American stocks become expensive along with the dollar

By IFCMarkets

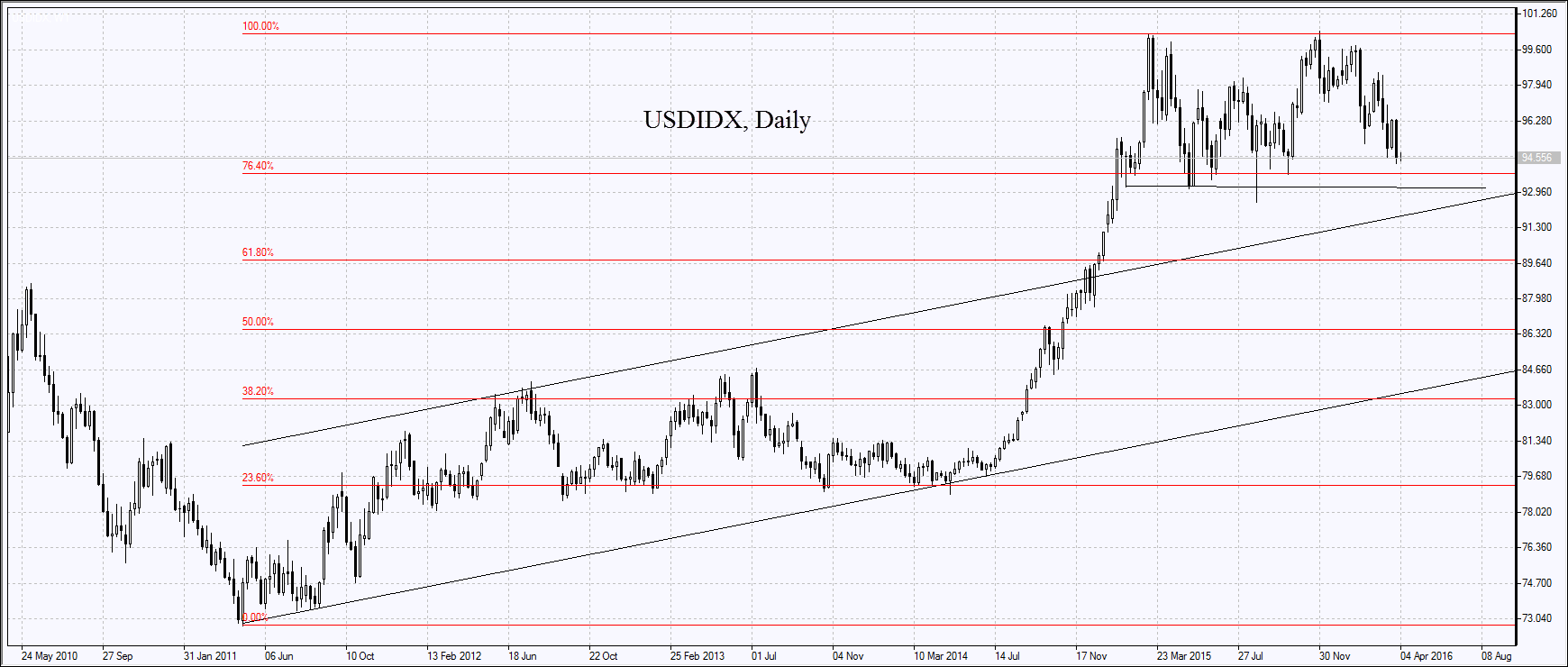

On Friday, the change in dollar was insignificant and quotations of US stocks rose. Investors reacted positively to the data on the US labor market for March. The number of new work positions in Nonfarm Payrolls was better than expected – 215 thousand. In addition, the growth of ISM Manufacturing index and increase in consumer confidence index, calculated by the University of Michigan, were also higher than expected. On Monday the US dollar index and stock index futures are demonstrating an increase despite the negative forecast on industrial demands data for February, which will be published at 16:00 CET. Market participants do not rule out that the real indicator will be better. They also expect the publication of the March Fed meeting on Wednesday, which could reveal the plans of American authorities regarding further rate dynamics. Note that according to the results of the first quarter of this year, the US dollar index dropped by almost 4%. This is its maximum quarterly fall for the last 3 years. The fall of dollar against euro in the 1st quarter of 2016 was 4.6% and was the highest since 2011. Some investors believe that the US currency looks undervalued. According to the US Commodity Futures Trading Commission, following the results of the last week net long position on dollar fell to 2-year low.

European stocks have been rising in price since Monday, following the US stock futures. Against the backdrop of cheap energy securities of energy companies Electricite de France (+ 5,6%), RWE AG (+ 4,3%) and E.ON (+ 2,6%) are in demand. Today at 15:45 monthly economic report will be released by the ECB. Tomorrow the release of data on industrial orders in Germany for February is expected, which turn out to be positive.

