The Energy Report

Source: The Critical Investor for Streetwise Reports 11/10/2019

The Critical Investor looks into the uranium explorer’s work in Argentina and the political situation in the country with the recent election of a new president.

1. Introduction

It has been a quiet year so far for Blue Sky Uranium Corp. (BSK:TSX.V; BKUCF:OTC), as the uranium oxide spot prices dropped off again after a run-up in H2 2018, rising almost 50%, only to pull back another 20% or so from these heights as can be seen at this chart, which can be found on the website of Cameco:

Nonetheless, as one of the premier low cost development plays in the uranium space, Blue Sky managed to continue working on its Amarillo Grande project in the Rio Negro province in Argentina, and recently raised fresh cash. This time it managed to get C$0.87M from the markets, earlier in July it closed a C$0.68M private placement. This is impressive, as uranium sentiment is not positive, and investors are not sure what to think of the newly elected president Fernandez in Argentina. He isn’t all that bad according to various sources, more on this later.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

As most exploration and drilling is very near surface, these new funds enable Blue Sky to continue working on its flagship Ivana project, which in turn could likely improve economics further. As a reminder, at a relatively (industry wide) low base case uranium oxide (U3O8) price of US$50/lb U3O8, the after-tax NPV8 is US$135.2 million and the IRR is 29.3%. These are very decent numbers as most competitors use US$6065/lb U3O8 for their base cases. Initial capex is US$128.05 million, and the all-in sustaining costs (AISC) net of vanadium credits is US18.27/lb U3O8. This AISC is amongst the lowest in the industry. However, keep in mind that the entire project is not economic at this time as the long term (or also called contract) uranium oxide price is US$32/lb U3O8, as is any project worldwide except the ISR operations in Kazakhstan and Arrow of NexGen Energy, but it sits at the front of low cost projects and operations, and as such might be one of the uranium projects with the biggest leverage to the uranium price. Let’s have a look at the current state of affairs for Blue Sky Uranium.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. Financings

As mentioned, the company recently closed a private placement (PP), to be precise on October 23. Blue Sky raised aggregate gross proceeds of $868,999.95 through the non-brokered private placement, by the issuance of 5,793,333 units at a subscription price of $0.15 per unit. Each unit consisted of one common share and one transferrable common share purchase warrant. Each warrant will entitle the holder thereof to purchase one additional common share at $0.25 per share for two years from the date of issue.

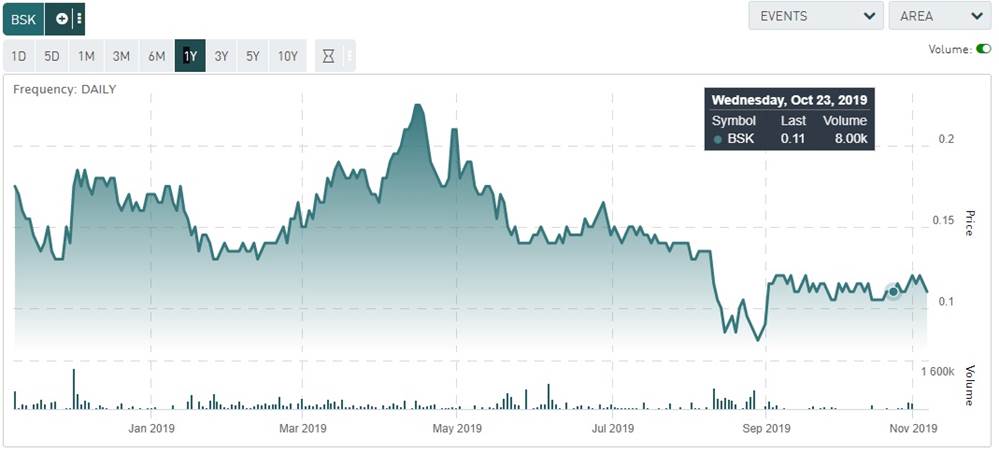

I always like a non-brokered PP, as in this case management didn’t have to use the brokers, which in turn not always mobilize the most committed shareholders. Usually management taps into its own group of personally known investors, which almost guarantees longer term holders, and no warrant flippers. The subscription price of C$0.15 is also a decent premium compared to the closing price of C$0.11 that day:

Share price; 1 year time frame

I could say something about the full warrant as existing shareholders probably preferred to see a half warrant or no warrant at all, but we have to be realistic here; Blue Sky did well at such a premium at this subdued sentiment. At least the warrant period is limited to two years, but there was no accelerated expiry clause for the warrants, as we will see at the July private placement which comes up next. The proceeds of the financing will be used for exploration programs on the projects in Argentina and for general working capital. This financing is subject to regulatory approval, and keep in mind that there is a four month hold period expiring on February 23, 2020.

