By The Gold Report

Source: Peter Epstein for Streetwise Reports 05/07/2020

Peter Epstein of Epstein Research looks into the Gross Overriding Royalty that just changed hands on the company’s flagship Red Hill project, and discusses what it means for the firm.

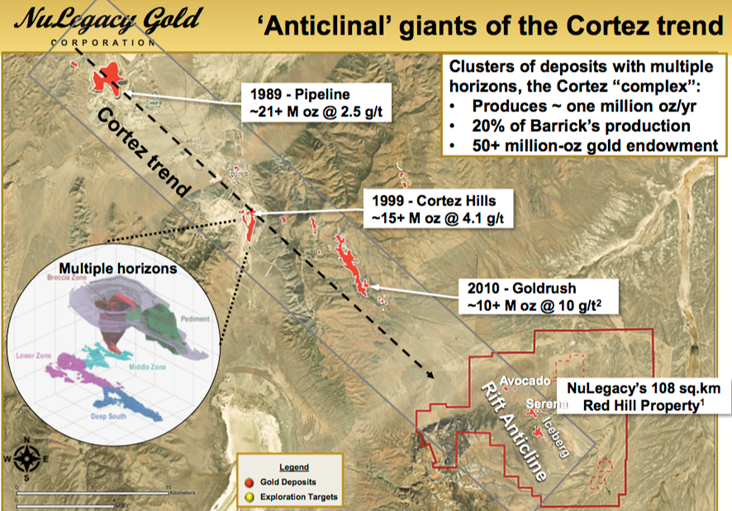

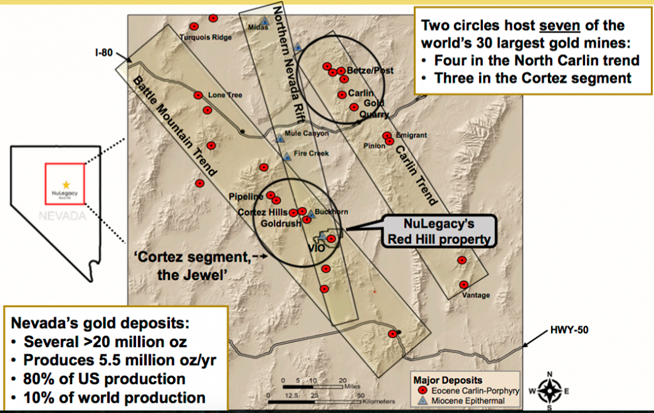

In late April, Metalla Royalty & Streaming acquired two royalties, one of which was a Gross Overriding Royalty (GOR) on NuLegacy Gold Corporation (NUG:TSX.V; NULGF:OTCQX) flagship Red Hill project, a Carlin-style deposit in Nevada’s world-famous Cortez trend.

To be clear, this was a transaction between Metalla and a private company; no cash or other remuneration flowed to NuLegacy. However, this news is still exciting and thought provoking as it pertains to a potential (implied) valuation of Red Hill. So much so, thatCEO/director of Finance and MarketingAlbert Matter put out this press release highlighting it. {corporate presentation}

Metalla’s news is applicable to NuLegacy for a number of reasons. Let me start by saying I know the Metalla team, I’ve written about the company several times (although not recently).

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

This is a smart, hard-working, market-savvy group, with global experience, integrity and expertise. When dealing in streams and royalties, it’s all about industry connections, market knowledge and deal flow. Metalla has that and is up to its eyeballs in deal flow (deals it can make or pass on).

Takeaways on implied valuation of NuLegacy’s Red Hill project?

That’s why this news is so interesting. It represents a reliable, unbiased vote of confidence in NuLegacy’s Red Hill project. I was able to track down the president, CEO and a director of Metalla, Mr. Brett Heath, to ask him about his team’s view of NuLegacy, their management and technical teams, and the Red Hill project,

“The Red Hill project is very interesting due to its location & position within the Cortez trend of Nevada that hosts globally significant mines & projects, specifically Cortez Hills, Pipeline & Goldrush. Although many near-surface deposits have been discovered, several blind deposits similar to Goldrush have yet to be found.

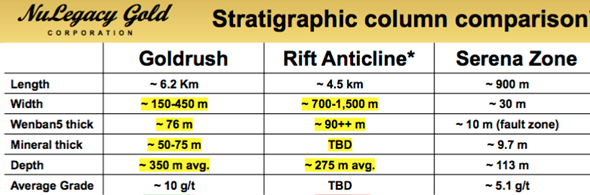

“NuLegacy’s Rift Anticline is a promising new drill target, a chance to discover a large, high-grade deposit. The close proximity of Red Hill to Goldrush heavily influenced our understanding of the geology at Red Hill. Specifically, it allowed us to better understand that the Rift Anticline has similar stratigraphy to Goldrush, and similar mineralization events nearby.”

Investors, shareholders and analysts are trying to figure out what (if any) read-throughs there are in terms of the valuation of the Red Hill project.

From the press release:

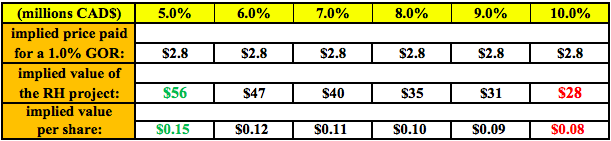

“Valuing Gross Overriding Royalties (“GORs”) is a complicated business made easier in this instance by the straightforward nature of the [transaction] . prorating the US$4 million purchase price for the total of 2% GOR that was acquired . values a 1% GOR in the Red Hill project at ~US$2 million.”

