By CentralBankNews.info

Thailand’s central bank cut its policy rate by 25 basis points to 2.0 percent, saying “downside risks to growth have risen in the wake of the prolonged political situation” and that “monetary policy has some scope to ease, in order to lend more support to the economy and ensure continuous financial accommodation.”

But it was a close decision with the Bank of Thailand’s (BOT) Monetary Policy Committee voting by 4 to 3 to reduce the rate, with the minority doubting that a rate cut would help boost growth as the weak economy is due to political unrest that has unnerved consumers and kept tourists away.

The three members of the committee that voted to maintain rates were quoted as saying the bank’s policy was already accommodative and the main headwinds to growth were not financial in nature.

“Monetary policy should be used when it is effective in supporting the economic recovery,” the bank said, a sign of how intense the committee’s debate had been.

The BOT cut its rate by 50 basis points in 2013 and at its last meeting in January it voted by 4 to 3 to maintain rates, with three voting for a rate cut. At that time it also said political unrest was weighing on the growth outlook and cut the 2014 growth forecast to 3 percent from a previous forecast of 4 percent.

A narrow majority of economists had expected the BOT to cut rates today, with those expecting the central bank to maintain rates citing stable inflation.

Thailand’s headline inflation rate rose slightly to 1.96 in February from 1.93 percent in January with the Thai baht strengthening slightly in the last month after falling sharply in 2013 as political unrest added to the general negative international sentiment toward emerging market currencies.

The BOT noted that core inflation had edged up but remained subdued. Core inflation rose to 1.22 percent in February from 1.04 percent the previous month. The BOT targets core inflation of 0.5 percent to 3.0 percent.

“Growth of the Thai economy slowed through the final quarter of 2013 and January 2014 from domestic demand amid lower private confidence,” the BOT said, adding that tourism has felt more of an import from the political situation.

Thailand’s Gross Domestic Product rose by only 0.6 percent in the fourth quarter of 2013 from the third quarter for annual growth of 0.6 percent, sharply down from a rate of 2.7 percent in the third quarter.

“Prolonged political uncertainties would continue to impede the recovery of private consumption and investment,” the bank said.

But economic growth should be supported by a gradual recovery of exports, the BOT said, adding that the global economic had continued to recover in the last two months, led by the major economies.

Thailand’s exports eased further in January to US$ 17.907 billion, the fifth month in a row with declining exports.

Along with many other emerging market currencies, the Thai baht fell from late April 2013, hitting a low of 33.075 to the U.S. dollar on Jan. 7, 2014, a drop of 13.5 percent. But since then the baht has recovered somewhat, trading at 32.44 to the dollar today, down 0.7 percent since the start of 2014.

Protestesters accused the former prime ministers, Yingluck Shinawatra, of corruption and are still occupying parts of the capital of Bangkok. A general election in February was disrupted by the protesters, leaving Yingluck with a caretaker government with limited powers to act.

