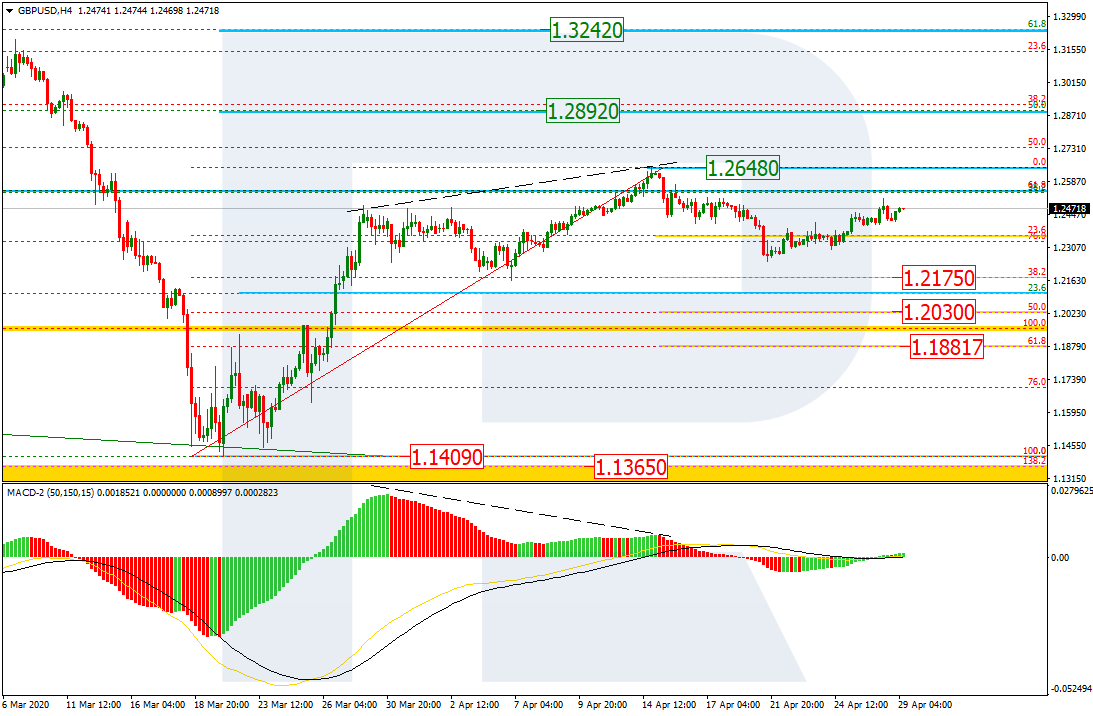

As we can see in the H4 chart, the divergence made the pair start a new bearish phase, which has already reached 23.6% fibo. At the moment, GBPUSD is forming a new ascending structure, which may be considered as an internal correction and later be followed by another descending wave towards 38.2%, 50.0%, and 61.8% fibo at 1.2175, 1.2030, and 1.1881 respectively. However, if the price manages to form a strong rising impulse and break the high at 1.2648, the instrument may start a steady growth to reach 50.0% and 61.8% fibo at 1.2892 and 1.3242 respectively.

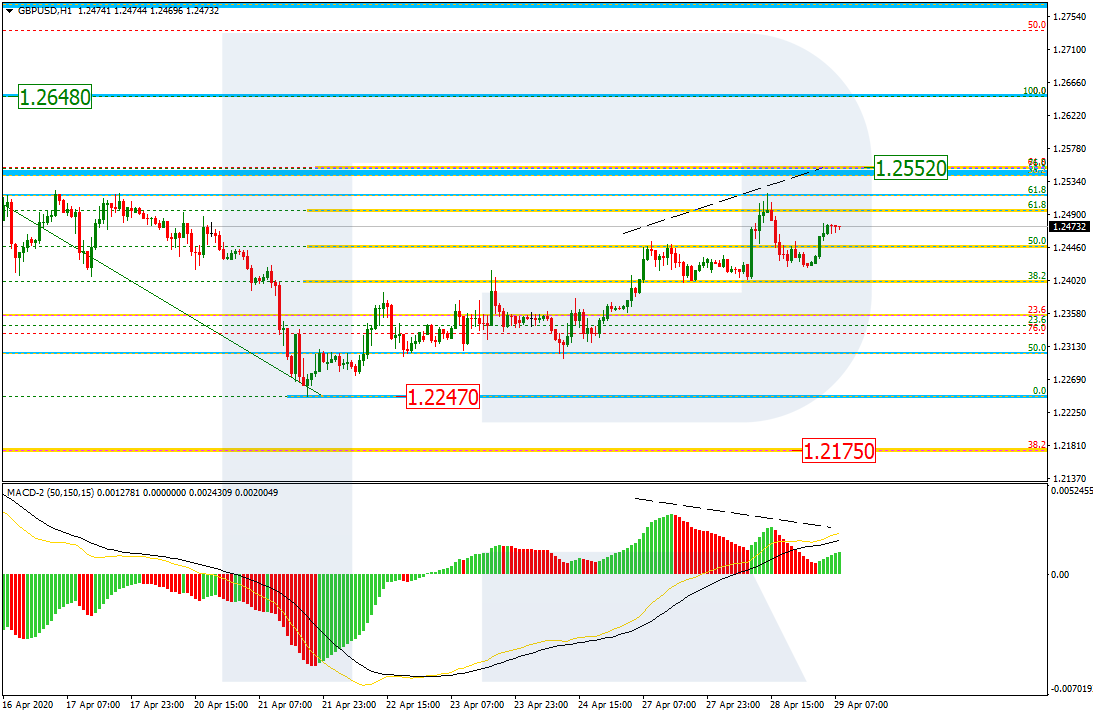

The H1 chart shows a more detailed structure of the current ascending correction. The pair has already reached 61.8% fibo and may continue growing towards 76.0% fibo at 1.2552. At the same time, there is a divergence on MACD, which indicates that the market is already preparing for a new decline with the target at 1.2247.

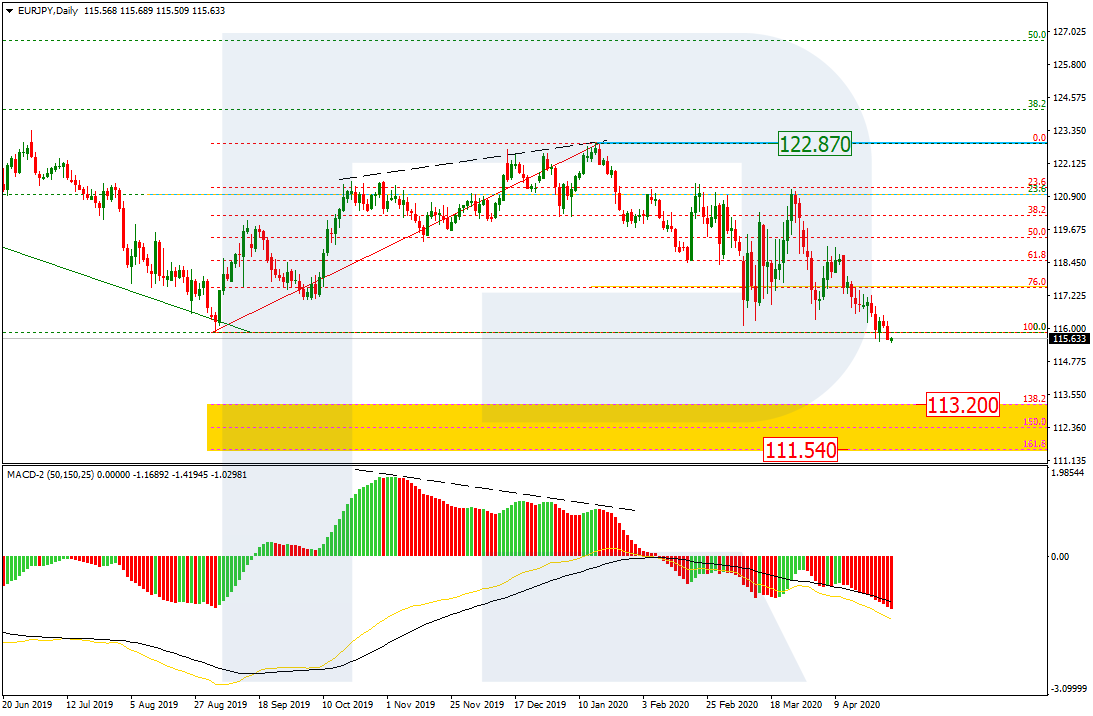

EURJPY, “Euro vs. Japanese Yen”

As we can see in the daily chart, EURJPY has broken the previous low and may continue falling towards the post-correctional extension area between 138.2% and 161.8% fibo at 113.20 and 111.54 respectively.

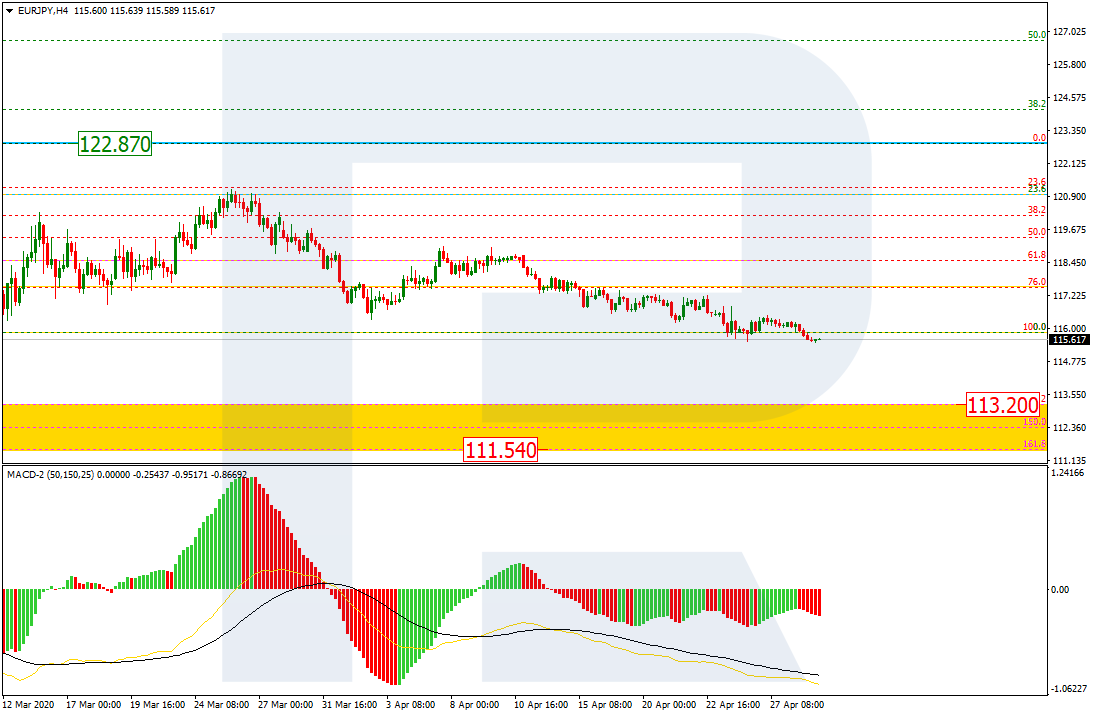

In the H4 chart, the current descending tendency is rather slow. At the same time, there might be a convergence on MACD to indicate a short-term pullback quite soon.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

In the context of globalization and the general computerization of world stock markets, a relatively new trading segment based on using special means of automation of financial operations is gaining a foothold. Trade automation allows good use of market trends activity and strengthening the mutual influence of world markets. With undeniable advantages over the traditional method of stock transactions, algorithmic trade allows neutralizing many of the shortcomings inherent in exchange trading.

