By IFCMarkets

SP 500, Dow continue extend record streak

US stock market extended the streak of records on Wednesday supported by better than expected data. The dollar weakened: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, retreated 0.1% to 93.489. The S&P 500 rose 0.1% settling at a record 2537.74 led by utilities and real estate shares. Six out of 11 main sectors of the index closed higher. The Dow Jones added 0.1% to new record high 22661.57 led by gains in Nike and Caterpillar. Nasdaq composite inched up less than 0.1% to 6534.63.

Treasury yields were little changed as investors watched closely who seems more likely to get picked by President Trump as next Federal Reserve chair: former Fed governor Kevin Warsh or current governor Jerome Powell. Warsh is considered more hawkish policymaker than Powell. Fed Vice Chair Fischer expressed his belief inflation would rise eventually, saying the pace of monetary tightening was “OK, it is not terrific”. In economic news a gauge of services sector activity came in stronger than expected: the ISM’s nonmanufacturing index in September hit a 12-year high of 59.8. A number above 50 indicates expansion. ADP’s private-sector jobs report showed 13500 jobs were created in September. The number was lower than 228000 reading in the previous month, in line with expectations of a negative impact from hurricanes.

Bank shares lead European markets lower

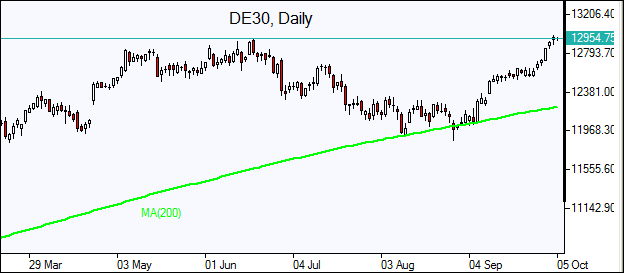

European stocks ended lower on Wednesday on increasing uncertainty spurred by Catalonia independence referendum. The eurocontinued the rise against the dollar while British Pound ended little changed. The Stoxx Europe 600 index lost 0.1%. Germany’s DAX 30gained 0.5% to 12970.52 catching up as it opened after a bank holiday on Tuesday. France’s CAC 40 slipped 0.1% and UK’s FTSE 100edged lower 0.01% to 7467.58. Stocks opened lower today.

Bank shares led the losses with Spain’s banks hardest hit on rising political risks to euro-zone prospect of Catalonia’s possible secession from Spain. King Felipe VI accused Catalan secessionist leaders of shattering democratic principles in a rare televised speech. Catalonia parties requested the regional parliament convene Monday to review the results of this week’s independence vote.

Asian indices flat

Asian stock indices are steady today in thin trading with markets in China and South Korea closed for the week. Nikkei was little changed inching 0.01% higher to 20628.56 as yen climbed against the dollar. Australia’s All Ordinaries Index added 0.01% as Australian dollar erased previous day’s gains against the greenback after unexpectedly weak retail sales report.

Oil rising after larger than expected US inventory draw

Oil futures prices are rising today buoyed by possibility of extension of major oil producers’ output cut agreement. Russian President Vladimir Putin said on Wednesday that a pledge by the Organization of the Petroleum Exporting Countries and other producers, including Russia, to cut oil output to boost prices could be extended to the end of 2018, instead of expiring in March 2018. Prices ended lower yesterday despite the US Energy Information Administration report domestic crude supplies fell by 6 million barrels last week. December Brent crude lost 0.4% to $55.80 a barrel on Wednesday on London’s ICE Futures exchange.

Market Analysis provided by IFCMarkets

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.