http://ift.tt/1iP0FNb

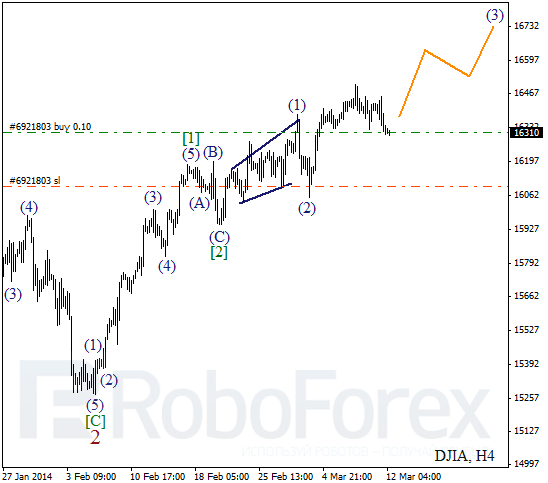

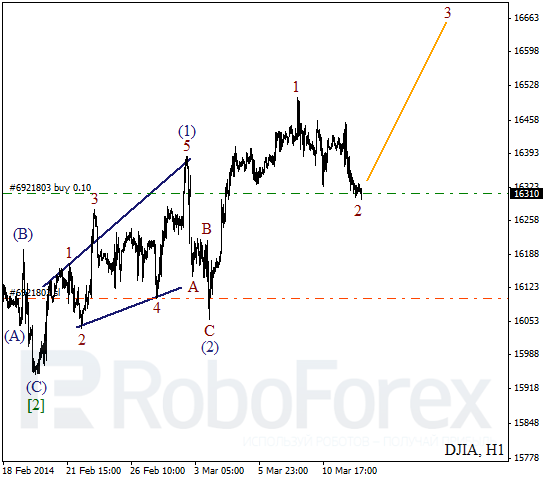

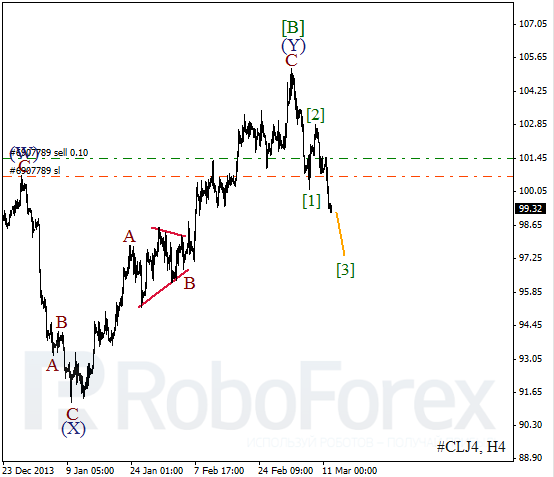

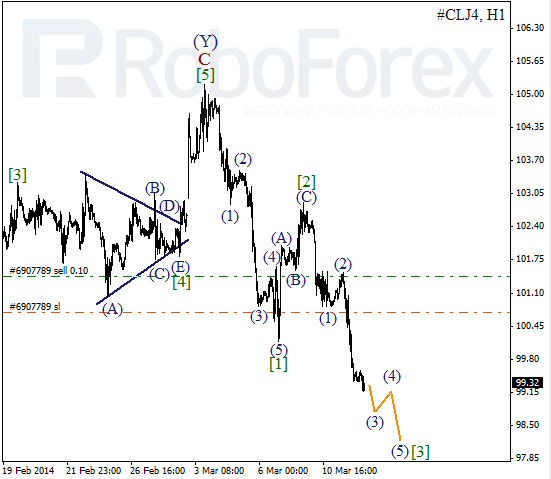

Wave Analysis 12.03.2014 (DJIA Index, Crude Oil)

Article By RoboForex.com

Analysis for March 12th, 2014

DJIA Index

In case of Index, main trend is still bullish despite slight correction. Possibly, in the nearest future may continue forming extension inside the third wave. Critical level here is minimum of wave (2).

As we can see at the H1 chart, after completing zigzag pattern inside wave (2), Index formed initial impulse inside the first wave on minor wave level. Current chart structure implies that pair may have already finished local correction. I’ll increase my long position as soon as price starts new ascending movement.

Crude Oil

Oil is falling down; bears have already broken minimum of the first wave. It looks like right now price is forming the third wave. Stop on my buy order is already in the black; I’m planning to increase my position during correction.

More detailed wave structure is shown on H1 chart. After completing short impulse inside wave (C) of [2], Oil started falling down inside the third one. In the nearest future, price is expected to finish wave (3) and start local correction.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Crude Prices Trades Lower as US Crude Supplies Climbs

Crude prices extended losses, falling for a third day, the longest losing streak in two month following the release of the latest API stockpiles report which revealed demand growth concerns in the world’s largest oil consuming country.

The North American WTI crude for April delivery dropped 0.83% to $99.19 per barrel on the New York Mercantile Exchange at the time of writing. While Brent crude for April settlement slid 0.37% lower at $108.16 per barrel on the ICE Futures Europe exchange at the same time.

The European benchmark crude was at a premium of $8.88 to WTI.

Crude – Ukraine

The ongoing tension between Russia and Ukraine over the Crimean region continues as the Ukrainian government appealed to the Western nations for help on Tuesday to help fight against Russia’s aggression in Crimea, which is still preparing for a referendum on joining Russia on March 16.

US Crude Supplies

On Wednesday, the American Petroleum Institute (API) released reports which revealed crude stockpiles at Cushing, the delivery point for WTI contracts, dropped by 1.31 million barrels in the week ending March 7.

According to the API report, crude inventories added 2.6 million barrels to 367 million, in the week ending March 7, compared to analysts forecast of an increase of 2.2 million barrels.

Distillate inventories, including heating oil and diesel, declined by 839,000 barrels, the industry group in Washington confirmed.

A separate report from the Energy Information Administration (EIA) is expected to be released later in the day.

According to the monthly Short-Term Energy Outlook released on Tuesday, the North American West Texas Intermediate could possibly average $95.33 per barrel this year.

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today

The post Crude Prices Trades Lower as US Crude Supplies Climbs appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Australian Dollar Drops on Weak Consumer Sentiment

The Australian dollar declined for a fourth day against the greenback on Thursday after reports from Westpac revealed consumer sentiment dropped to its lowest since May last year while home loans dropped.

The Australian dollar traded 0.18% lower at $0.8958 at the time of writing, following the release, after trading close to $0.8967 earlier in the session.

Australian Dollar – Weak Sentiment

Australia’s consumer sentiment index dropped 0.7% to 99.5 points in March, the lowest level since May last year and compared to the previous reading of 100.2 points seen in February, according to the Westpac-Melbourne Institute Consumer Sentiment gauge. A figure below the 100 mark indicates more consumers were pessimistic than optimists.

“The degree of concern around jobs is very high,” Westpac senior economist Mathew Hassan said in the statement on Wednesday. “We retain our view that rates will remain unchanged over the first half of 2014, but with two further 25bp rate cuts in the second half.”He also added “More recent falls though have had a very clear theme centering on a sharp loss of confidence in the economic outlook and escalating job-loss fears.”

