By IFCMarkets

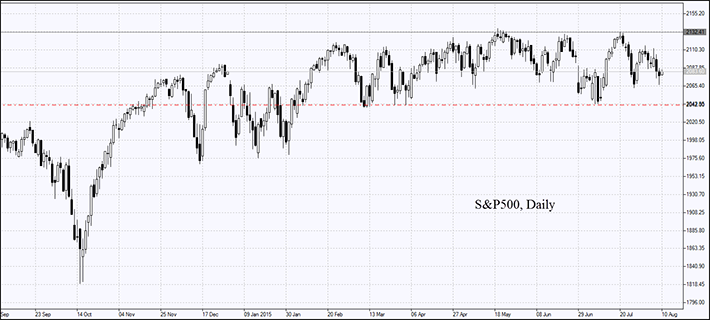

American stocks retreated on Friday, while US ICE Dollar Index edged a little bit higher as investors responded to labor market data. Unemployment remained at the 5.3% seven-year low. Non-Farm Payrolls turned out to be worse-than-expected but most market participants suppose that if new jobs total above 200 thousand, the American economy is growing. In general, judging from overnight swap quotes, the first since 2006 rate hike seems more likely. The chance Fed raises the rate at the regular meeting September, 17 increased to 52%. It is not that high so the growth in dollar price was originally restrained and then the expansion stopped. A higher rate may add to American companies’ debt burden. Consequently, this factor has a negative impact on stocks. S&P 500 lost 1.2% last week., at the moment it is traded 1% higher year to date. The aggregate P/E (share price to earnings per share) ratio is 16.6 – above the 14.7 10-year median value. To be noted, Nvidia graphic card producer shares gained 12.4% due to a good corporate report and the growing demand from expensive gaming computer builders. The American stocks trade volume on Friday was 4% below the weekly average, making 6.7bln shares. No important macroeconomic statistics are expected in the US today. A Fed representative will speak today at 15:00 CET.

European stocks have been falling 2 consequent days because of new Greek issues. Tomorrow the country may start another round of negotiations with international creditors. The Greek parliament is to adopt a new economic reformation package. Due to increased risks HSBC Holdings and Lloyds Banking Group shares dropped 1%. Industrial Prices fell 5.4% in July in China, putting additional pressure on European stocks. This has been the worst record since October, 2009. The prices have been going down 40 straight months. Investors believe that GDP growth may not reach the target 7% this year. Due to concerns about low demand for nonferrous metals BHP Billiton shares lost 2.5%. No important macroeconomic data are expected today in eurozone.

Nikkei expanded today due to good corporate reports by Yokogawa Electric (+6.3%), Nissin Foods (+5.9%) and the KDDI media company (+4.4%). The stocks were also underpinned by Current Account Balance surplus in June and strong Eco (Economy Watchers Survey) Indices of the same month. The proficit did not meet the expectations, however it is far better than the last year deficit.

Grain futures show good dynamics, reaching the 2-week high because of drought in US Middle West. We remind that US Department of Agriculture will release a report August, 12 and may cut crops forecast. In this case the uptrend may continue. Soy bean import by China in July hit the record of 9.5bln tons, which is 17.4% above the June level of 8.09bln tons.

Oil prices fell to their lowest due to weak economic data from China. However, we do not expect the quotes to slump. Oil imports by China increased 4.1% in July, while the total export contracted 8.3% indeed. US oil rigs number is growing at a slow pace and may stop if oil prices continue dropping. According to the Baker Hughes oil service company, only six rigs resumed operations last week with the overall working rigs number totaling 670. The US produces 9.5 barrels daily. As it is evident from the Commodity Futures Trading Commission (CFTC) report, hedge funds have increased the net long oil position for the first time for 7 weeks. It happened despite oil quotes have declined almost 25% for the last 6 weeks.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Market Analysis provided by IFCMarkets