By CentralBankNews.info

The European Central Bank (ECB) maintained its benchmark refinancing rate at 0.25 percent, as expected, along with its other main rates.

The ECB said its president, Mario Draghi would comment on the reasons for this decision at a press conference later today.

EURJPY: Price Correction Sets In

EURJPY- With the cross halting its weakness on Wednesday, further decline is likely in the days ahead. Resistance resides at the 143.78 level. Further out, resistance comes in at the 144.00 level where a break will turn attention to the 144.50 level and then the 144.00 level. A violation will push it further higher towards the 145.50 level. Conversely, on pullbacks support comes in at the 141.97 level where a reversal of roles as support is expected. Further down support lies at the 141.00 level where a breach will target the 140.43 level. Bulls may come in here but if this fails to occur, further decline will follow towards the 139.96 level. All in all, the cross remains biased to the upside on recovery.

Article by http://www.fxtechstrategy.com/

EUR/USD Forecast And Price Action For April 3rd

Article by Investazor.com

As I was expecting yesterday, the volatility rose around US publications. The release of the ADP did not surprise the market since it came around expectations, but triggered optimism in what concerns the NFP release from Friday. The surprise of the day came with the release of the Factory Orders. I was pretty sceptic in what concerns this release, but it surprised me as well as the market. The US Factory orders registered 1.6% rise.

These two releases have triggered dollar buying. The EURUSD dropped all the way to 1.3750. The down move was also sustain by the risk aversion triggered by the bomb explosion from the Cairo University.

See yesterday analysis: EUR/USD Forecast And Price Action for April 2nd;

Today from the Euro Area were released the Spanish Services PMI in line with expectations 54.0; Italian Services PMI below expectations and below 50.0 level (49.5) and the EU Retail Services up 0.4%. These did not have a great impact on the EURUSD quotation. The price was held between 1.3750 and 1.3770. Continue this article to see what the main events for today are and what the price action is telling traders

The following are expected next:

EU – Minimum Bid Rate (12:45). In the economic calendar the interest rate it is expected to remain at 0.25%. 57 of 60 Bloomberg analysts are expecting ECB to maintain the interest rate at current level and only 3 of them are expecting a diminish. For the moment I am also with maintaining it.

The post EUR/USD Forecast And Price Action For April 3rd appeared first on investazor.com.

