By CountingPips.com | Weekly Large Trader COT Report: Currencies

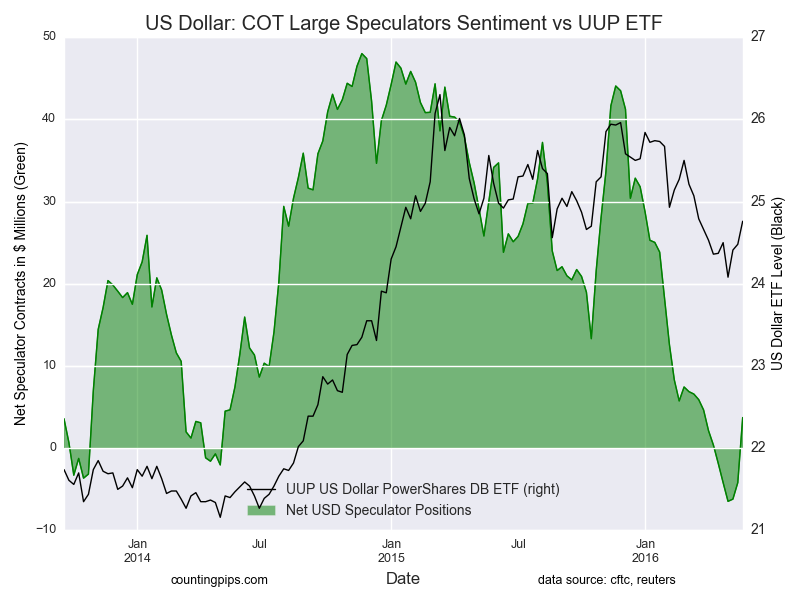

The latest data for the weekly Commitment of Traders (COT) report, released by the Commodity Futures Trading Commission (CFTC) on Friday, showed that large traders and currency speculators boosted their bets in favor of the US dollar last week and pushed speculative positions into a new bullish position after being in bearish territory for five straight weeks.

Non-commercial large futures traders, including hedge funds and large speculators, had an overall US dollar long position totaling +$3.73 billion as of Tuesday May 24th, according to the latest data from the CFTC and dollar amount calculations by Reuters. This was a weekly change of +$7.92 billion from the -$4.19 billion total short position that was registered on May 17th, according to the Reuters calculation that totals the US dollar contracts against the combined contracts of the euro, British pound, Japanese yen, Australian dollar, Canadian dollar and the Swiss franc.

The US dollar speculative position has now improved for three straight weeks and is back in bullish territory for the first time since April 12th.

Weekly Speculator Contract Changes:

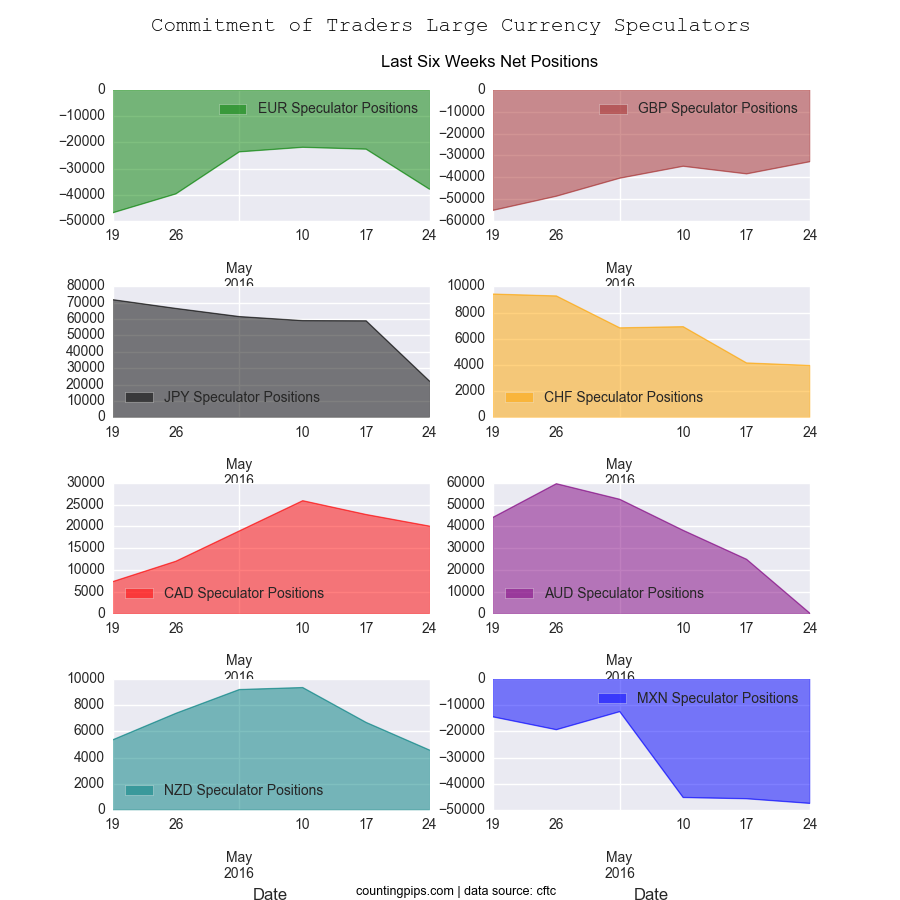

Last week’s data showed that only the British pound sterling (+5,587 change in weekly contracts) saw higher speculative positions against the dollar.