So far about the October financing, Blue Sky Uranium also did a raise in July as mentioned. In this, again, non-brokered private placement, 4,528,182 units at C$0.15 were issued in two tranches, and aggregate gross proceeds of $679,227 were received by the company. Each unit consisted of one common share and again one full warrant. Each warrant will entitle the holder thereof to purchase one additional common share at $0.25 per share for three years from the date of issue. So far this is in line with the latest financing, although the exercise period is one year longer which is good.

Another addition neutralizing this is the accelerated expiry of the warrants. If the volume weighted average price for the company’s shares is $0.50 or greater for a period of five consecutive trading days, then the company may deliver a notice to the warrant holder that the warrants must be exercised within twenty days from the date of delivery of such notice, otherwise the warrants will expire at 4:30 p.m. (Vancouver time) on the twenty-first day after the date of delivery of the notice.

As can be seen in the price chart above, this round was done at no premium, full warrant, three year warrant exercise period combined with an accelerated expiry at C$0.50. I am not a fan of accelerated expiries, especially in juniors and even more especially in uranium juniors, as the upside potential is truly explosive as we have seen during other spikes in the uranium price, and this is the reason most investors are willing to invest in uranium in the first place in my view. Notwithstanding this, Blue Sky did well to raise this in a very difficult market at no discount, so it could continue with its exploration program for 2019, consisting of IP surveys and auger drilling. Blue Sky expects to have sufficient funds to last well into Q2 2020, but expects to raise more in order to fund RC drilling in 2020. But before I delve into exploration, let’s rehash developments for uranium itself.

3. Uranium

I’m not going to repeat the entire paragraph from my first article on Blue Sky Uranium, but will mention and update the most important items. Consensus is nowadays, that necessary pricing to bring a lot of Western production online could involve US$50/lb U3O8 levels, and maybe even higher, for various reasons. It is rumored by experts that for example Cameco’s McArthur River mine, the largest and highest grade single deposit uranium mine in the world, needs a complex, difficult and expensive expansion to mine the next phase, and this is only economic at US$50/lb. It is even suggested that it would be cheaper to buy and build Arrow, the Tier I deposit of NexGen Energy, and this seems valid on the longer term as Arrow appears to be much more profitable than McArthur River or Key Lake at the moment. But of course, as a development project with long permitting periods as a uranium mine, it can’t be switched on just like that. In the meantime, Cameco fulfills its delivery duties by buying in the spot market, buying which could reach as much as 20 million pounds U3O8 this year.

It is not the only one doing this, as for example traders, banks and hedge funds are buying uranium oxides left and right in order to speculate on future price increases. A new fund, Yellow Cake PLC, has an offtake agreement in place with KazAtomProm, which accounted for the buying of 8.1M lb U3O8 at the discounted price of US$21.01/lb U3O8 in 2018, and gives Yellow Cake the possibility, not the obligation, to buy large quantities for the next nine years, to the tune of US$100 million each year.

Prices of uranium are always, just like gold, subject of widespread sentiments and not the result of a healthy supply/demand mechanism, although the uranium markets are well known by the number of utilities (the nuclear power plants) in production, under construction, etc. Something that isn’t very well understood, however, but obviously key to demand, is the stockpiling by utilities, usually by fulfilling their long term contracts, like the Japanese appeared to be doing during the shutdown since 2011. Because of this, for a while the markets expected a huge stockpile to come on the market sooner or later, when it would be clear Japan would dismantle its nuclear reactors. This development didn’t pan out as we know now, and it is expected that Japanese utilities will enter the LT markets in a few years after they restarted. It is also expected that not all Japanese reactors will be restarted, so in my view there should be a lots and lots of Japanese stockpiles available for restarting utilities.

