Global equities are mixed today after a volatile session on Thursday with US Labor department report showing nearly 36.5 million Americans have lost their jobs in the last eight weeks. Investors are awaiting for US retail sales report today – expected to show retail sales decline accelerated in April.

Forex news

Currency Pair

Change

EUR USD

-0.03%

GBP USD

-1.8%

USD JPY

+0.09%

AUD USD

+0.08%

The Dollar strengthening continues today ahead of April retail sales report expected to show sales drop accelerated to 12% over month from 8% in March. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.1% Thursday depite report initial jobless claims jumped another 2.98 million last week. Both GBP/USD and EUR/USD continued sliding yesterday with both pairs lower currently ahead of German GDP report expected to show German economy shrank in first quarter. Both USD/JPY and AUD/USD reversed sliding yesterday but are lower currently.

Stock Market news

Indices

Change

Dow Jones Index

+0.2%

Nikkei Index

+0.71%

Hang Seng Index

+0.29%

Futures on three main US stock indexes are mixed currently after a rebound Thursday. Earnings season is nearing the end with another batch of companies including Foxconn, Mitsubishi UFJ Financial Group and Sumitomo Mitsui Financial Group reporting quarterly results today. Stock indexes in US recovered most of previous session losses on Thursday led by banking shares: the three main US stock indexes recorded gains ranging from 0.9% to 2.6%. European stock indexes are rising today after ending solidly lower Thursday led by auto stocks. Asian indexes are mixed today after President Trump said White House is considering barring Chinese stocks trading on US exchanges unless they follow US accounting rules. However Australia’s All Ordinaries ASX 200 Index gained 1.4% while Shanghai Composite slipped 0.1%.

Commodity Market news

Commodities

Change

WTI Crude

+2.68%

Brent is extending gains today. Oil prices rallied yesterday despite the International Energy Agency forecast world demand for crude will drop by 21.5 million barrels a day this month. However the IEA upgraded its estimate for 2020 demand drop forecasting global crude demand will fall by 8.6 million barrels a day versus its April forecast for a fall of 9.3 million barrels a day. The US oil benchmark West Texas Intermediate (WTI) futures ended sharply higher yesterday: June WTI gained 9% and is higher currently. July Brent crude closed 6.7% higher at $31.13 a barrel on Thursday.

Gold Market News

Metals

Change

Silver

+0.4%

Gold prices advance is intact today. June gold rose 1.4% to $1740.90 an ounce on Thursday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

To calibrate current forecasts — such as the International Monetary Fund’s prediction of a 6.2 per cent decline in Gross Domestic Product for Canada — I’ve looked at the history of similar worldwide economic shocks, studied macroeconomics models and reviewed nearly 75 studies to better understand what might happen in a post-pandemic world.

The economic effects of 1918-20 flu

The influenza outbreak of 1918-20 killed at least 40 million people, or approximately two per cent of the world’s population. In Canada alone, at least 50,000 deaths were attributed to the flu, approaching the number of Canadian deaths in the First World War. Solid data about GDP did not exist for that era, so economic historians have to recreate economic measurements based on the data that was collected.

The most thorough study focuses on how the influenza pandemic 100 years ago affected Sweden. The Swedish study took advantage of the fact that the country kept very detailed data on causes of death, as well as having a history of accurate economic record-keeping dating back to the 1800s.

Sweden was a neutral country in the First World War, so unlike other Western nations, the war had limited impact on the country’s economy. The fatality rate from the flu in Sweden was comparable to most Western nations and its economy was similar to other developed countries.

The study of Sweden’s flu experience a century ago suggests there could be permanent negative long-term economic effects from the current pandemic. There was a decline in income from capital sources such as interest, dividends and rents of five per cent that lasted at least until 1929. This was a permanent decline not recovered once the flu pandemic passed.

Swedish poor never recovered

There was also an increase in absolute poverty for those Swedes at the bottom of the economic pyramid: enrolment in government-run “poorhouses” in higher flu-incidence regions jumped 11 per cent and did not decline over the next decade. There was some good news: while employment income was reduced during the crisis, it quickly rebounded to predicted normal levels.

A recent study attempts to measure the effects of the influenza on 1918-21 GDP. Harvard economist Robert Barro and his colleagues painstakingly put together a set of economic data that attempts to recreate what GDP in 42 countries would have been.

