Frank Holmes: Finding Winners in the Wreckage of the Economic Downturn

By The Gold Report

Source: Streetwise Reports 05/07/2020

While the broader markets have seen sharp declines, Frank Holmes, CEO and chief investment officer of U.S. Global Investors, homes in on gold, gold stocks and bitcoin, and gives his prognosis for the airlines.

Streetwise Reports: Let’s start with gold, which has seen an impressive rise in the last few months as the broader markets have declined on the back of the coronavirus pandemic. What do you think is ahead for the metal?

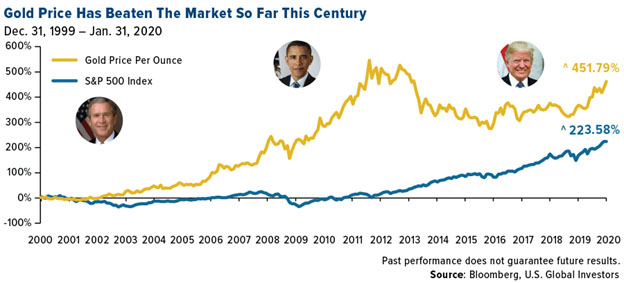

Frank Holmes: There is a short-term view and a long-term view. What’s really hard for so many investors and asset allocators to recognize is that gold bullion since 2000 has far outperformed the S&P 500. In fact, of the last 20 years, in 16 of those years gold has been positive. So if we look at the numbers, it’s double what the S&P 500 has done for the past 20 years.

With gold, there’s the fear trade and the love trade. The love trade is 60% of the demand and it is long-term demand. The fear trade is short-term demand, and it’s about 40%. Right now, we’re living with fear that’s really dominating the markets. The two factors that go with that are negative real interest rates and the amount of debt being printed by the government. So whenever you have the combination of a rising Fed balance sheet with Quantitative Easing 1, 2 and 3, buying junk bonds, whatever they’re doing in the stock markets to try and provide liquidity, as that flows dramatically so does the price of gold.

Free Reports:

Typically and most significant, in every country in the world we have found that when you have negative real interest rates, gold goes up in that country’s currency. Take the yield on 10-year government bonds and subtract the monthly Consumer Price Index (CPI) number; if it’s a positive return, gold is not attractive as an asset class. But if it’s a negative real rate of return, gold appreciates in that country’s currency.

When gold went to $1,900 in September of 2011, the 10-year government bond had a negative real rate of return of -300 basis points. Then five years later, the price of gold went down to $1,100 and real interest rates were +2% over the CPI number. So you had a variant swing from -3 to +2, which is 500 basis, and that’s why gold corrected. Since then, we’ve had these periods now, and particularly in the past year, of negative real interest rates in America. That’s how gold started staging a rally, which started about this time last year, peaked in August, sold off and now it’s coming back again.

The Federal Reserve said recently it’s going to keep rates basically at 0. The CPI is still running more than 1%. In fact, we could get big food inflation, the way it looks, for beef, chicken, etc. Inflation could have a big impact on negative real interest rates, and gold is moving higher.

So short term, it’s all about real negative interest rates. As long as they stay negative, then we’re going to see gold go up in the U.S. dollar. It could go up against the euro, against any country’s currency.

I mentioned earlier that 60% of gold demand is love, and it predominantly comes from China and India. China and India are 40% of the world’s population, and if you throw in the Middle East and Southeast Asia, we’re now talking about 50% of the world’s population. They give gold for weddings and for birthdays, and there’s a strong correlation of rising gross domestic product (GDP) per capita in those countries for the past 20 years, and rising gold consumption.

China and India comprise approximately 50% of the world’s gold demand GDP per capita. Indian women wear six times the amount of gold on their bodies than what is in Fort Knox, and they predominantly wear 24 karat, minimum 22 karat, gold jewelry. It’s protected them from bad governments and bad government policies.

SR: What do you see happening with silver?

FH: Silver has more industrial applications than gold, so silver is like a warrant on gold. If a stock takes off and there’s an option or a warrant in the money, it explodes and goes up much more percentage-wise. It has greater volatility. Every 10% move in gold usually translates to a 15% move in silver, up or down. And with this fear that’s been taking place with negative interest rates and the calamity of money printing around the world, what we see now is that silver didn’t move at first. Silver has always lagged.

SR: Do you recommend that the individual investor hold gold bullion?

FH: Yes. I think the easiest way is the SPDR Gold Trust (GLD). Or if you want to buy the physical gold insured, go to a reliable site like Kitco, and you can take physical delivery.

There is a company called Mene Inc. (MENE:TSX.V; MENEF:OTCMKTS) at mene.com. It sells 24-karat gold jewelry with only a 10% markup. And it will buy back your gold jewelry at a 10% discount to the price of gold if you ever want to sell it back. That’s the business model. It will deliver throughout the U.S., I think using Brinks for delivery of simple gold jewelry.

SR: Let’s talk about bitcoin for a moment and how that fits into a portfolio.