It is widely agreed upon that the growing net number of reactors will eventually generate increased demand, which would in turn create shortages based on current supply levels. However, this can take a few years to materialize.

Uranium oxide supply isn’t switched on in a short period of time, and an increase in demand by utilities can’t be met by the mining industry in time, and this is the catalyst all uranium investors are waiting for. It will probably take at least one year to have McArthur River and Rabbit Lake back online again, and the same or even longer goes for existing or new ISR operations of KazAtomProm. It recently said it could add 7M lb U3O8 of production annually by investing US$100 million many times over, but ISR is slow to ramp up, it takes about 18 months after the wells are in place. On a side note, it remains to be seen if these companies really can ramp up efficiently in this time frame, as we have seen that for example existing and producing lithium assets are ramping up to higher production rates much slower than anticipated. Whether this has technical reasons, pricing reasons or else remains to be seen, but I can’t rule out such developments with uranium either.

Besides this, there is spare capacity waiting in Australia (Olympic Dam [BHP], which will likely be expanded as soon as uranium contract prices improve meaningfully, and the Honeymoon Mine [Uranium One], which was closed in 2013 due to low prices, will be reopened again in that case) and possibly Kazakhstan, currently globally the largest producer. In Namibia there is the Langer Heinrich (Paladin Energy) mine waiting for better times, but it will be clear that new production capacity will take a lot of time. Besides this, the Chinese-owned Husab Mine is coming online this year.

But all these mines and projects have one thing in common: it takes time, to the tune of 1.52 years, before nameplate production is reached. And when the spot market has dried up because of all the buying by Cameco, etc., and utilities start buying, there is no time. Much has been made of the potential sale of current stockpiles of utilities, but most of these stockpiles are government owned and will not go back to the markets again. On an important side note: the ramping up production of Kazakhstan since 2005 at very cheap prices has effectively put most U.S. producers out of business. A large part of this Kazakh production went to China, which has massive stockpiles, accounting for more than half of total stockpiles worldwide.

According to the World Nuclear Association, global demand is expected to rise to 180M lb U3O8 in 2025, supply will be an estimated 140M lb U3O8 at the time, including restarted McArthur River, Key Lake and Kazatomprom mines. Six years is a long time of course, in the meantime the industry had to deal with another issue, the Section 232 Petition. The well-known proposal by Ur-Energy and Energy Fuels involving a 25% quota on domestic uranium was shot down by the U.S. government. President Trump denied his Secretary of Commerce the possibility of going forward with the proposal, as he seemed to deem current developments as too insignificant to take action:

“Currently, the country imports about 93% of its commercial uranium, compared to 85.8% in 2009,” Trump wrote. “The Secretary found that this figure is because of increased production by foreign state-owned enterprises, which have distorted global prices and made it more difficult for domestic mines to compete.

“At this time, I do not concur with the Secretary’s finding that uranium imports threaten to impair the national security of the United States as defined under section 232 of the Act. Although I agree that the Secretary’s findings raise significant concerns regarding the impact of uranium imports on the national security with respect to domestic mining, I find that a fuller analysis of national security considerations with respect to the entire nuclear fuel supply chain is necessary at this time.”

This outcome was more or less expected, as opposed to the miners supporting the proposal stood the very powerful utilities sector, which didn’t like potentially higher uranium prices as a result of eventual quota. But I must say, to see the proposal making it all the way to the Secretary of Commerce, putting it on the desk of Trump, was impressive in itself as I didn’t see much viability in it. Canada and Australia account for almost 60% of U.S. uranium supply, and Kazakhstan delivers another 11%, so I don’t see a large dependence on countries like China or Russia. I had to revise my views on the position of Kazakhstan, which I viewed as relatively independent of Russia, because of being a NATO partner country

This might be true in a direct way, but indirectly the Kazatomprom facilities were built by Russia and served the Russian nuclear program for decades, and Russia still has enormous financial/business influence in the country with large investments, so although the Kazakh president might not be the best friend of Putin, I don’t expect him to act independently from Russia in this regard. Therefore, all actions by Kazatomprom must be seen in this light, and I believe now that they will do everything to gain world dominance in uranium production. They might have used the Chinese rare earth strategy, the parallels are remarkable.