They have found that the flu was responsible for an additional six per cent decline in global GDP. The study concludes that the effects were reversed by 1921. This estimate of the flu’s historical GDP effects is strikingly similar to the IMF’s current prediction of six per cent reduction in GDP for Western economies as a result of the coronavirus pandemic.

Modelling economic effects of a pandemic

Beyond economic history, we can look at macroeconomic models of the global, regional or national economies that run scenarios about pandemic economic shocks.

One scenario by British economists and health science academics is particularly apt in light of COVID-19.

Their scenario models virus incidence and fatality rates close to the current best estimates and includes strong and early social distancing measures such as school closures and work-from-home arrangements that we see today in many countries fighting the pandemic.

Their model estimates a 21 per cent decline in U.K. GDP in the first full quarter of the pandemic, with a 4.45 per cent decline in GDP for first year. The model also suggests the time frame to economic recovery is about two years. The current IMF projection for the U.K. is a 6.5 per cent decline in annual GDP.

There is no doubt that COVID-19 is a major shock to the global economy. Across all the studies I reviewed, the conclusion of a significant decline in GDP in the order of 4.5 to six per cent with full recovery within two years seems to be well justified.

The economic history of the influenza pandemic 100 years ago suggests early easing of social distancing measures and the inability to develop an effective vaccine contributed to second and third flu waves. These waves might have greater effects on the modern service-based economy of Western nations than they did on the more agrarian economy of 100 years ago.

Economic history serves as a potential warning that the economy could get much worse if these measures are ignored.

It’s important to remember that GDP is a marker of a nation’s overall economic health. On an individual level, the effects may be more far-reaching and painful. There are financial and professional losses that may never be recovered.

The 1918-20 flu offers an important history lesson for the world’s current economic outlook: there may be significant declines in the returns to capital in the next decade, as well as relative increases in poverty for the neediest in our society.

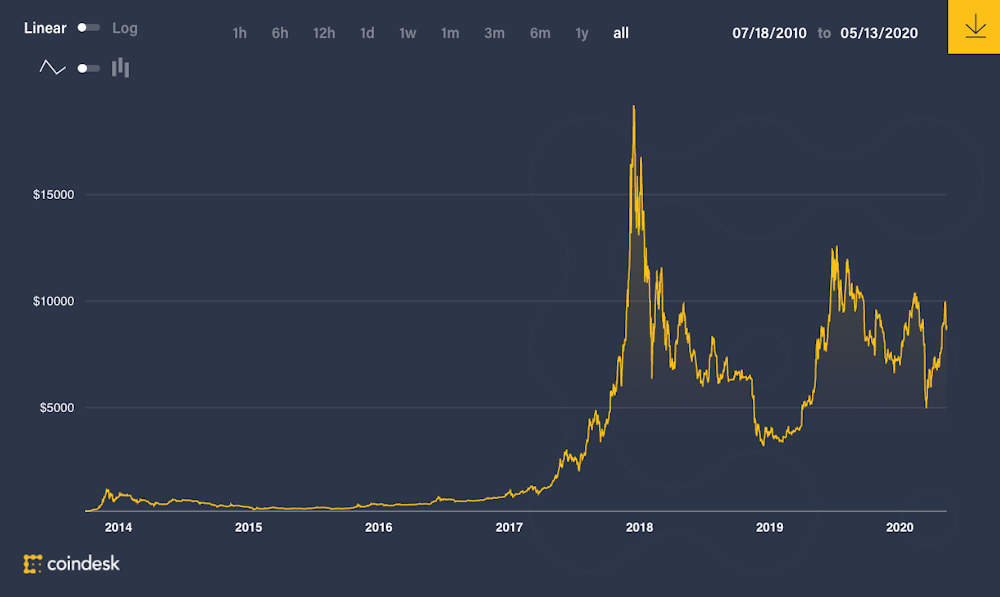

Bitcoin, the first and leading cryptocurrency in terms of trading volume and market capitalisation, went through its third “halving” on May 11 2020. This major adjustment to how the cryptocurrency operates has only happened twice before and happens every four years. But what does this actually mean and what impact will it have?

Q: how does bitcoin work?

Bitcoin is a digital currency that makes use of blockchain technology to store and record all transactions. First proposed in a white paper published online in 2008 by a mysterious person (or group of people) called Satoshi Nakamoto. The unique features of bitcoin compared to fiat currencies like dollars or pounds are that there is no central authority or bank. Each member of the network has equal power. This decentralised network is completely transparent and all transactions can be read on the blockchain. At the same time it offers privacy in terms of who owns the cryptocurrency.