The latest figures from the job market revealed unemployment climbed to a ten-year high of 6% in January, while the participation rate came in at an eight-year low of 64.5%. The labour market report for February is expected to be released on Thursday, with the jobless rate and participation rate forecasted to remain unchanged.

The sub-index tracking consumer which tracks the views on the outlook conditions over the next year fell 4%, following the fall of 7.1% seen in February, reports from Westpac confirmed.

Home Loans

Meanwhile in the housing sector, the number of loans granted to purchase or build homes was unchanged in January from the previous month, after it dropped by 3.3% from December, the statistics bureau said today.

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today

The post Australian Dollar Drops on Weak Consumer Sentiment appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Fibonacci Retracements Analysis 12.03.2014 (EUR/USD, USD/CHF)

Article By RoboForex.com

Analysis for March 12th, 2014

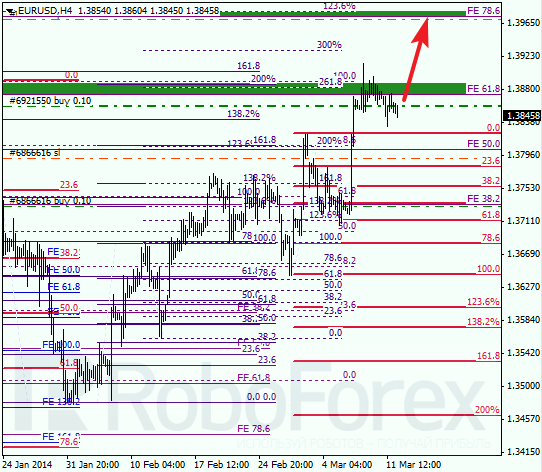

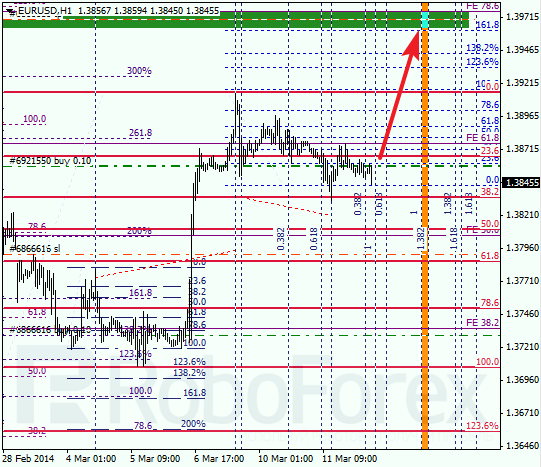

EUR USD, “Euro vs US Dollar”

Eurodollar is still being corrected. Earlier market rebounded from level of 61.8% and then started growing up. Most likely, bulls will each their target at level of 1.3970 in the nearest future.

Yesterday bulls rebounded from local level of 38.2%. It looks like price is going to start new ascending movement. According to analysis of temporary fibo-zones, upper target levels may be reached during the next 24 hours.

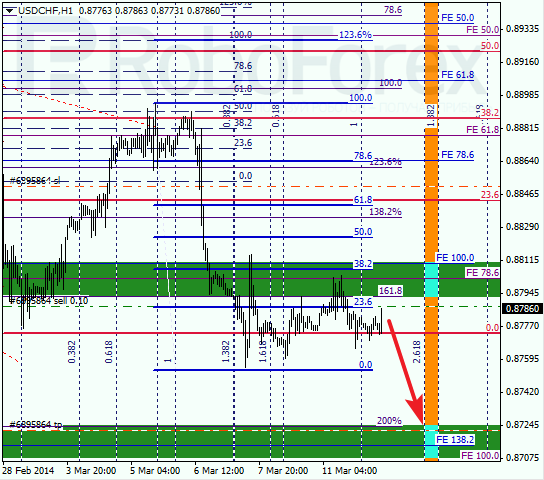

USD CHF, “US Dollar vs Swiss Franc”

Franc is still consolidating. Last week, pair rebounded from level of 38.2% and then bears reached new minimum. Main target is still close to several lower fibo levels at 0.8720.

At H1 chart we can see, local correction reached level of 38.2%. According to analysis of temporary fibo-zones, predicted targets may be reached on Wednesday. Later these levels may become starting point of new correction.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Investment Firm Smashes Record, Notches 99.92% Win Rate

Prepare to be stupefied…

Over the course of 1,238 trading days – from January 1, 2009 to December 31, 2013 – Virtu Financial had one day in which it lost money. One!

Let that sink in for a moment… 1,237 days of profits and only one day of losses.

And we thought J.P. Morgan’s (JPM) stretch of 365 days of trading without a loss was impressive?

I assure you, this isn’t the stuff of Bernie Madoff. It’s not a statistical anomaly. It’s the stuff of high frequency trading (HFT). And it’s totally legit.

Today, I want to share two ways you can get a piece of the action. So let’s get to it…

Believe the Hype

On Monday, New York City-based Virtu Financial filed IPO plans with the SEC to raise up to $100 million. Although no date has been set yet, it plans to list on the Nasdaq under the ticker VIRT.