What is the situation in Argentina these days regarding nuclear energy?

Argentina has three nuclear reactors generating about 5% of its electricity. Its current annual consumption is approximately 300 tonnes U3O8 (or 660,000 lb U3O8). The country’s first commercial nuclear power reactor began operating in 1974 and collectively the three plants produce 1667 MWe. The current reactors include a CANDU 6 and a Siemens design; the next two planned reactors are to be built by China National Nuclear Corporation. Additionally, five research reactors are operated by the National Commission of Atomic Energy (CNEA) and others.

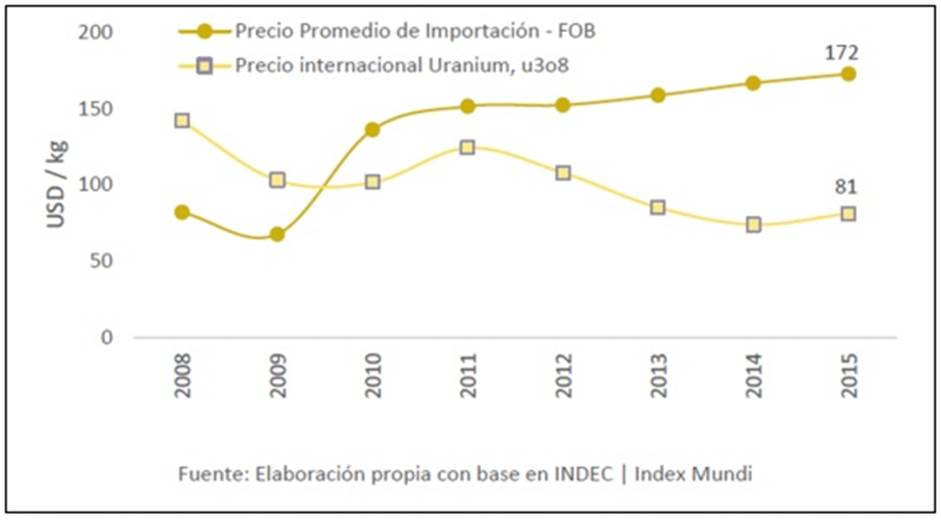

Two further research reactors are under construction. The CAREM-25 nuclear reactor, which has been developed by CNEA with INVAP and others, since 1984, is a modular 100 MWt simplified pressurized water reactor designed to be used for electricity generation (27 MWe gross, 25 MWe net) or as a research reactor or for water desalination. The prototype will be followed by a larger version, possibly 200 MWe with potential to upscale to 300 MWe. Sites in Argentina and internationally are being considered for the CAREM-25. Argentina requires 100% importation of its uranium supply. As shown in Figure 19-1 below, sourced from the Mining and Energy Industry of Argentina, the 2015 price paid for uranium was more than double the international market price for uranium.

It doesn’t look like this situation will be solved anytime soon in Argentina, and provides an excellent environment for Blue Sky and the Grosso Group to negotiate with the government on long term contracts. Talking about Argentina, let’s have a quick look at the result of the elections.

4. New President for Argentina

On October 27, left wing politician Alberto Fernandez was elected as president of Argentina, and right beside him stood the one and only Christina Fernandez de Kirchner, coming in as the new vice president of the country. Foreign capital can’t be too happy about this development, and as anticipated, a turn in the federal government is almost certainly after the pro-business course of current and outgoing president Macri. The only problem for Macri was that he couldn’t turn around the economy of Argentina, and actually aggravated the situation.

This upcoming political change has already represented uncertainties for the Argentine economy and the Argentine peso has suffered a significant depreciation in the last two months, and it may continue for a while until new government is established. This kind of uncertainty however also represents a reduction in costs due to the depreciation, as long as this depreciation outscores inflation. This reduction could also compensate the anticipated increase in country risk to a certain degree. Nobody is waiting for another YPF nationalization debacle as Kirchner pulled off in 2012, but not all is lost as it is anticipated that Fernandez is more moderate.

