By The Gold Report

Source: Michael J. Ballanger for Streetwise Reports 07/17/2018

Precious metals expert Michael Ballanger discusses movements in the base metals sector, as well as in precious metals.

met·tle [ˈmedl] NOUN

“a person’s ability to cope well with difficulties or to face a demanding situation in a spirited and resilient way.”

My beloved Fido is an awesome pet and one truly remarkable canine. Not only is he as strong as a bull, great with children, highly protective and unwaveringly obedient, he is also able to disembowel toy giraffes and imitation grizzly bears with wondrous aplomb and frightening fervor. As a particularly hectic three days had passed without the pleasure of his company, I asked my patience-of-Jobe partner where he might be hiding, given that I thought I had weaned him off the irritating habit of hiding under the tool shed every time I embark on one of my vitriolic tirades complete with soaring desk adornments and tumbling furniture. I had just completed an exceedingly unsightly excavation of the sub-toolshed cavern in search of my fine canine when I was reminded that the trusty lad went missing on July 5th, a day which saw trade war fears torpedo “all things metal” and slam energy and grains but MAGICALLY allow for sharp gains in stocks.

What happened that morning was that after the desk lamp went flying into the “wild blue,” I allegedly grabbed a family heirloom given to me by a distant American cousin and attempted to use it as a weapon. You see, my cousin barely survived the Mount St. Helens volcanic eruption that literally obliterated the mountain and everyone living on it. My cousin had sent me a memento, which was a glass ball with water and a small imitation town named St. Helens that, when you shook it, rained down volcanic ash in the same manner that those Christmas snow globes create the semblance of a snowfall. In a moment of ill-timed outrage, I imagined the “volcano globe” as a five-pin bowling ball and proceeded to hum it down the hallway at what appeared to be five decorative pink flamingos closely resembling bowling pins. At the very last moment, the flamingos revealed themselves as Fido’s legs prompting a screeching, “Fido JUMP!” Barely missing the barreling ball, Fido raced from the room and the house and, most importantly, my VILE presence, never to be heard from nor seen ever again. Meanwhile the speeding orb slammed into the door jamb and exploded into a shower of glass, water, imitation post office and general stores and a disgusting film of “real Mount St. Helens ash” all over the just-washed kitchen floor. Needless to say, I was, for the remainder of the day, persona non grata in the eyes and minds of both the canine and non-canine inhabitants of our humble abode.

Now as upset as I was at losing the volcano globe, I could not have been nearly as upset as the zinc zealots and copper cowboys that are now bleeding from the eye sockets from their unwavering and unconscionable worship of the “base metals trade” all based on inflationary expectations and global growth. What they forget is that by the time they are discussing the fundamentals for ANY trade in an internet forum, the guys that convinced you to buy (that make a living off driving volume) have sold. They are gone; they have vamoosed; they and the King have LEFT THE BUILDING. You, in your undying loyalty to the now-dated ownership rationale, are left holding a very large and very empty bag. I could cite more than a few examples of this but there is none more glaring than Noront Resources back in 2009 that was “THE NEXT COMING OF VOISEY’S BAY!!!!” I recall IBK Capital Founder Bill White holding the Jacquie McNish book on Bob Friedland and the Voisey’s Bay nickel discovery over his head urging some 200 attendees to “BUY THIS BOOK!” or miss out forever! Well, Noront is now at $0.36 after hitting an all-time high north of $7.00 in 2010.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Prominent fund managers took massive losses on Noront and then a small group of them actually removed management after the stock peaked at $7.25. It was one of the most masterful mining promotions to ever grace the hallowed halls of Bay Street, and it made a lot of the early speculators fortunes while those that continued to echo the “next Voisey’s Bay” meme were crushed. And that is exactly how the much-daunted “Trump Inflation Trade” has been replaced with the “Trump Trade War Dump” while all of the base metal bag holders continue to echo the very old and very stale “global demand/supply tightness” mantra all the way down from copper $3.30/lb to the very painful $2.76/lb. Classic

</p >

</p >

Copper is down 15.3% from $3.30/lb a month ago and sits a snick above $2.80. Zinc is down 19.49% in the same period while lead is down a paltry 11.1% over the same period. These are ONE-MONTH hits and they are wreaking havoc on managed money P&L’s “Business First!” hero, Donald J. Trump, has brought all of this on with his bellicose attitude toward literally every country on the planet. “If ya’a ain’t WIF me, ya mus’ be AGIN me!” is the mantra carried into battle by this self-proclaimed “swamp drainer” and he is certainly proving it with his anti-China bellicosity. For a man whose business endeavors have included more than his share of bankruptcy filings, DJT is playing a high stakes game of poker with the one country that holds all of the ink that winds up on the cards.