Bitcoins are created (or mined) by so-called miners who contribute computing power to securing the network, as well as processing transactions on the network by solving complex mathematical puzzles through computational power. These miners are rewarded for their work processing the transactions on the blockchain with bitcoins. But to combat inflation, Nakamoto wrote into the code that the total number of bitcoins that will ever exist will be 21 million. Right now there are 18.38 million.

The first ever block recorded on the bitcoin blockchain was on January 3 2009 where Nakamoto received 50 bitcoins. In the white paper, Nakamoto specified that after every 210,000 blocks the reward for miners will half. So the first halving took place on November 28 2012 where the miner’s reward was reduced from 50 bitcoins to 25 bitcoins. The second halving was on July 9 2016 and the miner’s reward was reduced from 25 bitcoins to 12.5 bitcoins. And the third, most recent halving on May 11 2020 means bitcoin miners now receive 6.25 bitcoins.

Q: Why does bitcoin halve?

Nakamoto has never explained explicitly the reasons behind the halving, but many, such as Michael Dubrovsky, co-founder of cryptocurrency mining firm PoWx, have speculated that the system was designed to distribute coins more quickly at the beginning to incentive people to join the network and mine new blocks. Block rewards are programmed to halve at regular intervals because the value of each coin rewarded is deemed likely to increase as the network expanded. However, this may lead to users holding bitcoin as a speculative asset rather than using it as a medium of exchange.

Q: What impact does halving have on bitcoin?

The obvious impact is that the amount of newly mined bitcoins per day will fall from about 1,800 to 900 bitcoins and the daily revenue of miners will reduce by half. This decrease in the rate of bitcoin creation tightens supply and some argue will lead to a bullish market and an increase in the price of bitcoin.

Meanwhile, the reduction of revenue for miners may squeeze out miners who are least efficient and therefore the computing power connected to the Bitcoin network may fall significantly.

The previous two halvings led to the most dramatic bull runs in Bitcoin’s history, although initially there was a brief sell-off. Marcus Swanepoel, co-founder and CEO of Luno, a cryptocurrency wallet which lets you store and carry out bitcoin transactions, believes that bitcoin may achieve a growth of 270% between this and the fourth halving in 2024.

Q: How is coronavirus affecting things?

Although bitcoin has gained more than 20% since the beginning of the year, where this halving may differ from its predecessors is the volatile and uncertain economic environment that it has taken place in. The International Monetry Fund predicted a 3% shrinking of global growth in its April forecast and this is expected to fall further. In the UK, the Bank of England has projected a decrease of 30% in the country’s GDP during the first half of 2020.

The only certainty is that the growth of new bitcoins has halved. It remains to be seen what impact this will have on the price and interest of this cryptocurrency.

Mexico’s central bank lowered its benchmark interest rate for the third time this year, as expected, saying it had room to ease its monetary policy stance further in light of falling inflation and a considerable contraction of economic activity. The Bank of Mexico, known as Banxico, cut its target for the overnight interbank interest rate by another 50 basis points to 5.50 percent and has now cut it 175 basis points this year following cuts in February, March and April. Since August 2019, when Baxico began to unwind some of the 500-basis points hikes from December 2015 to December 2018, the rate has been cut eight times by 275 points. The bank’s governing board was unanimous in its decision.

The Bank of Mexico issued the following statement:

