By IFCMarkets

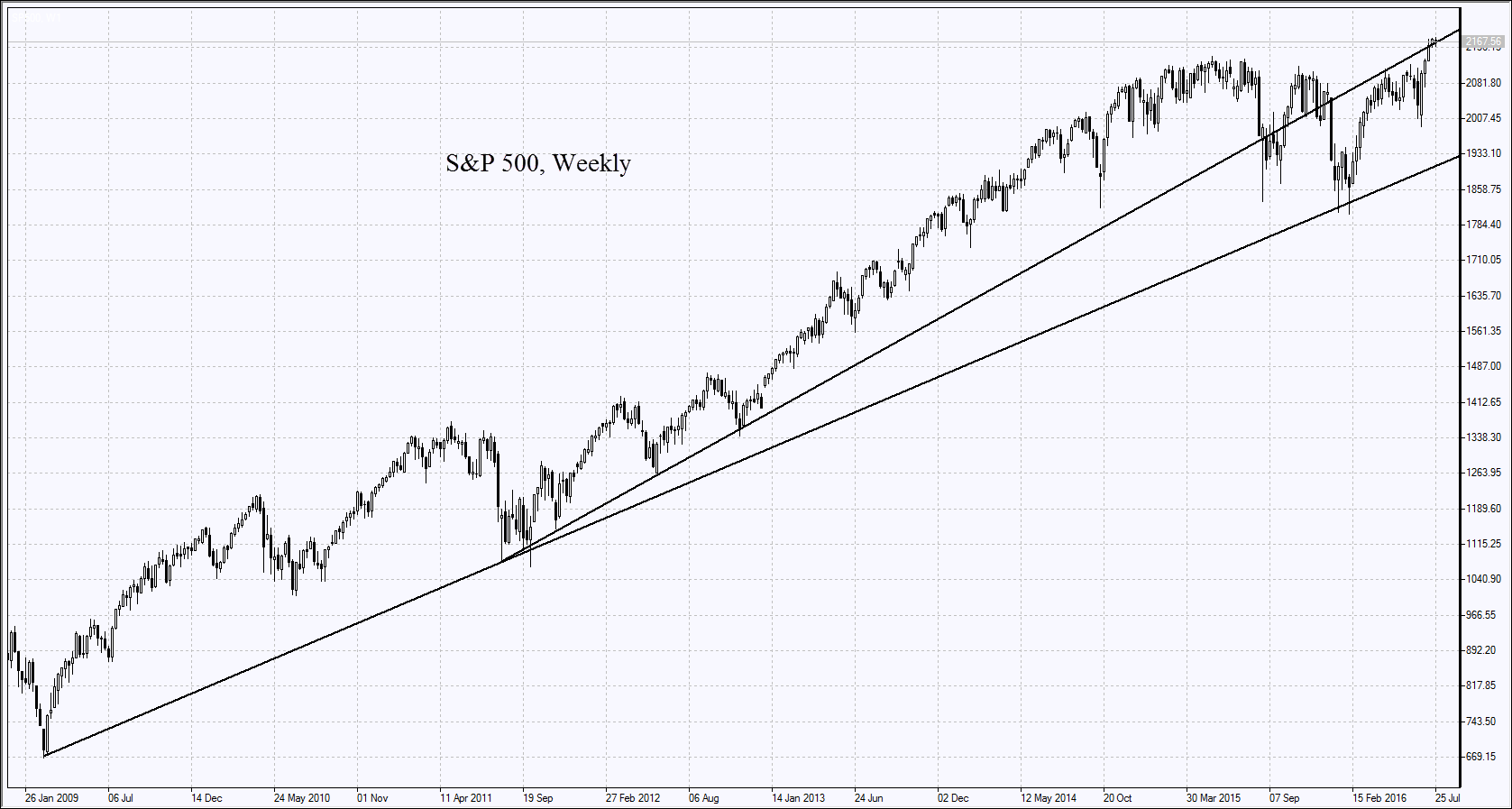

On Thursday, the US stocks slightly rose within a narrow neutral range, which lasts for already 10 trading sessions in a row. Due to good quarterly reporting, the stocks of Apple (+1,3%), Alphabet (+4%) and Amazon.com (+1,7%) rose. However, the total growth of the stock market was weak because of the very bad reporting of automaker Ford. Its stocks fell by 8%, which had a negative impact on the entire industry. The quotes of General Motors fell by 3,2%, and the quotes of Fiat Chrysler – by 4,8%. Yesterday’s macroeconomic data was negative. The initial jobless claims rose in the week and exceeded the preliminary forecasts. The US trade deficit in June was more than expected. This has contributed to the weakening of the US dollar. Today, at 14:30 CET, important macroeconomic data will be released in the United States: GDP and personal expenses for the second quarter. Michigan Consumer Sentiment Index (MCSI) for July will be reported at 16:00 CET.