At the same time, disputes about the nature of the influence of algorithmic trading on markets and the consequences of further growth of this segment do not cease. In response to the wide

distribution of algorithmic trading periodically, one can hear calls for active measures to curb its spread. And one of the main problems is the reaction to market slumps which will be discussed in this article.

Market reactions

There have been multiple mentions from AI trading corporations or small companies that there was very little reaction from their software in regards to the market slump. This has mostly to do with the design of these platforms. According to the representatives of the crypto sphere’s successful AI trading company Bitcoin Billionaire app, the software is always designed with small market changes in mind.

It is very actively being used in stock and FX trades and is usually referred to as HFT (High-Frequency Trading). The large market slump that has occurred over the COVID pandemic did not really affect the way the AI works. Sure, it did not take advantage of the large slump and started shorting on FX, but it is now starting to regain its effectiveness through these small, yet profitable corrections that every financial market is going through these days.

Algorithm trade is one of the most perspective financial innovations

With the development of computer technology and the advent of Internet trading in the stock market, a separate direction of commissioning began to develop. Operations based on the use of algorithmic trading systems. With this type of trading, transaction algorithms are embedded in a special computer program, which, based on processing market data, makes decisions and makes stock transactions.

When using algorithmic systems, the trader does not directly participate in the process of trading stock assets, only monitoring the overall adequacy of the trading system to the market situation. Behind Algorithmic systems are also called trading robots with a high degree of autonomy and automation of nested procedures.

Full automation of the trading process has significant advantages. The first of these is the exclusion of the subjective factor from the trading process. This is achieved through continuous adherence to embedded algorithms and allows you to completely eliminate erroneous operations performed under the influence momentary emotions of a trader, motives of fear, excessive joy from previous successful transactions when the trader is losing vigilance as well as all kinds of “Mechanical” mistakes made by traders in inattention.

A trading robot can’t get tired, sick, not affected by the weather, able to work continuously and around the clock for a long time, which is especially important in an era of strong interconnections of world stock markets.

Other advantages of algorithmic trading are formed by the high speed of decision-making and transactions, which allows you to stay ahead of more slow bidders – traders. Robots are able to analyze a large number of diverse information, while simultaneously tracking hundreds of stock quotes and related indicators, using sophisticated calculations to processing.

Another advantage of algorithmic trade is the ability to carry out operations for several exchange strategies at the same time, which is especially important when managing a portfolio that includes a variety of financial instruments.

Market slumps

Obviously, the capabilities of a trading robot are, in many ways, superior to the capabilities of a trader. As a result, – robots are able to demonstrate significantly better indicators of trade profitability. But it should be noted that the recent events surrounding the coronavirus have been very tough for algorithmic traders.

First of all, COVID-19 has hit every possible field of business in the world. Cryptocurrencies have suffered, and the price of the stocks fell significantly. AI trading robot is created to determine any change in the market and look for the best possible way, but in the current situation, robots become confused as well and started panic buying of decreased stocks. The fact shows that while algorithmic trading is indeed a good thing, it does not have emotions, which sometimes is vital in trading. AI trading may make the market crash even worse.

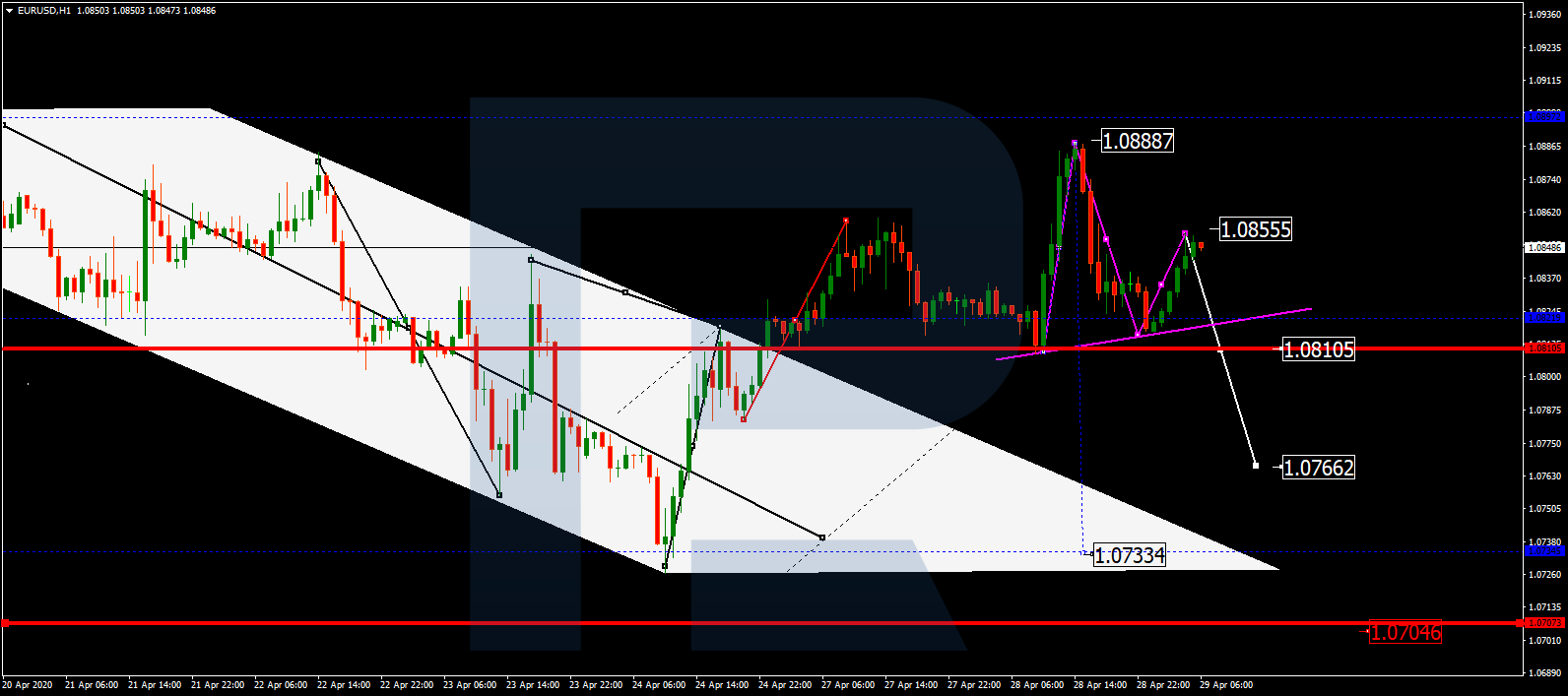

After completing another ascending structure from 1.0810 towards 1.0888, EURUSD may try to update 1.0915. According to the main scenario, the price is expected to return to 1.0810 and break it to the downside. After that, the instrument may continue trading inside the downtrend with the short-term target at 1.0766.

GBPUSD, “Great Britain Pound vs US Dollar”

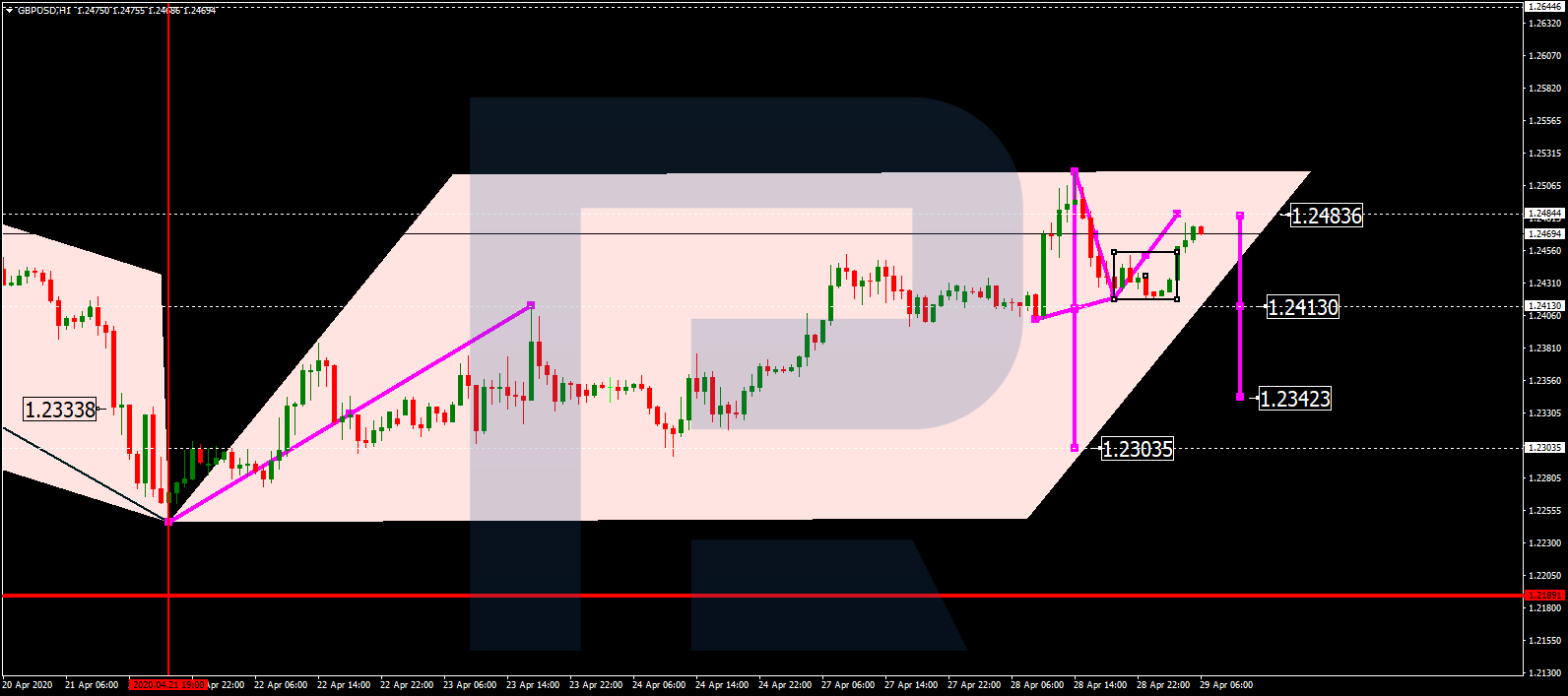

After finishing the first descending impulse at 1.2420, GBPUSD is correcting towards 1.2483. Later, the market may start a new decline to break 1.2410 and then continue falling with the short-term target at 1.2343.

