By IFCMarkets

Revised healthcare legislation vote expected today

US stocks closed lower on Wednesday after the Federal Reserve left interest rates unchanged. The dollar inched higher as the Fed deemed first quarter GDP as ‘transitory’: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, closed up 0.4% at 99.356. The S&P 500 lost 0.2% settling at 2388.13 led by materials and telecom stocks. The Dow Jones industrial average inched up less than 0.1% to 20957.90. Nasdaq index fell 0.5% 6072.55.

Federal Reserve emphasized the strength of the labor market which was interpreted as a sign the central bank plans two more rates this year as previously expected. Markets deemed bullish central bank’s assessment that consumer spending continued to be solid, business investment had firmed and inflation has been “running close” to the Fed’s target. Investors expect Federal Reserve will raise rates at its June meeting. Market reaction to private sector jobs data was muted. Private sector employment slowed down in April as employers added 177 thousand jobs, ADP reported Wednesday, down from a revised 255 thousand jobs created in March. In other economic news, Markit’s services activity report for April showed an increase to 53.1 from the previous month’s 52.5. And ISM reported a nonmanufacturing index of 57.5, indicating growth, from previous month’s 55.2 reading. Investors will be focusing now on corporate reports, which have been mostly positive. A vote in the House of Representatives today is expected on newly revised healthcare legislation which would repeal most Obamacare taxes, including a penalty for not buying health insurance, cut funding for Medicaid, the program that provides insurance for the poor, and roll back much of Medicaid’s expansion. Today at 14:30 CET initial jobless claims and unemployment claims will be released, as well as March Trade Balance will be published, the outlook is positive for dollar. And at 16:00 CET March Factory Orders will be released, the outlook is negative.

European stocks end lower ahead of Fed decision

European stocks retreated from 20-month high on Wednesday after the first reading on euro-zone economic growth of 0.5% on quarter matched market’s expectations while the fourth quarter growth was revised up. Both the euro and British Pound slipped against the dollar. The Stoxx Europe 600 lost less than 0.1% in a cautious trade ahead of Federal Reserve’s interest rate decision. Germany’s DAX 30 outperformed rising 0.2% to 12527.84. France’s CAC 40 closed 0.1% lower and UK’s FTSE 100 index fell 0.2% settling at 7234.53.

Other economic data were mixed: the 0.3% decline in producer prices in the euro was bigger-than-expected in March. At the same time the German unemployment rate in April stayed at 5.8%, the lowest since 1992. Today at 10:30 CET April Services and Composite PMI will be published in UK, the outlook is negative for Pound. At 11:00 CET March Retail Sales will be published in euro-zone, the outlook is negative for euro.

Asian stocks track Wall Street

Asian stock indices are down dragged lower by commodities, energy and financials stocks. Markets in Japan are closed for the Golden Week holiday. Chinese stocks are down as growth in services sector slowed with Caixin Services PMI slipping to 51.5 in April from 52.2 in March: both the Shanghai Composite Index and Hong Kong’s Hang Seng Index are 0.3% lower. Australia’s All Ordinaries Index is 0.3% lower despite a weaker Australian dollar against the buck.

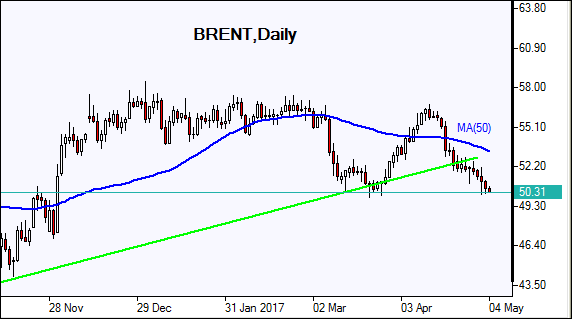

Oil prices slip as US inventories fall less than expected

Oil futures prices are inching lower today after data showed the decline in US inventories was much less than the market expected. Crude inventories fell by 930 thousand barrels last week, fourth consecutive decline, but at 527.8 million barrels they are still 3% higher from this time a year ago. Investors are anxious to see whether OPEC and other producers will extend production cuts into the second half of the year as they monitor their compliance with their 2016 deal to cut output around 1.8 million barrels per day (bpd) by the middle of the year. Russia, contributing the largest production cut outside OPEC, said as of May 1, it had cut output by more than 300,000 bpd since hitting peak production in October.

Market Analysis provided by IFCMarkets

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.