By IFCMarkets

On Thursday the US stocks slumped as well as the US dollar. The S&P 500 live data show the index fell 1.4%. The main factor weighing on the markets was the ECB decision to leave the current level of the bond-buying programme at 60bn euros a month expanding the programme by six months to March 2017. Moreover, the ECB has cut the deposit rate by 10 points to -0.3%. The key rate remains unchanged at 0.05%. Investors expect these moves to support the European economy preserving the stable currency. As a result, the euro sky-rocketed and the dollar slumped subsequently. The US dollar index, a measure of the dollar value against the basket of six major currencies, fell on Thursday to the monthly low at $97.591. Thus, it lost 2.1% which is its biggest daily decline since March 2009. Even the Fed Chair Janet Yellen’s hawkish comments failed to support the US currency. Yesterday she testified in the US Congress. The increased rates may raise the credit burden of the US corporate sector and may have a negative effect on the stocks. Yesterday the sell-off was going on amid the heightened activity on the markets. The trading volume at the US exchanges was 8.2bn shares which is 20.6% higher the average for the recent 20 trading days. Today at 14.30 CET the November labour market data will come out in the US. Markets closely watch them as they are one of the key factors of the US interest rate hike. In our opinion, the preliminary outlook for the non-farm payrolls is neutral. Additional 200 thousand jobs are expected to have been created. Thus, the higher reading may lead to the positive reaction of investors while the lower reading will be seen as negative.

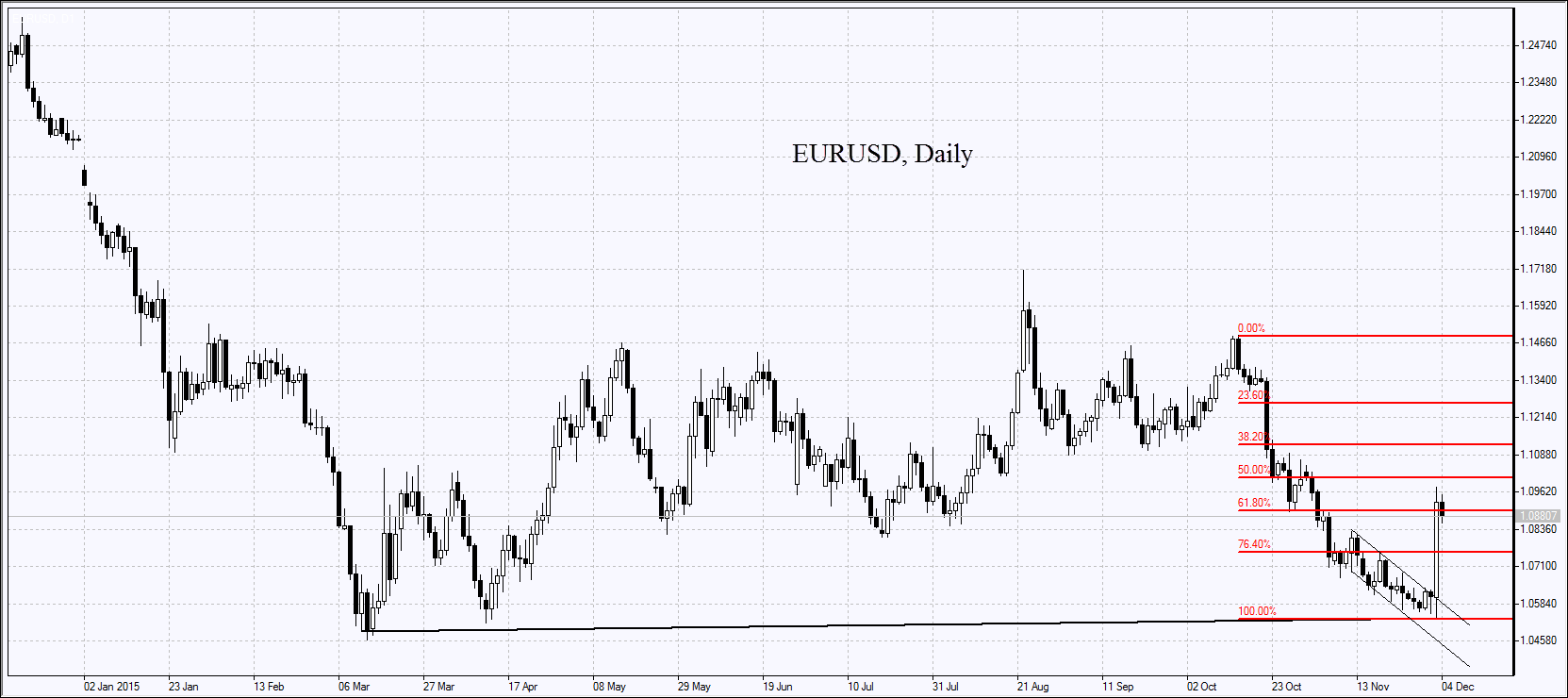

The European stocks experienced on Thursday the sharpest fall in 4 months from the 3-months highs after the ECB decisions were revealed. The EUR/USD edged up by 3.1% which is its record daily increase since March 2009. Euro slid to $1.0523 early in the day but later rebounded to $1.0981. Analysts and markets were anticipating more aggressive measures of monetary stimulus from the ECB. The base rate remained unchanged at 0.05%. As for the parameters of the QE programme, its volume was not expanded despite the expectations but Mario Draghi said it would be prolonged for six months. As a result, the markets reacted negatively on these scarce stimulating measures. The pan-European FTSEurofirst 300 fell 3.3% which is its record daily fall since late August although it reached the 3-month highs ahead of the ECB meeting. The UBS analysts believe the yesterday’s decisions left the room open for further monetary easing but state that judging by ECB actions further steps are likely only in case of extremely weak inflation or the worsened prospects of economic growth. The Euro STOXX 50 index and German DAX 30 index lost 3.6% each reacting on the surge of theEUR/USD pair. The Britain’s FTSE 100 outperformed having lost 2.3% yesterday. Today the European stock indices continue extending losses.

Nikkei fell 2.2% today to 19’504 which was its biggest daily fall since late September. Active shorts in US dollar against the euro led to the dollar losing its value against other major currencies too. For instance, the USD/JPY fell to 122.23 while the EUR/JPY edged up 2.5%. The Chinese CSI 300 lost 1.6% with yuan getting stronger against the dollar and reaching 6.39 in the spot market.

Oil edged up by around 3% yesterday as traders were hedging positions ahead of today’s OPEC meeting. On Thursday the Brent oil prices reached the $43.92 a barrel bouncing up from the 3-month low of $42.43 hit on Wednesday.

Gold edged up too by 0.8% on Thursday amid the US dollar weakening closing at $1,062.20.

Copper continues hovering around the 6-year low amid the expected interest rates hike in the US and the slowed demand for the metal from China. The three-month London copper is traded at $4,560.50 a tonne.

Market Analysis provided by IFCMarkets

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.