FH: I am the chairman of HIVE Blockchain, which became the first real cryptomining company. We are mining using green energy, surplus energy in Iceland, Sweden and now Quebec, which sells electricity to New York state. Quebec has a surplus of it. So we started mining these coins.

What I found is that the Bitcoin is very different than Ethereum. Bitcoin is going to become, to me, like Andy Warhol’s art. If you look at the original paintings of Marilyn Monroe or Elvis Presley, when he came out with his prints in different colors, they came out at $1,000, went up to $10,000, fell, went up to $50,000, fell, went up to $100,000 and went to $125,000because there are just more people, widened GDP, over time, and then they become art collectors. I think that if you have an original Bitcoin that’s never been traded, it’s going to be in that space.

The other part is that cryptocurrency is very new, and digital money is going to only grow. Blockchain technology is a superior piece of technology. What we saw was that Bitcoin bottomed a little over a year ago. Then it rallied, it went up to $14,000. All the central banks got worried. They knocked it down, and it’s making a comeback.

Bitcoin, in mid-May, is going to halve production. There’s a limited number of Bitcoins allowed to be ever created. The methodology when you mine them is you get new Bitcoins. They’re called genesis or virgin coins. The number of coins you get every time you mine is going to halve. So the supply is going to shrink dramatically. A thought process with that is that Bitcoin will trade higher, probably above $10,000. Bitcoin is very speculative, just like buying Andy Warhol’s art early.

I think that anyone who looks at Bitcoin or Ethereum must recognize that the daily volatility is four times the S&P 500 and gold. Thirty percent of the time gold or the S&P can go up or down 1%. For Bitcoin and Ethereum, it’s 45%. Cryptocurrency is a huge secular trend, but it’s going to be volatile.

SR: How do you feel about gold stocks? Are you looking at seniors or juniors or both? What should investors be looking at?

FH: For the first time in a long time, I’m becoming very bullish on gold stocks. I’ve been very negative on gold mining companies for over a decade now, for raising capital and actually destroying value per share. But over the decade, new boards of directors and new chief executive officers have come on, and there’s become a greater discipline on cash flow returns rather than on cash flow, revenue per share growth, cash flow per share growth, rising dividends, all the normal things you buy a Starbucks or any great company for. It’s the capacity to have revenue growth. Mining companies did a lot of silly mergers and acquisitions work, with which they destroyed capital, but that has changed.

During this past decade I’ve been a big advocate of royalty companies, such as Franco-Nevada Corp. (FNV:TSX; FNV:NYSE), Wheaton Precious Metals Corp. (WPM:TSX; WPM:NYSE), Royal Gold Inc. (RGLD:NASDAQ; RGL:TSX). These three had the highest revenue per employee in the world.

Franco-Nevada has a royalty on Newmont Goldcorp Corp. (NEM:NYSE) and Barrick Gold Corp.’s (ABX:TSX; GOLD:NYSE) joint venture assets in Nevada. The revenue per employee at Franco-Nevada is over $20 million. For Barrick or Newmont, it’s $500,000 of revenue per employee. Goldman Sachs has $1 million of revenue per employee. So these royalty firms are very efficient companies. If you look at the past decade, Franco-Nevada has far outperformed Berkshire Hathaway. It has far outperformed any gold stock. It’s because it’s showing revenue per share growth, cash flow per share growth, over the rolling one year over three years on a consistent basis.

What’s now happening is we have new management for these other gold stocks. The big move in gold stocks occurs when the generalists start to buy the sector. They’ve not been owning the underweight gold stocks because of the bad discipline by management and boards or silly acquisitions. Now what we’re seeing, for the past three years, through the end of March, we’re going to see the one year revenue growth over two years strong. Now you get 36 months of a strong growth in revenue and cash flow from the industry, and all of a sudden, generalists show up. When you start seeing more and more of the stocks in that industry showing free cash flow, the generalists start to show up.

The coronavirus this past quarter hurt the S&P 1500 stocks because the majority of them had free cash flow yields of about 4%, and they got evaporated, obliterated, because of this global shutdown. But the gold stocks didn’t. They actually have rising free cash flow. They’re going to show this quarter the price of gold is up, some of them had shut-ins for very temporary periods of time but their revenue, their cash flow, as a whole is going to truly outshine the overall industry. And when the quants and the fundamentalists start looking at where their growth is, these stocks are going to show up.

I did an analysis of only looking at free cash flow and picked the 10 gold stocks every quarter that had the highest free cash flow yield. And I sold them and bought them every quarter. I far outperformed any gold index. So that discipline shows up as a key metric to attract the quant fund or the generalist. When I look at my datathe two-year number is so importantI’m becoming very bullish on gold stocks.

When we talk about the names, my bias is U.S. Global GO GOLD and Precious Metal Miners ETF (GOAU). I launched this several years ago as a smart quant approach to picking gold stocks. It has three royalty companies that we talked about, Franco-Nevada, Wheaton Precious and Royal Gold. They’re 30% of that ETF. They rebalance every quarter.