According to this Mining.com article, during his campaign, Fernandez met with representatives from 24 mining companies with projects in the country and told them he considered mining an opportunity, rather than a problem. He also promised to revisit the country’s controversial glacier protection law, and said that his technical team, led by economist Guillermo Nielsen, is working on a regime to guarantee clear rules for 10 years within the natural resources sector. A large pipeline of projects is waiting for development, to the tune of US$29 billion. Fernandez seems to have developed an economic agenda which includes a 10 year growth plan for the mining industry, led by the lithium sector. This is somewhat of a surprise to me as lithium is very speculative and the relevant lithium projects aren’t anywhere close to a large part of this US$29 billion pipeline, but who knows.

Other articles (in Spanish) tuned in on how Fernandez recognizes the importance of mining and its exports, but also mentioning for example the province of San Juan as a guiding example, as this province always looked after the interests of local communities surrounding mining projects. Furthermore, Fernandez is looking to initiate a Minister of Mines as he sees mining as key in revitalizing the economy, a position to be filled by the current Minister of Mining at San Juan Province, Alberto Hensel.

Other plans to stimulate exports by mining are series of tax breaks and other fiscal stimuli, as Hensel did when he was in charge as provincial minister. Hensel also acknowledged that Argentina changed mining regulations and fiscal regimes far too often, resulting in foreign capital fleeing the country. He wants to change this. So it seems although Peronist and protectionist by nature, the new government seems to understand they have to do things differently this time, very different. Let’s wait and see.

At provincial level, the Governor of Rio Negro was already elected few months ago and the actual governing party will continue for another four years. Therefore, the provincial supports to the sector is not expected to be modified. In fact, elected Governor has strongly mentioned the support to non-conventional O&G production and mining development.

On a closing note for politics before I switch to an update of exploration programs: Blue Sky Uranium also has numerous projects in the Chubut province. Situated directly south of Rio Negro, Chubut hosts several uranium deposits; however, none are currently in production and the provincial government has enacted restrictions against open-pit mining. The company’s projects in this area, Sierra Colonia, Tierras Coloradas, Regalo and Cerro Parva, comprising more than 150,000 hectares of 100% controlled mining properties, are shelved now because of this. Chubut is known as one of two anti-mining provinces that didn’t sign the new Macri normalization policy, which aimed at having a universal mining policy for every province in Argentina. Chances are that the new government can make changes in this regard.