“Banco de México’s Governing Board decided to lower the target for the overnight interbank interest rate by 50 basis points to 5.5%. In view of the complex economic and financial situation worldwide, Banco de México has been closely monitoring the behavior of domestic financial markets, economic activity and inflation, in order to take the necessary actions in a timely manner. The COVID-19 pandemic and the measures adopted to prevent its spread have affected world economic activity considerably. This has led to unprecedented revisions of economic expectations, which incorporate a strong contraction of productive activity in 2020. In turn, this has resulted in a sharp fall in commodity prices, especially of crude oil. As a consequence of these factors, several central banks have reduced interest rates significantly and implemented other extraordinary measures to foster the proper functioning of their financial markets. Likewise, several countries have implemented fiscal stimulus measures to mitigate the adverse effects on employment and on households and firms’ income. This environment has led to a significant deterioration of global financial conditions, to a recomposition of investors’ portfolio towards lower risk assets, and to the greatest contraction ever recorded of holdings of emerging economies’ assets, especially of fixed-income instruments. This adjustment contributed to a depreciation of these economies’ currencies and to volatility in their foreign exchange markets, including the Mexican peso. The actions adopted by advanced economies to provide liquidity and restore financing have contributed to the more stable behavior observed in international financial markets. Such actions have also contributed to the better performance of domestic financial markets over the last weeks, where lower interest rates on government securities for all terms were registered, while the Mexican peso exchange rate traded in a narrower range. Nevertheless, global and domestic financial conditions will continue to be subject to the outlook for the effects of the pandemic. Available information shows that economic activity in Mexico contracted significantly during the first quarter of the year, incorporating the effects associated with the pandemic in March, which affected the production of goods and services considerably. Although the magnitude and duration of the effects of the pandemic are still unknown, these are expected to intensify during the second quarter, and to result in a significant contraction of employment. Slack conditions thus continue to widen considerably, in a context in which the balance of risks for growth is significantly biased to the downside. Annual headline inflation decreased from 3.25 to 2.15% between March and April 2020 due to declines from 2.19 to -1.96% and from 3.60 to 3.50% in its non-core and core components, respectively. A particularly relevant factor was the decline in the annual change of energy prices, particularly of gasoline. Short-term expectations for headline inflation have decreased, while those for long and medium terms have remained relatively stable, albeit at levels above the 3% target.

The challenges for monetary policy posed by the pandemic include both the unprecedented impact on economic activity as well as those associated with the financial shock that we are currently facing. As for the risks to the foreseen trajectory of inflation, the most important to the downside are a significant widening of the negative output gap and the effects of the fall in energy prices. To the upside, a greater or more persistent depreciation of the peso and possible disruptions to chains of production and distribution of certain goods and services. In this context, the balance of risks for inflation remains uncertain. Taking into account the referred risks for inflation, economic activity and financial markets, major challenges arise for monetary policy and for the economy in general. Considering the room for maneuvering that on balance monetary policy has as a result of these implications, and with the presence of all its members, Banco de México’s Governing Board decided unanimously to lower the target for the overnight interbank interest rate by 50 basis points to a level of 5.5%. The Governing Board will take the necessary actions on the basis of incoming information and considering the large impact on productive activity as well as the evolution of the financial shock that we are currently facing, so that the policy rate is consistent with the orderly and sustained convergence of headline inflation to Banco de México’s target within the time frame in which monetary policy operates. Perseverance in strengthening the macroeconomic fundamentals and adopting the necessary actions, regarding both monetary and fiscal policies, will contribute to a better adjustment of domestic financial markets and of the economy as a whole.” www.CentralBankNews.info

The development timeline for Inovio Pharmaceuticals’ coronavirus vaccine candidate is discussed in an H.C. Wainwright & Co. report.

In a May 8 research note, H.C. Wainwright & Co. analyst Ram Selvaraju wrote that the efforts being made in general to accelerate development of a coronavirus vaccine “bode well for Inovio Pharmaceuticals Inc. (INO:NASDAQ), which is advancing a DNA vaccine, INO-4800, to address the unmet need posed by the COVID-19 pandemic.”

For instance, Selvaraju pointed out, on May 7, Moderna announced it is finalizing the protocol for a Phase 3 trial of its COVID-19 vaccine, mRNA-1273, for which it hopes to start pivotal testing this summer. This disclosure “follows hot on the heels of U.S. Food and Drug Administration clearance to conduct a 600-subject Phase 2 trial with mRNA-1273,” he added.

As far as the timeline for Inovio’s COVID-19 vaccine, the Pennsylvania-based company plans to produce 1 million doses of INO-4800 by year-end 2020, reported Selvaraju. In terms of progress to date with the vaccine, Inovio finished enrollment for its Phase 1 trial, and participants are receiving their initial doses. Interim immune response and safety results could be released in late June. Also, the biotech is carrying out several challenge studies in animal models.

This summer, Inovio plans to launch a Phase 2/3 trial of INO-4800. If the study succeeds, “COVID-19 spread could persist in the coming quarters, and INO-4800 could be used for vaccination across the globe,” Selvaraju commented.

The analyst concluded that “Inovio and Moderna may effectively wind up running neck and neck; we also feel that Inovio’s DNA vaccine platform could be considered to have certain advantages from an ease of manufacturing and storage standpoint versus a messenger RNA vaccine.”