USDRUB, “US Dollar vs Russian Ruble”

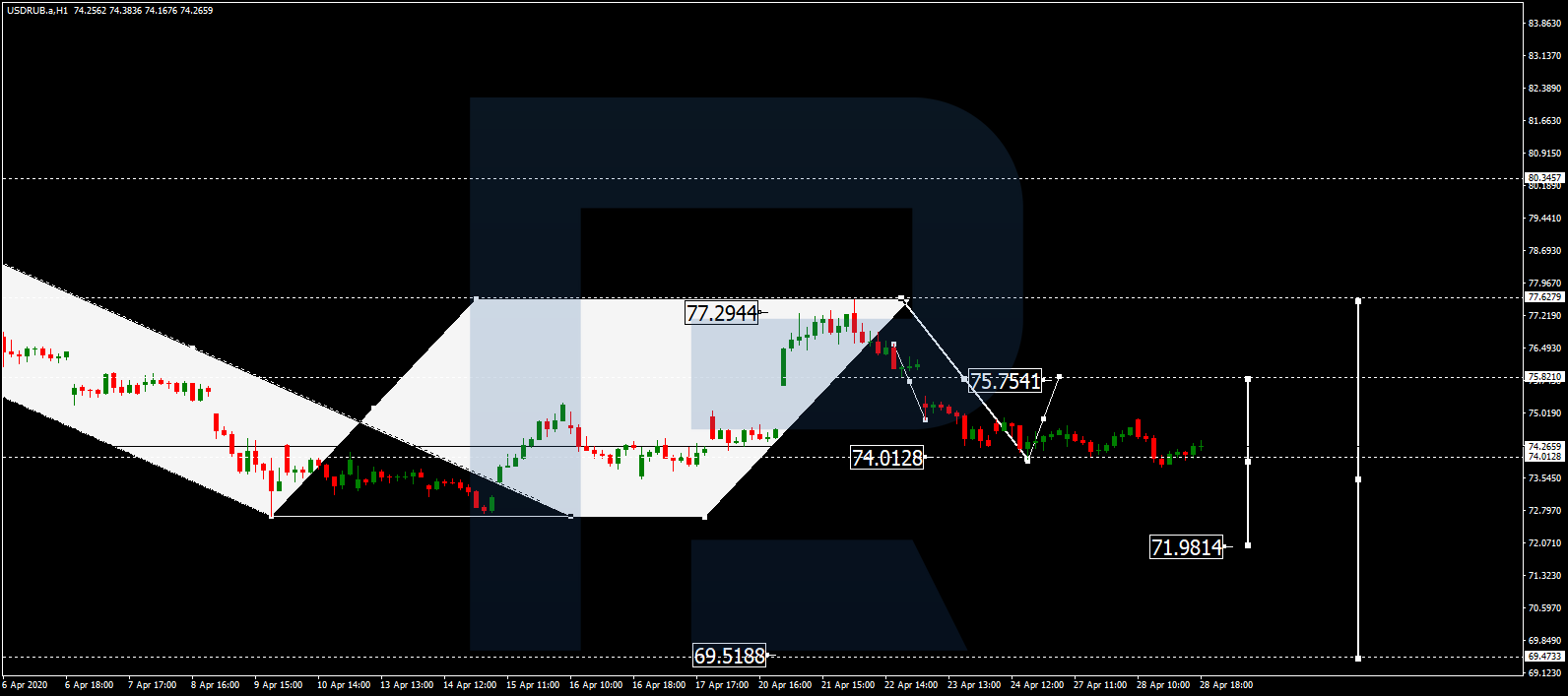

USDRUB is consolidating above 74.00 without any particular direction. If later the price breaks this range to the upside at 74.80, the market may start another correction to reach 75.75; if to the downside at 74.00 – resume trading downwards with the short-term target at 71.30.

USDJPY, “US Dollar vs Japanese Yen”

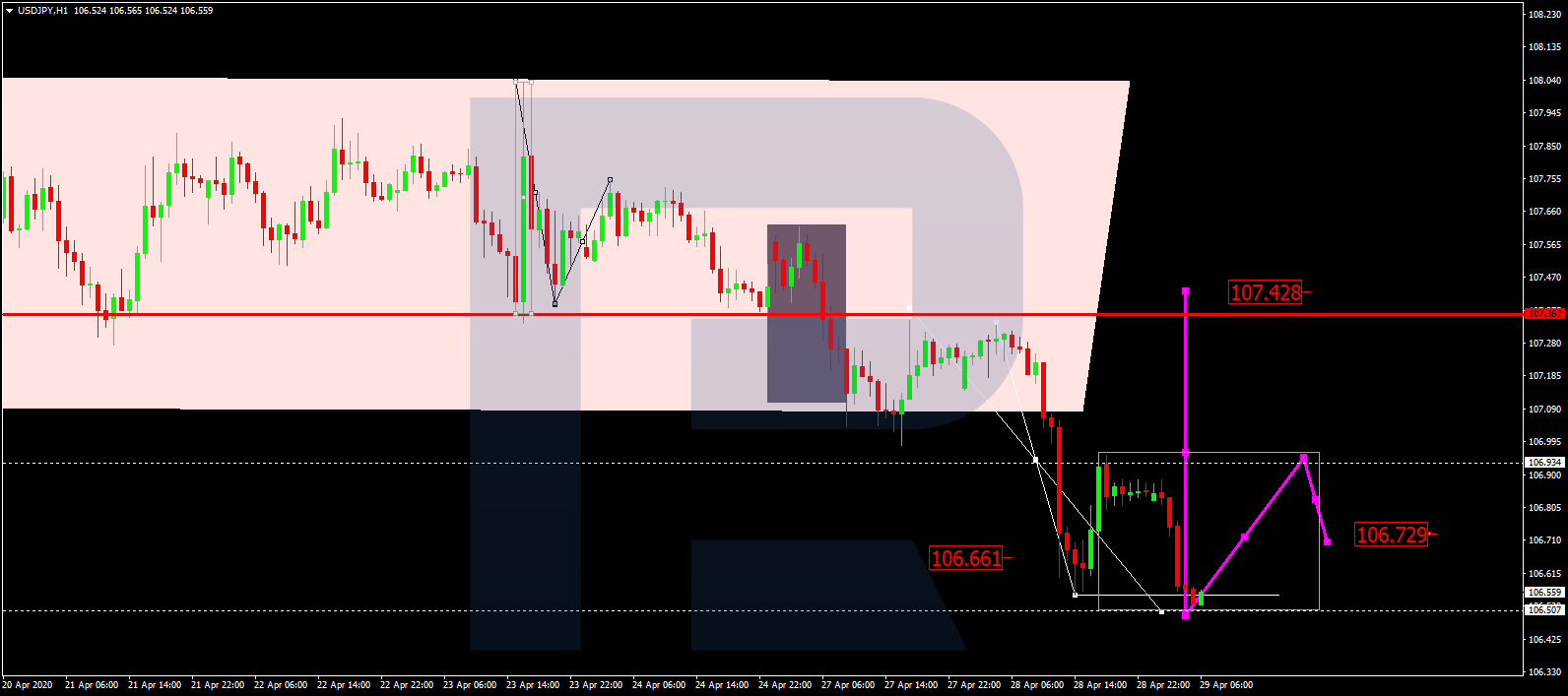

After completing the descending structure at 106.66, USDJPY is consolidating around this level. Today, the pair may expand the range down to 106.00 and then grow towards 106.90. If later the price breaks this range to the upside, the market may form one more ascending structure to reach 107.42; if to the downside – extend the descending wave towards 105.50.

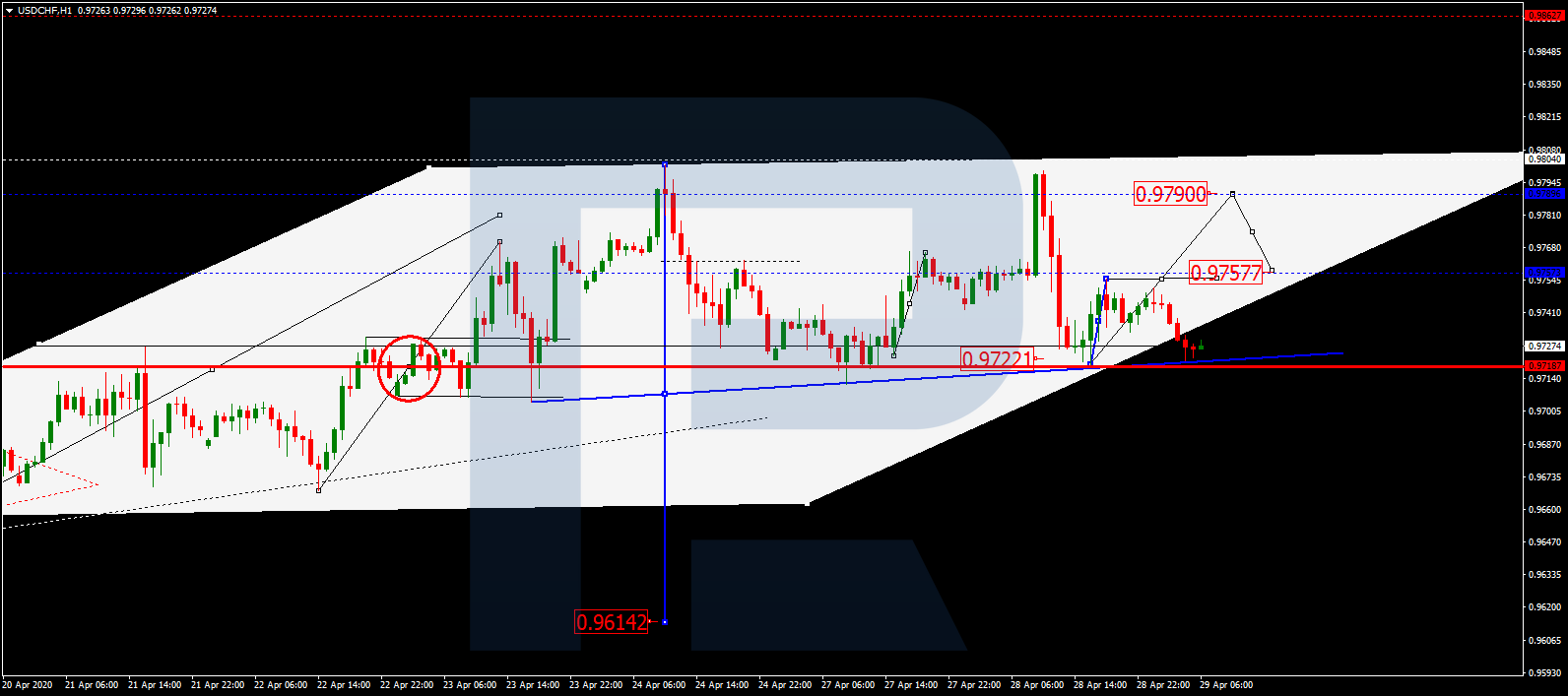

USDCHF, “US Dollar vs Swiss Franc”

USDCHF is consolidating above 0.9722. The main scenario implies that the price may form one more ascending wave to break 0.9757 and then continue trading upwards with the short-term target at 0.9790. However, if the pair breaks 0.9700 to the downside, the instrument may continue the correction to reach 0.9670.

