By IFCMarkets

Yellen reaffirms Fed’s gradual rate hike plans

US stocks fell on Tuesday after Senate Republicans delayed the vote on health care legislation until after the July 4 holiday. The dollar weakened: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, ended 0.9% lower at 96.491. Dow Jones industrial average lost 0.5% closing at 21310.66. The S&P 500 dropped 0.8% settling at 2419.38. The Nasdaq index fell 1.6% to 6146.62 as technology stocks extended losses.

With stock valuations at historical highs driven by expectations of President Trumps pro-growth policy promises, the progress on Trump administration’s first legislative initiative is seen as an indicator of administrations ability to deliver on Trump’s promises including tax reform. Fed chair Yellen, speaking in London on Tuesday, repeated her stance that rates overall would remain low for some time and would be raised gradually. Philadelphia Fed President Patrick Harker, a voting member of Federal Reserve’s policy committee, restated his view that another rate hike was needed this year and said the balance sheet reduction process should be on “autopilot”. In economic news the Conference Board’s consumer confidence index rose to 118.9 in June from 117.6 in May.

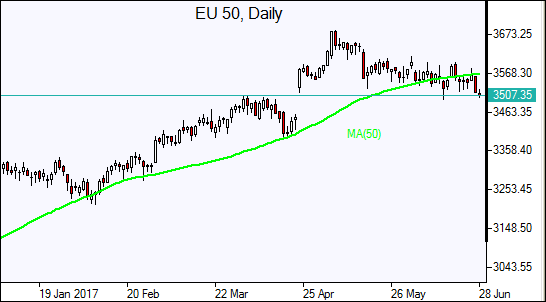

Stronger euro weighs on European markets

European stock indices ended lower weighed by stronger euro and profit warnings. Both the euro and British Pound resumed gains against the dollar. The Stoxx Europe 600 fell 0.8%. Germany’s DAX 30 lost 0.8% closing at 12671.02. France’s CAC 40 retreated 0.7% and UK’s FTSE 100 slipped 0.2% to 7434.36.

Euro jumped 1.3% after remark by European Central Bank President Draghi “a considerable degree” of stimulus is needed in euro-zone, instead of “very substantial” level used in earlier speeches. This was interpreted as a signal the ECB considers winding down its quantitative easing program. A stronger euro hurts earnings prospects of exporters, pressuring their stock prices.

Asian markets lower

Asian stock indices are mostly down today as investor confidence was undermined by US Senate decision to delay the health care reform vote and technology stocks fell tracking Wall Street overnight. Nikkei fell 0.5% to 20130.41 despite a weaker yen against the dollar. Bank stocks posted gains though as Yellen’s comments supporting gradual rate hikes in US raised their earning prospects expectations. Chinese stocks are down: the Shanghai Composite Index is 0.5% lower and Hong Kong’s Hang Seng Index is down 0.6%. Australia’s All Ordinaries Index is up 0.8% despite stronger Australian dollar against the greenback.

Oil down on expected US stock draw

Oil futures prices are rising today. Oil prices rose on Tuesday on expectations of a weekly drop in US crude oil inventories. August Brent crude closed 1.8% higher at $44.24 a barrel on London’s ICE Futures exchange on Tuesday. However, The American Petroleum Institute showed late Tuesday US crude stocks rose by 851 thousand barrels last week and gasoline supplies rose 1.4 milion barrels. Today at 16:30 CET the Energy Information Administration will release US Crude Oil Inventories. Analysts polled by S&P Global Platts expect a decline of 3.25 million barrels in crude inventories.

Market Analysis provided by IFCMarkets

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.