscal policy is best placed to directly support households and businesses. The role of monetary policy is to support the economy by ensuring that interest rates remain low, which will complement the effects of fiscal measures.

Members discussed the fiscal assumptions in the economic scenarios. It was noted that the government has publicly announced that $52 billion has been made available for pandemic recovery packages. This figure is used as the core fiscal spending assumption in each scenario.

Members agreed that a ‘least regrets’ monetary policy approach is needed, delivering stimulus sooner rather than later, and thus minimising the risk that the stimulus delivered turns out not to be enough.

The Committee discussed the world economic situation. Members noted the global environment is volatile and uncertain. Some commodity prices are strong, but many of New Zealand’s trading partners are experiencing economic disruption and declining activity. Despite pockets of relative strength, conditions in trading partners will be a drag on domestic activity.

The Committee discussed the balance of risks around the baseline scenario and agreed that the risks are to the downside. Activity could be lower than expected as a result of containment measures having more severe economic effects than assumed. Another risk is that the pandemic itself lasts longer or has more severe effects on trading-partner economies than assumed. There is also uncertainty about the impact of monetary policy actions on the economy.

Members noted some chance that activity could be higher than expected. There is some possibility that trans-Tasman travel could restart earlier than assumed, or that a return to alert level 1 could happen sooner than expected. Either of these events would result in spending and employment recovering faster. Another possibility is that supply-chain disruption leads to relative price shifts for specific consumer products, keeping average inflation higher than expected. Members agreed that these possibilities were not material enough to shift the overall balance of risks around the baseline scenario.

The Committee noted evidence on the effects of the Large Scale Asset Purchase (LSAP) programme so far. Members were pleased to note that both wholesale and retail interest rates have fallen. The functioning of markets has also improved – a secondary goal of the LSAP programme. Further declines in retail interest rates would be needed to fully deliver the stimulus. The Committee noted that long-term interest rates in the government bond market are also sensitive to a number of factors outside the LSAP programme, including bond issuance and foreign bond yields.

The Committee discussed the secondary objectives of monetary policy. Some members expressed concern about financial stability due to the economic disruption of the pandemic. The Committee noted that the banking system is sound and markets are functioning satisfactorily. Members agreed that all policy areas – monetary, financial stability, and fiscal – are mutually reinforcing in this environment, all working to achieve complementary goals.

The Committee discussed the range of monetary policy options. Members noted that there are policy tools available that have not yet been used. The Committee agreed that it will stand ready to deploy further tools as needed, should the need for stimulus continue to increase. Tools available include further reductions in the OCR; a term lending facility; and adding other asset classes, such as foreign assets, to the LSAP programme.

The Committee noted that a negative Official Cash Rate (OCR) will become an option in future, although at present financial institutions are not yet operationally ready. The current goal of monetary policy tools is to reduce borrowing rates for New Zealanders, and further OCR reductions at this stage would not be effective in achieving that. Consequently, the Committee reaffirmed its forward guidance that the OCR will remain at 0.25 percent until early 2021. It was noted that discussions with financial institutions about preparing for a negative OCR are ongoing.

Members agreed that an expansion to the LSAP programme is the most effective way to deliver further stimulus at this time. The Committee noted advice that adding inflation-indexed government bonds (IIBs) to the LSAP would improve both market function and policy effectiveness. The Committee agreed to add IIBs to the LSAP.