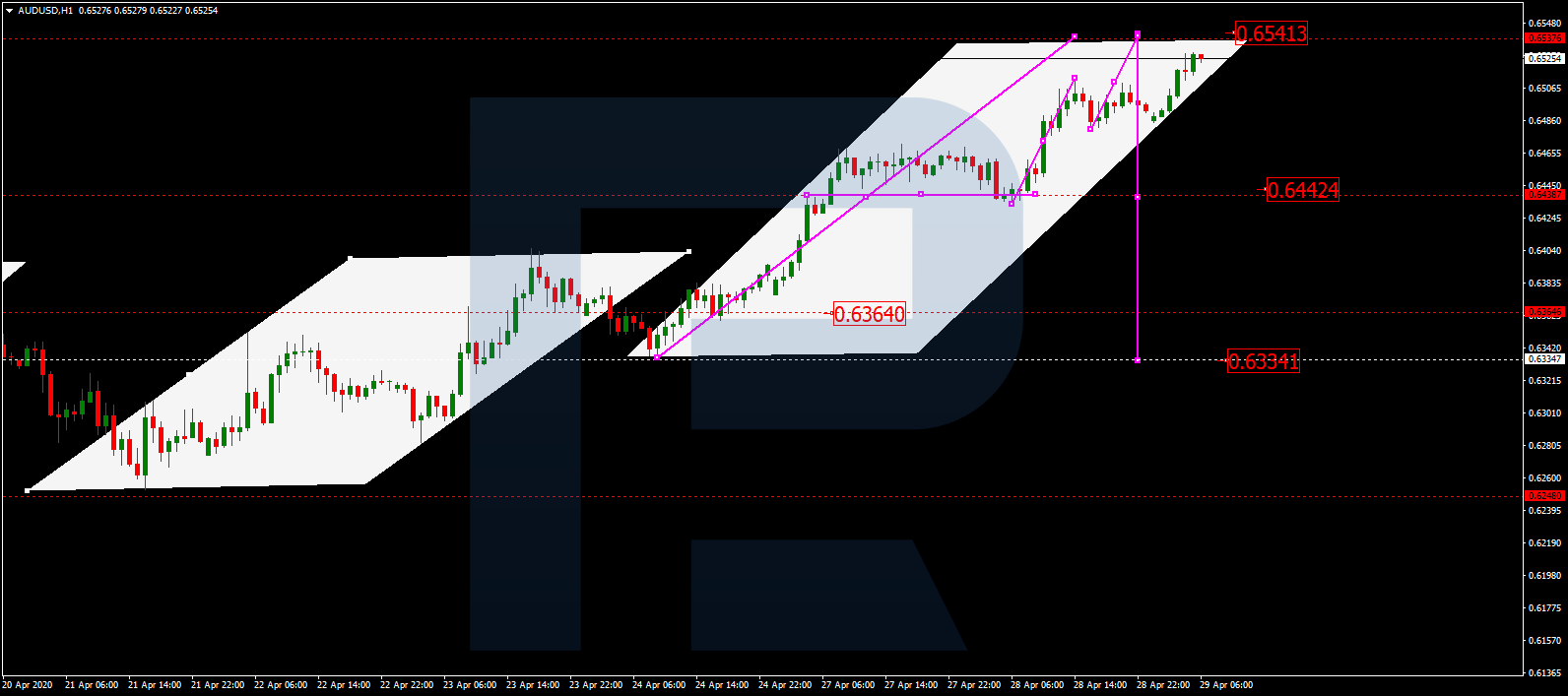

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD continue moving upwards. Possibly, the pair may reach 0.6542 and then start a new decline to break 0.6440. After that, the instrument may continue trading downwards with the target at 0.6330.

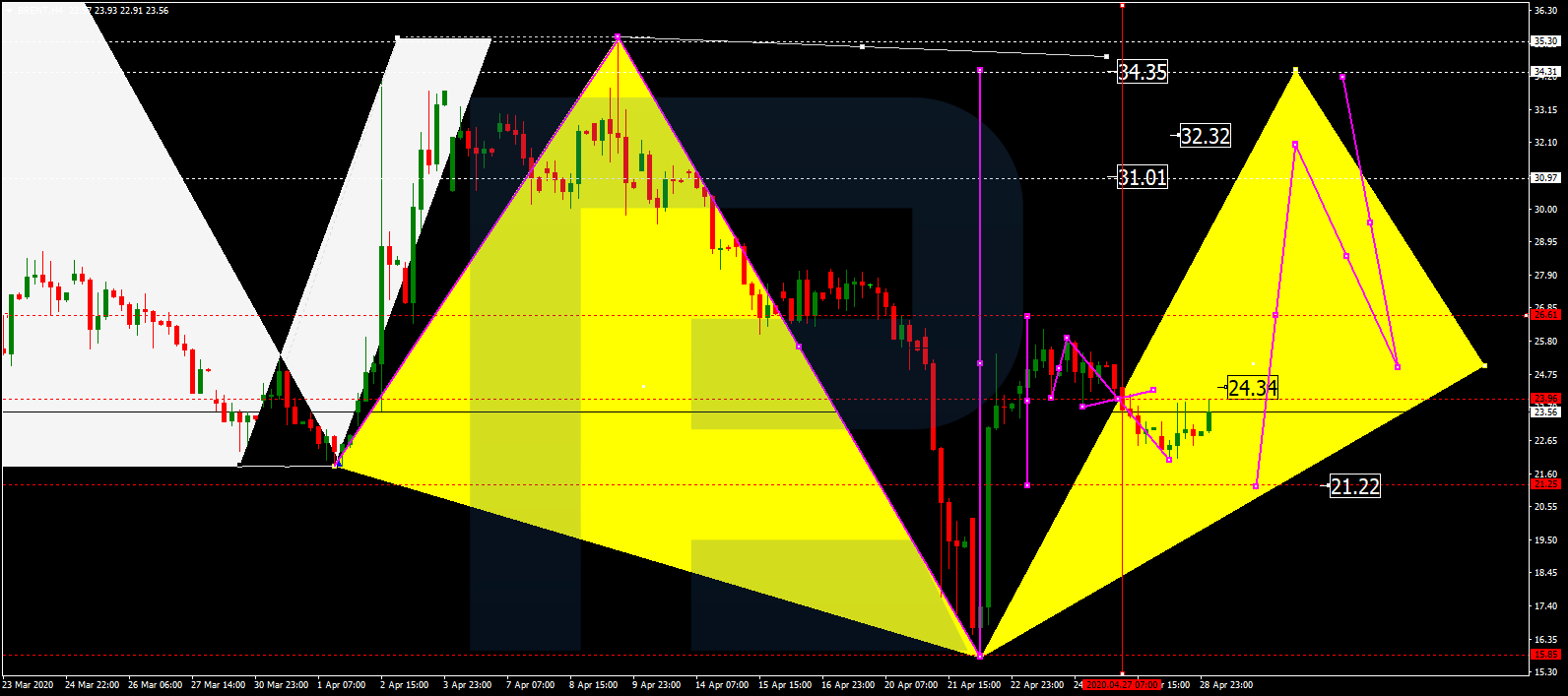

BRENT

Brent is consolidating around 24.34. Possibly, today the pair may fall to reach 21.21 and then form one more ascending structure to break 27.00. Later, the market may continue trading upwards with the target at 32.32.

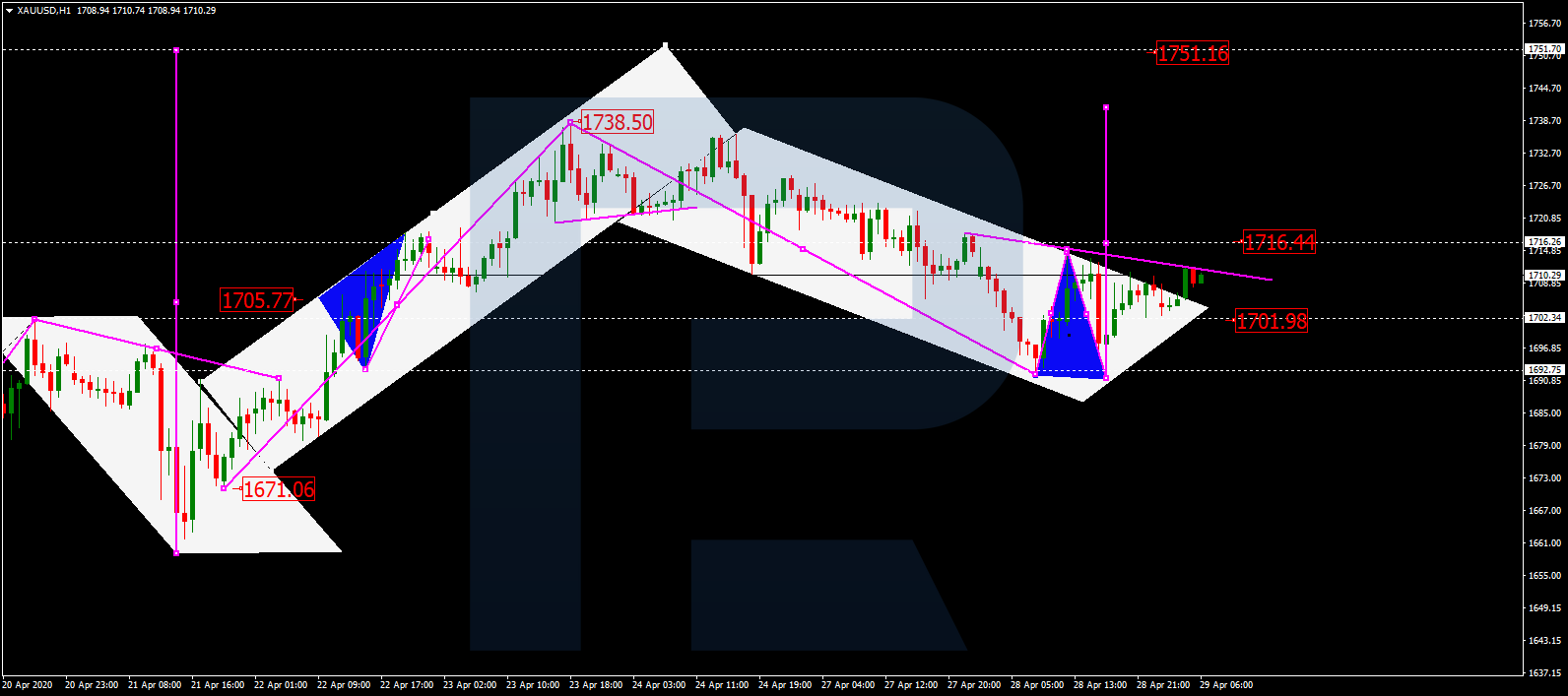

XAUUSD, “Gold vs US Dollar”

After completing the descending structure at 1691.60, Gold is growing to reach 1716.44. After that, the instrument may correct towards 1702.50 and then form one more ascending structure to break 1717.00. Later, the market may continue trading inside the uptrend with the target at 1751.50.

