By IFCMarkets

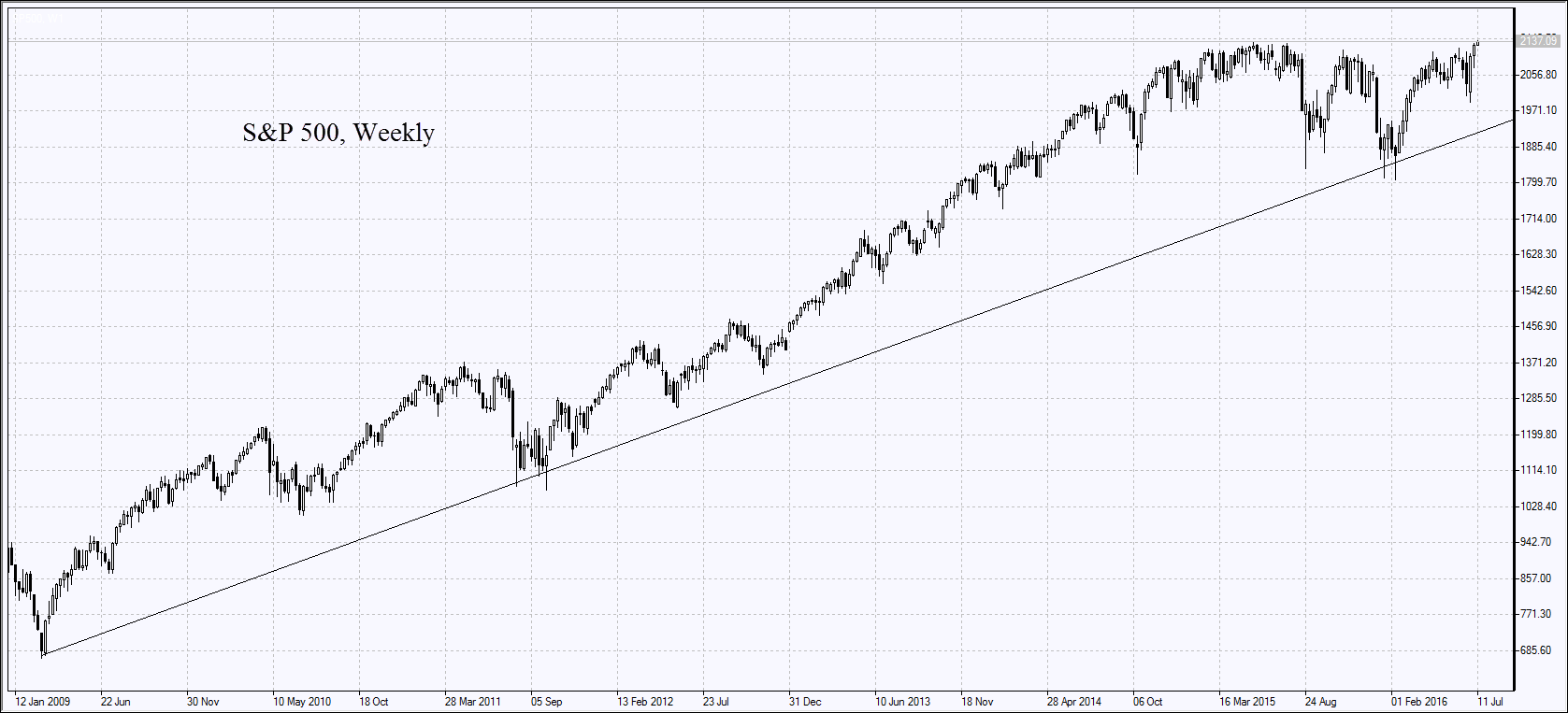

The US labour market data for June came out positive on Friday. Non-farm Payrolls rose 287 thousand which is the record growth since last October. For the first time in recent 4 months the real data exceeded forecasts which pushed the stock indices up. S&P 500 approached once again its historical high hit in May 2016. The reaction of the money market was moderate as market participants still doubt the Fed is to hike the rates this year. The probability of rate hike is around 25%. No significant economic data came out on Monday. US stock markets continued Friday upward movement. The US dollar index rose amid weaker yen. The wholesale stockpiles data will come out on Tuesday, the outlook is moderately negative. This week investors will be focused on quarterly earnings of US companies. Aluminum producer Alcoa will report its earnings on Monday after the bell. The total earnings of S&P 500 components are expected to fall by 3.9% in Q2 2016 compared to the same period of 2015. It fell 5% in Q1 which did not weigh on stocks.