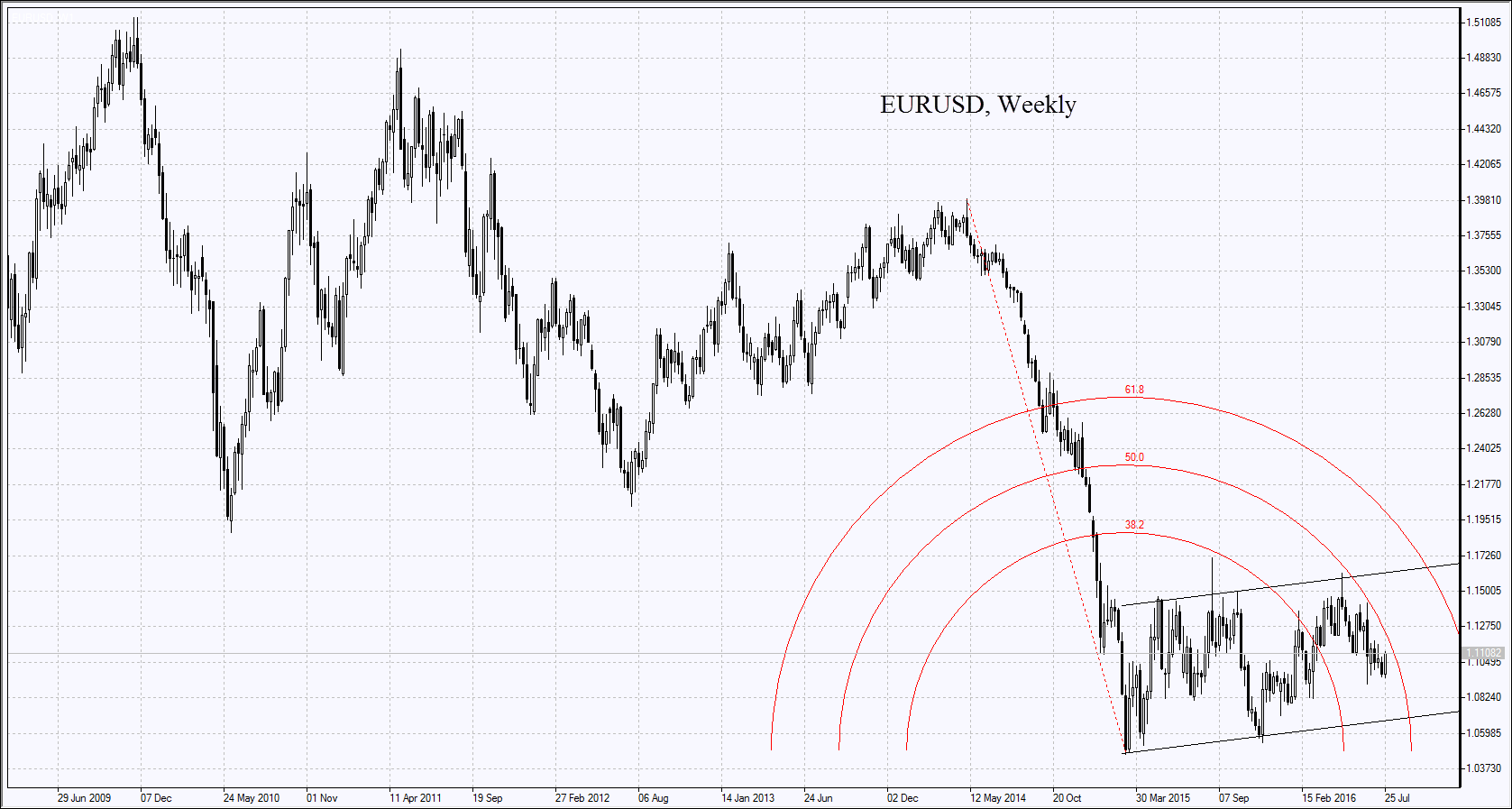

The European stock indexes are rising on Friday after a small decline on Thursday. Yesterday, the British bank Lloyds announced about the negative impact of Brexit and its stocks fell by 5,8% pulling the entire banking sector. The quotes of Credit Suisse declined by 5% because of its reorganizational plans. The yesterday’s Eurozone statistics was positive, but investors ignored it. Various confidence indexes increased in the EU (industrial, consumer, business climate, etc.). In Germany, the unemployment rate has decreased slightly and the inflation has increased in July. The moderate rise in consumer prices is now a good factor, as it reduces the risk of deflation. Today, the pan-European STOXX 600 index rose by almost 2% due to good corporate information. The stocks of French energy company EDF rose by 9,5% after the board of directors approved the construction of Hinkley Point NPP. The prices of Kering rose by 5,6% due to the increase of sales of its Gucci brand by 7,4% in the second quarter. An additional positive for the European stock indexes and the euro was the growth of the Eurozone GDP in the second quarter of the current year by 1,6% and the 0,9% July inflation rate in annual terms. Both indicators slightly exceeded the forecasts. Today, no more macroeconomic data is expected in the EU. Note that in July the pan-European STOXX 600 index demonstrated 3, 2% maximum growth since October. The STOXX Europe 600 banks index rose by 6,4% in a month, which is its maximum growth since February of the 2015. However, in comparison with the beginning of 2016, Stoxx 600 banks index has fallen 27%.