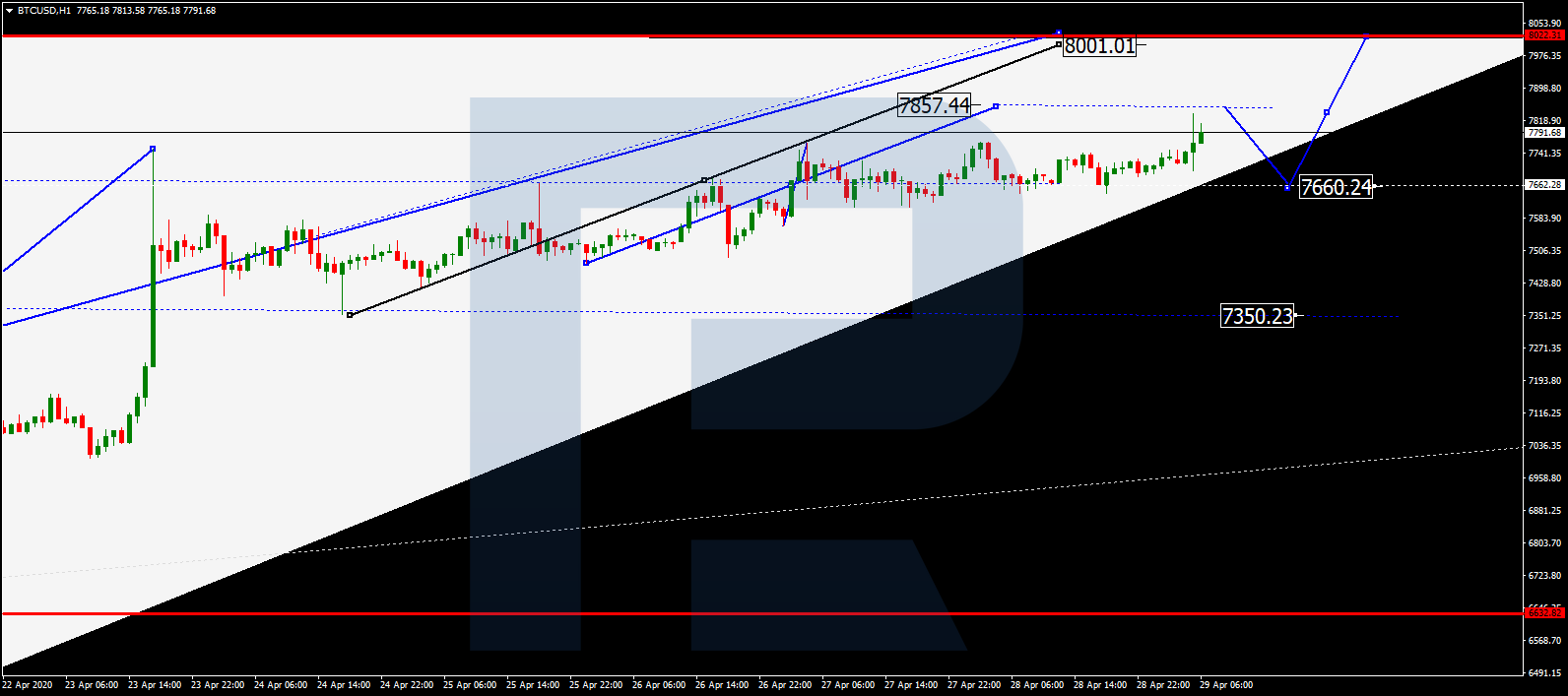

BTCUSD, “Bitcoin vs US Dollar”

BTCUSD continues growing towards 7860.00. Later, the market may start a new correction to return to 7660.00 and then form one more ascending structure with the first target at 8000.00

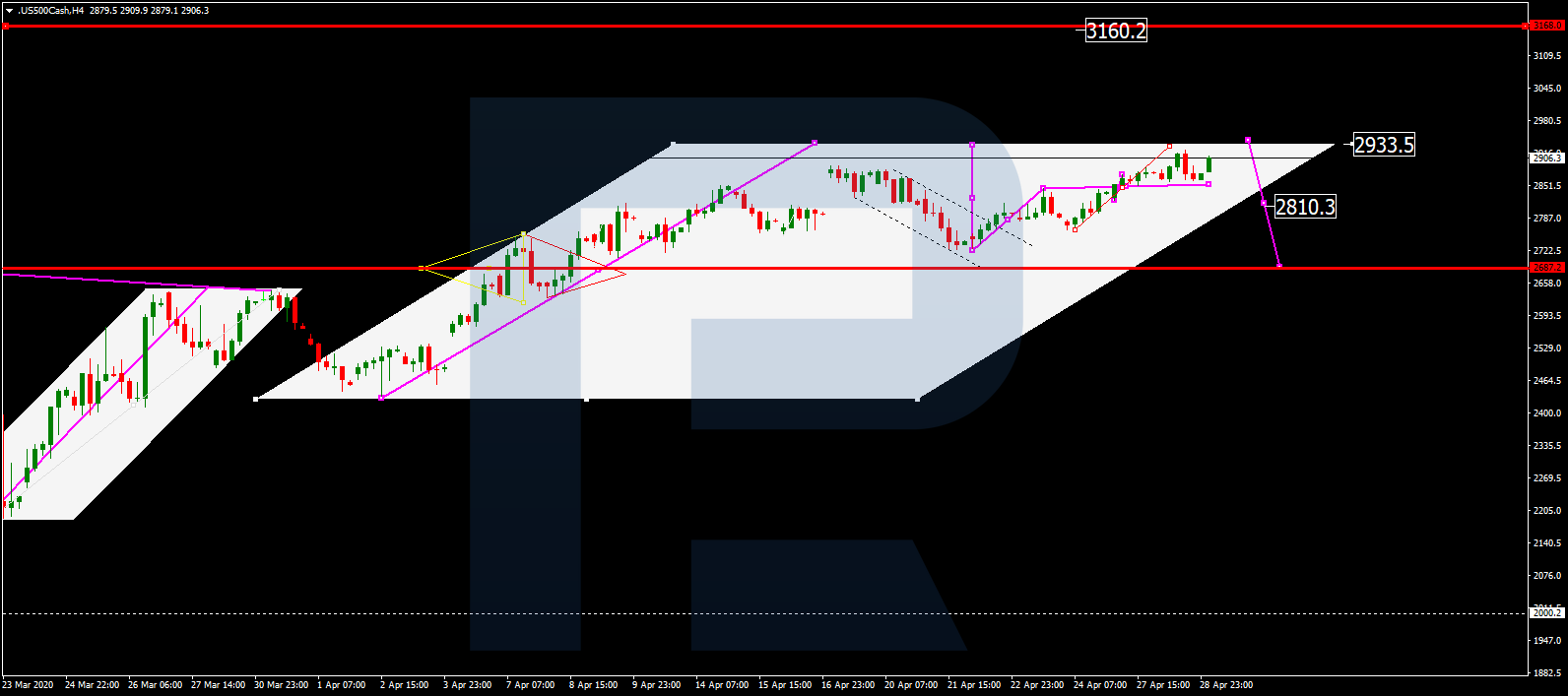

S&P 500

S&P 500 is moving upwards. Possibly, today the pair may reach 2933.3 and then start another correction towards 2700.0. After that, the instrument may form one more ascending structure with the target at 3160.2.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Since the beginning of this week, trades on the EUR/USD currency pair are active enough. At the same time, there is no defined trend. At the moment, EUR/USD quotes are testing the supply zone of 1.0870-1.0890. The nearest support is 1.0835. Investors have taken a wait-and-see attitude before the Fed meeting. It is expected that the regulator will leave the key marks of monetary policy unchanged. We recommend paying attention to the comments by representatives of the Central Bank. Financial market participants will also assess the US GDP report for the first quarter. Positions should be opened from key levels.

The Economic News Feed for 29.04.2020

– US GDP data at 15:30 (GMT+3:00);

– Pending home sales in the US at 17:00 (GMT+3:00);

– Fed interest rate decision at 21:00 (GMT+3:00).

Indicators do not give accurate signals: 50 MA has crossed 100 MA.

The MACD histogram has started rising, indicating the bullish sentiment.

Stochastic Oscillator is in the overbought zone, the %K line has crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.0835, 1.0810, 1.0785

Resistance levels: 1.0870, 1.0890, 1.0930

If the price fixes above 1.0870, the EUR/USD currency pair is expected to grow. The movement is tending to 1.0900-1.0930.

An alternative could be a decrease in the EUR/USD quotes to 1.0800-1.0780.

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.24281

Open: 1.24186

% chg. over the last day: -0.04

Day’s range: 1.24186 – 1.24853

52 wk range: 1.1466 – 1.3516

There is an ambiguous technical pattern on the GBP/USD currency pair. The British pound is in a sideways trend. At the moment, the following local support and resistance levels can be identified: 1.2425 and 1.2485, respectively. Financial market participants have taken a wait-and-see attitude before the Fed meeting, as well as the publication of important economic reports from the US. We recommend opening positions from key support and resistance levels.

The news feed on the UK economy is calm.

Indicators do not give accurate signals: the price has crossed 50 MA.

The MACD histogram is in the positive zone, but has started declining.

Stochastic Oscillator is in the neutral zone, the %K line is below the %D line, which indicates the bearish sentiment.

Trading recommendations

Support levels: 1.2425, 1.2385, 1.2315

Resistance levels: 1.2485, 1.2515, 1.2570

If the price fixes above the resistance level of 1.2485, further growth of GBP/USD quotes is expected. The movement is tending to 1.2540-1.2580.

An alternative could be a decrease in the GBP/USD currency pair to 1.2380-1.2350.

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.40330

Open: 1.39942

% chg. over the last day: -0.26

Day’s range: 1.39308 – 1.40033

52 wk range: 1.2949 – 1.4668

USD/CAD quotes have been declining. The trading instrument has set new local lows. The loonie is currently consolidating in the range of 1.3930-1.3975. The USD/CAD currency pair has the potential for further decline. The Canadian dollar is supported by price recovery in the “black gold” market. We expect the Fed meeting. Positions should be opened from key levels.

The news feed on Canada’s economy is calm.

Indicators signal the power of sellers: the price has fixed below 50 MA and 100 MA.

The MACD histogram is in the negative zone, indicating the bearish sentiment.

Stochastic Oscillator is in the neutral zone, the %K line is above the %D line, which gives a signal to buy USD/CAD.

Trading recommendations

Support levels: 1.3930, 1.3900

Resistance levels: 1.3975, 1.4005, 1.4065

If the price fixes below the support level of 1.3930, a further drop in the USD/CAD quotes is expected. The movement is tending to 1.3900-1.3860.

An alternative could be the growth of the USD/CAD currency pair to 1.4000-1.4040.

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 107.243

Open: 106.855

% chg. over the last day: -0.34

Day’s range: 106.358 – 106.893

52 wk range: 101.19 – 112.41

There are aggressive sales on the USD/JPY currency pair. During yesterday’s and today’s trades, the yen added more than 80 points. The greenback demand has weakened before the Fed meeting. At the moment, USD/JPY quotes are testing the support level of 106.40. The 106.65 mark is the nearest resistance. A trading instrument has the potential for further decline. Positions should be opened from key levels.

