By IFCMarkets

On Friday US stocks and US dollar rose both. US payrolls for April were not as catastrophic as investors anticipated. On Wednesday the independent ADP agency reported the US economy created the lowest in three years number of jobs: 156 thousand. The US Department of Labour data came out on Friday being above the ADP data which relieved investors’ anxiety. US Nonfarm payrolls showed the number of 160 thousand newly created jobs in April while the February and March data were revised up by 19 thousand. As a result, the nonfarm payrolls were the lowest in 7 months but not three years. Anyway, the data emphasize the weakness of the US economy. Now investors do not expect at all the Fed interest rate hike on the next meeting on June 14-15. The probability of the September rate hike is estimated at 42% and at 61% in December. On Monday morning the US stock index futures are advancing. According to the latest consensus forecasts, the total earnings of S&P 500 companies in Q1 contracted only by 5.1%. About 60 companies from S&P 500 index have not reported their quarterly earnings yet. Previously, the total earnings were expected to contract much more – by more than 7%. No significant economic data are expected today in US and little data will be released this week.

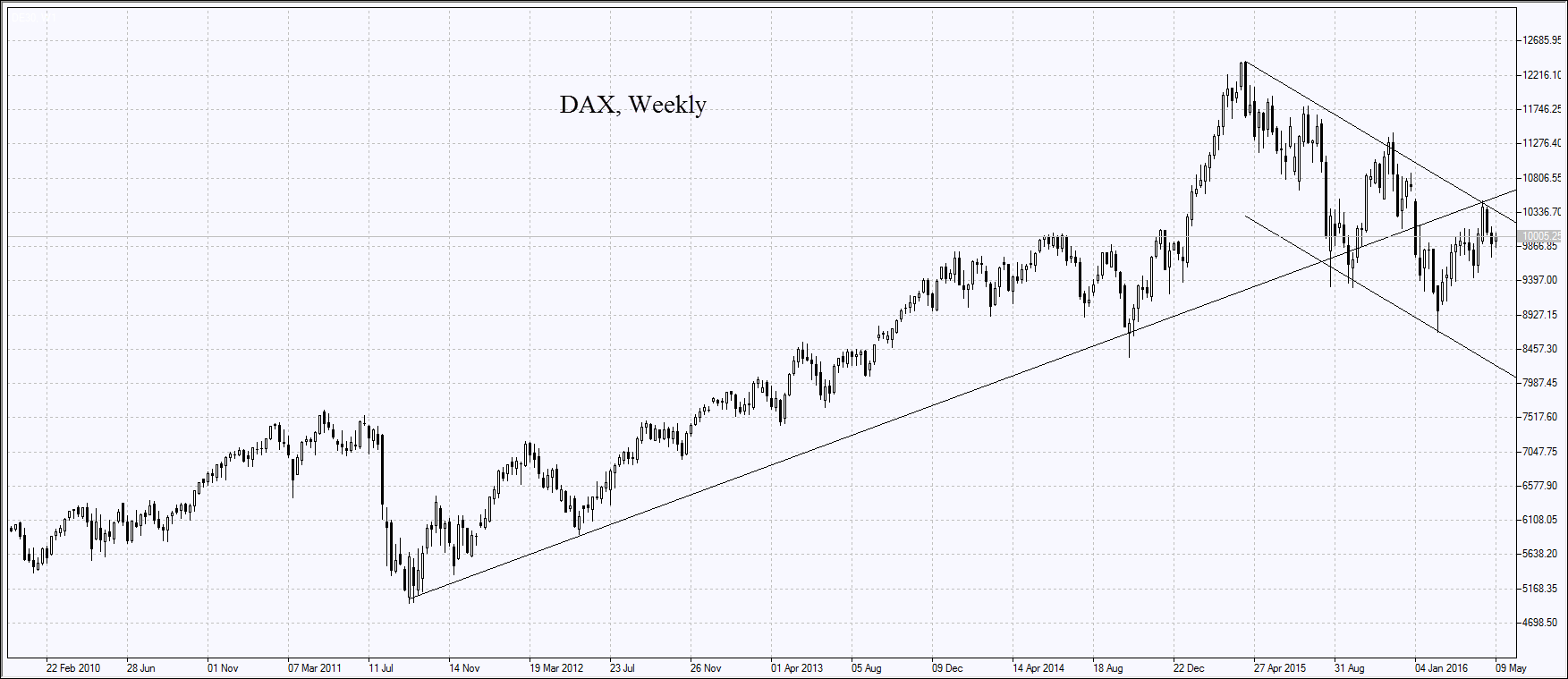

US dollar index is advancing today on external factors and on weaker euro and yen. Market participants expect the further monetary easing by ECB. Meanwhile, the current QE volume of 80bn euros has a positive impact on the economy. The Germany’s factory orders rose 1.7% in March year on year which is far above the expectations. This supported the Germany’s DAX 30 index and European stocks on Monday. No more significant economic data are expected today in Eurozone.

