By IFCMarkets

The US dollar strengthened for the 3rd straight day while no trend was observed in the stock market. The US dollar strengthened mainly on external news from Eurozone and Japan. The Dow and S&P 500 indices advanced while the hi-tech Nasdaq edged lower. Investors shrugged off the fallen preliminary US manufacturing PMI for April having focused on corporate data. The positive S&P 500 dynamics was supported by the revised-up forecast of its components’ gross earnings slump from -7.8% to -7.1% compared to the Q1 2015. Nasdaq daily loss was 0.8% on weak quarterly earnings of Microsoft and Alphabet (which owns Google). The shares of those two companies have slumped 7.2% and 5.4% respectively. Today at 16:00 СЕТ the March new homes sales will be released in the US, the tentative outlook is positive. This week the Apple quarterly report on Tuesday will be the key corporate event in the US. Moreover, such giants as Facebook, 3M, MasterCard, United Technologies, UPS and AT&T will release their quarterly statements too. The key macroeconomic event will be the results of the next US Fed meeting on Wednesday. No interest rate change is expected but the market participants will watch closely the US regulator comments on the economic performance and the possible changes in monetary policy.

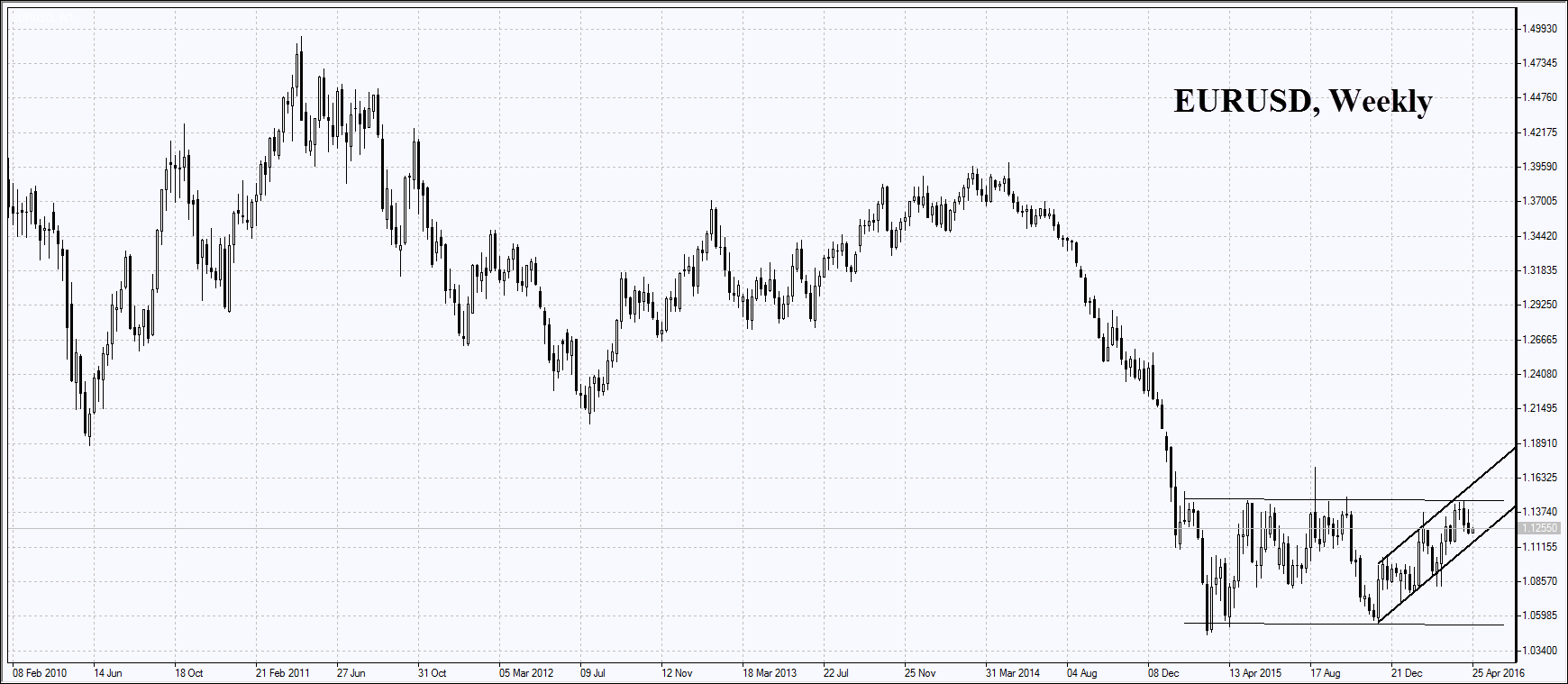

The euro fell dramatically against the US dollar after the ECB meeting last week. No changes in monetary policy and interest rates were introduced but the ECB President Mario Draghi said that interest rates will remain at the current record lows for quite a long time. The pan-European FTSEurofirst 300 stock market index edged lower on Monday. The weak business climate IFO came out in Germany for April as well as much weak corporate news. Investors did not approve of the new investment plan of the French energy company EDF which pushed its stocks 6% down. Philips announced an IPO of its lighting business and its stocks lost 5.3%. Today no significant economic data are expected in Eurozone. The most significant data will come out on Friday: inflation and GDP.

Nikkei edged slightly lower today after surging 4% last week. The yen fell against the US dollar to the lowest in 3 weeks ahead of the BoJ meeting this Thursday morning. The market participants assume the Bank may go negative in the interest rates it offers banks to borrow from it. Yen weakened 2.1% on Friday which is its record daily slump since October 2014 when the BoJ eased its monetary policy for the second time. Weak yen support the Japanese exporters and pushes their stocks up. The yen slightly corrected upwards on Monday after strong movements last week. No significant economic data are expected in Japan on Tuesday and Wednesday.