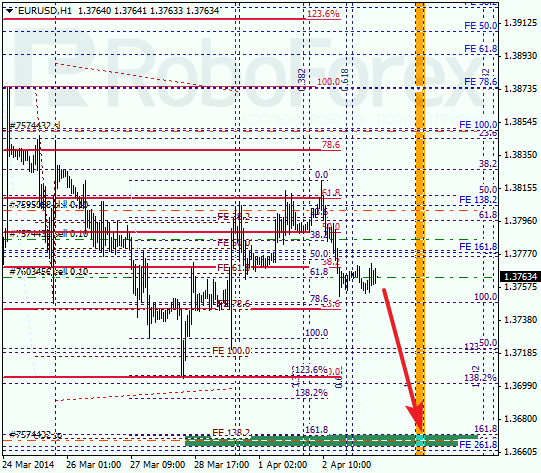

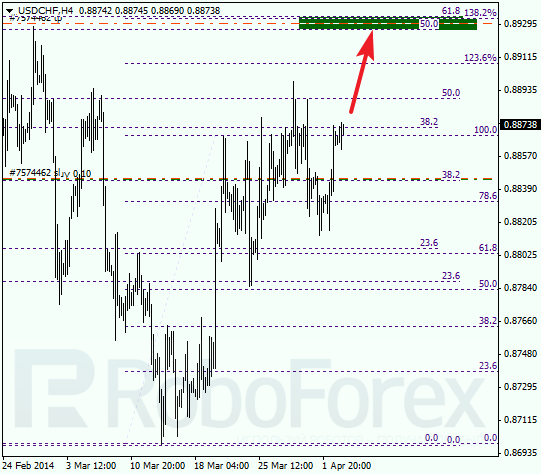

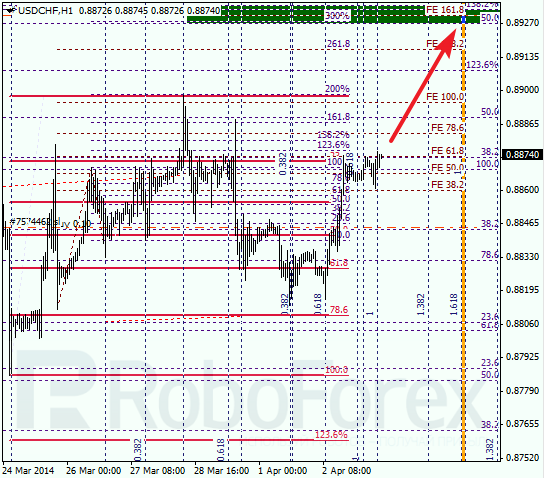

Fibonacci Retracements Analysis 03.04.2014 (EUR/USD, USD/CHF)

Article By RoboForex.com

Analysis for April 3rd, 2014

EUR USD, “Euro vs US Dollar”

Eurodollar is starting new descending movement. I opened another sell order during correction. Main target is still near the group of lower fibo levels at 1.3665.

As we can see at H1 chart, yesterday pair rebounded from local correctional level of 61.8%. Bears are returning to the market and may break latest minimum during the day. According to analysis of temporary fibo-zones, lower target levels may be reached until the end of the trading week.

USD CHF, “US Dollar vs Swiss Franc”

Franc is starting new ascending movement and I decided to move stop on my buy order into the black. Possibly, price may break local maximum in the nearest future. Target is still near the group of upper fibo levels at 0.8930.

As we can see at H1 chart, bulls were able to rebound from local level of 61.8%. Most likely, they will reach upper targets on Friday. If later pair rebounds from these levels, market may start new and more serious correction.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

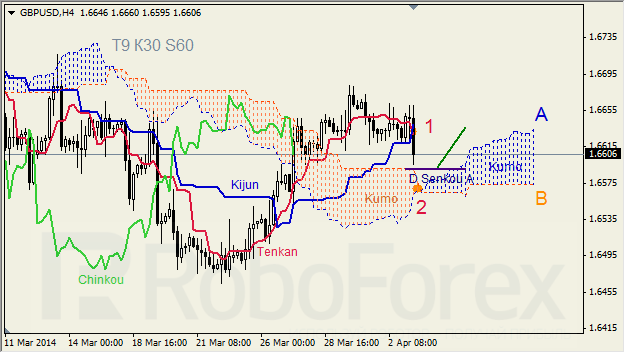

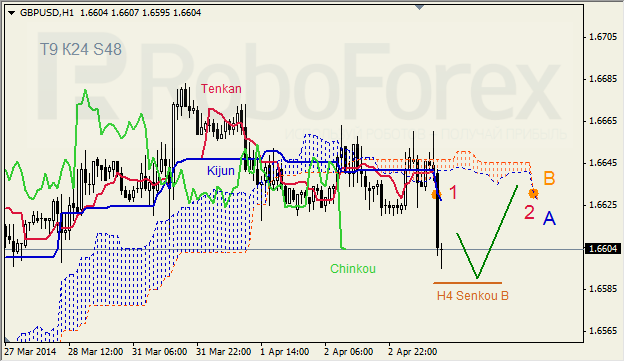

Ichimoku Cloud Analysis 03.04.2014 (GBP/USD, GOLD)

Article By RoboForex.com

Analysis for April 3rd, 2014

GBP USD, “Great Britain Pound vs US Dollar”

GBP USD, Time Frame H4. Tenkan-Sen and Kijun-Sen are close to each other above Kumo Cloud (1); Kijun-Sen and Senkou Span A are directed upwards, Tenkan-Sen is moving downwards. Ichimoku Cloud is going up (2), and Chinkou Lagging Span is on the chart. Short‑term forecast: we can expect support from D Senkou Span A, and growth of the price.

GBP USD, Time Frame H1. Tenkan-Sen and Kijun-Sen are close to each other below Kumo Cloud (1); all lines are directed downwards. Ichimoku Cloud is closed (2), and Chinkou Lagging Span is below the chart. Short‑term forecast: we can expect support from H4 Kijun-Sen.

