By IFCMarkets

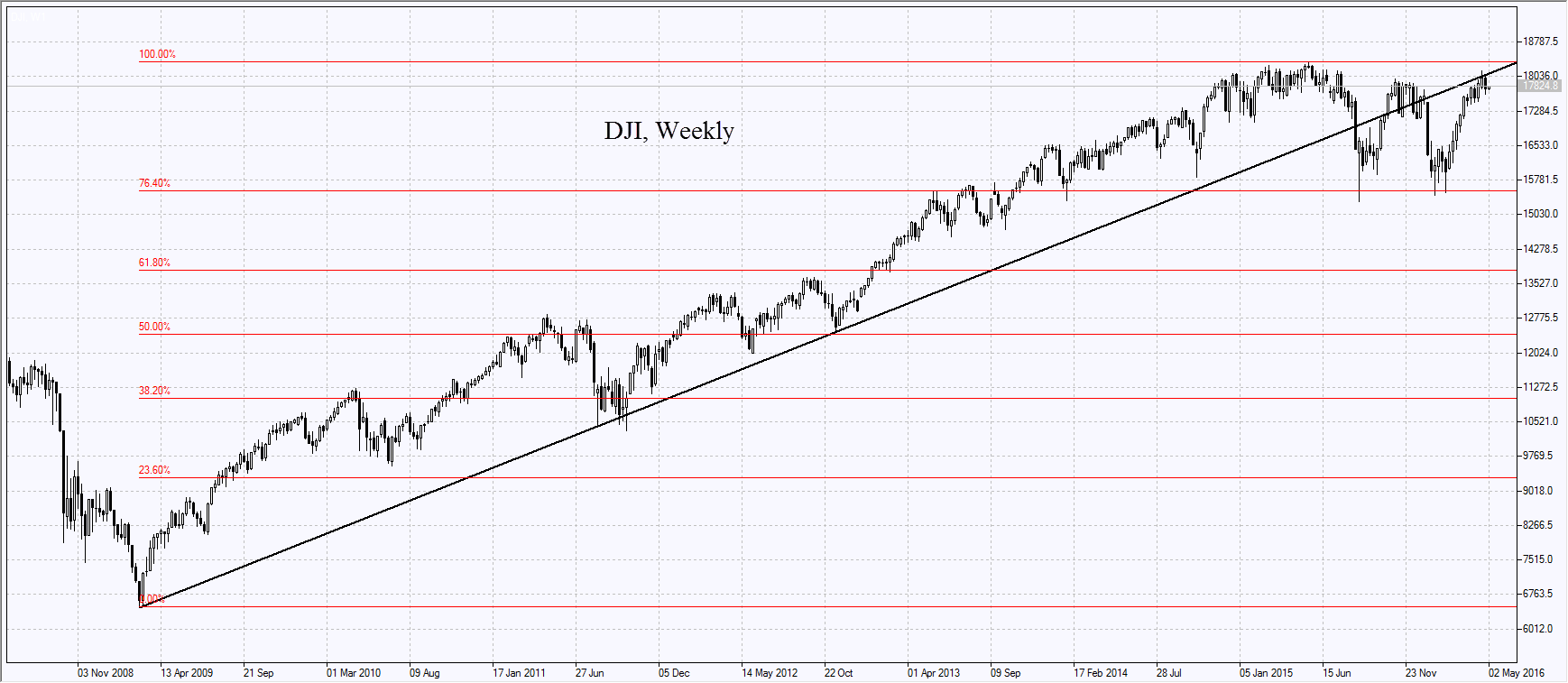

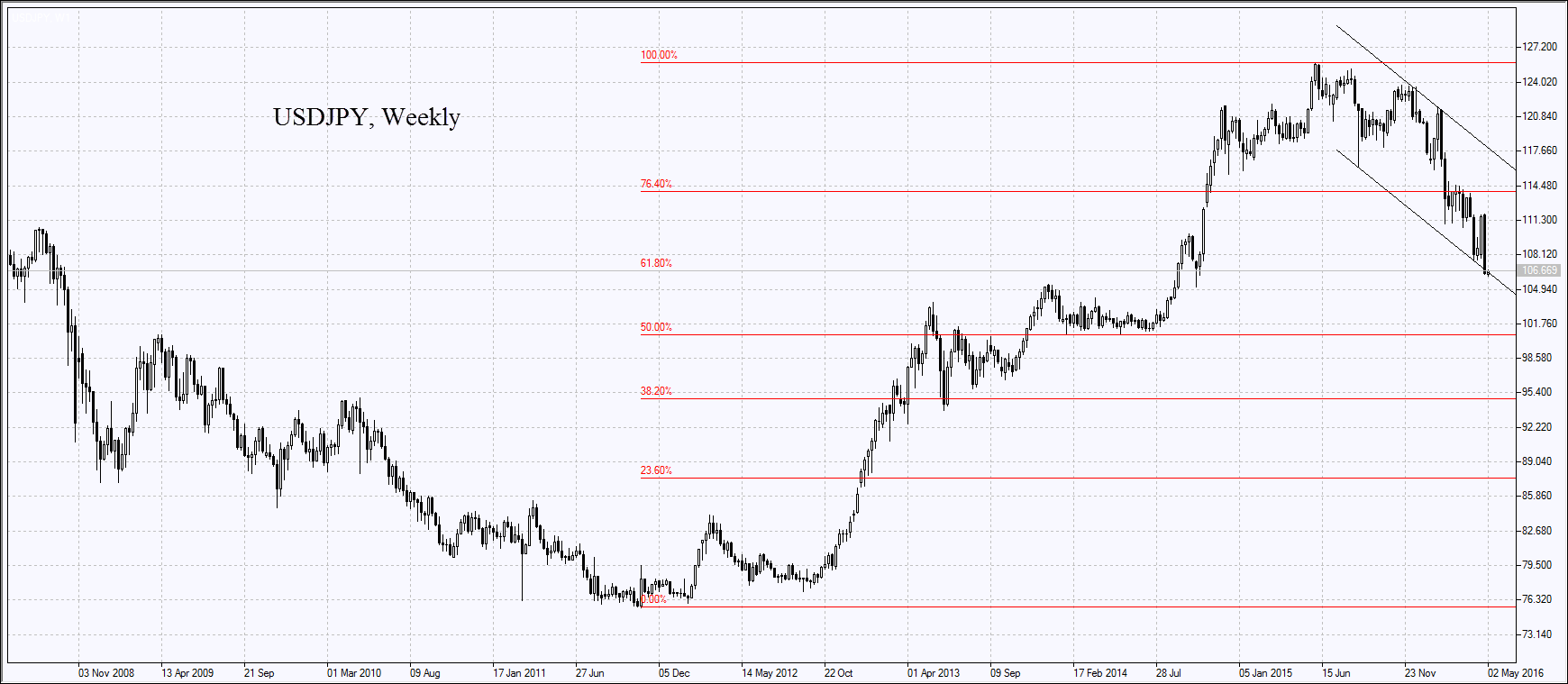

On Friday US stocks edged lower together with US dollar index on weak economic data in US and in global markets. The personal expenditures, Chicago PMI for April and consumer confidence by Michigan University were below the forecasts. AS a result, the weekly fall in Dow, S&P 500 and Nasdaq were the record high in 3 months and almost 3%. Apple stocks tumbled in week almost 12% which was their record fall since January 2013. The US currency found negative in stronger yen after the Bank of Japan introduced no additional monetary easing on its latest meeting. Investors expected the bank to cut the rates or expand monetary easing volumes. As a result, the Japanese currency showed a record weekly strengthening against the US dollar in recent 7 years reaching the 18 months (it looks as the low on the USDJPY chart). Today US dollar continues falling while US index futures are in the black as the consensus-forecast of S&P 500 total earnings fall in Q1 2106 was revised up from -7.1% to -5.9%. So far 311 from S&P 500 reported this earnings.

European stock indices are edging lower higher after their weekly fall. The Manufacturing PMI for April rose in Eurozone. In Germany it is edging up for the third month. This week 65 companies from STOXX 600 index will release their Q1 2016 earnings including such giants as Lloyds, Royal Bank of Scotland, Shell, Continental, HSBC Holdings, BMW and UBS Group. 43% of European companies reported their earnings so far. In 62% cases the earnings were above the estimates but STOXX 600 is still 6.4% below the openings of the year. Today in Great Britain are the banking holidays so the trading volume in the exchanges is low and about 60% of the recent 30 days average. Now STOXX 600 is traded the Р/Е of 15 which is 17% above the average for the recent 5 years.