Free Reports:

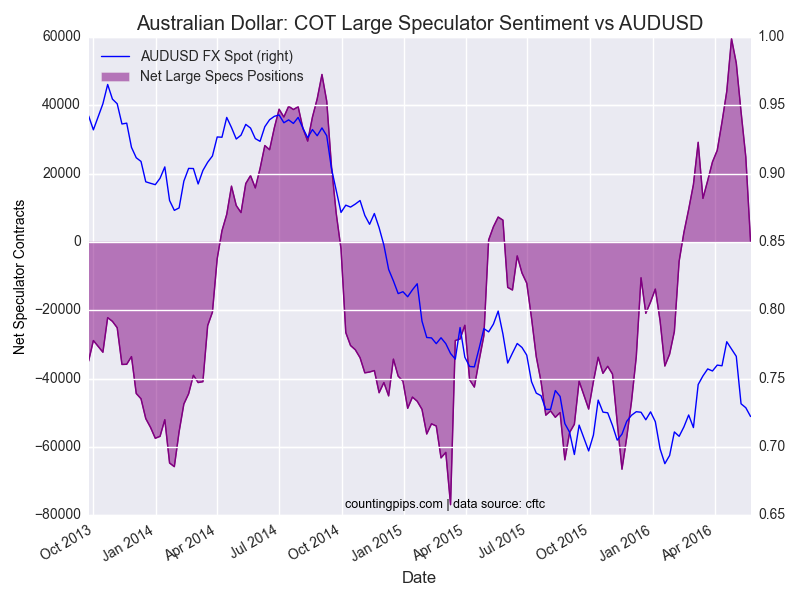

All the other major currencies recorded lower speculative positions against the dollar on the week with the sharpest declines taking place in the Japanese yen (-36,860 weekly change in contracts), the Australian dollar (-24,769 contracts) and the euro (-15,308 contracts).

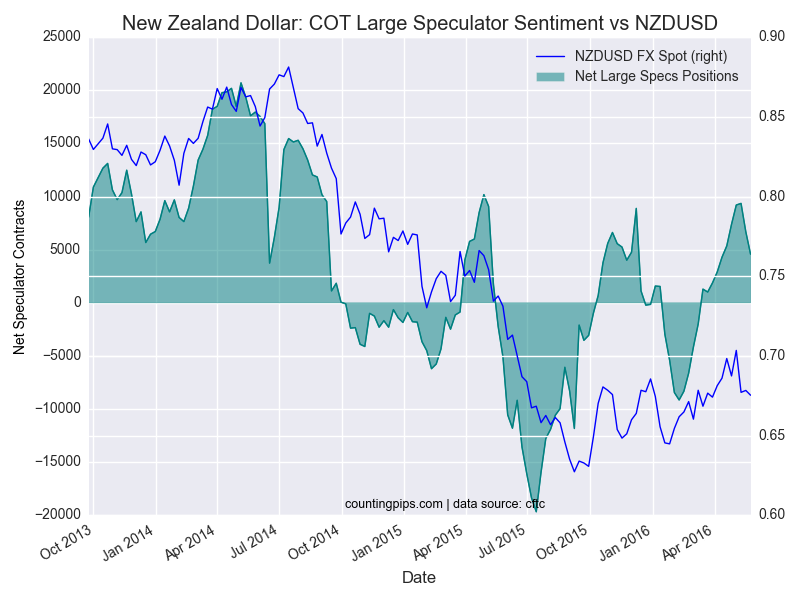

Other currencies last week showing speculative positioning declines were the Swiss franc (-193 contracts), New Zealand dollar (-2,112 contracts), Canadian dollar (-2,659 contracts) and the Mexican peso (-1,769 contracts).

