Article by ForexTime

In a week where investors were preparing for news around political risk to be dominated by the upcoming UK election and ongoing headlines in Washington, the markets were caught completely off-guard on Monday morning when a Saudi-led alliance unexpectedly cut diplomatic ties with Qatar. This unexpected development consequently led to pressure on markets in the region, where the Qatar stock market suffered its heaviest fall since 2009 at around 8% during early trade.

Political risk was something that was not being priced into the regional markets, therefore the markets were caught unprepared for this development and it attracted the most international attention to begin the new trading week.

This news comes at a time where political instability in Washington and uncertainty ahead of the UK general elections was already presenting risks to investors becoming cautious, and the increase in political tensions following this news is not likely to seize the spotlight until the UK election on Thursday evening. The question that markets are probably wondering is how Qatar might react, with this increase in political risk potentially weighing on stocks throughout the region beyond what we saw on Monday.

While the Oil markets edged slightly higher following the news around Qatar, gains were later pared when investors refocused on the ongoing oversupply in the market. On headline, the Saudi-led alliance cutting diplomatic ties with Qatar doesn’t actually change the outlook for the Oil markets as it currently stands. The main story around Oil still revolves around the ongoing oversupply concerns with OPEC’s effort to stabilize the markets repeatedly obstructed by production elsewhere, most notable US Shale Production.

The decision by the Saudi-led alliance to cut diplomatic ties with Qatar could raise questions over whether Qatar will fulfil its production quota. Qatar is not seen as a major producer of Oil, but the threat of a possible reaction could lead to investors revisiting the previous concerns over a lack of compliance when it comes to the OPEC deal.

I believe that the threat of Qatar going against the production quota could encourage other OPEC members to also cheat on the agreement, ultimately exposing the oil markets to further downside shocks if this were to occur.

Dollar losses attitude

The Greenback was under renewed selling pressure last week Friday after the soft U.S jobs data for May raised concerns over the Federal Reserve’s ability to raise US rates beyond the expected rate increase in June. Although the jobless rate unexpectedly dropped to 4.3% and hourly earnings printed in line with expectations at 0.2%, the soft headline NFP figure of 138k was seen as a thorn in the flesh which sparked concerns over the resilience of the US labour force. With bears swiftly exploiting the downside surprise in May’s jobs report to pressure the Greenback, further downside could be a risk moving forward.

It still look likes the risks to the Dollar are tilted to the downside, as political uncertainty in Washington and soft economic data weighs on the currency.

From a technical standpoint, the Dollar Index is heavily bearish on the daily charts. The breakdown below 96.80 should encourage a further decline towards 96.00.

Sterling – UK General Election in focus

Sterling traded slightly higher on Monday with the GBPUSD hovering around 1.2900 as investors remained on standby ahead of the Thursday’s General Election in the UK. It is becoming quite clear that Brexit developments may dictate where Sterling trades and uncertainty is likely to limit upside gains. With the recent polls suggesting a potential situation where Theresa May is unable to secure enough seats to form a government, investors have become quite jittery ahead of a potential “hung parliament” scenario playing out.

Uncertainty and anxiety are likely to heighten ahead of the General Election on Thursday and such outcomes should expose the Sterling to further selling pressure.

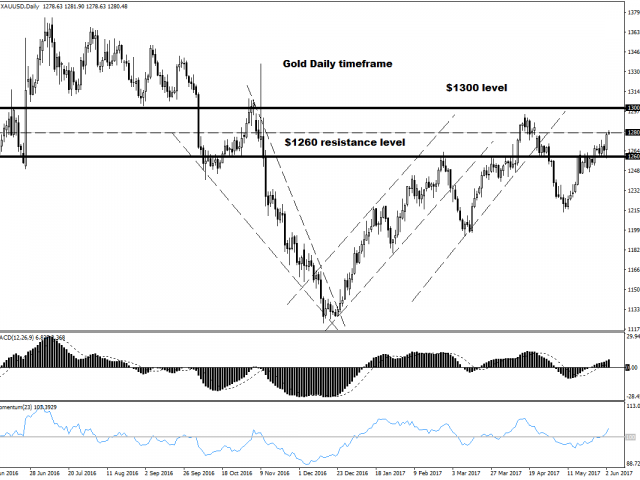

Commodity spotlight – Gold

Gold ventured higher on Monday with prices appreciating towards $1281 as Dollar weakness provided a firm foundation for bulls to initiate heavy rounds of buying. With expectations of the Federal Reserve raising US interest rates beyond June taking a hit following May’s disappointing jobs report, the yellow metal remains well supported.

I believe that the outlook for Gold remains tilted to the upside, especially when considering how political instability in Washington and Brexit woes could accelerate the flight to safety. From a technical standpoint, a breakout above $1275 is likely to encourage a leg up higher towards $1300.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]()

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com