Indicators signal the power of sellers: the price has fixed below 50 MA and 100 MA.

The MACD histogram is in the negative zone and below the signal line, which gives a strong signal to sell USD/JPY.

Stochastic Oscillator is in the neutral zone, the %K line is above the %D line, which indicates the bullish sentiment.

Trading recommendations

Support levels: 106.40, 106.00

Resistance levels: 106.65, 107.00, 107.35

If the price fixes below 106.40, a further drop in the USD/JPY quotes is expected. The movement is tending to the round level of 106.00.

An alternative could be the growth of the USD/JPY currency pair to 106.80-107.00.

When looking at Gold, the overall picture hasn’t changed. The precious metal continues to trade around 1,700 USD, even though it has technically picked up with a slight bearish touch from the bearish divergence in the RSI(14) on a daily time-frame (orange).

On Wednesday the main focus will likely be on the US GDP data, and the Fed in the evening.

The GDP Growth Rate is expected to come in at -4%, mainly due to the Corona lockdown. This would indicate the first signs in terms of an economic downturn, and any print which comes in below -4% could potentially result in stronger demand for Gold.

In the evening, the Fed will announce its decision for the benchmark interest rate, and while according to the Fed Watch Tool, no change is expected, but some indications that the Fed may cut into negative territory can be seen.

But even if this won’t happen, market participants will carefully watch other monetary policy moves the Fed may consider as an influence on markets and the world economy.

In general, we sustain our bullish take on Gold, favour Long engagements from a risk-reward perspective, and also from a purely technical perspective, as long as we trade above 1,440/450 USD.

If we get to see a short-term corrective move, a potential first target around 1,650 USD while a first target on the upside can be found around 1,800 USD:

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between January 24, 2019, to April 24, 2020). Accessed: April 24, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of Gold fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, in 2019, it increased by 18.9%, meaning that after five years, it was up by 28%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

On Tuesday the 28th of April, trading on the euro closed down by 9 pips. In the European session, the euro rose to 1.0889. By close, the EURUSD pair had dropped 71 pips to 1.0818.

The dollar has again come under pressure from the majors amid rising stock indices. US stock indices began the day on a positive note before closing with declines ranging from 0.13% to 1.4% as the tech sector posted big losses.

US consumer confidence fell short of expectations. A report released by the Conference Board showed that US consumer confidence in April fell to its lowest level since 2014 (86.9 points), although consumer expectations improved.

21:00 US: Fed interest rate decision and monetary policy statement.

21:30 US: FOMC press conference.

Current situation:

Tuesday’s forecast didn’t come off. Buyers took advantage of the increased demand for risky assets on account of rising stock indices. They also failed to defend 1.0890. In anticipation of upcoming events, the pair returned to the channel, erasing all previous gains.

In the Asian session, the majors are trading up against the US dollar. The growth of stock indices and oil prices had a positive impact on the foreign exchange market. The EURUSD pair is following the growth leaders (NZD, AUD, CAD) upwards.

The price is near the balance line (1.0840) within a range of 1.0810 – 1.0890. At the time of writing, the euro is trading at 1.0848. Too many factors are currently affecting the pair.

On Tuesday, the two-day meeting of the US Federal Reserve Open Market Committee began. After the meeting, Jerome Powell will hold a press conference. On Thursday, a meeting of the Governing Council of the ECB. Additionally, a report on the Eurozone’s GDP will be released.

In such uncertainty, there’s not much point making a forecast given that any news and the reaction to it can change everything. However, we can share some thoughts. For a rally, the bulls first need to break through 1.0900. If futures on US stock indices continue to rise, the bulls may risk testing 1.0900 before the ECB meeting. It would be better to break 1.0900 on Thursday. In this case, the price model will be more successful for a reversal. There’s still a risk of the pair dropping to 1.0790.

Airlines face an unprecedented international crisis in the wake of the coronavirus pandemic. The International Air Transport Association (IATA) estimates that the global industry will lose US$252 billion in 2020. Many airlines are cutting up to 90% of their flight capacity. On March 1, more than two million people in the US were flying per day. A month on, fewer than 100,000 people are going through airport security daily.

Some climate activists have welcomed the emptied skies, pointing to the dramatic fall in carbon emissions. But others worry that the bounce back and attempts to take back some of the losses might mean that an opportunity for fundamental, sustained change may be missed.

In the US, a federal government US$50 billion bailout fund – part of which will fund cash grants going towards airline workers, and the other part loans for the airlines themselves – was rolled out piecemeal in March, with revisions announced on April 14.

More than 200 airlines applied. American Airlines will get US$5.8 billion, Delta US$5.4 billion, and Southwest US$3.2 billion, among others. Donald Trump, the US president, stated that the airline bailout was needed to return the industry to “good shape” and was “not caused by them”. Another US$4 billion is available for cargo airlines and US$3 for contractors.

In the UK, it was initially announced that no industry-wide bailout would be offered. Instead, the industry would have to rely on broader aid packages covering 80% of salaries (below a cap) for furloughed employees. But subsequently, the government quickly gave easyJet a £600 million loan (US$740 million). Flybe, a smaller regional or “secondary” airline with pre-crisis financial issues, was not bailed out and collapsed. Many money-making routes Flybe ran have since been picked up by others.

Continental Europe is in worse shape. Italy has re-nationalised Alitalia, forming a new state-owned entity and investing €600 million (US$650 million). France has indicated it will do whatever it takes to bailout Air France/KLM (France owns 15% and the Dutch 13%), with a possible €6 billion bailout package (US$6.5 billion).

Meanwhile, Australia’s Qantas secured a A$1 billion loan (US$660 million). Debt-laden Virgin Australia, meanwhile, was denied a A$1.4 billion loan (US$880 million) and has subsequently plunged into voluntary administration. Singapore Airlines, however, got a US$13 billion aid package.

The airline industry has faced many crises before – 9/11 and the 2010 Icelandic volcano eruption, for example. But these pale in comparison to the economic hit that airlines are currently facing. Some are asking: can it recover? Is this an economic crisis that could reshape how we travel and live? Or will it turn out to be more of a pause, before returning to business as usual? And what role does the climate crisis play in all this – how will sustainability figure in any rebooting of the industry going forward?

We are all experts in the airline industry. Darren Ellis (Lecturer in Air Transport Management) considers these questions first, looking at the industry’s structure and response. Jorge Guira (Associate Professor in Law and Finance) then explores bailout options and likely future scenarios for the industry. Finally, Roger Tyers (Research Fellow in Environmental Sociology) considers how the industry might just be at a turning point in terms of how it tackles climate change.

This article is part of Conversation Insights

The Insights team generates long-form journalism derived from interdisciplinary research. The team is working with academics from different backgrounds who have been engaged in projects aimed at tackling societal and scientific challenges.

A global problem

Darren Ellis, Lecturer in Air Transport Management

Most of the global airline industry is currently grounded. Although some routes are still managing to operate, and there is evidence of a gradual domestic air market rebound in China, 2020 will certainly not see the 4.6 billion annual passengers of 2019. The long-term trend of ever-rising air passenger numbers year on year has been brought to a dramatic and rapid halt.

What this means for the global airline industry is vividly on display at airports around the globe as terminals remain empty and aircraft occupy any available parking space.

Like the predominately national response to the virus, so the airline industry is also seeing a wide range of policies and practices tailored and implemented almost exclusively at the national level. This means that some airlines, thanks to well-chosen national policies, will fare better, while others will flounder.

This is because beyond the multilateral single air market of Europe, the global industry remains firmly structured on a bilateral system. This web of country to country air service agreements (ASAs) is basically made up of trade treaties which governments sign with one another to determine the level of air access each is willing to permit. Even in Europe, the single air market essentially acts as one nation internally, while externally, individual European countries continue to deal with many countries on a bilateral basis.

The bilateral system is based on a bundle of rules and restrictions, including airline ownership (typically, a minimum of 51% of an airline must be owned by people from the country where the airline is based), national control, single airline citizenship and home base requirements. This effectively locks airlines into a single country or jurisdiction.

Despite this structure, global cooperation in aviation is strong, particularly across safety standardisation, but less so on the economic front. A lot of this cooperation happens via the International Civil Aviation Organization (ICAO), the industry’s specialised UN agency. Meanwhile, the IATA supports and lobbies on behalf of member airlines.

Likewise, international mergers and acquisitions are rare – aside from in Europe, where partial mergers have created dual and multiple brands like Air France/KLM. Where single airline brands have been created with cross border mergers – such as LATAM Airlines in South America – national aircraft registration and other restrictions remain in place, thereby reflecting multiple airlines in these respects.

Consequently, national responses will be front and centre as the industry responds to the current pandemic. In countries where a single flag carrier is based, such as Thailand and Singapore, governments are unlikely to let their airlines fail. While in others, where multiple airlines operate, a level playing field of assistance and support is more likely, even if outcomes differ widely. This is not to say that all airlines will necessarily survive what is likely to be an extended U-shaped crisis, unlike the more V-shaped crises of the past, such as 9/11 and the 2008 global financial crisis.

The national structure of the industry also highlights why major airlines failing is relatively rare. Yes, airlines have merged in domestic air markets like the US, and individual brands have disappeared as a result, but few major airlines have gone out of business because they failed. Even Swissair, which was famously bankrupt and defunct in late 2001, soon reappeared as Swiss International Airlines.

And so, although airline brands have come and gone, the industry had remained on a growth path for decades. It will take time to recover from the pandemic. Some airlines will fail. But widespread changes to the industry’s structure are unlikely to occur. People will, of course, need and want to travel by air again when this pandemic is over. Which airlines survive – and which go on to thrive – will largely depend on how successful individual countries’ economic support packages turn out to be.

Bailout essentials

Jorge Guira, Associate Professor in Law and Finance

The global outcomes of the crisis, then, are firmly anchored in national responses. The airline industry is cyclical: it is used to peaks and valleys. Bailouts have repeatedly been vital for airlines, so many countries have some sort of precedent to go by.

In any bailout, the key question is whether this is a solvency or liquidity crisis. Solvency means that the airline will be very unlikely to ever remain financially viable. Liquidity means that the airline has a high risk of running out of cash flow but should be solvent soon, if supported. Assessing this is sometimes complex.

Cash is king. “Streamlining” – a fancy word for cost cutting – can help. Unencumbered assets such as aeroplanes can be sold, or used as collateral for loans. But many planes are often leased, so this may be problematic.

Existing contracts must be reviewed. Breach of covenants, which are legally binding promises to do (or to refrain from doing) things in a certain way, may need to be waived. For instance, lease agreements for the planes often require flights to carry on, and business as usual is suspended at present. Other agreements require flights to maintain landing spaces in airports – leading to the “ghost planes” many were appalled by earlier on in the crisis, and that still continue.

Certain financial tests may not be met, such as how much debt there is compared to earnings. These can alarm creditors. And this can lead to deterioration in bond credit ratings, reflecting increased financial distress. Other triggers may also arise. Defaulting on one financial contract usually requires informing other creditors. This can trigger defaults on other agreements, creating a domino effect.

So renegotiating operating and financial contracts is crucial. Airlines may have to pick and choose who to pay first. Unions must be kept happy, and other stakeholders must focus on recovery.