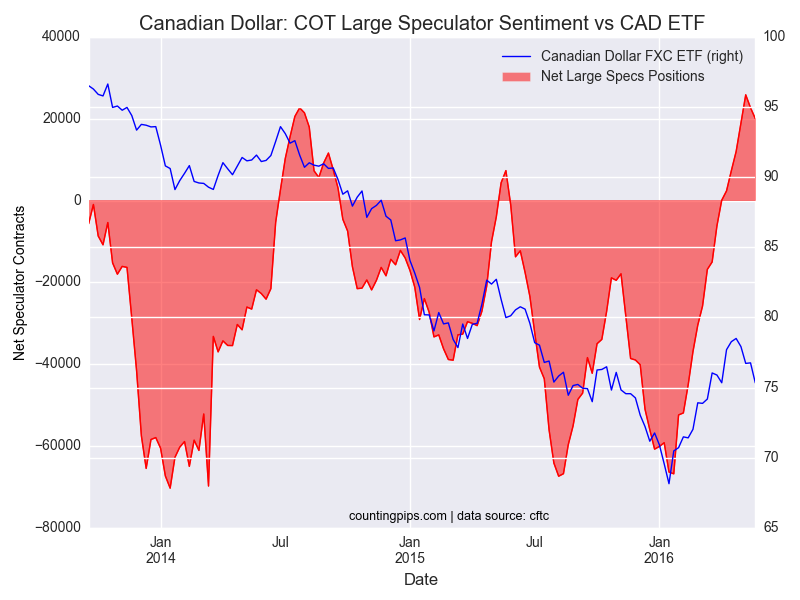

Notable changes showed that Canadian dollar positions fell for a second week after rising for the previous sixteen straight weeks while Japanese yen positions dropped sharply and have now declined for five straight weeks.

Australian dollar positions have fallen rather sharply for four straight weeks and now hold a barely positive net position of just +124 contracts.

This latest COT data is through Tuesday May 24th and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets. All currency positions are in direct relation to the US dollar where, for example, a bet for the euro is a bet that the euro will rise versus the dollar while a bet against the euro will be a bet that the dollar will gain versus the euro.

Please see the individual currency charts and their respective data points below. (Click on Charts to Enlarge)

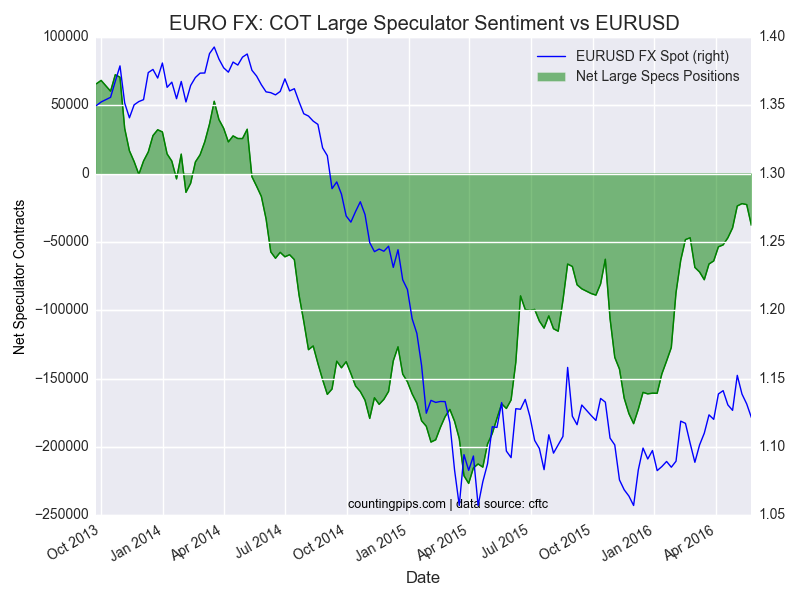

EuroFX:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | 51940 | -3863 | -46917 | 5134 |

| 20160426 | 44726 | -7214 | -39667 | 7250 |

| 20160503 | 27558 | -17168 | -23619 | 16048 |

| 20160510 | 29484 | 1926 | -21872 | 1747 |

| 20160517 | 34116 | 4632 | -22587 | -715 |

| 20160524 | 48501 | 14385 | -37895 | -15308 |

British Pound Sterling:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | 71019 | -3162 | -55152 | -3842 |

| 20160426 | 67606 | -3413 | -48669 | 6483 |

| 20160503 | 56878 | -10728 | -40408 | 8261 |

| 20160510 | 55022 | -1856 | -34935 | 5473 |

| 20160517 | 60935 | 5913 | -38422 | -3487 |

| 20160524 | 54031 | -6904 | -32835 | 5587 |

Japanese Yen:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | -76829 | -6071 | 71870 | 5680 |