Nikkei continued edging lower on Monday amid yen strengthening of 13% since the start of the year. The exporters stocks fell: Toyota Motor (-3,8%), Nissan Motor(-5%) and Honda Motor (-4%). Meanwhile, market participants expect the Bank of Japan to intervene to weaken the national currency. In such a case Nikkei is likely to correct upwards so its stocks are falling less than previous week. The slight increase in Manufacturing PMI for April also supported the stocks. On the other hand, Sony Corp stocks lost 4% and Panasonic Corp lost 7.4% on weak earnings. This week there are three holidays in Japan since Tuesday so the stock exchanges will be closed.

On Sunday the Manufacturing PMI for April came out in China being below the forecasts which limited growth of commodity futures. Chinese and Hong-Kong stock exchanges are closed on Monday due to the holiday. The commodities increase in April was at record high since 2010.

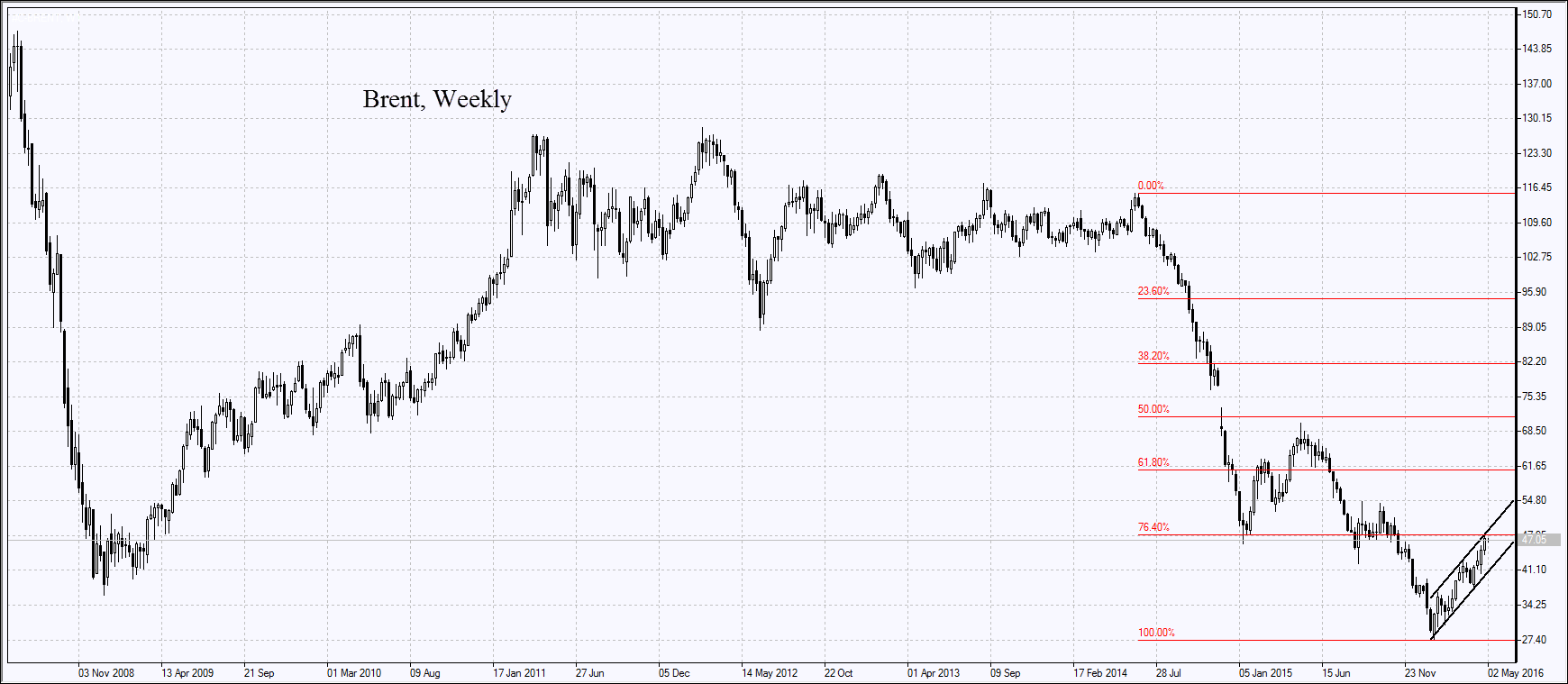

Oil prices were edging lower on Monday for the second straight day from the year-high hit on Friday. This happened on the news the OPEC production volumes came close to the historical high in April amounting to 32.64mln barrels a day.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.