And it’s in the IPO prospectus where we find this mind-blowing chart, showing the company’s daily net trading income.

You’ll note, there was only one day, during 2012, when the firm lost money. Every other day, Virtu pocketed anywhere from $500,000 to upwards of $5 million in profit.

Such a hefty daily haul explains the $624 million in “trading income” the company reported last year, as well as the founder’s $114 million NYC mansion.

So how does the company do it?

Per the S-1: “We stand ready, at any time, to buy or sell a broad range of securities, and we generate revenue by buying and selling large volumes of securities and other financial instruments and earning small bid/ask spreads.”

To be clear, the company doesn’t speculate. Instead, its strategies are “designed to lock in returns through precise and nearly instantaneous hedging.”

It simply provides liquidity, scalping pennies on billions of market orders, which clearly add up over time.

Here’s the most shocking revelation in the S-1: “If our risk management system detects a trading strategy generating revenues outside of our preset limits, it will freeze, or ‘lockdown,’ that strategy and alert risk management personnel and management.”

In other words, if the company is making too much money in a particular market, it shuts down trading, just to be safe. Don’t we all wish we had that problem?

If You Can’t Beat ‘Em…

Virtu’s runaway success reveals something we’ve known for a long time: Markets aren’t even close to being efficient. If they were, Virtu couldn’t survive – let alone thrive.

Despite what you’ve been told to the contrary, even the most liquid and widely traded securities aren’t efficient.

Case in point: On March 3, the bid-ask spread on the SPDR S&P 500 ETF (SPY) became inverted for 500 milliseconds, according to Cristian Zarcu of TradeDynamiX.

That means the bid price was above the ask price for half a second. Not by a little bit, either. At one point, the spread reached as high as $0.09 ($184.24 versus $184.15).

In a world where HFTs like Virtu can trade inefficiencies down to the millisecond, this represented a free lunch.

And if this is going on in an ETF that sees the heaviest trading, rest assured, it’s going on elsewhere in the market, too.

So how can we compete against the “can’t lose” profit machines that are HFTs? We have two options:

We can either concede defeat and invest right alongside them by buying into Virtu’s IPO. (Yes, I’ll let you know when the stock begins trading.)

Or we can go where HFTs can’t – micro caps.

As my friend and fellow micro-cap specialist, Ian Cassel, points out, they represent the last inefficient market cap class where individual investors like us hold a distinct advantage.

How so? Well, Wall Street analysts routinely ignore micro caps. In fact, over 40% of companies with market caps of less than $300 million have no analyst coverage. That allows us to uncover meaningful information first – before it’s reflected in share prices.

At the same time, daily trading volume in micro caps is way too infrequent for HFTs to even bother.

Bottom line: Although we can’t duplicate the exact trading successes of companies like Virtu, we can generate more than enough profits in micro caps to make it worthwhile.

Ahead of the tape,

Louis Basenese

The post Investment Firm Smashes Record, Notches 99.92% Win Rate appeared first on Wall Street Daily.

Article By WallStreetDaily.com

Original Article: Investment Firm Smashes Record, Notches 99.92% Win Rate

Paul Adams: Investor-Friendly Australian Projects Around the World

Source: Kevin Michael Grace of The Mining Report (3/11/14)

http://www.theaureport.com/pub/na/paul-adams-investor-friendly-australian-projects-around-the-world

Rather than shoot for the stars, Paul Adams of DJ Carmichael argues that junior miners should focus on more modest projects best suited to maximizing shareholder value. This means projects with reasonable capex, good grades and short turnaround times. In this interview with The Mining Report, Adams suggests gold, copper, iron ore and rare earths projects that can weather the complete commodities cycle, as well as a fascinating gold-silver outlier in Peru.

The Mining Report: After over two years of gloom, we’re seeing renewed optimism regarding mining equities in North America. Is there similar optimism in Australia?

Paul Adams: There is, but the change in sentiment is pretty much in its infancy down here. We recently undertook some analysis of the returns from the various subindices in the market. The small resources index here in Australia is at about +4.3% for 2014 compared to a -8% return for December. The recent surge in the gold price has certainly helped lift the mood. Newcrest Mining Ltd. (NM:TSX; NCM:ASX), our largest-cap gold stock, has risen about 63% since its recent lows in December.

The materials sector in Australia is tied closely to sentiment on Chinese growth, and headwinds there tend to have major repercussions. Both BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK) and Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK) have had really strong starts, but they’re pulling back a little now as the price of iron ore landed in China has dropped about $10. But those two companies have such a heavy weighting on the materials index that it’s really difficult to get a full picture of what’s going on.

TMR: With regard to China, how much growth do you foresee?

PA: Five years ago, China’s GDP growth was around 12%. Obviously, as the size of the Chinese economy increases, they can’t continue growing at that speed. We expect growth in the 6.5–7.5% range for the next year or two.

TMR: What’s your 2014 outlook for precious and industrial metals prices?

PA: We think the current gold price is about right, plus/minus $100 per oz ($100/oz). Wobbles in the emerging markets have prompted gold’s recent move up into the $1,300/oz range. We’re seeing gold coming back as an alternative investment, a bit of a safe haven.