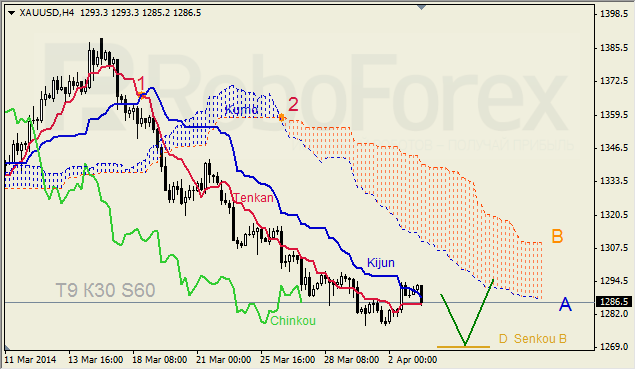

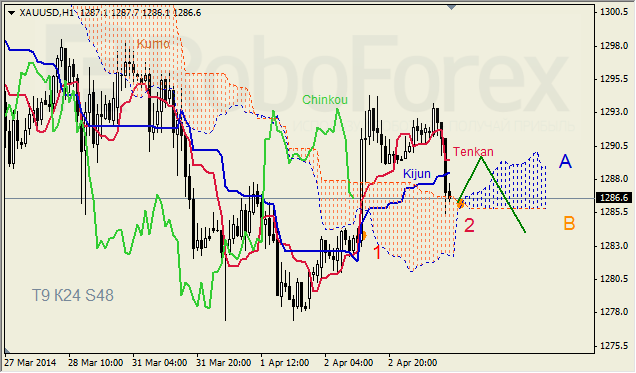

XAU USD, “Gold vs US Dollar”

XAU USD, Time Frame H4. Tenkan-Sen and Kijun-Sen are very close to each other below Kumo Cloud; Kijun-Sen is directed downwards. Ichimoku Cloud is going down, and Chinkou Lagging Span is below the chart. Short-term forecast: we can expect decline of the price towards support from D Senkou Span B.

XAU USD, Time Frame H1. Tenkan-Sen and Kijun-Sen are very close to each other above Kumo Cloud. Ichimoku Cloud is going up (2), and Chinkou Lagging Span is above the chart. Short‑term forecast: we can expect support from Senkou Span A and resistance from Tenkan-Sen.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

The One Sector Where Crash Helmets Are Advised

For months, the experts have been duking it out about whether or not the biotech sector is in a full-blown bubble.

In one corner, we have the Richard Bernsteins of the world. Even though the iShares Nasdaq Biotechnology Fund (IBB) essentially doubled in price over the last two years, they’re dismissive.

“Bubbles pervade society,” says Bernstein. “They are bigger than the financial markets. I don’t think the biotech speculation is that broad… So, no bubble, in my opinion.”

In the other corner, we have those like Reformed Broker’s Josh Brown, who believes that the bubble is plain as day.

“Anyone with a protein compound under a microscope and a clean suit can go public right now,” says Brown.

Now, I admit that the data backs Brown up.

An uncharacteristically high number of biotech companies (37) went public last year. Yet the pace isn’t letting up one bit. By March 20, another 24 biotech companies have gone public in 2014.

So is there more pain in store for biotech stocks? And, more importantly, does it really matter to investors who aren’t invested in the sector? Let’s discuss.

A Risky Proposition

Let’s be honest about one thing: If any sector in the market is pre-disposed to overheating, it’s biotech.

After all, an investment in any biotech stock is a speculation on the future sales of an unproven drug. So by nature, every bet you place in the sector is extremely hit or miss.

Yet, true to form, we’re prone to focus on the potential upside more than the downside risk. Especially since analysts tend to be exceedingly optimistic, too…

Case in point: After analyzing over 1,700 analyst forecasts, Morgan Stanley’s (MS) Matthew Harrison and Dr. David Friedman found that consensus drug sales estimates were completely inaccurate.

“Most consensus forecasts were wrong, often substantially. And although consensus forecasts improved over time as more information became available, accuracy remained an issue several years post-launch.”

And when the researchers say “substantial,” they mean substantial. “A significant number (53) of consensus forecasts were overly optimistic by more than 160% of the actual peak revenue of the product.”