All this means that state bailouts, help and other guarantees are crucial for the industry to survive. In the US, for example, net operating losses are carried forward and used to shield revenues and offset these from tax for when things return to normal.

If liquidity is the problem, the real issue is time: how long will it take for the airline to get back on its feet and resume flying more normally? If solvency is the problem, the company cannot survive the demand collapse it is facing. The COVID-19 pandemic is such a fraught time for airlines because of the difficulty in predicting when the crisis will end. This can complicate determining whether it is a more temporary liquidity crisis or a deeper solvency concern.

After 9/11, the airline industry completely shut down in the US. People witnessing the horrifying scenes of the Twin Towers’ collapse were hardly eager to board a plane. So, the government chose to step in to restore confidence. And it did so, successfully, by offering aid including loans and used warrants, which involves investing in airlines when the stock is at a reduced or rock bottom price and waiting for it to go up again. The US government’s COVID-19 financial rescue package parallels this approach.

The US approach is noteworthy because of its size and scale, and the fact that it is built on the 9/11 case and has been modified for the unique present circumstances. It is also an interesting counterpoint to the strategy of the strongly free market-oriented UK, and Australia, which has been more restrained in its approach.

Airline norms suggest that 25% of revenues should be kept in case of any emergency, but this has tended not to happen recently. Corporate earnings have generally not been held for a rainy day, and now that rainy day has arrived. This creates a classic moral hazard problem: many airlines seem to act as if they are too important to fail, because in the end, they believe they will be bailed out. And regulation does not otherwise hold any excesses in check.

Compounding this, some US airlines have recently been accumulating cheap debt, due to low interest rates and lots of credit availability. The five big US carriers, instead of paying off debt, have been spending 96% of available cash on stock buybacks. Many question whether airlines should be bailed out in these circumstances. Limits on paying dividends, buyback of stock, and other terms would logically apply here, as in the earlier US bailout measures announced in March.

While the US case may provide a helpful initial focus, the UK approach is likely to be highly influential, perhaps more so given the reduced resource level – and greater level of climate awareness – there. As Darren pointed out earlier, one model does not fit all but this may offer a useful comparative framework for other approaches that favour national champions or nationalisations.

The UK is reportedly considering partial nationalisation, such as in the case of British Airways. British Airways has furloughed 35,000 employees, with many pay packets supported by the government – for now. British Airways appears better placed to cherry pick key routes, assets and companies as it ranks in the top group for liquidity.

If Virgin Atlantic were to collapse, its size means it may fit in the too important to fail category. It appears that bailout talks are ongoing but Richard Branson’s life as an offshore UK resident, and Delta’s ownership of a 49% stake, present potential political clouds. Questions about whether it should get state aid given current crisis conditions also arise. This is generally forbidden, although the EU has temporarily indicated a COVID-19 relaxation of the rules. No environmental strings have apparently been attached, as former EU officials and others have suggested should be the case.

Overall, the survival of the global industry therefore depends on bailouts, not only to keep airlines afloat but also for the wider travel and leisure ecosystem.

The lack of of sustainability conditions in UK and indeed US bailouts appears to be mirrored globally. But a Green New Deal in a second recovery phase of aid could provide this. And greater awareness of the issue thanks to the likes of Greta Thunberg, an increased culture of working from home, and ongoing measures to increase accountability and reporting of emissions means this aspect may well play a vital role in the repackaging of airlines going into the future. Much of it begins with how emissions targeting interacts with the COVID-19 crisis.

Aviation and climate change

Roger Tyers, Research Fellow in Environmental Sociology

As Jorge says, for the growing number of people concerned by aviation’s rising carbon emissions, this pandemic may be a rare chance to do things differently. When air travel is eventually unpaused, can we set it on a more sustainable trajectory?

Even before this pandemic hit, aviation faced increasing pressure in the fight against climate change. While other sectors are slowly decarbonising, international aviation is forecast to double passenger numbers by 2037, meaning its share of global emissions may increase tenfold to 22% by 2050.

Most flights are taken by a relatively well-off minority, often for leisure reasons, and of questionable necessity. We might wonder whether it is wise to devote so much of our remaining carbon “allowance” to aviation over sectors like energy or food which – as we are now being reminded – are fundamental to human life.

Regulators at the UN’s ICAO have responded to calls for climate action with their Carbon Offset and Reduction Scheme for International Aviation (CORSIA) scheme. Under this, international aviation can continue to expand, as long as growth above a 2020 baseline is “net-neutral” in terms of emissions.

While critics cite numerous problems with it, the idea is to reduce emissions above the 2020 baseline through a combination of fuel efficiencies, improvements in air traffic management and biofuels. The remaining, huge shortfall in emissions will be covered by large-scale carbon offsetting. Last year, IATA estimated that about 2.5 billion tonnes of offsets will be required by CORSIA between 2021 and 2035.

This plan has been thrown into disarray by the COVID-19 crisis. The emissions baseline for CORSIA was supposed to be calculated based on 2019-20 flight figures. But given that the industry has come to a standstill – demand may take a 38% hit in 2020 – that baseline will be much lower than expected. So once flights resume, emissions growth post-2020 will be much higher than anyone predicted. Airlines will need to purchase many more carbon offset credits, raising operating costs and passing these onto customers.

Airlines trying to get back on their feet will be hostile to any such additional burdens, and will probably seek methods to recalculate the baseline in their favour. But for environmentalists, this might be an opportunity to strengthen CORSIA, which despite its flaws is the only current framework for tackling aviation emissions globally.

Some still consider CORSIA to be an elaborate sideshow. The real game-changer for sustainable aviation would be fuel tax reform, which might receive more scrutiny when attention shifts onto how to repay the eye-watering levels of public debt incurred during lockdown.

Since the 1944 Chicago Convention, which gave birth to ICAO and the modern aviation industry, putting VAT on flight tickets and tax on kerosene jet fuel has been effectively illegal. This is the primary reason why flying is relatively cheap compared to other transport modes, and arguably why the industry has under-invested in research into cleaner fuels.

With the most-polluting form of transport enjoying the lowest taxes, this regime has long been questionable in terms of emissions. It may soon become untenable in terms of tax justice, too. In 2018, France’s Gilets Jaunes movement was partly motivated by anger at increased fuel tax for cars and vans, while air travel continued to benefit from historic tax exemptions. This anger may return when governments inevitably raise taxes to repay their multi-billion-dollar COVID-19-related debts.

Campaigners are already demanding that any airline bailout be linked to tax reform, and there is huge potential there. Leaked EU papers in 2019 suggest that ending kerosene tax exemptions in Europe could raise €27 billion (US$29 billion) in revenues every year. Such sources of revenue may soon become irresistible, and national governments might seek to collect them unilaterally, with or without a coordinated ICAO response.

Tony Blair, the former UK prime minister, once said that no politician facing election would ever vote to end cheap air travel. But – to state the obvious – these are unprecedented times, and public attitudes to flying may well change.

On the demand side, once borders reopen, there could be a short-term travel boom as postponed flights are rebooked and stranded people fly home. But even after an official virus “all-clear”, those considering holidays may think twice before sharing cramped plane cabins with strangers. Business travellers, crucial to airline profits, may find that they’ve got so used to using Zoom, they don’t need always to fly to meetings in person.

As members of the industry admit, by the time passengers return to air travel in significant numbers, the airlines, routes and prices they find may look very different. Governments will face huge industry pressure to safeguard jobs and return to business as usual as soon as possible. But managed properly, this could be the start of a just and sustainable transition for aviation.

The future’s up in the air

All three of us feel the airline industry is at a key turning point. The size and scale of bailouts will vary. Government political will and philosophy, access to capital, and the viability of the industry itself are key factors that will inform whether a company is worth saving.

Any future must be based on the premise of preserving economic vibrancy while reducing climate risk. But not all governments will factor this in.

Events are moving fast, with Emirates in Dubai starting to test passengers for COVID-19 before boarding. Meanwhile, easyJet is considering social distancing on planes as part of a “de-densification” policy, with fewer passengers and higher prices, albeit across more routes.

Longer term, there are various ways this could play out. All depend upon the duration of the crisis and the confluence of political, legal and economic factors.

It is possible that market structure remains unchanged, with ownership of airlines staying relatively stable, supported by bailouts. Under this business-as-usual scenario, sustainability would incrementally be enhanced through airlines retiring older, less carbon efficient planes and replacing them with better ones. But this scenario is subject to tremendous uncertainty.

Or, sustainability might become more important after the crisis, thanks to increased environmental awareness, demand loss, and new green investment. This would take place at different speeds, with Europe perhaps being more proactive through government incentives and serious emissions targeting. The US would lag behind, but making some advances due to increased stakeholder concerns. In this scenario, there is some scaling down of travel to meet demand, which is reduced. Increased sustainable investment emerges. Due to partial recovery, a new normal emerges.

It is also possible that prolonged, severe shortage of capital and an awareness of the climate crisis could, hypothetically, lead to massive change. But governments’ concern for jobs is likely to crowd out environmental concerns. Political forces on the left and right would have to mend fences and agree that, in a depression-like scenario, a new world is needed, not just a new normal.

Here’s what should happen during a bear-market rally as sentiment rises

By Elliott Wave International

A question was posed to Elliott Wave International President Robert Prechter for a classic Elliott Wave Theorist (Prechter’s monthly publication about financial markets and social trends since 1979):

Under the Wave Principle, what is the most important thing to watch other than price?

Prechter answered:

Volume.

You see, high trading volume means that traders are displaying a great deal of conviction about a given market, whether the trend is up or down. Low trading volume means a lack of enthusiasm.

In other words, during strong bull markets, up days are often accompanied by high trading volume, while countertrend declines usually occur on low trading volume. In bear markets, down days are generally powered by tons of trading volume with rallies occurring on weak volume.

When a bear market is near an end, price declines usually begin to occur on contracting volume. Likewise, when a bull market is exhausted, price rises are usually accompanied by waning volume.

For example, here’s a chart and commentary from EWI’s Oct. 5, 2007 U.S. Short Term Update:

Note how weak the volume pattern has been in the push from the August 16 low, which is one of the reasons that we keep saying the rise is “narrow.” The middle clip on the chart shows the 10-day average of NYSE New Highs minus New Lows, showing yet another indicator that is lagging as prices make new highs.

Less than a week later, the S&P 500 index hit a then intraday record high before beginning a bear market slide.

Now, let’s consider the current market environment, and this chart and commentary from the April 20, 2020 U.S. Short Term Update:

The power of a second-wave rally should wane as sentiment rises. So far, the market’s advance since March 23 fits this profile. As the chart shows, daily market volume has contracted steadily as the advance has progressed. The 3-day average has come back to nearly the level it was in late-February, when the Dow was still above 27,000.

Now, let’s get back to that question from the classic Theorist about “the most important thing to watch other than price.”

The question itself implies that no other indicator is as important as price — or price patterns, to be more exact. And that is absolutely correct.