Then all the other names, they go down to a $200 million market cap but they have to be able to show the highest cash flow returns on invested capital. Once they do something silly or stupid, they’re thrown out. Back testing, that model has outperformed the VanEck Vectors Gold Miners ETF (GDX) and the VanEck Vectors Junior Gold Miners ETF (GDXJ) just on a basket of 60 gold stocks. This only has 28 names. Since I launched it, it’s far outperformed on a rolling 12-month basis. It’s smart data, and it dynamically recalibrates every quarter.

If you want to buy the individual names, then I would focus on those three big royalty companies. Thereafter, I would focus on those companies that have this metric I talk about, free cash flow yields. Out of the 100 gold stocks in the world that we follow, there are only about 14 of them that really have attractive free cash flow yields. What’s interesting is that Barrick and Newmontand Newmont’s part of the S&P 500does have a free cash flow yield that is positive, so you’re seeing it has really done exceptionally well this past quarter because it has an attractive free cash flow yield and has not been hurt by the coronavirus.

SR: Let’s switch gears for a moment. U.S. Global Funds runs the Jets ETF, an airline ETF. Obviously, the airlines have been battered. Do you see them coming back? Do you see bankruptcies?

FH: I think that the government agencies and the politicians have learned a lot from two big corrections: the 9/11 correction and 20082009. When you look at this industry, the Federal Aviation Administration says that 1 in 15 people is associated with the airline industry. That’s huge. When you look at the multiplying effect of the airline industry, it’s massive, just as housing is. One dollar for housing is worth $16 approximately. So when it comes to airlines, we’re talking a double digit number of multiplying effect.

What’s happened is that the government has been very smart this time to say we must make sure that we don’t unwind this industry as we’ve done in previous times. So I think there’s going to be a faster turnaround from the bailout policies.

What’s happened with the airlines is they have ancillary revenue that has been very significant in the past five years. Some $20 billion of revenue then went to $100 billion of revenue, which covers a lot of costs. It aggravates you and me when we fly: change fees, baggage fees, but all these fees have let the airlines not be victimized by the price of oil because every time the price of oil went up, airline stocks fell. Every time oil went down, airlines went up. It was this inverse relationship that took place. Oil has represented less and less of ancillary fees. Now what’s happened on this correction is not only the ancillary fees and everything have fallen, but oil has crashed. So airlines’ biggest cost is way, way down. That means when they turn, and they come out of this correction, they have huge upside. Not only do they have the support of the government, they have the ability to start adding on these fees.

Because of the bailouts, airlines are not going to be able to buy back their stocks and they’re not going to be increasing their dividends in this process. But that doesn’t matter. Their revenue capacity per share is explosive. So I think that that’s a very big difference.

SR: Anything else that you would like to talk to our readers about in this period of extreme volatility and uncertainty?

FH: Yes, bad news is good news. There’s the optimism of trying to find who’s going to be the solution to the problem. Had the U.S. Food and Drug Administration and the Centers for Disease Control and Prevention used Google and Amazon technology, they probably could’ve adapted faster to this coronavirus. Amazon hired 100,000 people. It’s amazing that in all that negative news, it adapted the fastest. It’s trying to understand how capital markets morph. There are certain industry leaders. I love Clorox. I don’t think that stock is going to be given away. I think it’s one of those just steady dividend payer and growing dividend stocks. So it’s in the negative news where you can find opportunities besides airlines, besides gold. You can turn around and find these other pockets.

SR: Thank you, Frank. I appreciate your time today.

Frank Holmes is CEO and chief investment officer at U.S. Global Investors, which manages a diversified family of funds specializing in natural resources, emerging markets and gold and precious metals. In 2016, Holmes and portfolio manager Ralph Aldis received the award for Best Americas Based Fund Manager from the Mining Journal. In 2011 Holmes was named a U.S. Metals and Mining “TopGun” by Brendan Wood International, and in 2006, he was selected mining fund manager of the year by the Mining Journal. He is also the co-author of The Goldwatcher: Demystifying Gold Investing. More than 30,000 subscribers follow his weekly commentary in the award-winning Investor Alert newsletter, which is read in over 180 countries. Holmes is a much sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg, BNN and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications.

Disclosure:

1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or members of her immediate household or family own, shares of the following companies mentioned in this article: None. She is, or members of her immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this interview are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Frank Holmes: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: N/A. I, or members of my immediate household or family, are paid by the following companies mentioned in this article: HIVE Blockchain Technologies. My company has a financial relationship with the following companies mentioned in this interview: N/A. Funds controlled by U.S. Global Investors hold securities of the following companies mentioned in this article: Mene Inc., Franco-Nevada Corp., Royal Gold Inc., Wheaton Precious Metals, Newmont Mining, Barrick Gold Corp. I determined which companies would be included in this article based on my research and understanding of the sector. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Franco-Nevada and Newmont Goldcorp, companies mentioned in this article.

( Companies Mentioned: FNV:TSX; FNV:NYSE,

MENE:TSX.V; MENEF:OTCMKTS,

RGLD:NASDAQ; RGL:TSX,

WPM:TSX; WPM:NYSE,

)