If nothing else, let this be a reminder to all of us to 1) take any expectations we have about a biotech’s potential and 2) slash it in half – immediately.

Getting back to the matter of a biotech bubble, average valuations certainly appear frothy.

The IBB fund trades at a price-to-earnings ratio of 44.1 and a price-to-book ratio of 11.23, which compares to 18.0 and 2.6 for the S&P 500 Index, respectively.

So there certainly could be more bloodletting ahead. But only time will tell whether or not the 15% pullback for the sector since February 25 represents the beginning of the end, or just another breather before the next upward charge.

My take? If you’re sitting on profits in the sector, protect them with trailing stops. It’s better to be safe than sorry.

Don’t Sweat the Little Stuff

If you’re not invested in any biotech stocks, it’s only natural to still be concerned that a nasty downturn in the sector could end up sinking the entire stock market.

Fight your instincts! It’s not a legitimate concern.

Although investments in biotech stocks might represent a good measuring stick for investors’ appetite for speculation, the sector’s significance in the big picture is minimal at best.

Or, as Howard Silverblatt of S&P Dow Jones Indices notes, the market cap of the S&P biotech industry is only equal to about 2.4% of the entire market cap of the S&P 500.

Granted, that’s swelled noticeably from the 0.4% level during the height of the 1999/2000 bubble. But it’s still too small to matter much.

Put simply, even if the biotech sector disappeared completely, 97.6% of the S&P 500 would remain intact. And the overall impact on performance would be minimal.

Bottom line: We can’t be certain whether or not the impressive bull run for biotech stocks is officially over. One thing we can be certain about, though, is that no matter what happens next with biotech stocks, it won’t unduly impact the broad market.

Ahead of the tape,

Louis Basenese

The post The One Sector Where Crash Helmets Are Advised appeared first on Wall Street Daily.

Article By WallStreetDaily.com

Original Article: The One Sector Where Crash Helmets Are Advised

Strong U.S. Manufacturing Data Pushes Gold Down

Gold is seen as a safe haven for investors when other markets are too volatile. For example, when equities are on the decline, chances are gold prices will rise. For this reason, gold options traders should keep a close eye on economic data that impacts the stock and other markets to attempt to predict movement of the precious metal.

One report that has had an impact is on manufacturing, which was recently released showing U.S. factory activity increased in March. Production posted its biggest gain since the recession – a sign that the economy could be headed in the right direction after a slow winter, according to Reuters. If the economy continues to gain momentum, gold options traders should be aware the prices may fall.

However, experts say not to expect too steep of price declines, as demand could pick up if prices fall steeply.

“Given gold’s recent drop below $1,300 an ounce, we have noticed a slight increase in physical demand from Asia,” James Steel, chief precious metals analyst at HSBC, told Reuters. “Further weakness to gold prices may elicit stronger buying from the emerging markets and help cushion further losses.”

In fact, prices increased from a seven-week low based on speculation that declines could spur purchases of bars and jewellery in China, according to Bloomberg.

“People are betting on increased physical buying and bargain hunting at these levels,” Phil Streible, a senior commodity broker at R.J. O’Brien & Associates in Chicago, told Bloomberg.

With an improving U.S. economy driving gold prices down, and the potential for Chinese demand pushing it the other way, a boundary option on gold could be a good move right now if traders can identify upper and lower levels in which they believe gold prices will remain.

The post Strong U.S. Manufacturing Data Pushes Gold Down appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

The History of Debt, Money and Gold

The future of money dominated the World War D conference — but Greg Canavan’s presentation charted the history of money.

His first task was to define money. Why would you define money? It’s just the stuff you put in your wallet, right?

Well Greg gave the audience this simple definition: money = credit = debt. All money created in the economy is simply debt.

Think about it. When you take out a loan, the bank assesses your credibility and then credits your account — money is created out of thin air. It happens on a bigger scale with business loans too.

But it wasn’t always like this, said Greg.

Up until 1914 gold was money. Money was not debt, it was not credit, it was simply gold. The classical gold standard ensured only the credible borrower got credit, and most of the credit extended was business credit.