We’re relatively bullish on platinum and palladium given conditions in Southern Africa.

TMR: What about silver?

PA: I don’t see a major diversion from the current gold/silver ratio.

TMR: How about industrial and critical metals?

PA: The consensus data for the industrial metals generally looks positive for 2014 and into 2015. Obviously, we want to see what effect the Indonesian ban on raw exports will have. That’s very important to nickel prices.

Zinc and lead should be reasonably well supported. There is very muted mine supply growth. As the global economy improves, there are going to be some increases in industrial demand for those particular metals. There’s softness in the copper market. With the consensus price probably falling below $7,000/ton, inventories are growing. These data are conflicting, however, and copper has a history of staying up longer than many had anticipated.

TMR: You’ve said that juniors should choose appropriately sized projects in order to have the best chance of generating shareholder wealth. Could you expand on that?

PA: In a post-global-financial-crisis and post-metals-boom world, we’re seeing a lot of companies with large projects that can’t get financed. Investors today want to see projects that can weather the complete commodities price cycle. Our view is that we would rather see a good management team take on a Tier 2 or Tier 3 project in a good jurisdiction with a reasonable capex and a reasonable timeframe, rather than a Tier 1 project they ultimately won’t be able to develop without joint ventures.

TMR: With regard to timeframe, how long is too long?

PA: A project that looks like it’s going to take much longer than four to five years to get into production is probably a little bit too far out.

TMR: What’s the danger zone for capex?

PA: It depends on the economics of the individual project, but I think a capex north of about $600–700 million ($600–700M) is pretty high. The sweet spot for small companies is somewhere up to $200–250M.

TMR: Is it difficult for mining companies to keep expectations modest? Isn’t there a natural tendency to shoot for the stars?

PA: With many mining companies, management has come from majors such as BHP, Rio Tinto or Freeport-McMoRan Copper & Gold Inc. (FCX:NYSE). They’re used to dealing with big projects and big budgets. There’s a degree of relearning when you’re in a small company; you have to be quick, nimble and you must count the pennies. There is a tendency to shoot for the stars, with the belief that maybe you’ll settle for the moon. But the statistics tell us this isn’t likely to happen.

We look for teams that have a measured approach to development because smaller projects are easier to develop without overly diluting shareholders in the process. Some management teams forget about that. They’re so intent on making a huge discovery that they forget about the shareholders along the way.

TMR: Which jurisdictions do you like best now?

PA: Certain parts of South America offer good opportunities. We particularly like Chile. The other emerging jurisdiction for Australian Stock Exchange (ASX)-listed companies is the United States. Nevada would certainly be front and center, then Arizona, then parts of Utah and Wyoming.

TMR: Chile is politically and socially stable, but concerns have been raised about infrastructure, in particular, deficiencies of water and electricity. What do you think of this?

PA: We’ve been to Chile three or four times over the past three years, and water and electricity are major issues. For instance, Barrick Gold Corp.’s (ABX:TSX; ABX:NYSE) Pascua Lama capex has blown up. To get water to the high Andes, it must be pumped from the coast. And if you’re not close to existing infrastructure, power costs are a major hurdle.

TMR: What companies do you like in Chile?

PA: We’ve followed Hot Chili Ltd. (HCH:ASX) for quite a long time now. We like the way management went about targeting its copper projects. Back in 2009, there really wasn’t much of a junior presence in Chile. Two or three companies dominated most of the belts, in particular, Corporación Nacional del Cobre (CODELCO). Hot Chili didn’t go into the country looking to see what was on offer. It went there with certain criteria in mind. It then sought areas that fulfilled that criteria and found, negotiated and acquired three projects very quietly.

Hot Chili chose projects in the iron-oxide-copper-gold (IOCG) belt. The advantage there over the high Andes projects is stark. They’re low altitude, close to the coast and close to infrastructure, so development hurdles will be lower.

TMR: Hot Chili did over 100,000 meters (100Km) of drilling at Productora last year. How productive was it?

PA: Productora has increased in size quite dramatically. If you have a footprint several kilometers long, that requires quite a bit of drilling to get it up to reserve status. The company wants to move its current resource, now mostly in the Inferred category, into the Measured and Indicated categories. And its delineation drilling at Productora has enabled it to do just that.

In addition, Hot Chili made several new discoveries through the application of some very clever geochemistry. That opened up a second front for exploration to keep expanding the resource base and that required further drilling over and above the delineation drilling.

TMR: When can we expect a reserve announcement from Productora?

PA: Very soon. Toward the end of Q1/14.

TMR: The estimates that I’ve seen for Productora’s capex are in the $600–650M range. How will Hot Chili raise that capital?

PA: That’s a good question, and I have to note that a capex of this size is pushing our envelope with respect to what we think is appropriate for a small company. But Hot Chili is in a favorable position. The relationship between the company and its major partner in the project, Compañía de Acero del Pacífico (CAP), Chile’s largest iron ore producer, is extremely important.