As Frost & Prechter’s Elliott Wave Principle: Key to Market Behavior notes:

Since wave analysis is based upon price patterns, a pattern identified as having been completed is either over or it isn’t. If the market changes direction, the analyst has caught the turn. If the market moves beyond what the apparently completed pattern allows, the conclusion is wrong, and any funds at risk can be reclaimed immediately.

You can read the online version of this Wall Street classic book in its entirety — 100% free. Simply sign up for a free Club EWI membership for instant access.

This article was syndicated by Elliott Wave International and was originally published under the headline This Major Stock Market Indicator is Flashing a HUGE Signal. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

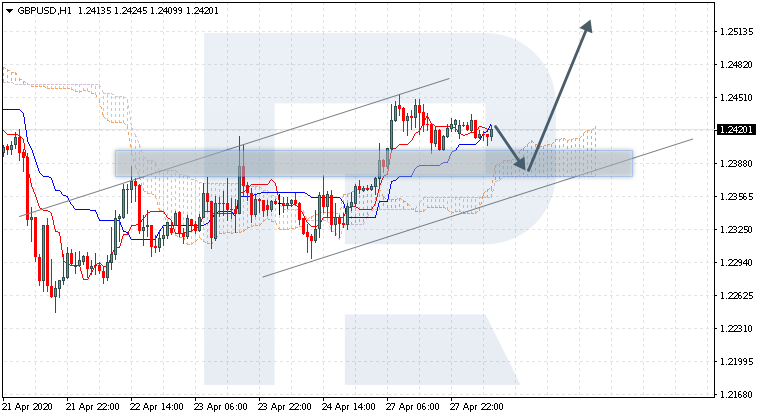

GBPUSD is trading at 1.2420; the instrument is moving above Ichimoku Cloud, thus indicating a bullish tendency. The markets could indicate that the price may test the cloud’s downside border at 1.2380 and then resume moving upwards to reach 1.2525. Another signal in favor of further ascending movement is the price’s rebounding from the rising channel’s downside border. However, the scenario that implies further growth may no longer be valid if the price breaks the cloud’s downside border and fixes below 1.2350. In this case, the pair may continue falling towards 1.2285.

USDJPY, “US Dollar vs Japanese Yen”

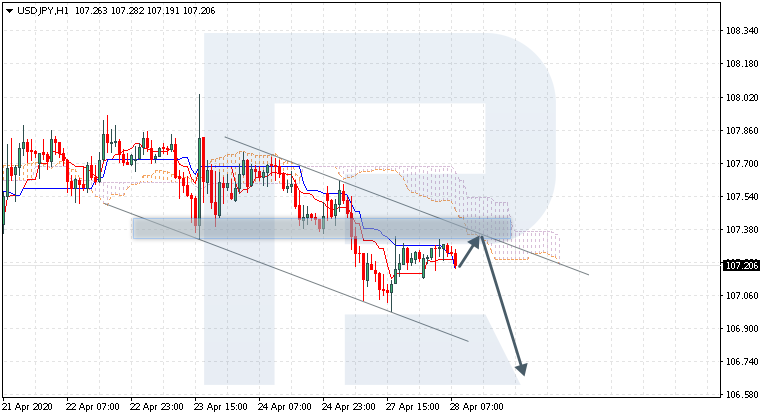

USDJPY is trading at 107.20; the instrument is moving below Ichimoku Cloud, thus indicating a descending tendency. The markets could indicate that the price may test the cloud’s downside border at 107.35 and then resume moving downwards to reach 106.65. Another signal to confirm further descending movement is the price’s rebounding from the descending channel’s upside border. However, the scenario that implies further decline may be canceled if the price breaks the cloud’s upside border and fixes above 107.65. In this case, the pair may continue growing towards 108.35.

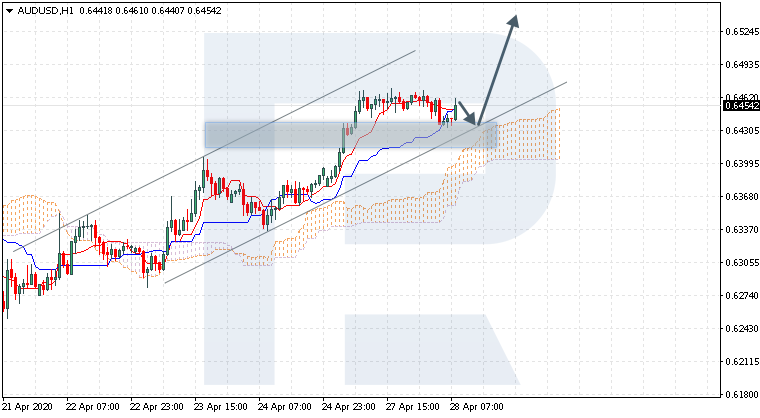

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD is trading at 0.6454; the instrument is moving above Ichimoku Cloud, thus indicating a bullish tendency. The markets could indicate that the price may test the cloud’s upside border at 0.6430 and then resume moving upwards to reach 0.6535. Another signal to confirm further ascending movement is the price’s rebounding from the support level. However, the scenario that implies further growth may be canceled if the price breaks the cloud’s downside border and fixes below 0.6365. In this case, the pair may continue falling towards 0.6285.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Most of that is aimed at individual Americans in the form of additional unemployment insurance or the so-called economic impact checks. About $1.2 trillion – and counting – represent bailouts for American companies, large and small.

And more than 60% of that is in the form of grants or other financial assistance that will likely become grants – funds that will not be recovered by taxpayers. The Congressional Budget Office estimated on April 23 that the company-related coronavirus bailouts, excluding the fourth one just signed into law, will ultimately cost more than $400 billion over 10 years. Given that most of the latest bailout, worth $484 billion, will most likely end up becoming grants to small businesses as well, the price tag is bound to get a lot higher.

It may not come as a surprise that taxpayers ultimately foot the bill when lawmakers spend their money to bail out a corporate industry – such as Wall Street during the Great Recession – or the entire economy today. But this is actually the exception, not the rule.

The truth is, as my research shows, the vast majority of business bailouts passed by Congress over the past half century have either broken even or generated a profit.

Image by MotionStudios / Pixabay

Profitable bailouts

As part of my ongoing research on economic policymaking during recessions, I studied 10 corporate bailouts approved by Congress since 1969.

I only looked at bailouts that involved direct assistance – in the forms of loans, guarantees, grants or capital injections – by Congress to a company or industry in financial distress. I excluded the Savings and Loan crisis of the 1980s and 1990s because that was less of a bailout and more of an expensive regulatory wind-down. All of the figures below have been adjusted for inflation.

I found that half of the bailouts made a clear profit for taxpayers.

For example, Lockheed Martin ran into financial difficulties in 1971 because the planes, helicopters and other military equipment it was making for the U.S. Department of Defense cost more than the Pentagon agreed to pay, which led to significant losses and fees. The defense contractor pinned its survival on making money off its state-of-the-art TriStar airliner but struggled to secure enough financing to finish the project.

Congress, concerned with the loss of at least 25,000 jobs if Lockheed went bankrupt, provided Lockheed with a lifeline in the form of loan guarantees. That is, it agreed to back a $1.62 billion private loan in exchange for a fee. Although the TriStar was a flop, it was enough to keep Lockheed solvent, and taxpayers earned $198 million.

Similarly, automaker Chrysler found itself in financial peril in late 1979 in part due to its slow reaction to market shifts brought about by the 1970s energy crisis. Consumers wanted more fuel efficient cars; Chrysler made too many gas guzzlers. Post-bailout studies suggested the company was headed toward insolvency.

The potential loss of 250,000 jobs and the adverse impact on automotive dealers and suppliers spurred Congress to offer Chrysler up to $4.98 billion in loan guarantees. As a precondition for this help, Chrysler, in addition to paying fees on the loans, granted the U.S. government rights to buy 14.4 million company shares at a set price. This arrangement provided taxpayers with $1.03 billion – on $4 billion worth of loans – when the government sold the shares in 1983.

And more recently, Congress pledged trillions of dollars saving the financial system in 2008. For my purposes, I split the aid to companies into four distinct bailouts, three of which made large profits.

One in particular, the much-deridedTroubled Asset Relief Program, was a $854 billion bailout for financial companies. Ultimately, $382 billion was dispersed to Wall Street firms like Citigroup, JPMorgan and AIG in exchange for preferred stock and other compensation. Taxpayers earned $32.5 billion.

A separate bailout to Fannie Mae and Freddie Mac was even more lucrative. The U.S. government received preferred stock for the $234 billion invested in the two housing giants. Taxpayers got its money back as well as $123 billion in profits.

There were also two bailouts – for the Farm Credit System in 1987 and the Steel and Oil and Gas industries in 1999 that likely made money, but I was unable to find all the details necessary to do the full analysis. At a minimum, my review suggests both broken even.

Losses (mostly) by design

Three bailouts approved by Congress since 1969 cost taxpayers’ money. In two of the cases, this was by design.

The railroad industry, from 1960 to 1970, saw its total net income cut in half due, in part, to mismanagement, market shifts in transportation from rail to vehicles and poor oversight by regulatory agencies. Its collapse not only ensured a large spike in unemployment, it meant losing a mode of transportation that, at the time, moved 41% of the nation’s goods and shipped U.S. military equipment domestically.

Congress, seeing this industry as vital to U.S. commerce and defense, wanted to ensure the railroad industry remained afloat. Beginning in 1970, several ailing railroad companies received $25.3 billion worth of loan guarantees and grants that were never meant to be repaid. Eventually, seven bankrupt rail companies were consolidated into one profit-making corporation on the taxpayers’ dime.

The terrorist attacks on 9/11 shut down the national aviation system for three days and significantly reduced airline traffic for the remainder of 2001. The airline industry, which made up close to 10% of U.S. GDP at the time, was expected to lose $5 billion by the end of 2001.

Congress quickly provided the industry with $22.1 billion in financial assistance to ensure its stability and viability. A third of this assistance came in the form of grants never meant for repayment as compensation for losses stemming from 9/11 and the three-day shutdown of the national aviation system. The remainder came in the form of loan guarantees that produced a slight profit.

And with extra money left over from the Troubled Asset Relief Program, the U.S. Treasury loaned automakers General Motors and Chrysler and their financing units about $97.2 billion in exchange for the right to purchase stock at a set price. This was in addition to a $30.5 billion loan issued in September 2008 to finance more fuel-efficient cars. While most of the aid actually disbursed was paid back, taxpayers lost $14.9 billion after both companies went bankrupt.

Coronavirus bailouts

Like the bailouts for the railroad and airline industries, a large chunk of the coronavirus aid is never meant to be paid back.

As long as small businesses keep workers on their payrolls, they won’t have to pay back the $659 billion in total assistance under the payroll protection program.

The airline industry has received $61 billion in financial assistance from Congress, including a little more than half in grants. Small passenger airlines, the bulk of applicants, will not repay this assistance, while large airlines are expected to.

Congress also authorized Treasury Secretary Steven Mnuchin to provide distressed corporations and state and local governments with up to $454 billion in loans and $17 billion for public companies deemed critical to national security. Taxpayers will get interest and possibly equity stakes in some cases.

At the end of the day, Congress knows that when literally tens of millions of jobs, millions of small businesses and dozens of vital industries are at stake, you don’t haggle over the details. You just rescue them.