It was a stable system, but when the First World War came along the system couldn’t cope. There was a run on banks, which led to shrinking credit and shrinking money supply. Gold’s virtue is that it acts as a natural break on the economy when things start to heat up, but as the First World War ramped up this virtue became a failing.

And so in 1922 the system was slowly unravelled with the introduction of the Gold Exchange Standard, which allowed British pounds and US dollars to be exchanged for gold. It ‘…enabled countries to pay for goods and services with debt. Money stopped being gold and became debt,’ said Greg. ‘The world went on a massive credit expansion, leading to the roaring twenties, technological advancement and a global stock market boom.’

Booming debt, technological advancement…does it sound familiar? Greg went on: ‘Credit was created to the point where anyone with a shred of credibility could borrow.’ The system was unsustainable, and the Great Depression struck in 1929, ending the world’s addiction to debt.

‘It took many, many years for the world to accept debt again,’ said Greg. After the depression, the credible person saw debt as something to be avoided, and it had major implications for the financial system.

So another system was introduced in 1944. Known as the Breton Woods System, it pegged gold at the rigid price of $35 per ounce. And for a while the system worked and the global economy chugged along nicely.

But by 1960 the first strains hit. The gold price spiked to $40 an ounce in London, which was a ‘major warning sign something wasn’t right in the system,’ according Greg. It doesn’t sound like much of a price shock, but prior to this the gold price moved in the range of 5–10 cents. So in the early 1960s the US, the Bank of England and European banks got together to control the price of gold by secretly trading with each other — this was known as the London Pool System. That also worked — but only for a while.

Again, war brought shock to the system. Following its decision to invade Vietnam the US printed a lot of money. That money flowed through the global system, and people who ended up with US dollars in their hand decided to swap their dollars for gold. By 1968 volumes in the London gold market spiked massively, forcing the US to fly plane loads of gold to the UK every week.

When the gold market eventually closed for two weeks to cope with the shock, the unofficial price of gold was $44 per ounce. It took another three years for the US to move on from the gold standard entirely.

So what does that tell us about today? ‘If you take a step back and realise the flow of money is slow to manifest in larger changes, it makes you realise these things take time to evolve,’ said Greg. ‘We know the current system [of huge debts] is absurd but could quite possibly go on for 5–10 years. When you think something is unsustainable, it is.’

Today’s unsustainable global finance system took off in the 1980s as debt to GDP exploded, led by what Greg termed ‘iceberg finance’.

(Catch Greg’s full presentation by snapping up the World War D DVD now. Go here for details.)

The tip of this iceberg, the small visible part, is securitisation. That’s where banks package up the debts on their balance sheets and sell them as securities.

The mostly invisible mass of the submerged iceberg is the shadow banking system where hedge firms, investment banking and insurance companies exist, lending large sums to borrowers.

But to facilitate this lending, securities are swapped between borrowers and lenders as a form of collateral. The same securities are passed on and on to the point where one Treasury note supports a whole bunch of credit.

It’s as dodgy as it sounds, and prone to collapse, according to Greg. ‘It’s not going to take much of a chink in the chain to bring that system down,’ he said.

We saw the disastrous effects of shadow banking when Lehman Brothers went under. It was using securitised mortgage debt as collateral to borrow money and speculate. As a property market collapse swept through everyone realised that this collateral had no value. This caused a run on the banks that nearly brought the whole financial system down with it.

This is how the world got lumped with QE. Greg said that after the financial crisis, government debt was the only form of collateral left in 2008. But Governments can’t just go to the bank to get a loan when they want debt. The government requires the market to buy its debt, but without liquidity in the market, that’s impossible. QE provided this liquidity, so government borrowing could continue. Global debt is now US$100 trillion and perceived credibility — the belief that this debt will be paid back — is all that’s keeping it together. With QE set to ease in the future, what will happen?

‘I’m not sure how the world is going to cope,’ said Greg.

Greg recommended a prudent approach to navigating this risk. ‘Gold is a great wealth preserver over the long time.’

Holding on to a decent amount of cash is very important too — since no one knows when the proverbial will hit the fan. So too are good value, quality stocks — though Greg believes there aren’t any around at the moment. The search for yield and dividends mean most of the quality stocks in the market are overpriced and share markets look set to deliver very low long term returns at these prices, according to Greg.

