By IFCMarkets

Nasdaq ends at all time high

US major stock indices rebounded on Thursday on upbeat earnings reports as the House passed the Republican tax cut plan. The dollar weakened marginally: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, ended little changed at 93.899. Dow Jones industrial average rose 0.8% to 23458.36, buoyed by steep gains in Cisco and Wal-Mart shares on stronger than expected earnings. TheS&P 500 gained 0.8% to 2585.64 led by telecom and consumer staples stocks. The Nasdaq composite index jumped 1.3% to a record high 6793.29.

Treasury yields rose after House approval of Republicans’ tax plan proposing a cut in corporate rate to 20% from 35% and a repeal of the estate tax. While this brings the bill one step closer to final approval in the Senate the final version will most likely be much different since the Senate Finance Committee’s tax overhaul version differed in many areas. Economic data were positive: industrial production climbed 0.9% in October, above a 0.6% forecasted gain. In the same month, import prices rose 0.2%. On the negative side initial jobless claims rose by 10000 to six week high 249000.

European stocks recover on positive earnings updates

European stocks recovered on Thursday on positive earnings updates. The euro ended little changed while the British Pound climbed against the dollar on positive October retail sales report. The Stoxx Europe 600 index rose 0.8%. Germany’s DAX 30 gained 0.6% to 13047.22. France’s CAC 40 rose 0.7% lower and UK’s FTSE 100 added 0.2% to 7386.94. Indices opened mixed today.

Auto maker shares rose after new car sales in the EU grew strongly in October after a dip in September. The Stoxx Europe Automobiles & Parts Index gained 0.8%. Pound strengthened after above-expected 0.3% over month rise in October retail sales. In other economic news, euro-zone inflation was confirmed at 1.4% in October, after 1.5% gain in September.

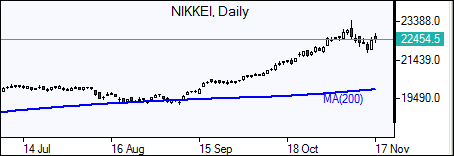

Asian markets up

Asian stock indices are mostly higher today as market sentiment was buoyed by recovery on Wall Street overnight.Nikkei rose 0.2% to 22396.80 capped by renewed yen strength against the dollar. Chinese stocks are mixed after the central bank of China injected more money into the financial system following recent soft data: the Shanghai Composite Index is 0.5% lower while Hong Kong’s Hang Seng Index is up 0.7%. Australia’s All Ordinaries Index is up 0.2% despite weaker Australian dollar against the greenback.

Oil lower

Oil futures prices are edging lower today on rising US output concerns as shale oil production increases on higher price incentives. Prices rose yesterday following a surprise build in US crude supplies and increase in domestic production to a record weekly level. Brent for January settlement fell 0.8% to end the session at $61.36 a barrel on Thursday.

Market Analysis provided by IFCMarkets

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.