I think we shall see an infrastructure agreement between Hot Chili and Compañía de Acero del Pacífico, which will bring access to port and rail and access to an infrastructure corridor to bring seawater to Productora. An agreement would facilitate capex certainty and perhaps reduce the capex slightly. Of course, it is no secret that there are other majors interested in this project.

TMR: Lundin Mining Corp. (LUN:TSX) owns more than 8% of Hot Chili. How significant is that?

PA: Lundin has been very active in Chile and has a strategy to expand its presence there. Will it be part of Productora at the end of the day? We’ll have to wait and see, but we wouldn’t be surprised.

TMR: What do you make of Hot Chili’s second project, the Frontera copper-gold project?

PA: Like Productora, Frontera is surrounded by Compañía de Acero properties. It has quite a lot of potential to become a project that would feed into this infrastructure hub idea Hot Chili is trying to generate. It’s a porphyry deposit, larger than Productora but lower grade. But, again, its geographical location gives it certain advantages.

TMR: What’s your rating and target price for Hot Chili?

PA: We rate it a Buy with a target price of $0.99. We think that 2014 is going to be a critical year for the company. We expect that the ownership of Productora will become somewhat more certain.

TMR: Which ASX iron ore project do you like?

PA: Amex Resources Ltd. (AXZ:ASX). It has the Mba Delta Ironsand project in Fiji. Initial capex is about $125M, and in December it secured a $100M debt-financing facility. In January, it entered into a $100M construction and procurement agreement. The project has, in fact, started. We like this because operating costs are less than $30/ton for its product. Mine life stands currently at 20 years, and there is a lot of opportunity to push that out to 45 years.

The Fijian government wants the delta dredged because it will reduce the risk of flooding to the surrounding area. So it’s a win-win, really: increasing employment and government revenue, as well as improving the environment. Mba is a really good example of a long-life, cash-producing asset with 100% ownership. This is what we mean when we talk about an appropriately sized project.

TMR: From this side of the world, Fiji is not a name one normally associates with the mining industry.

PA: Recent political events in Fiji have raised concern, but don’t forget, Fiji has a very long mining history. Most famous is the Emperor gold mine, which operated for decades. Placer Dome, before it got taken over by Barrick, had a big copper exploration project called Namosi.

TMR: What’s your rating and target price for Amex?

PA: We rate it a Speculative Buy with a target price of $2.15.

TMR: Let’s talk about critical minerals projects.

PA: One manganese project we liked the look of a couple years ago was Spitfire Resources Ltd. (SPI:ASX) South Woodie Woodie project in the Pilbara district in Western Australia. The company was looking to follow up on its initial exploration success at Contact and Contact North. Numerous lookalike geophysical targets were generated through 2012 and 2013. These were drilled last year, and manganese was discovered.

Management decided subsequently that the exploration necessary to fully assess its numerous opportunities would result in an uncertain outcome, and potentially very dilutionary to shareholders. So the company elected to try and find a partner.

TMR: What’s your rating and target price for Spitfire?

PA: Because of pending negotiations on South Woodie Woodie, we rate it a Hold.

TMR: How about rare earth elements (REEs)?

PA: Considering the activities of Lynas Corp. (LYC:ASX) and Molycorp Inc. (MCP:NYSE), we believe pricing in the light rare earth elements (LREEs) is going to be soft going forward. So we decided that our interest is only in projects dominated by heavy rare earth elements (HREEs). There are only three or four of those on the ASX.

We’ve elected to look at Northern Minerals Ltd. (NTU:ASX), which has the Browns Range HREE project in Western Australia. Northern has recently announced a massive increase to its resource base, which is now close to 50,000 tons (50 Kt) contained total rare earth oxides (TREO). That’s from a resource of 6.5 million tons (6.5 Mt) at about 0.75%, of which the Wolverine project is the flagship. A Wolverine feasibility study is scheduled for completion in late 2014.

The key to all REE developments is definitely metallurgy. Northern Minerals is blessed with one of the simplest mineral assemblages, dominated by xenotime. So here we have a company with 100% ownership, a fraction of the capex common to its peers and a very reasonable potential timeframe to production.

TMR: I’ve been told that REE projects that require huge production to become profitable are dubious because of the scarcity of end users. How does Northern stack up in this respect?

PA: The important thing here is the distribution of metals. Molycorp, for instance, does have to move very large amounts of material because the pricing for the lights is relatively soft. They can’t produce a lot of HREEs without producing a lot more LREEs. That’s the catch-22. But if you have a small, high-grade project like Northern’s that is dominated by HREEs, then you get a pricing advantage, and overproduction is not a problem.

TMR: What’s your rating and price target for Northern Minerals?

PA: We rate it a Speculative Buy, but don’t currently have a price target. We are awaiting results from their pilot project. So far, however, TREO recoveries are looking extremely good.

TMR: Are there any ASX-listed gold producers that have caught your interest?