H.C. Wainwright & Co. has a Buy rating and a $17 per share price target on Inovio, the stock of which is currently trading at about $12.19 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosures from H.C. Wainwright & Co., Inovio Pharmaceuticals Inc., Company Update, May 8, 2020

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Raghuram Selvaraju, Ph.D. and Yi Chen, Ph.D., CFA, certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of Inovio Pharmaceuticals, Inc. (including, without limitation, any option, right, warrant, future, long or short position).

As of April 30, 2020 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of Inovio Pharmaceuticals, Inc.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The firm or its affiliates received compensation from Inovio Pharmaceuticals, Inc. for non-investment banking services in the previous 12 months.

The Firm or its affiliates did not receive compensation from Inovio Pharmaceuticals, Inc. for investment banking services within twelve months before, but will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

The Firm does not make a market in Inovio Pharmaceuticals, Inc. as of the date of this research report.

Egypt’s central bank left its key interest rates unchanged for the second time and reiterated its view that keeping rates steady is consistent with achieving its inflation target of 9 percent, plus/minus 3 percentage points in the fourth quarter of this year. The Central Bank of Egypt (CBE) left its overnight deposit rate at 9.25 percent, the overnight lending rates at 10.25 percent, and the rate on its main operation and discount rate at 9.75 percent. CBE’s monetary policy committee added its decision to maintain rates reflected the 300 basis point rate cut at an unscheduled policy meeting on March 16. At its previous monetary policy meeting on April 2 CBE also maintained rates, saying this was consistent with achieving its inflation target. Since February 2018, when CBE began easing its policy as inflationary pressures began to subside, key interest rates have been cut by 9.50 percentage points. Egypt’s inflation rate rose to 5.9 percent from 5.1 percent in March, with CBE saying this was due to unfavorable base effect from muted prices increases last year and higher prices in April 2020 due to the outbreak of COVID-19 and Ramadan. The pickup in inflation led analysts to expect CBE to keep rates steady today. Egypt’s tourism sector has been hit hard by the spread of the coronavirus and CBE said leading indicators reflected a slowdown in March and April following a broad improvement in January and February. “Nevertheless, the diversity of the economy provides some cushion given the resilience of some sectors,” CBE said. On Monday the International Monetary Fund’s (IMF) executive board approved assistance of US$2.77 billion so Egypt can meet its urgent balance of payment needs from the pandemic. “The pandemic and global shock pose an immediate and severe economic disruption that could negatively impact Egypt’s hard-won macroeconomic stability if not addressed,” IMF said.

The Central Bank of Egypt issued the following press release:

“The Monetary Policy Committee (MPC) decided to keep the Central Bank of Egypt’s (CBE) overnight deposit rate, overnight lending rate, and the rate of the main operation unchanged at 9.25 percent, 10.25 percent, and 9.75 percent, respectively. The discount rate was also kept unchanged at 9.75 percent. Annual headline urban inflation increased to 5.9 percent in April 2020 from 5.1 percent in March 2020 due to a combination of unfavorable base effect stemming from muted price increases in April 2019 as well as higher prices increases in April 2020 which is broadly attributed to the impact of the outbreak of COVID-19 as well as a stronger seasonal factor due to Ramadan. Annual headline inflation in April 2020 was driven by higher annual food contribution, mainly core food items, which more than offset lower annual contribution of non-food items. Accordingly, annual core inflation increased to 2.5 percent in April 2020 from 1.9 percent in March 2020. Real GDP growth continued to stabilize around 5.6 percent in 2019 Q4, with the recovery in public domestic demand offsetting the moderation in private domestic demand, and the pickup in consumption offsetting the slowdown in investments. Meanwhile, leading indicators showed broad improvement on average in January and February 2020, before reflecting a slowdown in economic activity in March and April 2020. Nevertheless, the diversity of the economy provides some cushion given the resilience of some sectors. Globally, economic activity and employment have deteriorated significantly, which weighed on the outlook with risks mainly tilted to the downside. This was also reflected in the weakness of international oil prices, despite production cuts by major producers. Against this background, and following the reduction of 300 basis points during the unscheduled MPC meeting on March 16, 2020, the MPC decided that keeping key policy rates unchanged remains consistent with achieving the inflation target of 9 percent (±3 percentage points) in 2020 Q4 and price stability over the medium term. The MPC closely monitors all economic developments and will not hesitate to utilize all available tools to support the recovery of economic activity, within its price stability mandate.” www.CentralBankNews.info

