By IFCMarkets

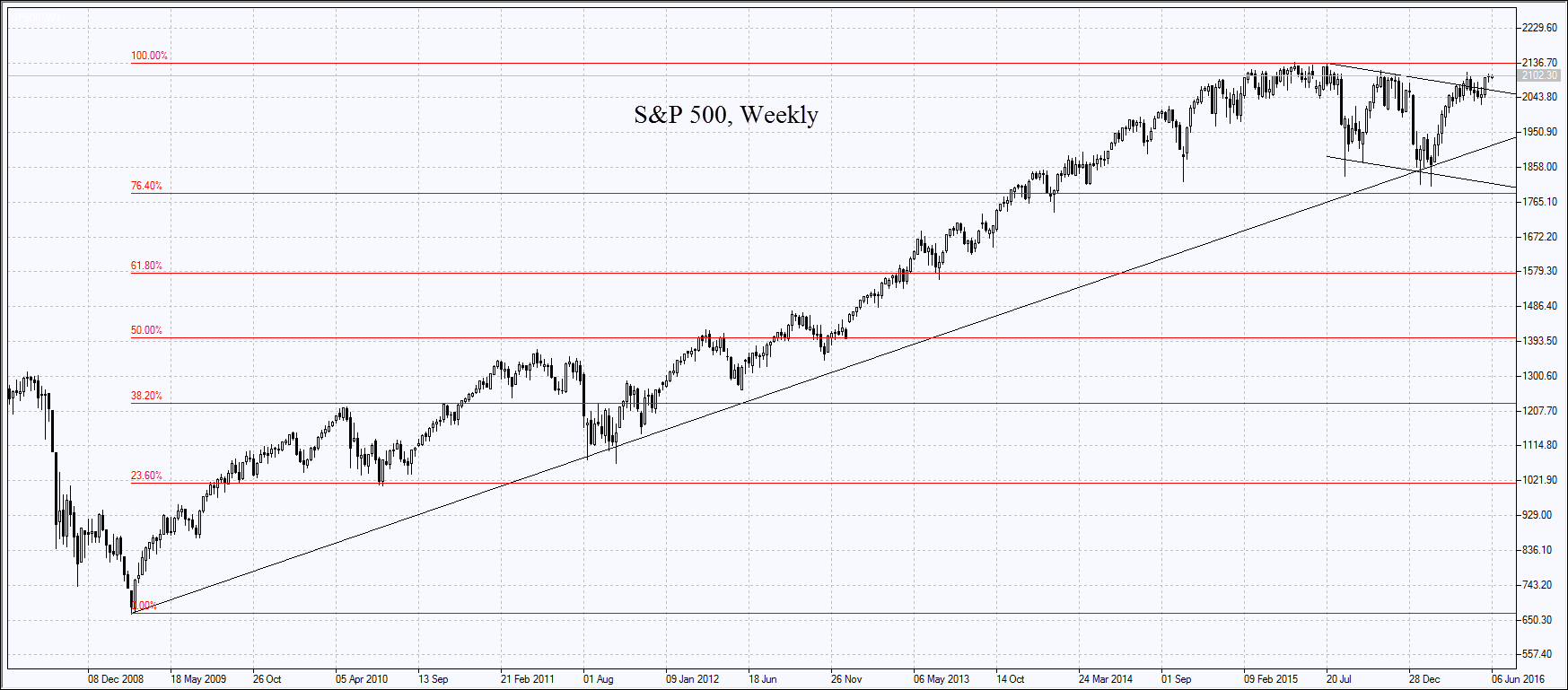

US dollar index showed the record daily fall in four months on Friday in the wake of unexpectedly weak labour market data for May. The Non-farm Payrolls totaled just 38 thousand which is their lowest since September 2010. As the number of 160 thousand was anticipated, the markets reacted strongly. The Fed funds futures now price in only 4% chance for the rate hike on June 15, the data showed on Friday, down from 21% on Thursday. The chances for July rate hike fell to 38% from 60%. The US unemployment decreased to 4.7%, its low since November 2007. This did not support investors’ optimism as nonfarm payrolls are more representative while the unemployment may show that some Americans stopped searching jobs or lost the “unemployed” status. US stock market indices edged slightly lower on Friday. Market participants believe the weak dollar may support exporters. Moreover, the possible delay in Fed rate hike will mean longer period of low credit rates. No significant economic data are expected today in US. The investors’ opinion is focused on the forthcoming Fed Chair speech in Philadelphia due on 18:30 СЕSТ. The speech may give some hints on probability of the rate hike in June. US dollar index is slightly advancing on Monday morning.

