By IFCMarkets

On Friday, the US stock market indexes rose. Moreover, S&P 500 renewed intraday historical high for the seventh time in July. Despite this, the total growth of the stock market over the past month was relatively modest. The Dow Jones Industrial Average rose by 2,8%, S&P 500 by 3,6% and Nasdaq – 6,6%. Quarterly earnings of high-tech companies increased significantly more than the ones of the “traditional economy” corporations. Weak reports of McDonald’s, Chevron and Exxon were released on Friday. Currently, market participants are waiting for the reduction of the total earnings of S&P 500 components by 3,7%, whereas, on Thursday, the forecast was better: minus 2,8%. The US stocks were buoyed by negative GDP data for the second quarter of 2016 published on Friday. The economic growth was 1,2%: much weaker than investors expected (+2,6%). This has significantly reduced the probability of the early rate hike by the Fed and has contributed to the maximum weekly fall of the US dollar index over the past 3 months. The weakening of the exchange rate and the low interest rates on loans may improve financial indicators of the US companies. An additional positive for the stock market was the increase in consumer spending by 4,2% according to the results of the second quarter of 2016. This is their maximum growth since the 4th quarter of 2014. This morning the head of the Federal Reserve Bank of New York said that the Fed could raise the interest rate before the November US presidential election, in case of the improvement in indicators of the US economy. This contributed to a slight strengthening of the US dollar. On Monday, at 16:00 CET, the June building expenses and the ISM manufacturing index will be released in the United States. We deem that their preliminary forecasts are moderately positive.

