By IFCMarkets

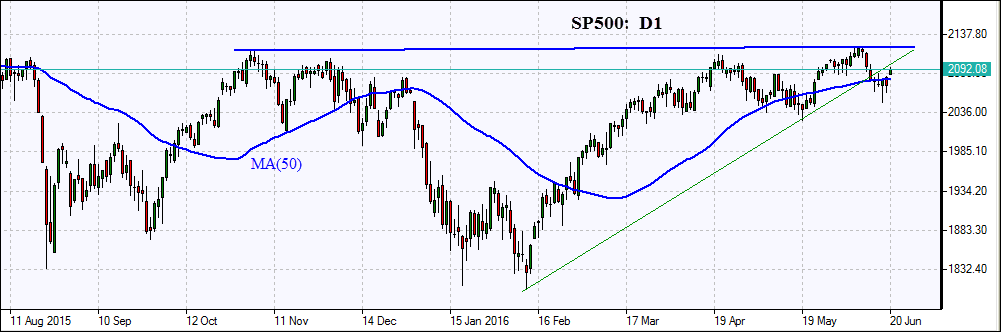

US stocks retreated on Friday as slower growth outlook for US economy that prevented the rate hike by Fed at its June meeting and concerns about Brexit’s impact weighed on market sentiment. The dollar ended lower: the live dollar index data indicate the ICE US Dollar Index, a measure of the dollar’s value against a basket of six major currencies, slipped 0.4% to 94.17, losing 0.5% over the week. The Dow Jones industrial average slipped 0.3% to 17675.03, ending the week 1.1% lower. The S&P 500 closed 0.3% lower, down 1.2% for the week. The Nasdaq Composite Index dropped 0.9% led by 2.3% loss in Apple stocks on news China ordered the US smartphone maker to stop sales of iPhone 6 and iPhone 6 Plus devices in Beijing as the design for the devices is too similar to a Chinese phone. The tech stock index tumbled 1.9% in the past week, its biggest weekly slide since the end of April. After Fed’s dovish statement on Wednesday indicated policy makers shifted to more cautious stance on monetary tightening St. Louis Fed President James Bullard said on Friday the Fed only needs to raise rates once through the end of 2018, with current low growth trend and low inflation likely to persist. In other economic news US housing starts dipped slightly in May but remained near recent highs. No important economic data are expected today in US.

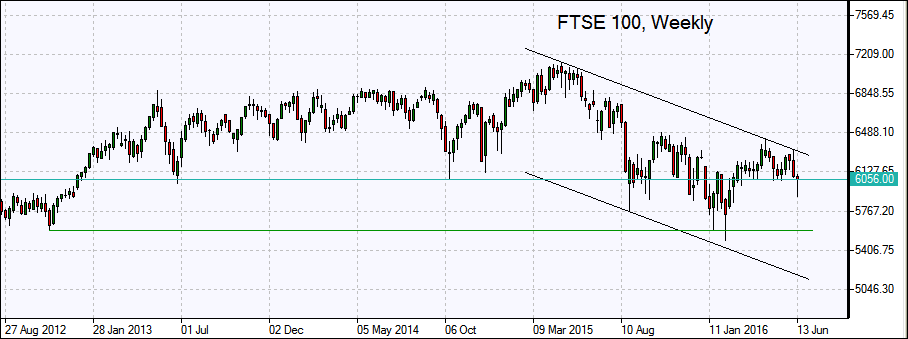

European stocks advanced on Friday after British campaigning before the referendum on UK exit from European Union was suspended the previous day and Friday following the killing of lawmaker Jo Cox on Thursday. The Labor Party member was a supporter of the UK remaining in the EU. The UK vote on Brexit will take place on Thursday, June 23. The euro strengthened against the dollar. The Stoxx Europe 600 closed up 1.4% led by bank stocks: Banca Popolare di Milano rallied 9.8% and Deutsche Bank gained 5.2%. German DAX 30 stock index rose 1% to 9631.36. France’s CAC 40 gained 1.1% and UK’s FTSE 100 lost 0.3%. No important economic data are expected today in euro-zone.

Asian stocks are recovering as fears that the UK would vote to leave the European Union receded somewhat today with the campaign to stay in EU regaining momentum though opinion polls suggest voters are evenly split. Nikkei rose 2.4% today recording the biggest gain in two months with a weaker yen helping exporter stocks. Panasonic shares jumped 2.7%, Toyota Motor gained 2.3% while Mitsubishi Motors was down 3.5% after announcement on Friday the company will allocate at least $600 million to compensate owners of some of its mini-vehicles for overstating fuel economy specifications.

Oil futures prices are advancing today with easing concerns about possible UK exit from EU. August Brent crude jumped 4.2% to $49.17 a barrel on London’s ICE Futures exchange on Friday despite a Baker Hughes report active oil rigs rose for the third week in a row with shale firms adding 9 rigs in the past week.

Gold prices are falling toady with spot gold down 1.1% at 1283.13 an ounce after adding 1.44% on Friday, biggest daily gain since June 3. Safe haven demand is supporting gold price as investors brace for higher volatility with opinion polls not indicating a clear lead for campaigners in favor of exiting from EU or remaining in the union. Managed funds increased their net long position in gold to the highest in nearly five years last week according to US Commodity Futures Trading Commission report.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.