If the history of money is anything to go by, then you can bet on a bumpy ride ahead.

Callum Denness

For Money Morning

From the Port Phillip Publishing Library

Special Report: ASX: 15,000

Satyajit Das on Economic Growth, Interest Rates and Central Banks

Satyajit Das, a man gifted with a unique insight into financial markets, was welcomed to the stage at the World War D conference on Tuesday. Part of his introduction was a mention that he doesn’t own a mobile phone.

Yes, that’s right. Apparently it’s news if someone doesn’t own a mobile phone.

The crowd politely laughed. Das wasn’t here to talk about technology, so it didn’t matter that he doesn’t own a mobile phone.

What did matter to the audience was Das’s take on the current mess we call a financial system…

Now Das is an entertaining speaker. His turn of phrase and emphasis had the masses laughing almost every minute. But underneath every line to elicit a giggle or snort was a serious message.

As he stood in front of the attendees, he opened with ‘Problems, what problems? We’re rich. Every minute of every day the Dow makes a new high.’

He then bombarded the audience with truly frightening statistics to demonstrate the absurdity of this statement.

Like the fact that Japan’s market is almost 50% below its all-time highs, and Australia’s share market is about 20% below its all times high. ‘But,’ he paused, ‘You are rich.’

Alarming the crowd further were the inflation-adjusted figures for superannuation over the period of 2000–2013. His calculations show we’re only up 3.51% on average. ‘But again, you ARE rich,’ Das told the room.

If anyone knows how to keep a crowd hanging, it’s Das. From here, no one dared shift in their seat…just in case they missed some valuable information from his rapid-fire presentation.

Americans on food stamps have risen to 47 million today, from 27 million in October 2007. These are essential, he argued, to keep people from rioting in the streets. He may have been joking. But that one line demonstrates two things: The rise in poverty in a ‘rich’ nation and the increasing dependency on the government to provide.

Moving on, Das wanted to ‘…look at the real economy, where they don’t shuffle papers around.’

But looking at the real economy paints a bleak picture, Das noted.

America needs US$1.6 trillion to create US$300 billion dollars of ‘growth’ in the economy. What’s more, debt levels haven’t been this high since the Napoleonic Wars.

Emerging markets, America and the other countries considered ‘rich’, financialised their economies. They spend more time shuffling assets and financial engineering rather than any real engineering.

Increases in debt levels, financial imbalances and entitlement culture were the causes of the crisis Das tells us.

‘The real solution is to reduce debt, reverse the imbalances, decrease the financialisation of the economy and bring about major behavioural changes,’ says Das.

‘But rather than deal with the fundamental issues, policy makers substituted public spending, financed by government debt or central banks, to boost demand.’

What no politician or central banker will ever tell you, expresses Das, is that we need a 30% drop in gross domestic product.

The historically low interest rates also got a mention from Das on Tuesday. This, he reasons, continues to create imbalances in the economy. However central banks have to keep fiddling with the interest rate. Simply because no one in the Western world has sustainable debt.

‘As an example’ Das explains, ‘a 1% rise in rates would increase the debt servicing costs to the US government by around $170 billion. A rise of 1% in G7 interest rates increases the interest expense of the G7 countries by around US$1.4 trillion.’

Without economic growth, you can’t pay back your debt. However, there is no economic growth. So interest rates won’t go any higher for now.

He points out when then Federal Reserve Chairman Ben Bernanke announced QE3 — quantitative easing — Bernanke said himself that it would not significantly increase economic activity directly.

This leads to the relevance, and perhaps stupidity, of central banks.

Forward guidance, he declared is an abused term in the central bankers handbook of doublespeak.

‘Nobody actually believes central banks anymore,’ he declared.

He likens their language to something similar to a Monty Python skit.

One European Central Bank member said last year, that ‘[forward guidance is] a change in communication but not in monetary policy strategy.’

Or this, from the current US Federal Reserve chairwoman, Janet Yellen. ‘If I thought that was a situation we will likely encounter in the next several years we would probably have revised our forward guidance in a different way. We revised it as we did, eliminating that language because it didn’t seem at all likely.’