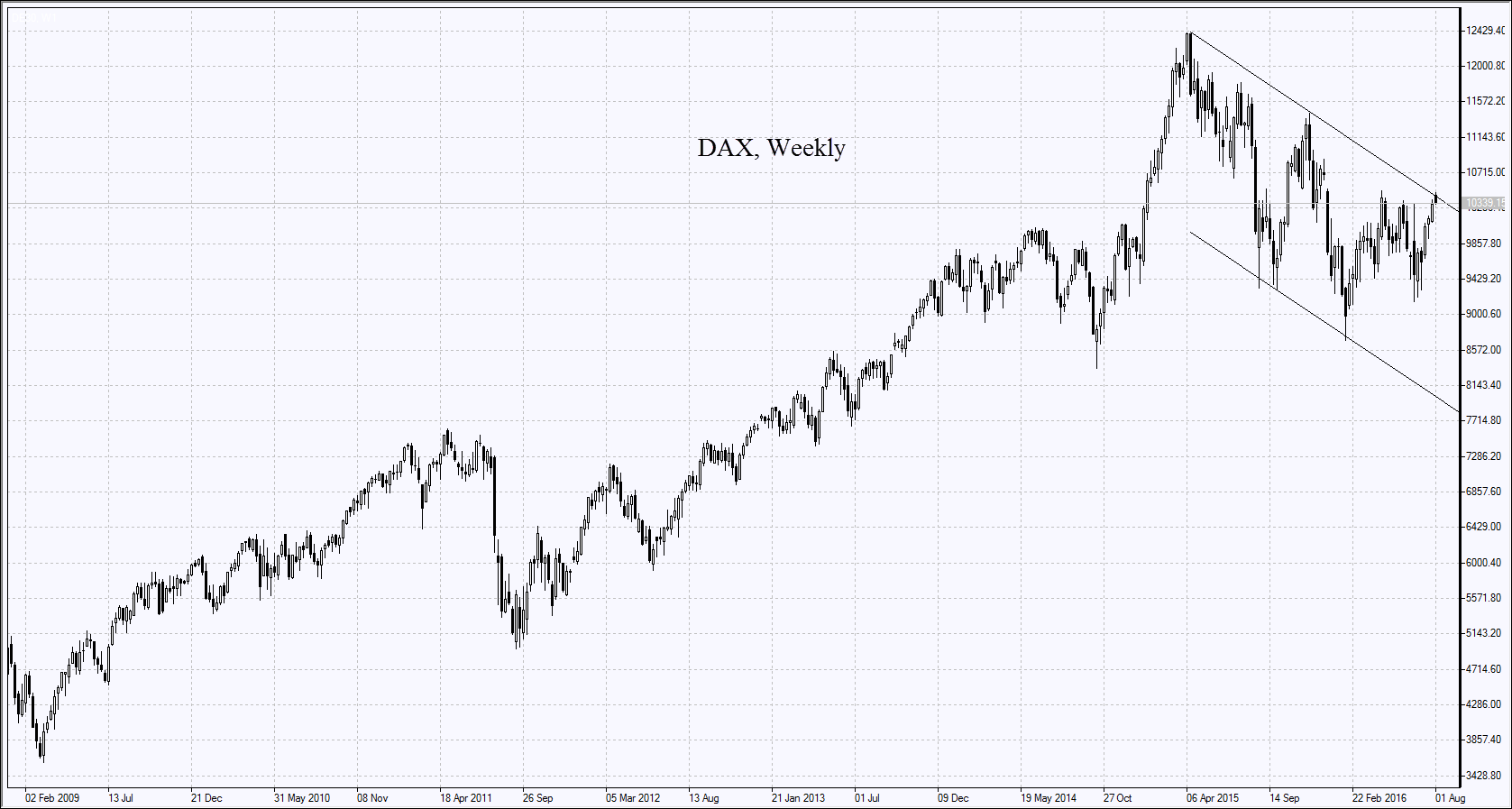

In July, the pan-European STOXX Europe 600 EUR index rose by 3,6%. On Monday, its growth is mainly contributed by the shares of banks, which are becoming expensive against the backdrop of the annual stress tests by the European Banking Authority. But there is also good news. The stocks of the most “problematic” Italian bank Monte dei Pasch rose by 5,8% and the stocks of German Deutsche Bank – by 2,6%. The quotations of the Raiffeisen and UniCredit banks have decreased, which limited the overall growth of the banking sector. The stocks of the British mining company Anglo American rose by 4% after the increase of its profit forecasts. This has contributed to the growth of quotations of other companies from this sector. This morning positive July industrial PMIs for Germany and for the whole Eurozone were published in the EU. Today, no more significant macroeconomic statistics are expected.

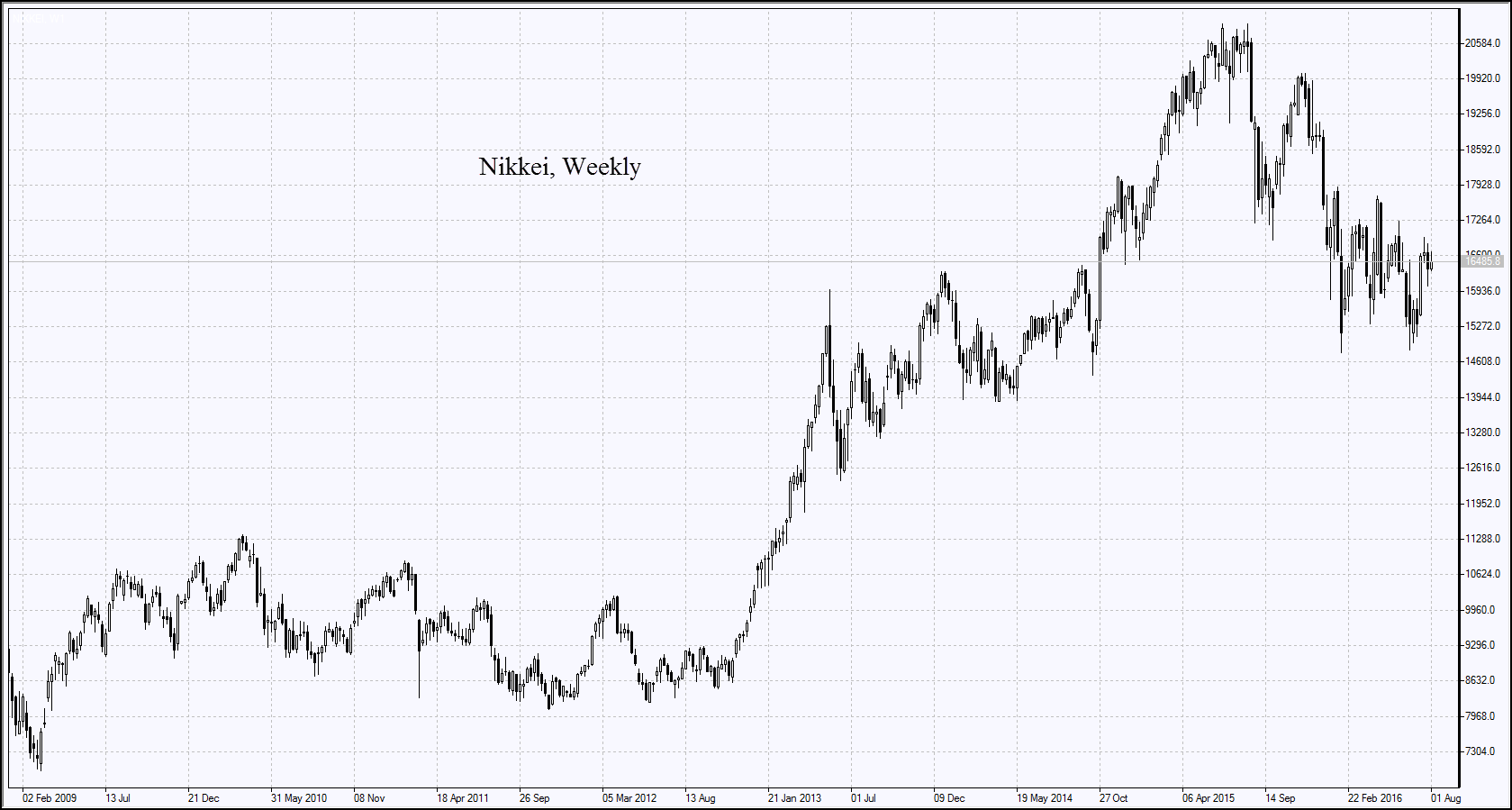

Nikkei rose on Monday due to the decision of the Bank of Japan to double the annual volume of redemption of ETFs to 6 trillion yen from 3.3 trillion yen. The volume of redemption of bonds and negative discount rate remained unchanged. The shares of Japanese banks and financial companies were leading the growth as on Friday. Note that tomorrow, the head of the Japanese government Shinzo Abe is going to present a plan for additional expenses to stimulate the economy of $ 28 trillion yen. This may affect the quotation of Japanese assets. In addition, on Tuesday, at 7:00 CET, positive July consumer confidence index will be released in Japan.