I was in a small touristy-type shop on Frying Pan Island in western Georgian Bay yesterday and there was an $80 sweatshirt with the marina’s name on it that was tagged “Made in China” that you could buy in any Dollarama for under $10. If DJT isn’t careful, the Chinese might decide to sabotage the beloved NYSE by dumping massive amounts of treasuries into an already illiquid market, triggering similar moves by overly leveraged longs in both bonds and stocks. The central bankers have had an easy time maintaining the chokehold headlock on gold and silver because they are relatively puny markets, in terms of order flow. However, when you throw base metals volatility at them as a first barrage followed by a collapsing bond market, the equity markets will be thrown about like corks in an Indian monsoon.

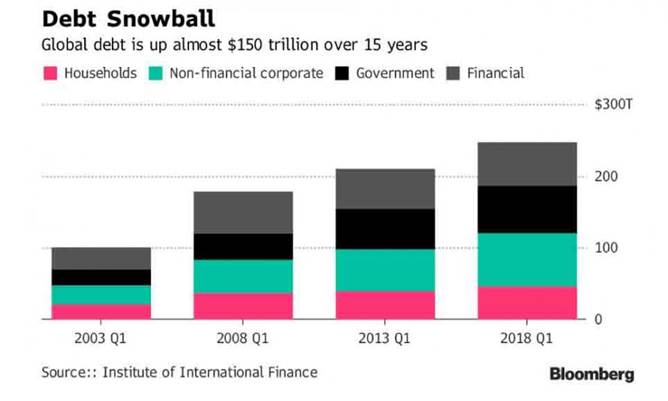

Since I began studying global debt levels back in 1972, I was consistently assuming that the constant buildup of debt and public sector entitlement would eventually result in a default reset that would repudiate paper and revalue gold on the basis of its collateralization utility. If I am Italy and I am a borrower of private capital, I must have gold to sanctify the purchasing power of the currency. If I am the United States and I need to maintain my role as provider of the global “reserve currency,” then I must demonstrate that my currency sanctifies the pricing structure for gold. The disconnect arrives courtesy of the paper markets, where derivative contracts are used as tools designed to disrupt and discourage trends that dishearten the bulls and accentuate trends that deflate the bears. This is the world in which we live today.

To say that we gold and silver investors have needed copious amounts of “ability to cope well with difficulties or to face a demanding situation in a spirited and resilient way” is at once nothing short of understatement. The conditions in the global debt arena carry hugely bullish overtones for the fundamentals for gold and silver (and the PGM complex) but those very same conditions carry ambiguous overtones for the pricing structure for gold and silver. I will explain: You cannot confuse bullish “FUNDAMENTALS” with bullish “PRICE POTENTIAL.” Global gold production has zero bearing on investment demand and global demand has zero bearing on pricing. The only thing that affects the price of the precious metals is the edicts handed down by the price managers manning the bullion bank trading desks across the globe. Period.

One glance at the chart posted above evokes a number of emotional responses: 1. Shock 2. Revulsion 3. Embarrassment and, (finally) 4. Disgust. All four responses are classified as synonymous with similar emotions seen at every market BOTTOM and I am fully aware that a great many blogsters and markets commentators are quick to point to the dreadful sentiment so prevalent out there as noted in a recent Financial Post OP-ED that said that Bay Street financings for mining-related issues was $21 million as at end-of-June 2018 versus $830 million at the same period last year. Dreadful “sentiment readings” are great attractions for those who prefer to buy cheap and await more favorable conditions in which to dump their holdings into the salivating mouths of the trend-chasing algobots, but those sentiment indicators were flashing “BUY” signals a month ago with RSI at 27 and yet prices continued to plummet. I bought a 50% position in the GLS July calls and will undoubtedly see them expire this Friday but keep in mind that my major position for 2018 is the GTSR (gold-to-silver ratio) in which I placed 70% of my trading portfolio in April at 82.70 and which now resides at 78.40. Betting that silver would outperform gold from an above-80 level seemed like a good idea back in April when everyone was strutting their stuff about a gold “breakout” at $1,375 being “imminent.” It wasn’t. I shorted gold and hedged it with an equivalent silver long position and now I am alivenot RICH, but at the very least, alive.

