By IFCMarkets

On Monday the US stock market was on decline. The November manufacturing PMI by Markit slumped to hit a fresh 2-year low. The existing US home sales for October were below expectations. The pharmaceutical giant Pfizer acquired the Irish Allergan for $160bn. Investors’ reaction was negative driving the stocks down by 2.6% and 3.4% respectively. The dollar index live data show the index has hit a new 8-month high on expectations of the Fed interest rate hike. The probability of the hike is currently estimated at 75%, according to the CME Group FedWatch. The trading volume on the US exchanges was 6.2bn stocks which is 14% less than the 20-trading-days average. Today at 14:30 CET the second reading of the GDP for the 3rd quarter will come out in the US. At 16:00 CET the November Consumer Confidence Index will be released. The tentative outlook is positive.

The European stocks are heading south today due to the weak corporate statements. Zodiac Aerospace stocks lost 10% on the news its annual profit may decline by 45%. The retail chain Kingfisher expects its earnings to decrease by 6.6% in the 3rd quarter which pushed its stocks 3%. Today in Germany the strong macroeconomic indices by IFO were released but markets did not react on this news.

Nikkei is slightly down today in line with other stock indices. As the global metal prices continue falling, the smelters Sumitomo Metal Mining and Dowa Holdings lost 1.8% and 1.1% respectively. The Sharp stocks sky-rocketed 14% after the Kyodo News reported some of its loans may be repaid by means of the public support. The Asahi newspaper reported the Japan’s government was planning to introduce additional measures of economic support late in November. In particular, the retirement benefits and minimum wages may be increased. This news has not yet made yen weaker. Tomorrow at 00:50 CET in the morning the Bank of Japan will publish the materials of its meeting on October 30.

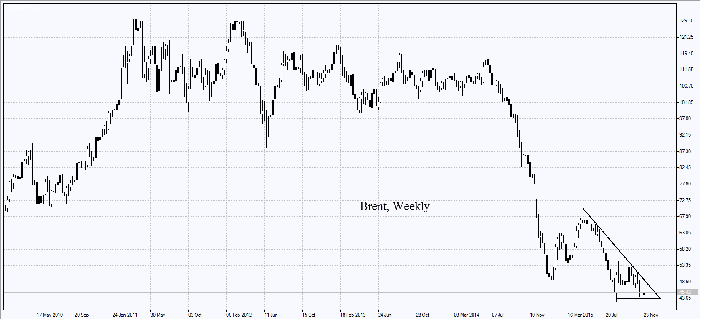

Brent oil prices increased after the crash of the Russian military airplane near the Turkish boundary. Markets are concerned with the heightened political risks in the Far East. According to U.S. Commodity Futures Trading Commission, the net shorts in oil increased by 70% since October to reach the axis since August. The net short position in oil at the ICE exchange hit a high since October 2014.

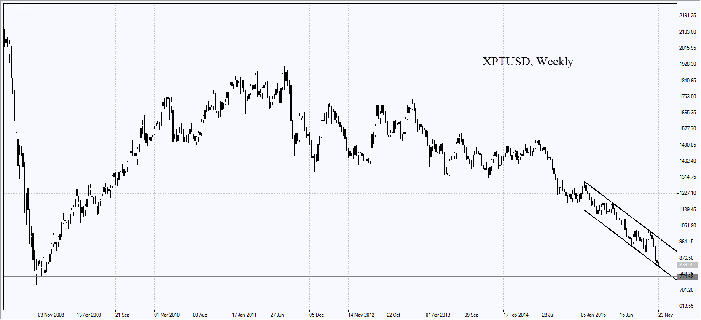

The platinum continued its way down. The World Platinum Investment Council forecasts that its deficit of 300 thousand ounces for 2015 will switch to the surplus of 5 thousand ounces in 2016. The change is to be caused by the 20% rise in platinum production in South Africa and Zambia. At the same time, the investment demand is expected to contract by 19% to 130 thousand ounces. Despite the platinum deficit, it slumped by more than 30% since the start of the year. Some investors believe the fall was excessive and wait for an upward correction.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

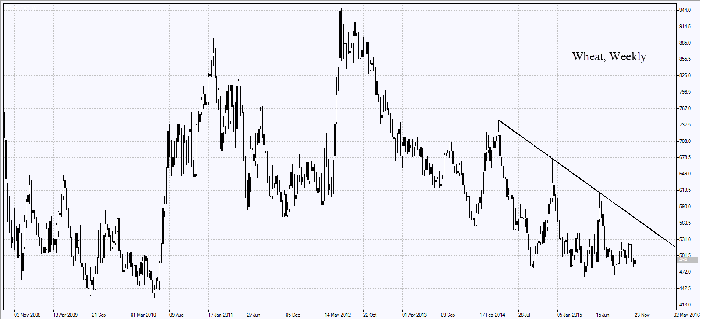

Wheat prices today were on the rise. Indian crops are delayed by extremely hot weather which may lead to the reduced yields for the first time since 2007. India is the second largest wheat producer after the US with the planting acreage of around 30mln ha.

Corn prices are up after the US Agricultural Department reported its stockpiles in China will amount only to 114mln tonnes in 2015/16. At the same time, the Chinese agencies expect the stockpiles to total 150mln. tonnes.

Market Analysis provided by IFCMarkets