5. Exploration Programs

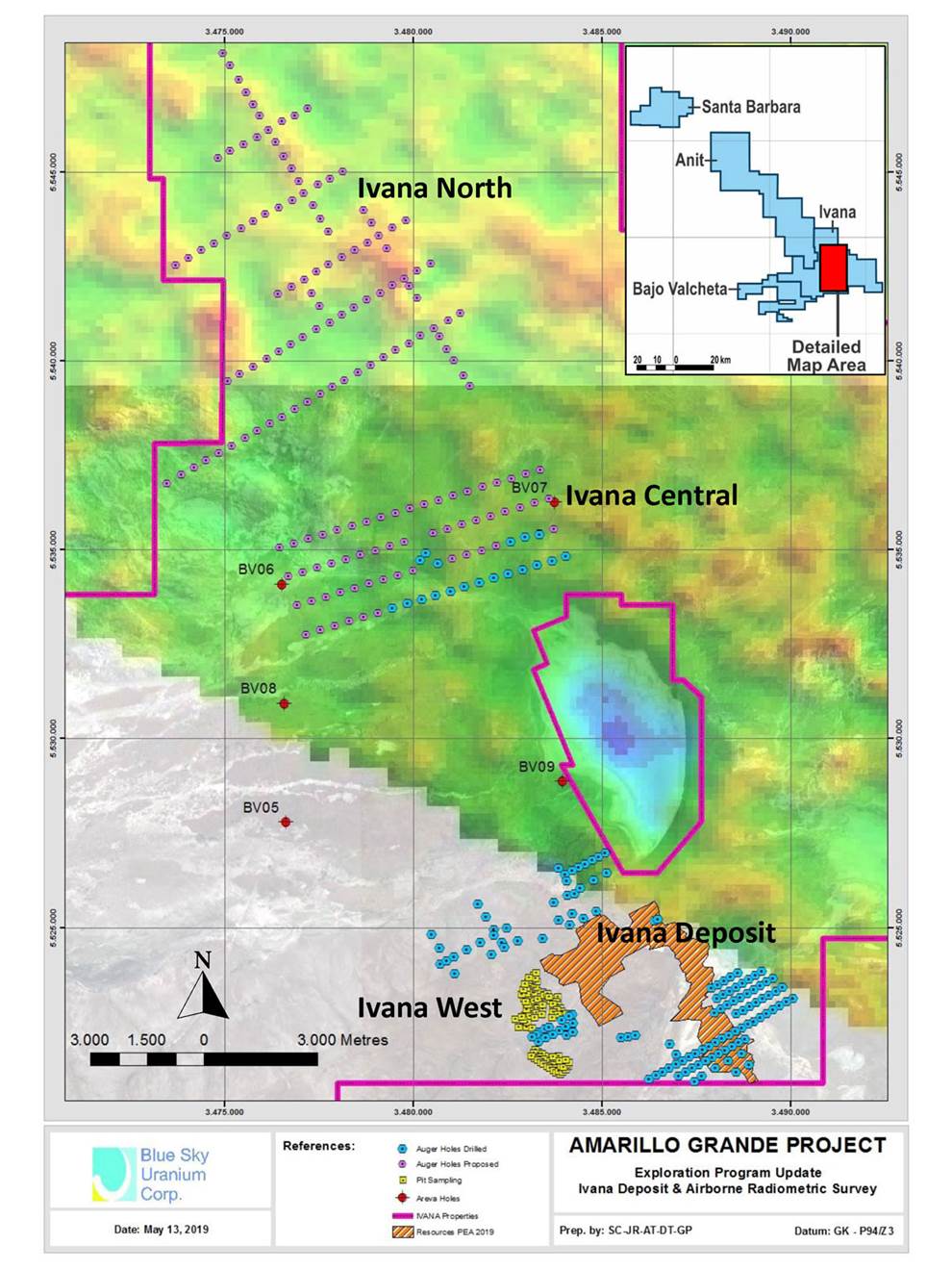

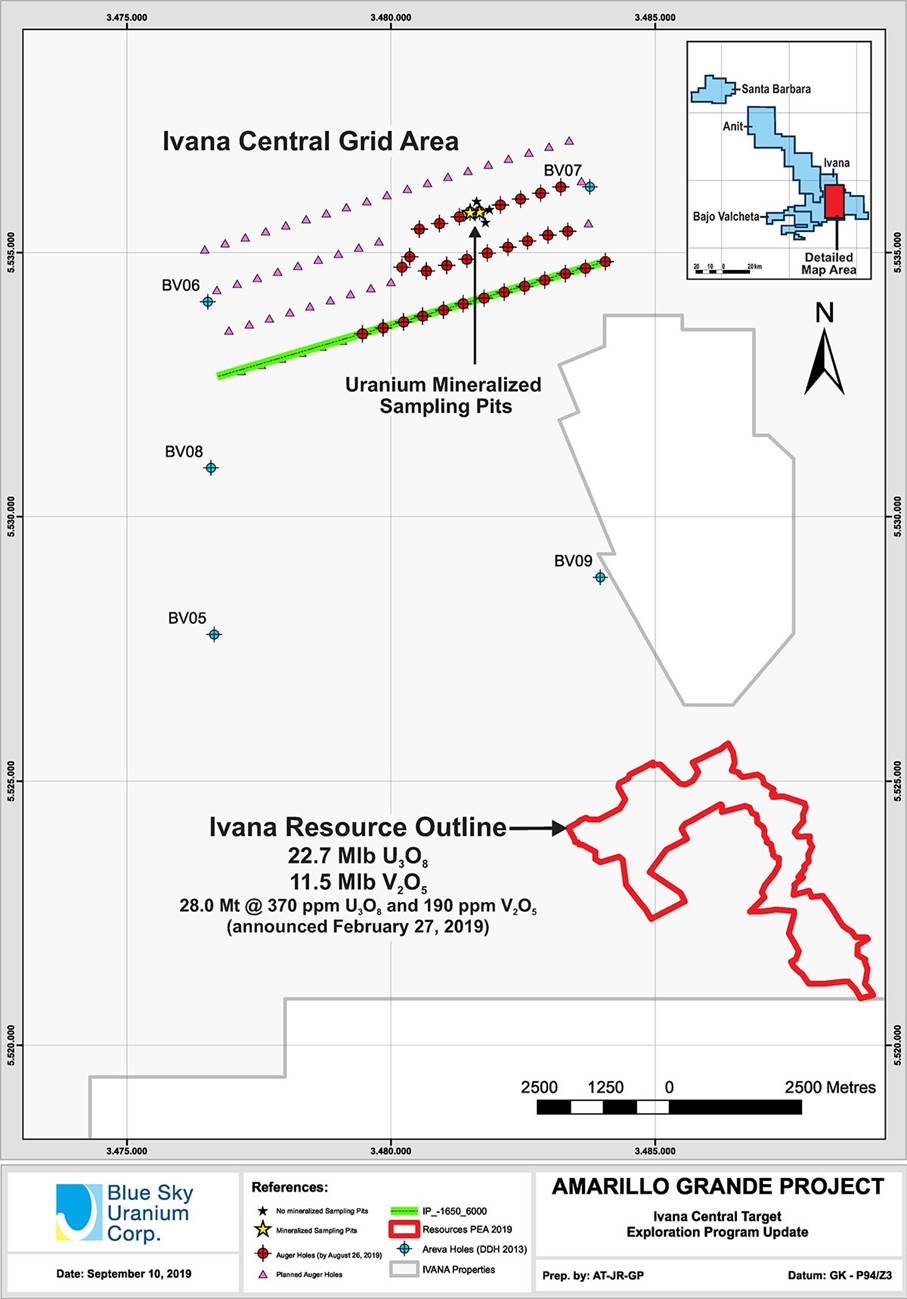

The exploration program continues on past recognized exploration targets located along a 25km-long corridor northwards of Ivana deposit, named Ivana North and Ivana Central, in order to increase the existing Inferred resource of 22.7M lbs U3O8 as much as possible:

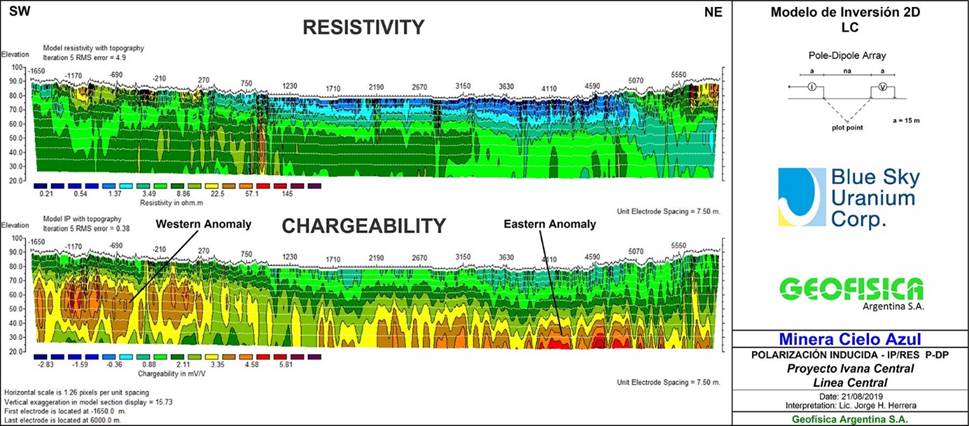

The strategy includes expansion of the known resources at Ivana deposit, and find more deposits near surface similar to Ivana deposit following the geological regional 145km trap, or redox front, where examples worldwide (as at Kazakhstan) composed of several deposits (4 of the top 10 mines are at the same district in Kazakhstan, and Cameco estimated the regional resource potential in 250 Mlb @ 500ppm U3O8). The exploration efforts were focused at Ivana Central until now, and included auger drilling and IP-survey. This target was developed based on re-assessment of the diamond drill cores drilled back in 2013 in JV with Areva. This assessment identified geological and geochemical signatures indicating the potential presence of multiple blind mineralized horizons similar to the primary mineralization at Ivana deposit, where the shallower horizon is potentially located at 30m in depth. According to management, the aim of the auger drilling is to catch subtle radiometric or geochemical anomalies confirming the presence of a blind system and its potential location. Initial auger holes helped, combined with previous exploration results, to locate a 6km-long IP testing survey, designed to detect the presence of pyrite or organic matter that may be interpreted as the trap for uranium, carried by oxidized waters in the past and generated an accumulative economic deposit. The original test was extended to 7.65km:

As a result, the IP detected two chargeability anomalies (pyrite and organic matter are chargeable), one to the west that may be interpreted as the expected horizon at 30m in depth, and another to the east located deeper probably at 4050m from surface. Both anomalies are open, and new IP-survey lines are expected to be completed in November.