However, Das said, nothing ever lives up to the comments from Alan Greenspan (former Fed Chairman): ‘I know you believe you understand what you think I said, but I am not sure you realise that what you heard is not what I meant.’

Later, Greenspan added: ‘If I have made myself clear then you have misunderstood me.’

Finally, when the crowd stopped laughing, Das reminded everyone that, ‘They get paid to do this.’

After the sledging on central bankers was over, he moved on to how we get out of this mess.

And right now, there is no ‘stage left’, according to Das.

Higher interest rates will crash the economy. And the actual limit of money printing isn’t known yet. Das wondered aloud just how much more the world can handle.

Policy incompetence, ‘pointy heads in financial markets’ and plenty of people talking but not actually saying anything aren’t going to dig the world out of the ongoing financial calamity.

From here, Das reckons there’s no path to normalisation. Perhaps secular stagnation or slow global bankruptcy.

More likely, he thinks we’re looking at a life of financial repression from governments. ‘After all, isn’t the art of taxation to pluck the goose with the least amount of hissing?’

With that, he offered the crowd a tip or two on where to stick their money (hint: it’s not shares). And then told the attendees ‘there’s no way out.’

Shae Smith+

Contributing Editor, Money Morning

PS: We captured Das’s full 90 minute presentation on tape. You can find out how to watch it, plus more than 15 hours-worth of other intriguing material and financial insight from the conference, here.

The Most Profitable Gas in the World

By OilPrice.com

There is only one certainty in Ukraine: The energy sector must and will be transformed, and how long this takes will depend on who ends up in the driver’s seat and how serious they are about becoming a part of Europe and reducing dependence on Russia. But by then, investors will have missed the boat.

The driving factor for any energy investor in Ukraine is the pricing environment. There is nowhere else in Europe—or some would even argue in the world—where you are going to get significant access to resources and potential resources for the price. Gas is selling at $13.66/Mcf, while it costs $4-$5 to produce and operate. That means producers are netting anywhere between $8 and $9/Mcf.

Whether it likes it or not, kicking and screaming, Ukraine will have to transform its energy sector, if it hopes to see promised IMF money. Kiev will have to start selling off assets and making the industry much more transparent. Greater transparency coupled with an already-favorable gas price environment, will make Ukraine one of the best places to be over the next 5-7 years.

While everyone is now closely watching the campaigns unfold in the run-up to 25 May presidential elections, in the end who wins the presidency—and even the energy ministry—will determine not if, but how fast the country moves to transform its energy sector.

The crucial next step is a psychological one: Ukraine’s new leaders must come to the realization that their energy assets, particularly the pipeline system, are not strategic assets, rather they are valuable commercial assets. Privatizing these assets could raise $50 billion.

Right now, the pipeline system is nothing but a conduit for Russian gas into Europe. It could be much more. The pipeline system, and the state-run company that manages it, should be turned into a transparent public company in London, for instance. The sale of 50% of the company could generate sizable profits—half of which could be used to pay down debt to Russia, while the other half could be invested in modernization, turning a potentially valuable assets into a commercially realistic one.

Without the right people in place in the new government, we could perhaps lose a year in getting the necessary reforms in place. And continued talk about the “strategic” nature of these assets could cause investors to lose faith in Ukraine’s seriousness about reducing its dependence on Russia. Eventually, it will happen, and what elections will tell us simply is how long it will take.

There are a lot of resources to be developed in Ukraine, and there are also quite a few companies who have assets they cannot development, primarily due to lack of funding or marginal management teams. These companies will now be seeking to transact with larger players.

Historically, the most significant red flag for new investors in Ukraine has been working with the government. It’s too early to determine whether that will change. Bureaucracy generally kills deals more than anything, and foreign companies coming in will never be able to understand how the bureaucracy works. The smart investor will employ capital through a Ukrainian private entity to maximize investment dollars. Western management teams, without help from local partners, won’t be able to operate in this venue even if they are top-notch managers.

The smart investor will also realize that there is no better time to invest in Ukraine’s energy sector. Once it is transformed, the best opportunities will have been seized.

Source: http://oilprice.com/Energy/

By Robert Bensh of Oilprice.com