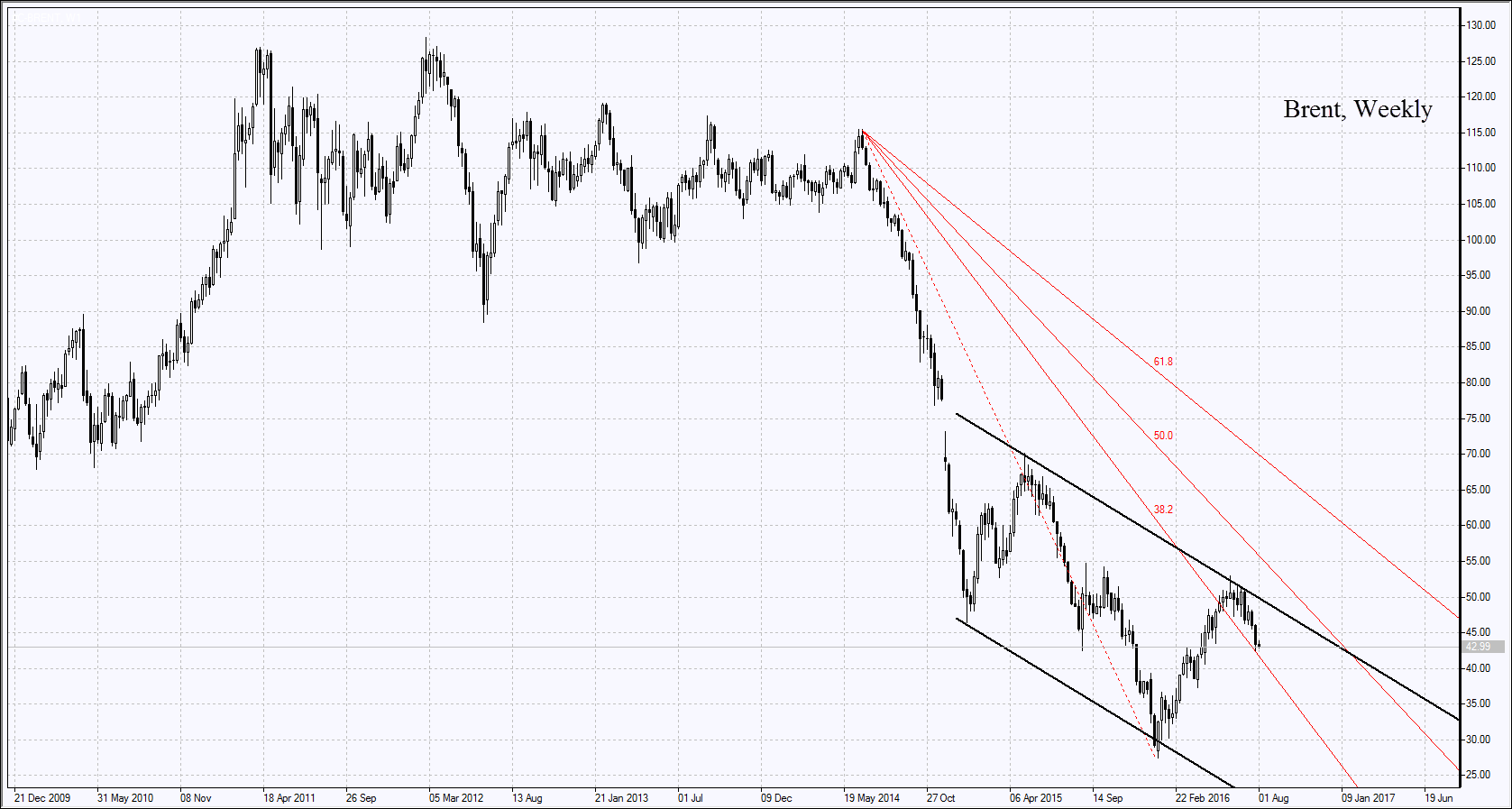

On Monday, the industrial PMI by Caixin/Markit was released in China. According to the results of July, it rose for the first time in the last 17 months, significantly exceeded the forecasts (48.7 pips): 50.6 points. This PMI has exceeded 50 pips for the first time since February, 2015. Market participants do not exclude the recovery of growth of the Chinese economy, which has had positive impact on the quotations of commodity futures. Note that in July of the current year, China’s oil demand rose by 2,9% compared with the same period of 2015 and was 11,06 million barrels per day. By the consumption of oil, it is on the 3rd place in the world after the United States and the European Union.

Market Analysis provided by IFCMarkets

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.