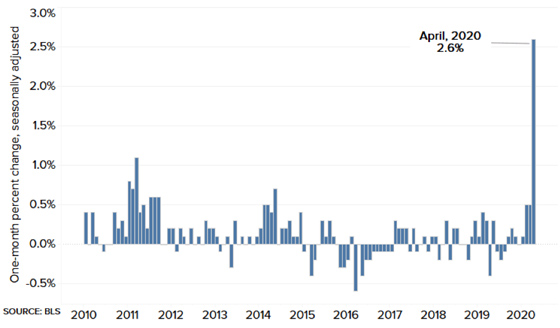

Foodflation is registering at the checkout lines of your local grocery store – and in a bigger way than has been seen in decades.

On Tuesday, the U.S. Labor Department reported that grocery prices paid by consumers surged 2.6% in April. That’s the largest one-month price spike recorded in 46 years.

Food Costs Jump

BLS/CNBC

The last time a food shock of this magnitude hit consumers was February 1974. Back then, inflation was just starting to heat up following President Richard Nixon’s de-linking of the U.S. dollar to gold – and ahead of a massive run up in precious metals prices that culminated in January 1980.

Could we be headed for a similar outcome in the 2020s? Many economists think it’s likely we are.

“A return to 1970s stagflation is only a broken supply chain away,” writes Stephen Roach in the Financial Times. “Soaring deficits and debt could compound the problem. For now, no one is worried about them because of a conviction that interest rates will stay at zero forever. But with fractured supplies set to push inflation higher, that assumption will be tested.”

Of course, the current forces driving foodflation at the grocery store are far different in nature from what hit the economy in the 1970s. An Arab oil embargo and wage-price spiral had ensued as interest rates rose relentlessly.

Today, the economy faces an oil glut, a record surge in unemployment, and interest rates near zero with no signs of heading higher anytime soon.

However, things could change quickly in an environment of unlimited Quantitative Easing.

The trillions of “stimulus” dollars injected into the financial system and consumers’ pockets by the U.S. Treasury and Federal Reserve have so far not ignited a broad inflationary trend in consumer prices.

In fact, energy, commercial real estate, and other sectors of the economy have suffered price collapses. April saw the steepest monthly fall (0.8%) in U.S. consumer prices since the 2008 financial crisis.

It’s hard for prices of discretionary goods to rise while consumers remain hunkered down. But they still need to buy groceries! And that’s where inflation is now showing up.

Food supply chains are being disrupted by pandemic fears and government “stay at home” decrees that have forced restaurants to close and driven farmers to take desperate measures just to survive.

Meanwhile, some large meat-packing facilities have been hit with virus outbreaks spread by their largely foreign-born workforces – threatening meat supplies to grocers.

The most dramatic price rises are being seen in beef, pork, poultry, fish, and eggs.

Kroger and other supermarket chains are putting quantity limits meat purchases – just as they previously had done for bottled water, toilet paper, and bleach over concerns that supply chains would not be able to keep up with growing demand for these household staples.

The availability of gold and silver coins depends on a smoothly functioning chain of suppliers – from mines, to refiners, to mints, to dealers. Unfortunately, the virus has caused many mines to shutter and some refiners and mints (including the U.S. Mint) to close temporarily.

Many bullion dealers are also struggling despite surging demand for their products. Poorly prepared dealers are having difficulty acquiring inventory and managing exposure to market volatility, costing them tons of customers to better positioned dealers like Money Metals Exchange.

Bullion customers, in turn, are facing elevated premiums for most bullion products. In the long run, though, these premiums may be a small price to pay for the security of being able to own physical precious metals.

There may come a day when surging demand so completely overwhelms the supply chain that physical precious metals become practically impossible to obtain.

Today’s spot prices for gold and silver may spike to previously unattained levels overnight… or over the course of months and years as currency debasement drives precious metals gains in fiat dollar terms.

If the 1970s are a guide, then investors can expect few investments other than precious metals to perform well. In a stagflationary environment, the stock market would be expected to trend down in real terms (though natural resource sectors may perform relatively well). Bonds would lose value in real terms as ultra-low yields fail to compensate for even slight upticks in inflation.

But first, the deflationary depression scenario must be ruled out. That will likely happen as the economy reopens state by state, country by country, unleashing pent-up demand and increasing money velocity.