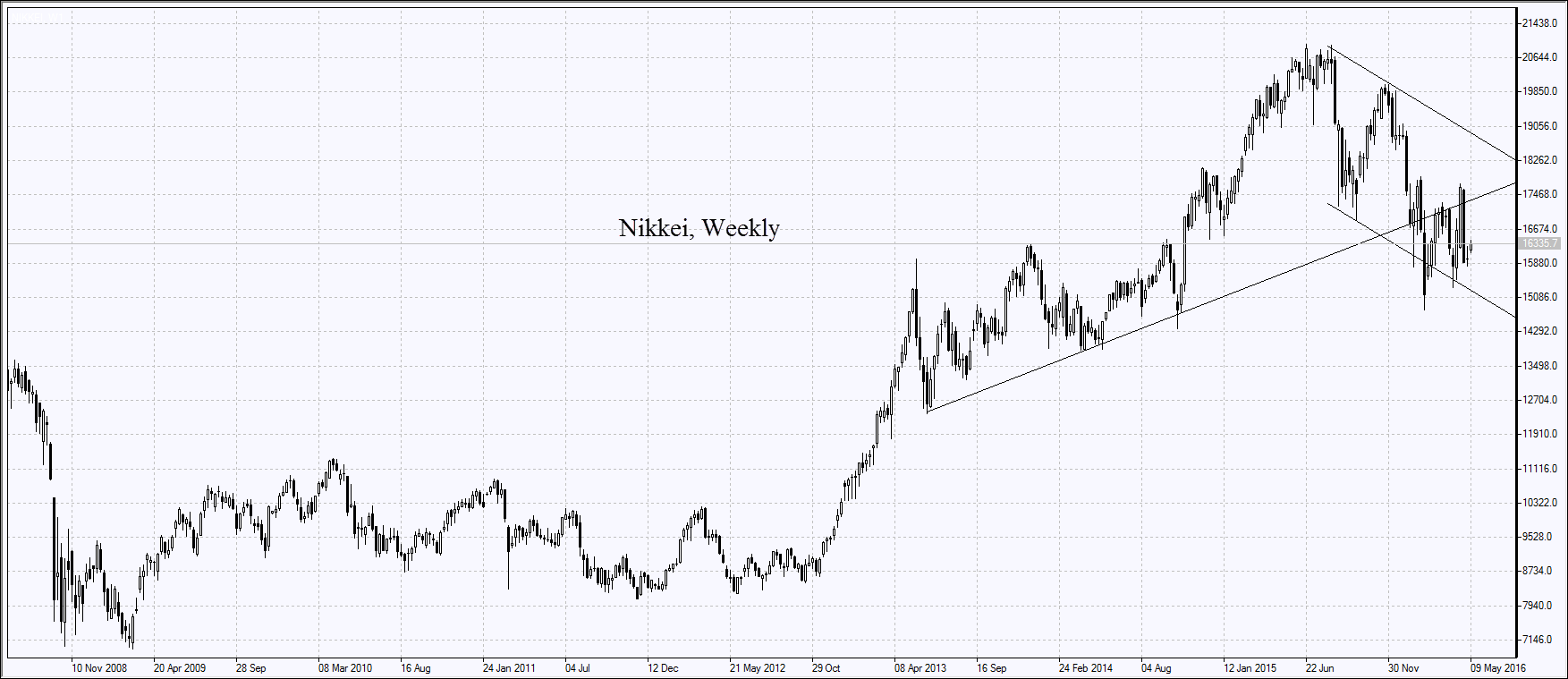

Japanese yen weakened a lot against the US dollar on Monday which looks as growth on USDJPY chart. The Japan’s prime-minister and minister of finance said the BoJ could intervene in case of further yen strengthening. Weak yen supported the Nikkei stock market index. The further significant economic data are to come out in Japan on Thursday: those are the current account balance and the trade balance for March.