| 20160426 | -67685 | 9144 | 66498 | -5372 |

| 20160503 | -65495 | 2190 | 61521 | -4977 |

| 20160510 | -63294 | 2201 | 59047 | -2474 |

| 20160517 | -62439 | 855 | 58919 | -128 |

| 20160524 | -23035 | 39404 | 22059 | -36860 |

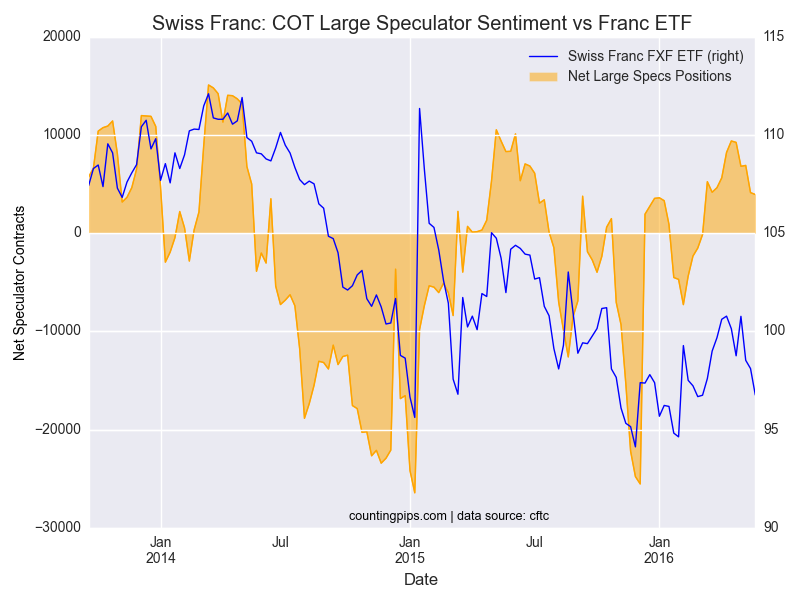

Swiss Franc:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | -10027 | -1890 | 9410 | 1172 |

| 20160426 | -4664 | 5363 | 9265 | -145 |

| 20160503 | -4870 | -206 | 6829 | -2436 |

| 20160510 | -978 | 3892 | 6917 | 88 |

| 20160517 | 4440 | 5418 | 4147 | -2770 |

| 20160524 | 11498 | 7058 | 3954 | -193 |

Canadian Dollar:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | -18065 | -7963 | 7308 | 4923 |

| 20160426 | -25684 | -7619 | 11999 | 4691 |

| 20160503 | -30745 | -5061 | 18943 | 6944 |

| 20160510 | -33890 | -3145 | 25874 | 6931 |

| 20160517 | -33527 | 363 | 22706 | -3168 |

| 20160524 | -25595 | 7932 | 20047 | -2659 |

Australian Dollar:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | -53551 | -8437 | 44106 | 8984 |

| 20160426 | -68470 | -14919 | 59540 | 15434 |

| 20160503 | -58577 | 9893 | 52395 | -7145 |

| 20160510 | -42718 | 15859 | 38158 | -14237 |

| 20160517 | -26088 | 16630 | 24893 | -13265 |

| 20160524 | -605 | 25483 | 124 | -24769 |

New Zealand Dollar:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | -5959 | -1985 | 5351 | 1059 |

| 20160426 | -9373 | -3414 | 7384 | 2033 |

| 20160503 | -10543 | -1170 | 9200 | 1816 |

| 20160510 | -9689 | 854 | 9352 | 152 |

| 20160517 | -6825 | 2864 | 6688 | -2664 |

| 20160524 | -4184 | 2641 | 4576 | -2112 |

Mexican Peso:

Last 6 Weeks of Large Trader Positions

| Date | Net Commercial Positions | Weekly Com Changes | Net Large Specs Positions | Weekly Spec Changes |

| 20160419 | 13463 | -33629 | -14409 | 32182 |

| 20160426 | 19344 | 5881 | -19315 | -4906 |

| 20160503 | 12550 | -6794 | -12420 | 6895 |

| 20160510 | 47903 | 35353 | -45220 | -32800 |

| 20160517 | 48932 | 1029 | -45691 | -471 |

| 20160524 | 50128 | 1196 | -47460 | -1769 |

*COT Report: The weekly commitment of traders report summarizes the total trader positions for open contracts in the futures trading markets. The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators). Find CFTC criteria here: (http://www.cftc.gov/MarketReports/CommitmentsofTraders/ExplanatoryNotes/index.htm).

The Commitment of Traders report is published every Friday by the Commodity Futures Trading Commission (CFTC) and shows futures positions data that was reported as of the previous Tuesday (3 days behind).

Each currency contract is a quote for that currency directly against the U.S. dollar, a net short amount of contracts means that more speculators are betting that currency to fall against the dollar and a net long position expect that currency to rise versus the dollar.

(The charts overlay the forex closing price of each Tuesday when COT trader positions are reported for each corresponding spot currency pair.) See more information and explanation on the weekly COT report from the CFTC website.

All information contained in this article cannot be guaranteed to be accurate and is used at your own risk. All information and opinions on this website are for general informational purposes only and do not in any way constitute investment advice.

Article by CountingPips.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}