Presently, both deflationary forces and inflationary forces are hitting the economy at the same time.

That has created an extreme distribution of winners and losers based on who happened to be positioned where when the economic lockdowns hit. Some have lost everything, while others (including mega billionaires like Amazon founder Jeff Bezos) have seen their wealth grow at an accelerated pace.

Those who have had ample cash reserves have at least been able to weather this recent storm. When the winds shift toward higher rates of inflation, however, cash will be trash, and hard money – gold and silver – will once again be king.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

By Jameel Ahmad, Global Head of Currency Strategy and Market Research at FXTM

World markets are providing the feel that they are trying not to give a slip on a banana skin moment as the warning signs to investors come in thick and thin that the recoveries in world markets since the February lows are challenging to justify.

It has frequently been highlighted that the recovery in risk has been largely assisted by central bank easing policies and easier accessibility to money through government initiatives and the warning from Federal Reserve Chair Jerome Powell just yesterday that the current pandemic raises concerns about long-term economic damage with significant downside risks to the outlook has further highlighted anxiety.

Now, if another period of risk aversion does hit us (if) then the likelihood is that safe havens will be in demand once again. This potentially sounds promising for those who hold USD, JPY or Gold in their portfolio. Of course and as it is often remembered, in USDJPY a period of market uncertainty generally indicates a weaker USDJPY.

For what it is worth, I hold some doubt over how long this risk aversion will last as the market remains erratic overall but in the event that USDJPY does point further lower, 106.50 and 105.90 could become points of interest.

(USDJPY Daily FXTM MT4)

The Nasdaq presents a more interesting picture on the Daily timeframe of an asset that is perhaps starting a trend lower, however it is also important to note that this index consists of many major corporations from the technology sector that have shown in recent times that they can perform strongly in times of a crisis. Such as Netflix and Amazon.

However, if the Nasdaq does continue to point lower then the Daily low last seen on May 5, May 4 and April 22 could be looked at as potential areas of support.

(Nasdaq Daily FXTM MT4)

The Daily chart on the S&P 500 highlights that 2710 and 2630 are potential support levels that the index could look for should the S&P hypothetically turn further lower.

(S&P 500 Daily FXTM MT4)

For the Wall Street 30 Mini on the H4 charts a decline below 2283 could indicate further potential price weakness towards 2260 or 2245.

(Wall Street 30 Mini Daily FXTM MT4)

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Steeper than forecast decline in German wholesale prices bearish for EURUSD

Wholesale prices in Germany fell in April more than expected: the Wholesale Price Index fell 1.4% in April after 0.4% decline in March, when 0.3% decline was expected. This is bearish for EURUSD.