The China’s trade balance data for April were released on Sunday. They were negaqtive for the global markets are confirmed the slowdown of the Chinese economy. Imports to Chana fell for the 18th straight month. Such a decline is not negative for China as exports rose slightly which means the US trade balance surplus widened. Nevertheless, the yuan weakened against the US dollar. The commodity futures also edged lower.

Oil prices remain almost unchanged as the data on Chinese economic slowdown and the risks of lower demand were offset by the news the wildfires in Canada may lead to 1mln barrels – or one-third –slump in daily oil production.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

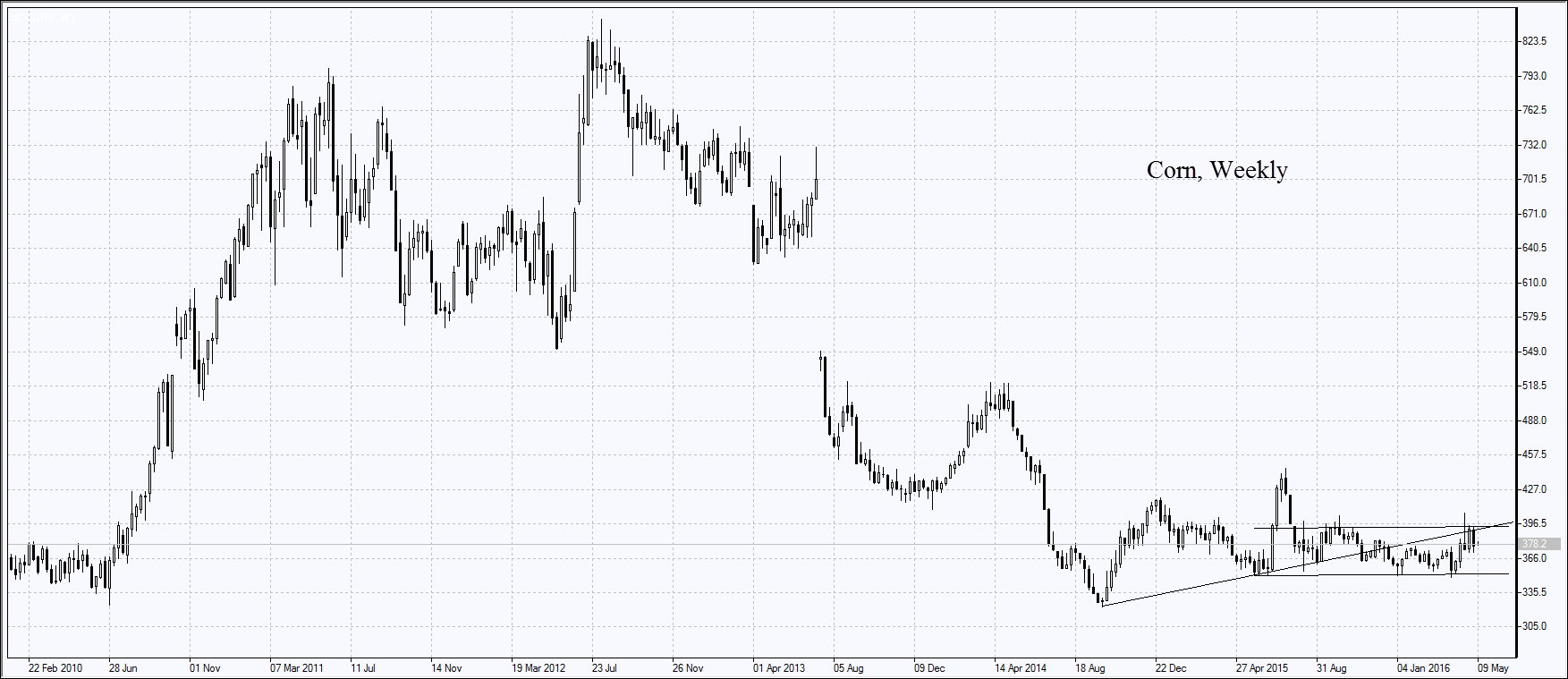

Corn prices may find support in China National Grain and Oils Information Center (CNGOIC) data. The Center forecasts the corn production to contract by 2.9% to 218mln. tonnes this year in China, while the consumption is to increase to 185.5mln tonnes or by 41.8mln tonnes compared to the previous period. This may reduce China’s stockpiles. Now markets remain calm as CNGOIC expects lower production will not stimulate corn imports to China. The situation may change is the crops fall more than projected.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.