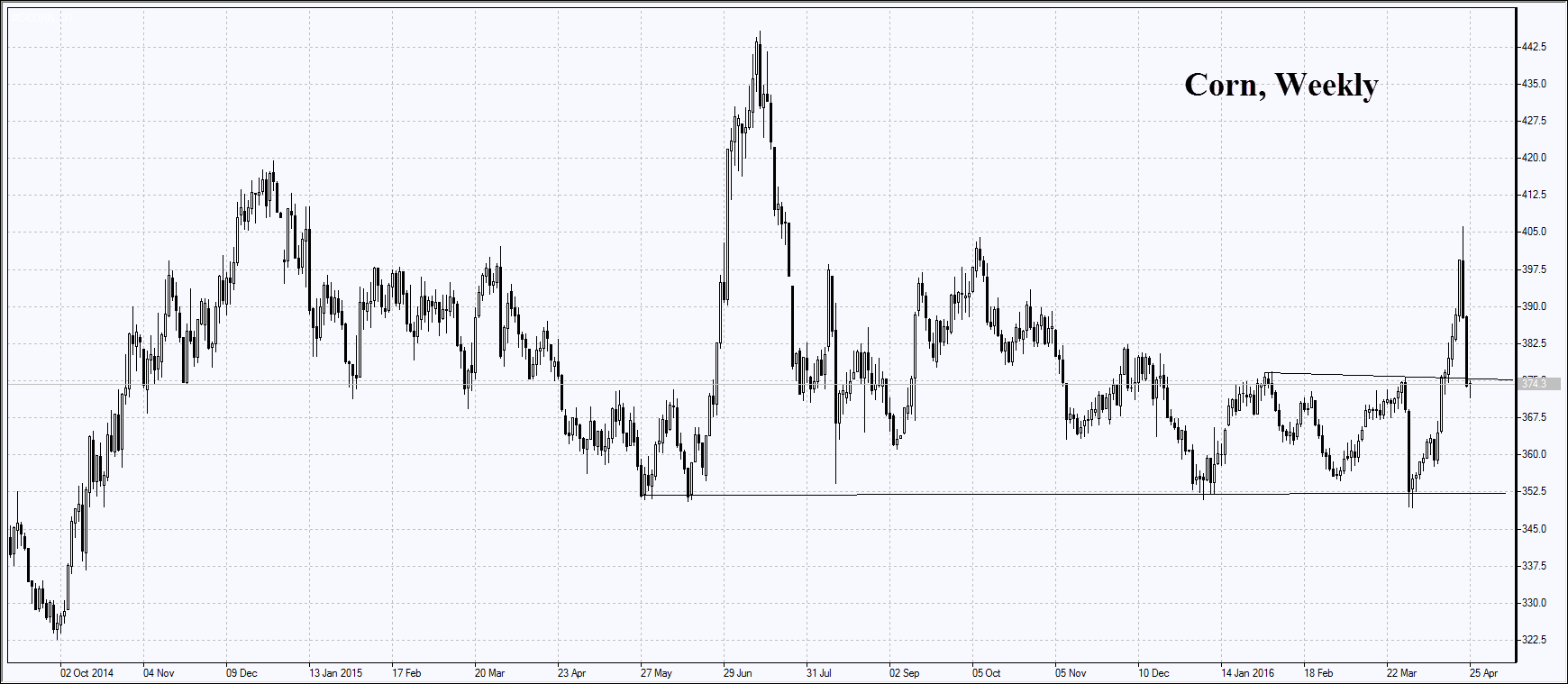

Grain futures edged lower after the explosive growth for several weeks in a row. Corn and soy edged up to the 9-month highs. After that corn slumped on Friday by 6% which has become its record daily fall in recent 3 years. Such an excessive volatility is fuelled by diverse weather forecasts from the leading meteorological bureaus. When they predict the possible drought in Latin America and US, the grains edge up in price. On the