PA: We look to low-cost gold producers that, again, can withstand the commodity price cycle. In 2006, for example, we took an early position in Medusa Mining Ltd. (MLL:TSX.V; MML:ASX; MML:LSE). Medusa had a high-grade, vein-style system in the Philippines, and its valuation exceeded $1 billion ($1B). Some of the personnel who were involved in Medusa moved to Kingsrose Mining Ltd. (KRM:ASK), which is exploiting a similar, high-grade, narrow-vein deposit in Sumatra in Indonesia called Way Linggo. Its costs after silver credits are going to be somewhere in the region of $300–400/oz, similar to Medusa’s.

TMR: Kingsrose trades now at $0.35. That’s rather modest considering its outstanding production cost, no?

PA: You’re right. Kingsrose currently has a market cap of about $116M. It has made a number of alterations to its milling circuit. It also had a tough year in 2013 following the death of a miner. However, after going through the necessary administrative hurdles, the company now anticipates full approval to recommence its production. We believe that when production begins again, likely in March or April, it will ramp up to its 40 Koz target relatively quickly.

TMR: What’s your rating and target price for Kingsrose?

PA: We rate it a Speculative Buy with a target price of $0.60.

TMR: How about ASX-listed gold projects in Brazil?

PA: We had followed Cleveland Mining Co. Ltd. (CDG:ASX) and its Premier gold mine. We liked its team, but we’ve also seen that Brazil has been very hard for ASX-listed gold producers. I think most of the problems there are geological because the gold tends to be very nuggety and discontinuous in some of these high-grade veins. We want to see Cleveland get a little bit further down the track before we feel comfortable reinitiating coverage.

Orinoco Gold Ltd. (OGX:ASX) has the Cascavel project in Brazil. We’re waiting for some further confirmation on its continuity of mineralization. It’s very hard to get a grade determination in some of these projects because of the nuggety nature of the gold.

TMR: Any other ASX companies you’d like to mention?

PA: One that has caught our eye is Inca Minerals Ltd. (ICG:ASX). It has the Chanape project in Peru. Several midtier and major mining houses are now requesting site visits and signing confidentiality agreements. So that gives you an indication that there is something going on there. Initial exploration was centered on gold- and silver-rich breccia pipes that outcrop on surface. More than 90 have been identified.

Our view is that these breccia pipes coalesce at depth to some degree, but a hole drilled from surface came up with a 108m interval at 2 grams per tonne (2 g/t) gold and 41 g/t silver. The last three holes drilled have targeted the deeper porphyry parts of the system. Through some really good geochemistry and some geophysics, Inca has determined the vectoring on the central parts of the system. So the indications are that it is getting closer. Hole 11 intersected a 460m-long intersection of porphyry and hydrothermal breccias with the most amount of visible metal seen so far. That tells you they are on the right track. Technical comparisons have been made to the Toromocho project, located 30Km away.

TMR: Whose project is that?

PA: Chinalco (Aluminum Corporation of China Limited) (ACH:NYSE). That’s a 2.15 billion ton (2.15 Bt) project bought for $750M and currently in construction. Inca is not saying that it has another Toromocho. What it is saying is that it has geological characteristics that display a similar complexity and similar alteration to Toromocho: near-surface, epithermal breccia-style mineralization that overlie a porphyry system.

Inca is ticking boxes with respect to the technical aspects of the project, and that’s what has piqued the interest of the majors that now want to have a look. Chanape does not fit our thesis of small companies choosing small projects, but there are always exceptions to the rule. It’s early days yet, but this could be quite exciting.

TMR: You don’t cover Inca Minerals yet?

PA: Not yet. We’ve written a couple of short notes on it. We’re extremely interested to see where their latest hole comes in with respect to grade. If results are similar to the first, we’ll be looking at this company a lot more seriously.

TMR: Paul, thank you for your time and your insights.

Paul Adams is a geologist and head of research at DJ Carmichael. He has 16 years of experience in the mining industry, in Australia and elsewhere, and was previously chief geologist and evaluations manager at Placer Dome’s Granny Smith mine. He is a member of the Australian Institute of Mining and Metallurgy and has a Graduate Diploma in Applied Finance and Investment from the Financial Services Institute of Australasia.

Want to read more Mining Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for The Mining Report and provides services to The Mining Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Mining Report: Hot Chili Ltd. and Northern Minerals Ltd. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Paul Adams: I or my family own shares of the following companies mentioned in this interview: Hot Chili Ltd. and BHP Billiton Ltd. (which is included in my Superfund). I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8999

Fax: (707) 981-8998

Email: [email protected]

The Future in Smartphones and What Apple Will do Next With the iPhone

Apple set the tech world buzzing recently when it dropped hints about its next wave of products.

Chief Executive Tim Cook, speaking at Apple’s annual general meeting, promised that new products were in development. The company spent $32 Billion on R&D last year.

Cook was cagey about specifics. But tech watchers reckon the next generation of Apple products will involve wearable technology and maybe even TVs.

Apple has long been a leading innovator with its iPhone, but to get a sense of what’s coming next in smartphones it’s worth looking at their competitors.

The smartphones enroute to oust the iPhone

Google for instance announced that its long-awaited smartphone should come on to the market next year. It should retail for around US$50.