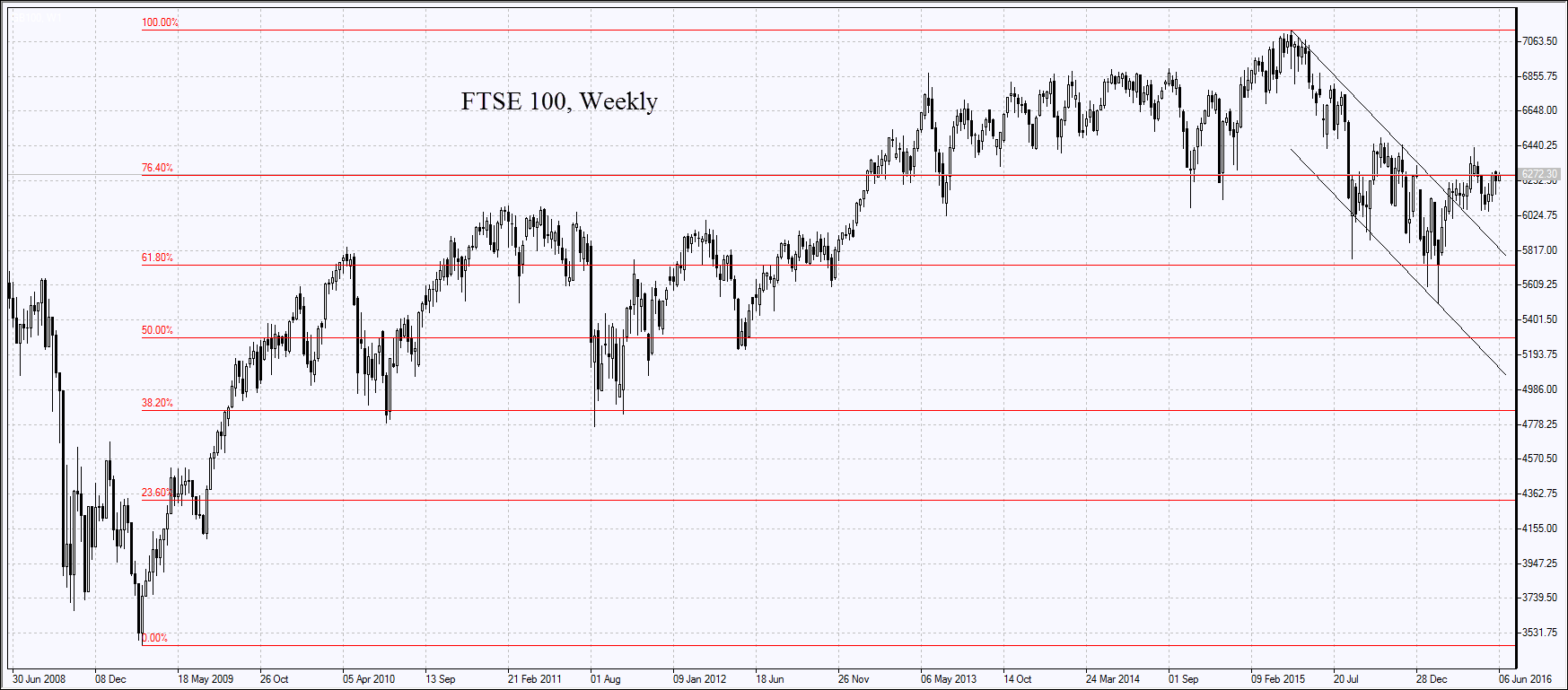

European stock market indices were almost flat on Monday after the fall of around 1% on Friday. The mining and oil companies advanced on dearer oil while air carriers and transport companies were in the red. Market participants worry about the Brexit on referendum on June 23. The result is weakening pound and falling European stock market indices. In the meantime, British FTSE 100 is advancing 0.7%. Today in the morning the Markit retail PMI for May came out in Eurozone and Germany. The German Bunds prices soared while yields fell to the year low. In theory, European stock market indices may also edge up today.