contrary, prices fall when rainy weather in expected. The prices may also edge up on the rumours Brazil is going to purchase 700 thousand tonnes of US corn for the first time in 20 years due to the poor domestic crops.

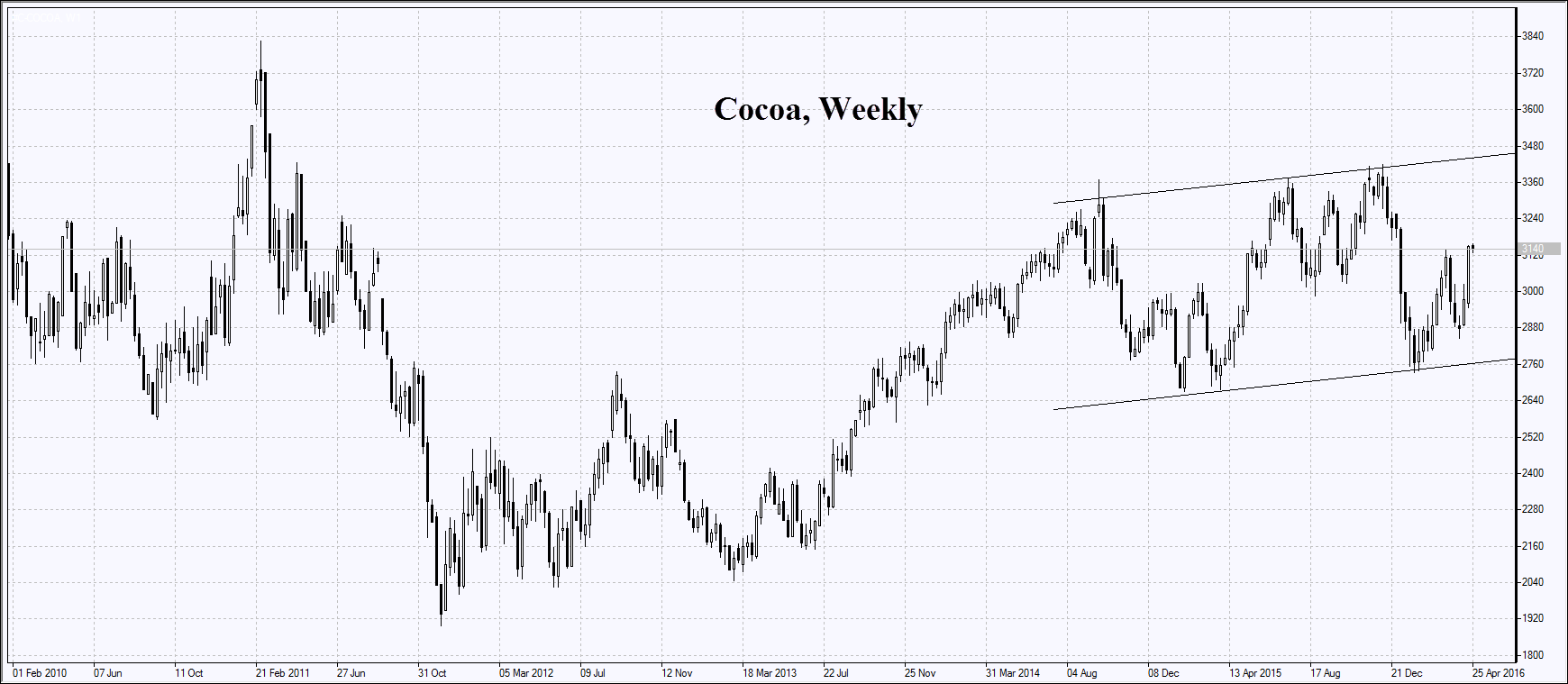

Cocoa prices showed the record weekly growth in the recent 11 months amid the continued drought in Cote-d’Ivoire and 2.9% higher demand for cocoa beans in Asia in Q1 2016.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.