Article by ForexTime

The Canadian dollar was back in focus today as the market was looking for hawkish signs from the Bank of Canada, on the back of the recent interest rate statement. The interest rate was kept at 1% however, and the market was caught off guard by the dovish comments made by the BoC. While the economy has been adding new jobs and Fridays figures were a testament to that (+441,400), the BoC is still concerned about the NAFTA negotiations that are ongoing, as well as recent housing market developments. This came as a shock for a lot of market pundits, but more important it forced forecasts further out for future rate rises, while before the market was betting heavily on the BoC to come through and cause further positive betting on rate rises.

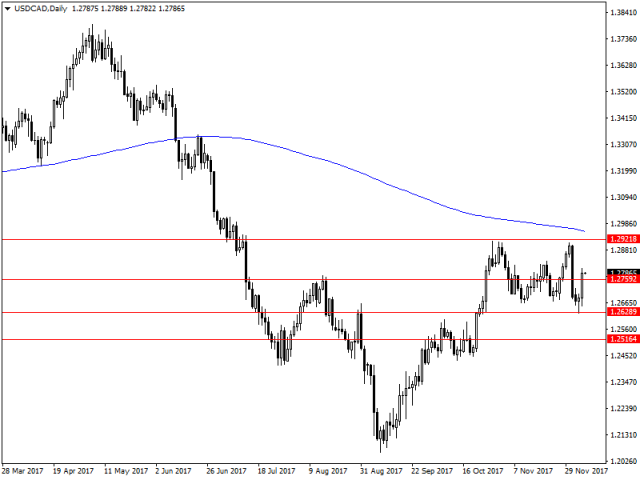

The USDCAD was quick to jump on the back of the news out from the BoC, as USD bulls rushed away with all the recent gains and pushed through resistance at 1.2759. Further levels higher can be found at 1.2921 with the potential for any higher gains to the 200 day moving average – which would be very hard to push through. If the market does turn around and head back south then support at 1.2628 and 1.2516 are likely to be the prime candidates for bearish traders, with the area between these two levels likely to act as a key selling point on the market.

Crude has been one of those funny players in the market as of late with a bullish rise, which has been purely on the back of OPEC extending production cuts. Now for many this comes as no surprise as the oil market did need to stabilise but today’s fall caught many off guard given that the drawdown came in stronger than expected at -5.61M (-2.5M exp). The reason for this was refined oil products with gasoline showing an increase to 6.8M barrels, beating market expectations and causing the oil market to sell-off. Selling pressure is common when you have a build up of refined products as the market might start to think it’s flagging or peaked already.

Oil now finds itself in a weird place at present as the recent rise has struck strong resistance at 59.08 in this market, and the fall today hit the current old trend line which the market is respecting before taking a pause and stopping all together. I’m not sure if there is further potential falls on the cards given the bulls have been so strong, and this could be an excuse to unwind. However, if the trend line did break then support could be found at 55.14. If oil does indeed jump back higher, then for me resistance at 57.38 and 59.08 are the key levels traders will look to target. Expectations are though that 59.08 will be the level to beat currently.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]()

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com