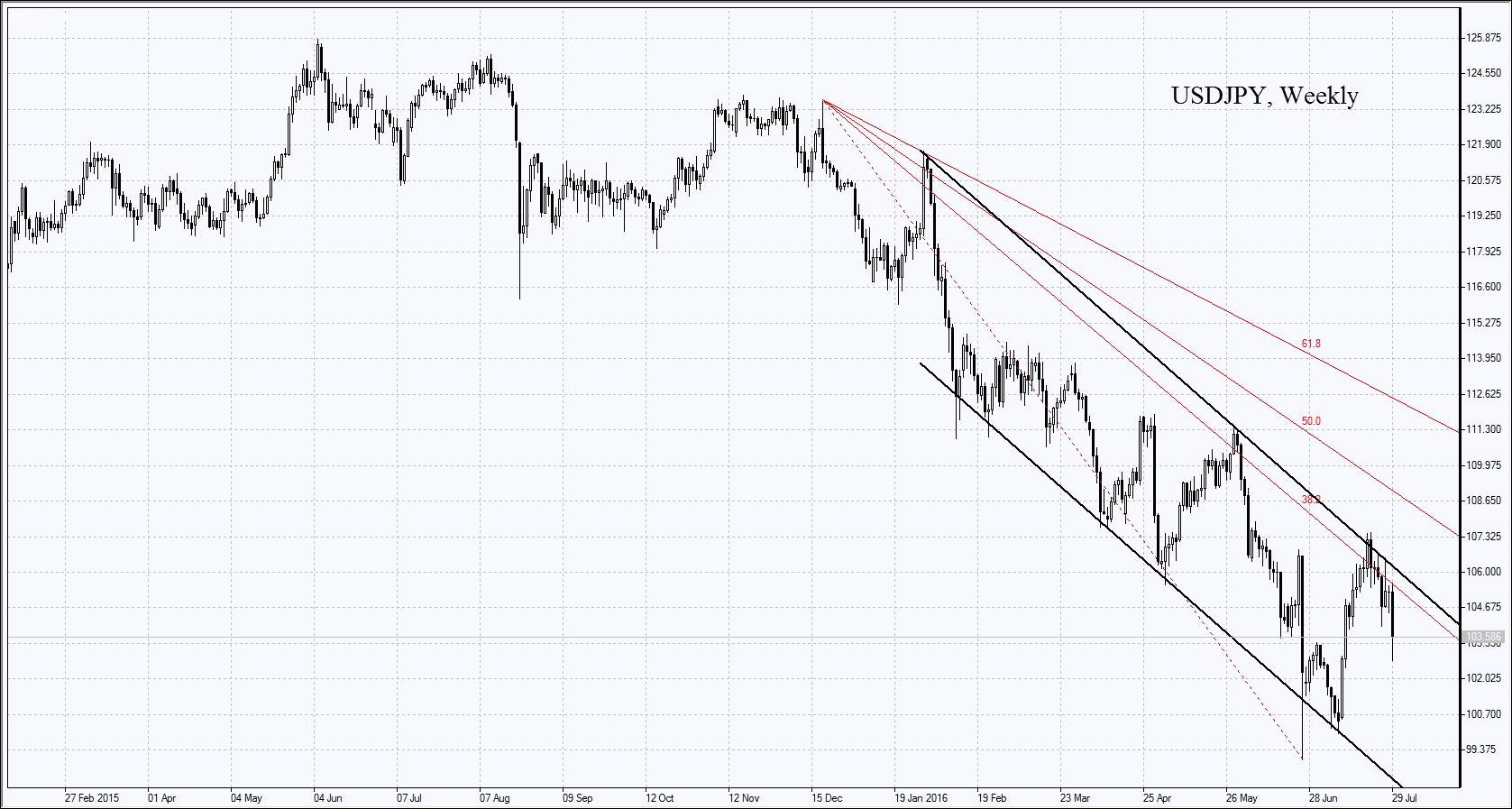

Today, Nikkei demonstrated strong fluctuations, but, nevertheless, according to the results of trades it rose. The Bank of Japan held its regular meeting. It kept the key rate unchanged at minus 0,1%, but increased the limits on the purchase of ETFs by 2 times to 6 trillion yen from 3,3 trillion. Such decision led to a marked strengthening of the yen. Nikkei rose due to the increase of stock prices of banks and financial companies against the backdrop of the expected redemption of securities by the Bank of Japan: Mitsubishi UFJ Financial Group (+7,7%), Mizuho Financial Group (+5,7%), Dai-ichi Life Insurance (+8,7%), Sompo Japan Nipponkoa Holdings (+4,3%). An additional positive was today’s Japanese macroeconomic data.

The unemployment rate decreased from 3,2% to 3,1% and the industrial production increased by 1,9%. In the morning, at 4:00 CET, will be reported the Japanese industry business activity index for July in the final reading. No changes are expected yet. This index is below 50 pips for already 4 months in a row, which means a decline in production.

Today, Brent oil prices are falling for the seventh trading session in a row and they are ready to demonstrate a maximum monthly decrease from December 2015. However, the Goldman Sachs bank confirmed its forecast that the oil will keep the range of $45-50 per barrel until the middle of the next year.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.