Nikkei index opened on Monday near its Friday low and has been rising for almost the whole day in bargain hunting after the incessant 3-day fall end of last week. The Japanese stocks also advanced on fair weakening of yen. Weaker yen is considered to support Japanese exporters. Last week the Japan’s Prime Minister Shinzo Abe postponed the sales tax hike from 8% to 10% from 2017 to October 2019. Moreover, some other measures are planned to support the economy which may stimulate Nikkei increase. Since the start of the year it has already slumped almost 13% while European stock market indices are almost unchanged as the US indices added up to 3%. The significant economic data are to come out in Japan this Wednesday and Thursday: the GDP, trade balance, factory orders and other.

This week the significant economic data will come out in China from Wednesday to Friday which may affect the commodity futures.

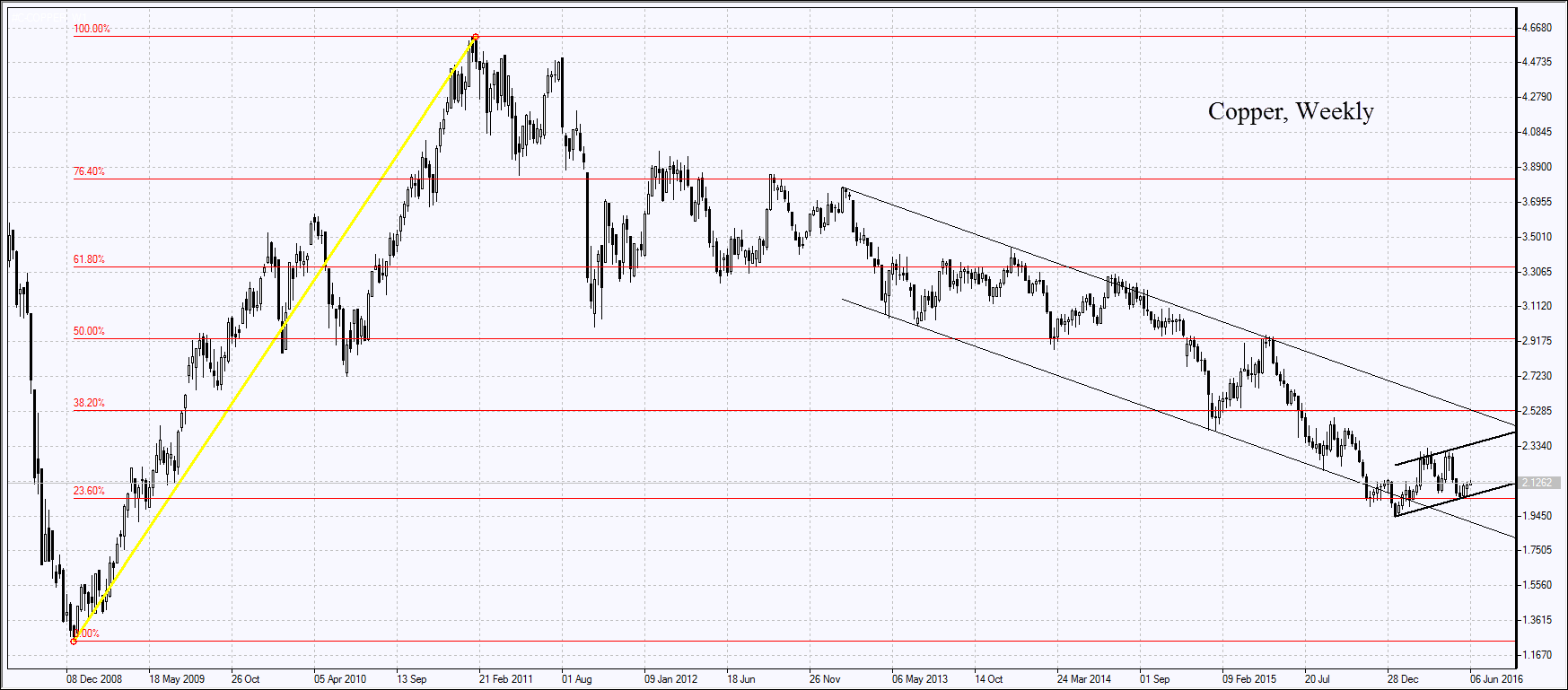

Copper prices reached the 4-week high while zinc reached the 10-month high. Copper is traded near its 7-year low. Several countries cut their production due to low prices. In Congo it fell by 20% or 55.2 thousand tonnes in Q1 2016. This country ranks 5th in global copper production.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.