What this valuation exercise boils down to is how does the value of a 1% GOR compare to a conventional working interest in the same project? GORs are highly case specific, so I will give a range of possibilities. Many factors make GORs unique, but a rule of thumb is that a 1% GOR equates to a 5% working interest.

However, due to the unknown terms of this particular GOR, let’s assume that the 1% GOR is equal to between a 5% and 10% working interest. By extending the range higher than 5%, more conservative valuations for Red Hull are obtained. In the chart below one can see that the implied ~US$2 million paid for a 1% GOR equals C$2.8 million at the current exchange rate.

Therefore, Red Hill’s indicative valuation could be viewed as C$28 million to C$56 million, or C$0.08 to C$0.15 per share. Currently, the stock’s trading at C$0.07. The company has a cash balance of C$4.5 million. {see corporate presentation}. I believe the C$0.08 to C$0.15/share range is conservative because Metalla’s purchase of the GOR had a built-in profit expectation. The true ascribed value of a 1% GOR on the Red Hill project might be higher than C$2.8 million.

A true vote of confidence in NuLegacy Gold

Perhaps more important than an implied (subjective) valuation of Red Hill are the following takeaways. First, Metalla not only likes Red Hill, it must also feel good about the long-term prospects for Nevada and the U.S. Metalla looks at hundreds of deals a year from all over the world. Management can, and does, invest in dozens of jurisdictions.

Yet, in April 2020, it chose the U.S., . Nevada . the Cortez Trend . Second, it chose a project that’s pre-maiden resource. Remember, Metalla has paid out ~C$2.8 million, but doesn’t make a penny of that back unless it re-sells some or all of the GOR it acquired, or Red Hill reaches commercial production. Therefore, I argue that investing at this relatively early stage is a stamp of approval in the extensive work done to date at Red Hill.

That Metalla chose to deploy capital in a gold asset rather than a silver asset, despite the gold-silver ratio being near an all-time high (over 110 to 1) seems promising. Finally, it chose the U.S. at a time when the currencies of Mexico, Australia, Canada and others have weakened considerably vs. the U.S. dollar, making exploration cheaper in those countries. One must have conviction to choose Red Hill over dozens of public and private, pre-maiden resource, projects around the globe.

In the end, a good project in a great jurisdiction is only as prospective as its technical/management teams. NuLegacy has prudently advanced Red Hill in good times and bad. For most of NuLegacy’s existence, the gold price traded between about $1,050 and $1,400/oz.

Gold price at $1,730/oz. is a game-changer .

Now gold is hovering around $1,730/oz after almost touching $1,800/oz in March. This is a game-changer for juniors like NuLegacy that have tremendous blue-sky potential, (look at neighboring mines and development projects, some of the best on the planet) but like most juniors, have limited funding to conduct aggressive drill programs in a strong gold price environment.

A savvy company betting on the Red Hill project is yet another indication that the time has come for precious metal players to become more active in M&A.

The day that Barrick commits its deep experience (and deep pockets!) to NuLegacy’s Red Hill, all royalties held on that project would soar in value. Why? The timeline to potential production would be shortened, perhaps by years, (more drilling, less investor hand holding, perhaps skipping a PEA or a PFS). The scope of the project would become largermore drilling across a wider footprint (a 108 sq. km land package).

The value of the royalties could double, triple, quadruple . who knows? The share price at which NuLegacy gets taken out could also be meaningfully stronger. After all the company has been through, I don’t think the Board would sell the company below C$0.30/share. At least not with the gold price at $1,730/oz (or higher). Readers are reminded that C$1.5 billon OceanaGold Corp. & giant natural resources fund Tocqueville own a combined 21.5% of the company.

Might there be a bidding war for NuLegacy?

In a best case example then, there could be multiple bidders for NuLegacy. This is not nearly as crazy as it sounds, especially if the gold price keeps going up, or if the next (fully funded) drill program hits the mark. If Barrick were to make a move, OceanaGold, Newmont, or even Tocqueville (they could hold out for higher price) might have something to say about it.

Those entities, and/or other mid-tiers/majors in Nevada or around the world would keep Barrick honest. Over the years NuLegacy has been in touch with several well-known names, but I never know who they’re talking with at any given time. Make no mistake, Barrick is best positioned by virtue of having the most synergies with Red Hill, so it can afford to pay several more pennies per share if need be. That’s how a share price of C$0.30+ becomes possible.

Bottom line, NuLegacy Gold (TSX-V: NUG) / (OTCQX: NULGF) is a high-risk exploration play, but I believe a good speculation. There’s no better time to be buying high-risk exploration than when the prices of the metals being explored for are moving up.

As more attention is drawn to NuLegacy, its team, the undisputed safety of Nevada, the prolific nature of the Cortez Trend, etc., I think there’s compelling relative and absolute value here that readers should consider investigating further.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about NuLegacy Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of NuLegacy Gold are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, NuLegacy Gold was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein’s disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Metalla Royalty & Streaming and Newmont Goldcorp, companies mentioned in this article.

Graphics provided by the author.

( Companies Mentioned: NUG:TSX.V; NULGF:OTCQX,

)

![]()