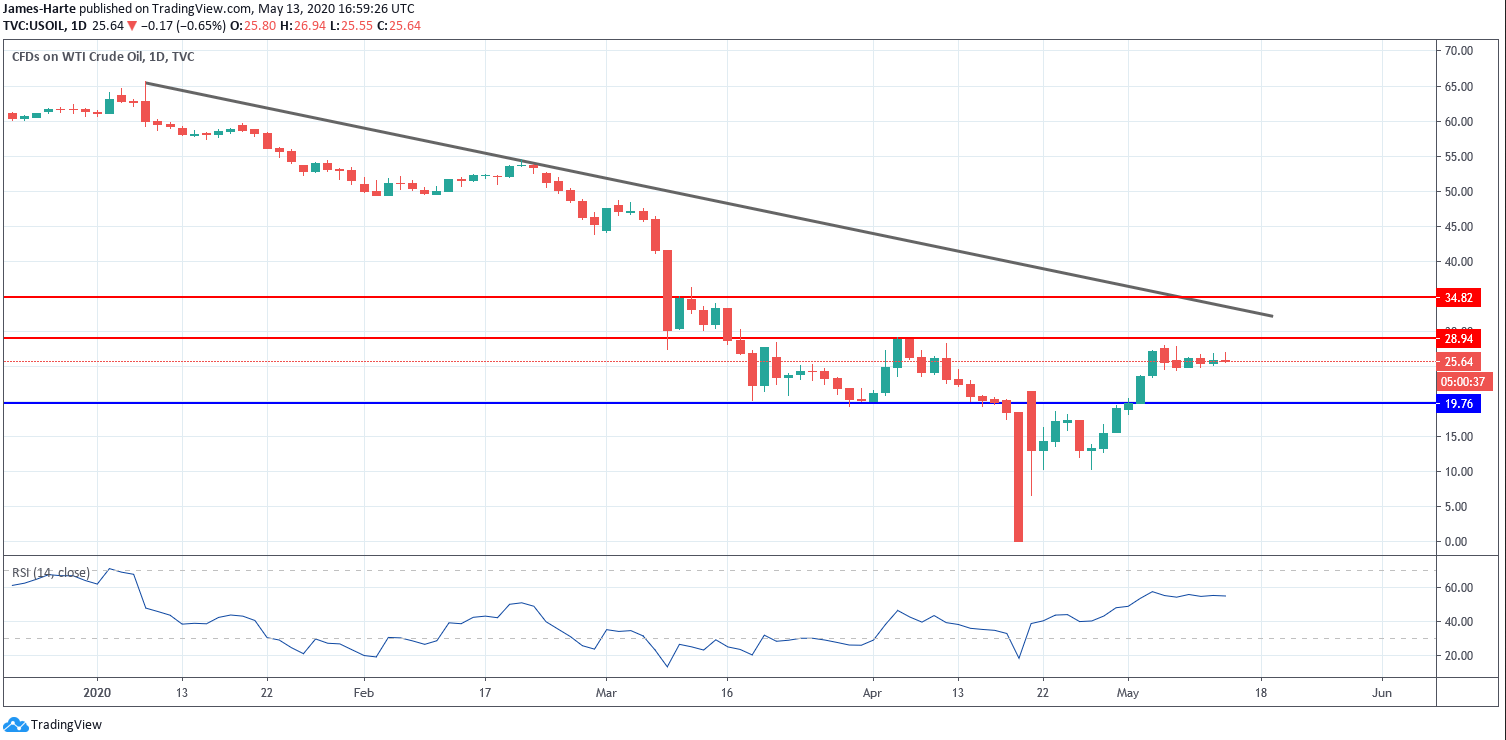

In its latest update, the Energy Information Administration reported an unexpected drop in US crude inventories. For the week ending May 8th, the EIA reported that US crude stores dropped by 745k barrels.

This was in stark contrast to the 4.1 million barrel increase the market was looking for and comes on the back of 15 straight weekly increases. This is now the first drop in inventory levels since the COVID-19 crisis began back in January.

Regionally, inventory levels at the Cushing delivery hub in Oklahoma, which is the largest in the US, fell by 3 million barrels. Despite the drop, the hub is still over 80% in terms of storage capacity.

Fuel demand, measured via the total-products supplied figure, was up last week. Despite that, the reading is still around 23% lower than the two-year average for the last four-week period.

US Crude Production Falls Further

Encouragingly for bulls, the report noted that US crude production dropped by a further 300k barrels over the week to 11.6 million barrels per day. This means that US crude production is now down at its lowest level since December 2018. This has, therefore, reversed the rampant increases we’ve seen over the last 18 months.

Refinery crude runs were higher by 593k barrels per day over the week amidst refinery utilization rates dropping by 2.6% to 77.9% of capacity. At this level, capacity is not far off all-time lows.

Gasoline Stocks Fall Again

Gasoline stocks fell last week as well. This marks the third straight week of declines as motor demand continues to rebound amidst the easing of lock-downs in the US.

Gasoline stores were lower by 3.5 million barrels over the week to 252.9 million barrels in total, marking a sharper drop than the 2.2 million barrel decline forecast.

Distillate stockpiles, however, including diesel and heating oil, were still up on the week. There rose by 3.5 million barrels to 155 million barrels. This was well above the 2.9 million barrel increase forecasted.

Risk Sentiment Flattened As Fed Disappoints

Despite the report, crude prices remain stubbornly flat this week amidst a weakening in risk sentiment. Risk assets have been lower as concerns over the health of US/China relations continue to build.

Comments by Fed chairman Powell also weighed on risk appetite this week as Powell shot down any talk of negative rates in the US. This came despite warnings over the “lasting harm” to the economy as a result of COVID-19.

Crude Holding Below Key Resistance

The breakout above the 19.76 level has stalled ahead of the 28.94 resistance. However, while price holds above the 19.76 level, focus remains on further upside and an eventual break higher. To the topside, the key level to watch will be the 34.82 structural resistance with the bearish trend line coming in just below. If price can breakout above here this will likely set up a much broader recovery.