This article first appeared on TaxAct.

If you are a U.S. resident that invested in Bitcoin or other cryptocurrencies in 2017, you may have recently received a tax document from the trading platform or cryptocurrency exchange you use and may need to pay taxes. While there is currently very little guidance on the taxation of cryptocurrency, one thing is clearly defined. The Internal Revenue Service (IRS) views cryptocurrency as property for tax purposes. That means you likely received a tax document because you either experienced a capital gain on that virtual investment in 2017 or received cryptocurrency as compensation, which is seen as ordinary income to the IRS.

For practical purposes, the IRS has issued guidance defining cryptocurrency such as Bitcoin and Ethereum as virtual currencies. This guidance is subject to interpretation, but for most people the main things to consider from a tax perspective are:

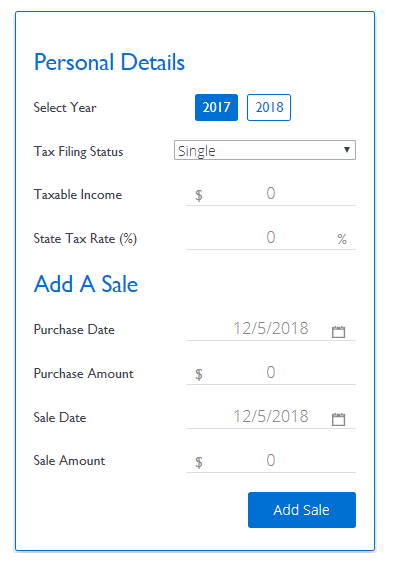

Step 1: Select the tax year you would like to calculate your estimated taxes.

Step 2: Select your tax filing status.

Step 3: Enter your taxable income excluding any profit from Bitcoin sales. For most people, this is the same as adjusted gross income (AGI).

Step 4: Enter your state’s tax rate.

Step 1: Enter the purchase date and purchase price. The purchase date can be any time up to December 31st of the tax year selected.

Step 2: Enter the sale date and sale price. Make sure the sale date is within the tax year selected.

Step 3: Repeat for all Bitcoin or cryptocurrency sales within the tax year selected.

This example calculates estimated taxes for the 2018 tax year for a person that made two sales. All values are in USD.

Free Reports:

Person A Tax and Finance Details

2018 Taxable income – 80,000

2018 Filing Status – Single

2018 State tax rate – 5%

Transaction #1

On Feb. 1, 2018, Person A sold Bitcoin for a total of $10,000. That Bitcoin was previously purchased on June 1, 2017 for $5,000. Since it was held for less than a year, the $5,000 profit is subject to short-term capital gains tax rates. Based on Person A’s filing status and income, the taxes are calculated as follows:

$2,500 X 22 percent + $2,500 X 24 percent = $1,150 federal taxes owed on short-term capital gains

$5,000 X 5 percent = $250 state taxes owed

$1150 + $250 = $1,400 total tax liability for transaction #1

Transaction #2

On Mar. 1, 2018, Person A sells Bitcoin for a total of $10,000. That Bitcoin was purchased on Feb. 1, 2017 for $3,000. Since it was held for longer than a year, the $7,000 profit is subject to long-term capital gains tax. In addition, Person A’s taxable income is now calculated at $85,000 to include the income from the previous sale. The taxes are calculated as follows:

$7,000 X 15 percent = $1,050 federal taxes owed onlong-term capital gains

$7,000 X 5 percent = $350 state taxes owed

$1,050 + $350 = $1,400 total tax liability for transaction #2

Total Taxes Owed

Since both long-term and short-term capital gains are positive, the total taxes owed are calculated as follows:

$1,150 federal short term capital gains + $1,050 federal long term capital gains + $600 state taxes owed = $2,800 total taxes owed

This article first appeared on TaxAct. Source: https://blog.taxact.com/bitcoin-tax-calculator/

{kind=link}

{kind=link}