While that price may seem low, if you look at what’s happening in the smartphone world at the moment it’s not all that surprising.

The biggest growth is at the affordable end of the market, as companies like HTC, Nokia and Samsung tap emerging economies in Asia and Africa.

And it makes a load of sense. After all, there are 2.5 billion people living in just China and India- that’s 36% of the world’s population.

Analysts had been expecting Apple to release a more affordable product last year.

Instead we got the iPhone 5C, which was cheaper than their premium phone, but not by much.

Apple is losing market share, but doesn’t seem that bothered. It’s focussing on profitability instead, which at the moment is paying off.

Where to from here for the iPhone – and smartphone innovation in general?

When it does release its new iPhone, Apple’s efforts will be heavily scrutinised.

While competition in the affordable smart phone market is growing, so too is innovation, and the tech giant must keep up to date in order to remain dominant.

Google’s phone for instance, will be modular in design. That means customers can easily customise their device by putting it together in pieces like Lego!

And in a sign that consumers are becoming more concerned about privacy, Boeing has launched a destructible phone. In the US a new encrypted device called Blackphone is taking off.

And while Apple’s iPhone hasn’t changed all that much in size, the average screen size of smartphones continues to gallop ahead as people want bigger screens in order to watch more video content.

Apple may be wealthier than many small countries, but it will be left behind unless it matches the innovation of its competitors.

Callum Denness

Contributing Editor, Money Morning

Join Money Morning on Google+

Rising Tension in Ukraine Pushing Gold Higher

It appeared as though tensions in Ukraine were on the decline last week, when Russian President Vladimir Putin said military action would only be used as a last resort, but major global markets are still being impacted by the international situation.

Investors who trade gold should be keeping a close eye on Ukraine, as prices increased early this week, with worries over war tensions.

“Market players remain cautious,” Guillaume Dumans, co-head of research firm 2Bremans told Reuters. “There’s a lack of enthusiasm in chasing stocks, and some are just thinking about moving to the sidelines after the roller-coaster ride we’ve had since the start of the year.”

One of the biggest concerns is that Ukraine’s acting president announced the formation of a volunteer national guard. Meanwhile, the ousted leader continues to insist that he is the country’s true president. Russia has yet to acknowledge the current administration in Ukraine, which has many worried that the situation could end with military action.

Ukraine also began military drills with residents of Crimea expected to vote on whether or not they want to join Russia in a March 16 referendum.

“The Ukraine situation situation is lending support to gold,” Frank McGhee, the head dealer at Integrated Brokerage Services LLC in Chicago, told Bloomberg. “The fear premium is back because of the developments.”

Gold has already increased 12 percent this year, following the biggest decline since 1981 in 2013. Until the situation in Ukraine is resolved, gold may continue to rise, so this is something investors should keep a close eye on moving forward.

The post Rising Tension in Ukraine Pushing Gold Higher appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Why a Rise in Australian Unemployment Will Mean Lower Wages

The Australian unemployment rate is now at 6%. That’s the highest level in decades. Unfortunately, the job loss tally seems to be growing: Toyota, Alcoa, Qantas…

But sacked workers aren’t the only ones facing bad news.

While Employment Minister Eric Abetz warned that Australia faces a ‘wages explosion’, the problem Australians are facing is the exact opposite.

Australian wages are falling quickly

There are a number of factors at play here. First, many of those who have recently lost their job will have to take lower positions at much less pay.

As unemployment in Australia grows, wage growth will flatline. After all, when people are grateful just to get a job, they won’t quibble about the pay.

The same principle applies to people already in a job. When there is a queue of unemployed people clamouring for your job, people are less likely to ask the boss for a pay rise.

And it shouldn’t be a surprise if your boss cuts your hours, either. In order to cut costs in the slowing Australian economy, bosses are slashing their wages bills by cutting hours. According to the ABS, underemployment is at 2010 levels.

Rising unemployment is not the only culprit for lower wages

But it’s not just growing unemployment at play here, either. Dun and Bradsheet’s business survey forecasts capital investment to rise by 19% this year.

This has the potential to lower wages in certain jobs as new hires are frozen in favour of capital investment and automation.

And here’s the final factor that’s pushing wages down: the Australian Government.

They’re sending the message to businesses that they should take a hard line in employee pay negotiations.

Eric Abetz accused employers of being ‘weak kneed’ in their dealings with employees, and blamed Toyota and SPC Ardmona’s troubles on high wages.

The government has also asked the Fairwork Commission — which is reviewing penalty rates — to take into account the concerns of business and the wider economy when it makes its decision. In other words the Government is siding with employers.

It’s not a new concern for the government. Tony Abbott and Eric Abetz have spoken previously of the negative effects of penalty rates on employers, while the issue of cutting penalty rates is a hot topic among back benchers.

Victorian Liberal MP Dan Tehan is the latest, saying he thought penalty rates should be cut and that he wasn’t alone in the Liberal party.

Between unemployment, job losses and low wages, the year is looking bleak for workers in Australia. Don’t expect a pay rise.

Callum Denness

Contributing Editor, Money Morning

Join Money Morning on Google+