The Ivana North area was first recognized back in 2010 as results of the airborne radiometric survey and follow up exploration prospecting. The initial sampling works done at Ivana North had already detected the presence of uranium/vanadium mineralization similar to the mineralization later recognized where the Ivana deposit is located today, at 20km to the south. The target area covering 10x6km radiometric and follow up sampling anomalies is planned to be covered by geophysics and auger drilling in order to adjust later RC drilling program. The works in this area are expected to be launched in the next weeks with the first IP-testing survey line followed by auger drilling.

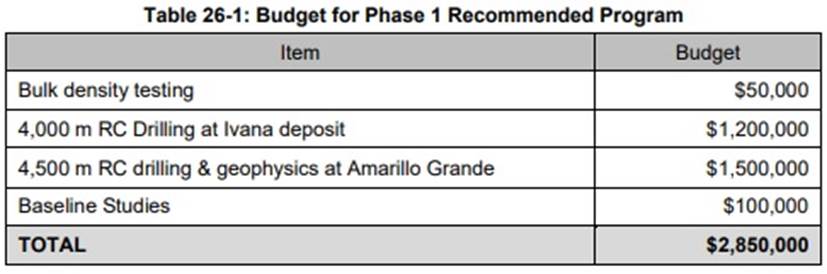

Once completed both programs, the company expects to launch a 4,500m RC drilling program in different phases at both targets. This program is expected to be initiated at the beginning of 2020, and the company is looking to raise more money to fund it, more or less following the budget estimates in the latest resource report:

The goal is to demonstrate that Blue Sky could actually control an entire uranium/vanadium district, with potential to comprise multiple deposits with significant upside potential for tonnage and economics.

As a reminder, if Blue Sky Uranium indeed manages to delineate an estimated 100M lb U3O8 and a useful amount of V2O5, it isn’t unrealistic in that case to double or even triple production capacity and double LOM. In this case some economies of scale could kick in, and despite the expected lower average grade and increased capex, the post-tax NPV8 should be able to come in at least around US$300350M, with the IRR roughly estimated at 2728% as well, maybe higher depending on the amount of higher grade ore they could delineate in the future. The company is proceeding with the expansion of the current resource and setting up work programs for the upcoming Pre Feasibility Study (PFS), and for this it is not allowed to include Inferred resources, so the entire resource needs to be converted first. Fortunately, the continuity of mineralization seems to be excellent according to management. Actual spacing of the drilling pattern allows to convert most of the resources into indicated resources. They were not converted yet by the QP because the metallurgical results were received after the resource estimation. The budget presented above includes the drilling costs to convert all actual resources into indicated (4000m).

6. Conclusion

Blue Sky Uranium managed to raise another C$0.87 million after raising C$0.68 million back in July, which is impressive in a subdued market for uranium, and mining in general except gold producers. It enabled the company to proceed with IP surveys and auger drilling, defining drill targets for a new RC drill campaign early next year. At the same time, Alberto Fernandez was elected as the new president for Argentina, and fortunately, despite his left wing Peron style protectionist/socialist background, he seems to be quite pro-mining. He not only recognized the importance and potential of the mining industry for revitalizing the economy, but is also planning on having a new Ministry of Mines, for which his Prime Minister candidate already has proven plans based on fiscal stimulation in mind. So although Kirchner is back as a vice president this time, it seems Fernandez is much more realistic with regard to mining than Macri and Kirchner combined. Very surprising. Let’s hope it all pans out well for Blue Sky Uranium.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclaimer:

The author is not a registered investment advisor, and has a long position in this stock. Blue Sky Uranium is a sponsoring company. All facts are to be checked by the reader. For more information go to www.blueskyuranium.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor’s disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

( Companies Mentioned: BSK:TSX.V; BKUCF:OTC,

)

![]()