European stocks rose on Monday for 3rd straight day while euro was steady. Nevertheless, unlike the US indices the pan-European STOXX 600 is still 10% below its high. The weak performance can be explained by Brexit risks. The news came out on Monday that German smelter ThyssenKrupp is planning to buy out some assets from Indian Tata Steel. This supported the European steel companies stocks increase. The additional positive was the neutral forecast from Goldman Sachs bank of Brexit influence on the stock market. British pound strengthened while British stocks rose on Monday on the news the only candidate to become UK PM after David Cameron’s resignation is current Home secretary Theresa May. Still, the further strengthening of pound is questionable. The Bank of England meets on Thursday. The changes it will cut the rate from 0.5% to 0.25% exceed 70%. Before Brexit the chances were estimated only at 13%. Expectations of rate hike pushed British FTSE 100 index up. It added 4.5% last week and 20% from its February low.

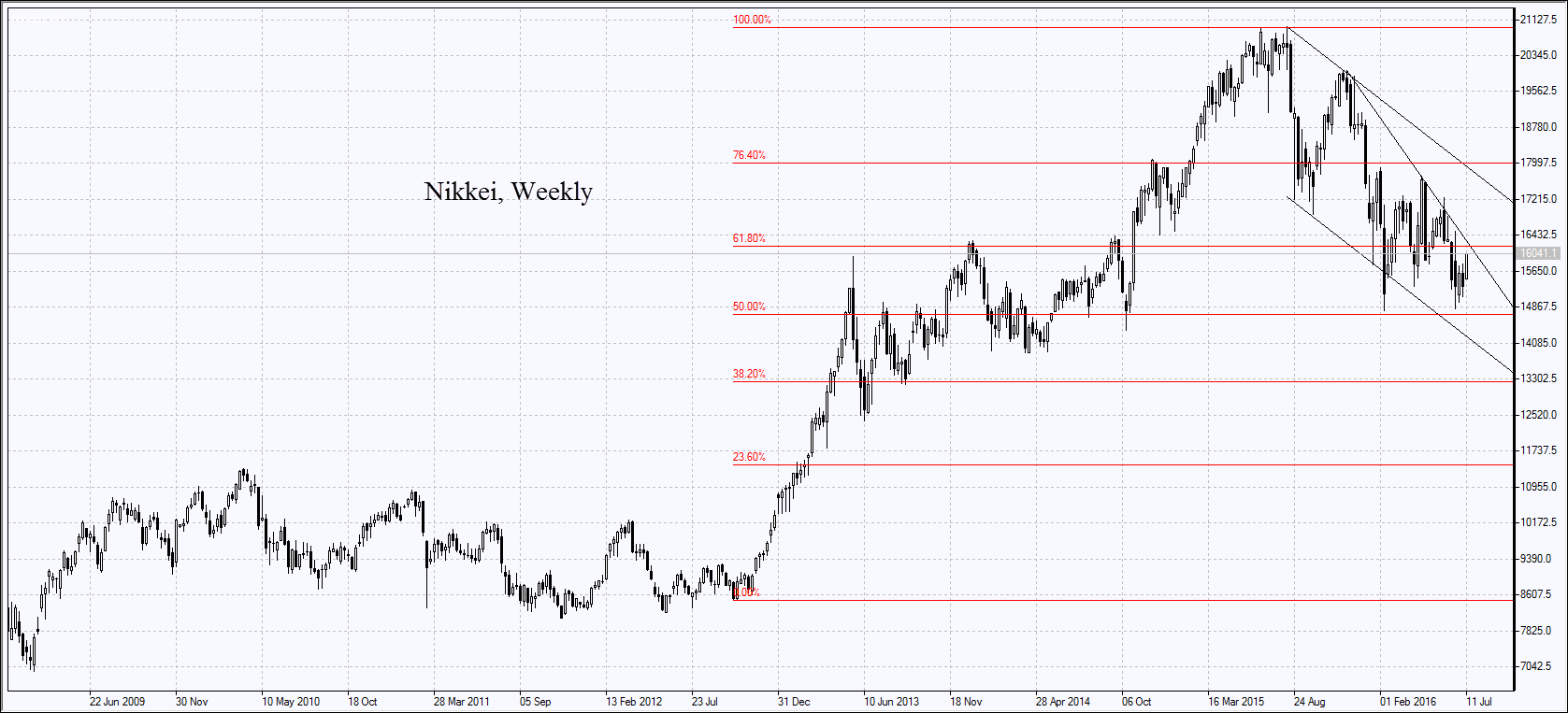

Nikkei advanced 4% on Monday amid severe weakening of Japanese yen by around 2%. The USDJPY showed the record growth in recent 3 months while Nikkei — in 5 months. In Japan, the governing coalition headed by PM Shinzo Abe, won elections to the upper chamber of Parliament. Investors expect further weakening of monetary policy by the Bank of Japan to stimulate the economy.

The China’s external trade balance data for June will come out on Friday and may affect commodity futures. We see their tentative outlook as moderately negative.

Grain futures edged up on Friday after drought was forecasted in Europe. The news that India increased corn imports by 0.5mln tonnes this year and that corn crops fell in Brazil also weighed on grain prices. The monthly world agricultural report from USDA will come out on Tuesday. The soy beans, corn and wheat crop yields are expected to fall in 2015-2016 season.

Market Analysis provided by IFCMarkets

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.