The number one junior exploration issue in my portfolio in terms of size and expectations in January 2017 was Canuc Resources Corp. (CDA:TSX.V)(C$0.18), which we (my friends and I) financed at $0.10 in 20152017 and then added to during the RTO at $0.25; it resides today at $0.18, which means it is modestly positive despite one horrific first-half 2018 for the vast majority of junior exploration issues. Stakeholder Gold Corp. (SRC:TSX.V)(C$0.105) has been a different story, touching a multi-year low today at $0.105 despite a superb share structure and highly prospective land positions in Canada’s Yukon Territories and the Carlin/Nevada Rift/Getchell trends. It has been agonizing trying to decide whether or not to move ahead and drill the Goldstorm project, given its proximity to Seabridge Gold Inc.’s (SEA:TSX; SA:NYSE.MKT) Snowstorm property located adjacent to and abutting Stakeholder to the northwest. However, when I spoke to Seabridge early last year, they were talking about a $25-million-plus drill program and in this putrid gold exploration market, the new plan is as such a mere $1.35 million:

Seabridge Chairman and CEO Rudi Fronk said: “Peak gold is the new reality in the gold business with reserves now being mined much faster than they are being replaced. Our industry is hungry for large discoveries and our exploration team’s success in finding gold resources over the past 15 years has been second to none. Although it has its challenges, Snowstorm is uniquely qualified to host a discovery that adds significant value for our shareholders, which is why we took it on,” said Fronk. “We are excited by the potential at Snowstorm. To have this much land in such a prospective location with this much data is a rare opportunity. Our initial focus on Getchell-style targets reflects the great value of these deposits which historically tend to be higher grade. Refining the most prospective stratigraphy with the best structural information should generate several drillable targets later this year. Although we are anxious to begin drilling, this background work needs to be completed first to give us the best chance of early success,” Fronk continued.

Stakeholder is located closer to the Midas and Hollister mines, which were indeed the initial evidence of these extremely high-grade gold mines in the vicinity of the Goldstorm property, so the dilemma that I face as an investor is this: With the enviable share structure (23 million shares issued), do I invest here to add to my holdings? If it does a $0.10 financing to adequately fund a Goldstorm exploration program, and it were to match Seabridge’s $1.35 million program, SRC would issue 10.35 million new shares with an additional 5.175 million new warrants with the new fully diluted capital at roughly 40 million shares issued (warrants but not directors’ options included). As a shareholder, I am torn between my innate optimism over the gold price outlook and the sad state of the junior exploration space as to what the correct move will be for SRC management to ponder.

If precious metals continue to decline, nothing will change investor appetites for discoveries. On the other hand, if a non-mining business venture materialized, the excellent share structure could make SRC an excellent candidate for an RTO or rebranding into a venture deemed worthy of millennial or Gen-X-er investment dollars. Bottom line: As painful as it is to watch SRC fade into these listless summer mining markets, to do anything dilutive would be madness especially if it is exploration and gold/silver-centric. I will await better markets in order to proceed.

As to the gold price, in mid-late-June I wrote that I was opening a modest 50% position in the GLD July calls as RSI (relative strength index) had dipped under 30, a level deemed oversold and from which gold had rallied on numerous occasions. Two weeks later, the RSI is back at 25.88 but gold is trading at $1,228, a solid $42 below where it was in June. The RSI readings are normally decent lead indicators for timing gold’s turning points but obviously this is one of the few times it has failed me. Mind you, if we get the seasonal strength for gold that is the JulyDecember period, being a couple of weeks early won’t be a disaster but it WILL be a disaster if I fail to add to my holdings. This is the second day of the down move for the RSI under 30 so with the current print of 25.88, there might be another day or two of weakness so I’ll buy 25% tomorrow and scale into the GLD October $120 calls starting at $1.30. October should be enough time to allow for a significant upward move and one which includes the month of September, seasonally the strongest month of the year for gold, falling into the Indian Diwali wedding season and the restocking of inventories for the Italian jewellery trade preparing for Christmas.

At the risk of resembling the hands of a broken clock and their twice-per-day accuracy record, I continue to call for a significant advance in the precious metals to kick off in this month of July. Based upon sentiment, gold stock resiliency, seasonality, and my forty-plus years as a gold investor, all of the stars are aligned for rally of majestic proportions. While I can’t yet identify the catalyst, sometimes price alone becomes the spark and with Large Specs starting to really lean on the short side, there is a lot of very dry timber awaiting that spark.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Stakeholder and Canuc. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: Stakeholder and Canuc. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Seabridge Gold. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Canuc Resources and Stakeholder Gold, companies mentioned in this article.

Charts courtesy of Michael Ballanger.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

( Companies Mentioned: CDA:TSX.V,

SRC:TSX.V,

)

![]()