Оn Monday Nikkei updated the minimum for month and then rose slightly, along with other world stock indices. The yen strengthened against the US dollar despite the rise of the US currency index. Investors believe that a strong yen could have a negative impact on Japanese exporters. Stocks of Toyota Motor and Nissan Motor fell by 2.5%, and Mazda Motor – by 5.6%. On Tuesday morning the data on wages in Japan for February will be released, as well as the PMI index of business activity in the sphere of services and the composite one for March. The forecast is moderately positive.

Quotes of copper declined after the world’s largest producer – Chilean company Codelco published a review which does not expect an increase in the world demand this year. In addition, the world’s largest electricity network company State Grid Corporation of China reported a drop in investments by almost 3% this year up to 439B Yuan. Market participants are afraid of the decline in demand for copper for the production of electrical cables and other power grid equipment. Last year China’s energy consumption of copper was estimated at 9.15M tons.

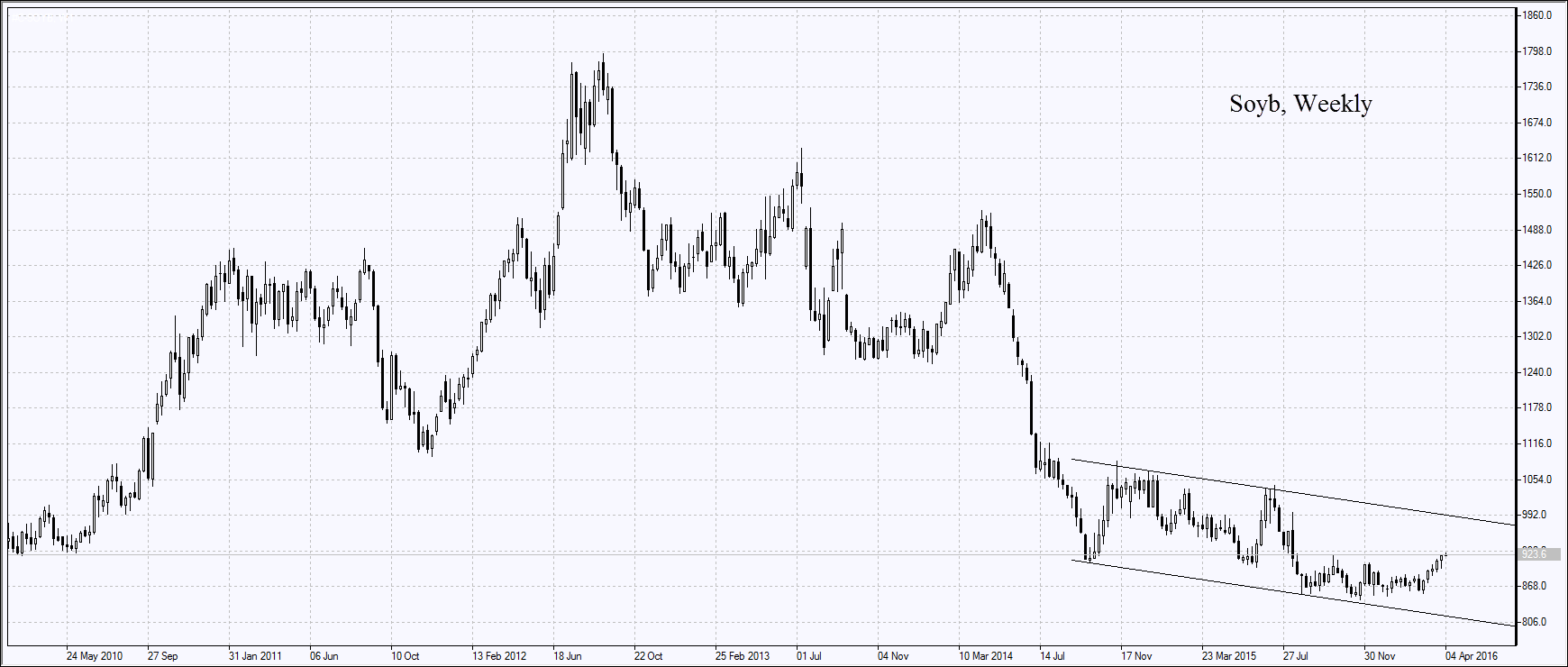

The price of soybeans reached the highest level since last August. The US Department of Agriculture (USDA) published a forecast which indicated that soybean seeds in the US could reach 82.24M Acres during this season. This is less than last year’s level of 82.65M Acres and the average evaluation of 83.06M Acres by market participants. Note that wheat seeds may also be less than last year’s level, but its price has not increased.

Free Reports:

Quotations of the corn have significantly decreased. The USDA believes that its seeds this season will amount to 93,600,000M Acres. This is much more than the last year level of 88M and the forecasts of market participants – 89,970,000M.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.