By CentralBankNews.info

Norway’s central bank held its policy rate steady at 1.5 percent and said growth prospects had weakened recently which implies “that the key policy rate should be held at the current level in the period to summer 2015 and be increased gradually thereafter.”

“The increase in the key policy rate is now forecast to occur one year later than projected in September,” Norges Bank Deputy Governor Jan Qvigstad said in a statement.

In September the central bank forecast that rates would be maintained at the current level until the summer of 2014 and then gradually raised. But last month the bank dropped this guidance, saying any rise in interest rates among key trading partners had been pushed further in the future.

Norges Bank, which last cut its rate in March 2012, said inflation had been lower than expected in the past two months, growth will be lower than forecast, house prices had declined and wage growth may be somewhat lower than projected.

On the other hand, the Norwegian krone currency had depreciated considerably.

“On balance, there are prospects that consumer price inflation will be somewhat lower than previously projected,” Qvigstad said.

Wave Analysis 05.12.2013 (EUR/USD, GBP/USD, USD/CHF, USD/JPY)

Article By RoboForex.com

Forecast for December, 2013 can be found here.

Analysis for December 5th, 2013

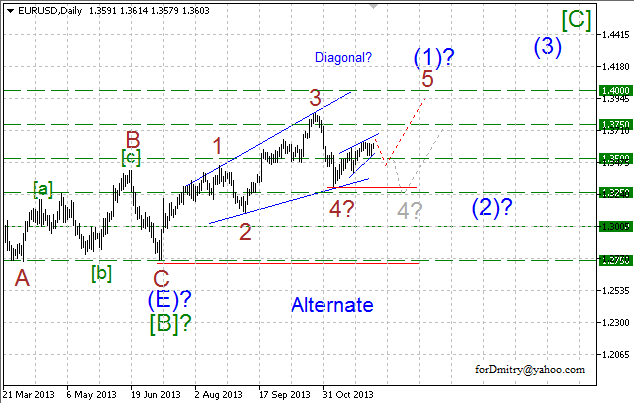

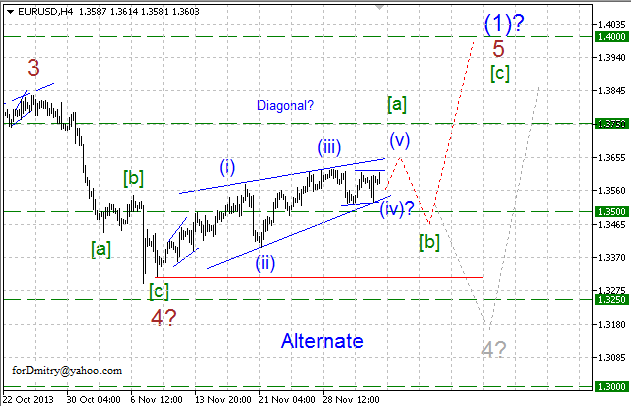

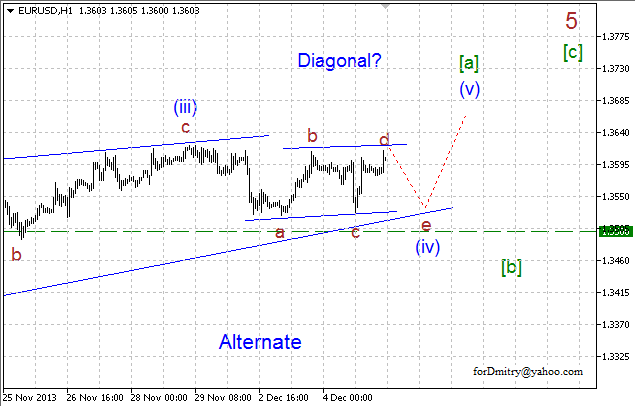

EUR/USD

Probably, mid-term ascending trend inside wave [C] started with diagonal triangle (1) of [C], which is about to be completed.

Possibly, right now price is finishing large ascending diagonal triangle (1) with final zigzag 5 of (1), which started with diagonal triangle [a] of 5 of (1).

Probably, price is finishing diagonal triangle [a] of 5, which may be followed by local descending correction [b] of 5.

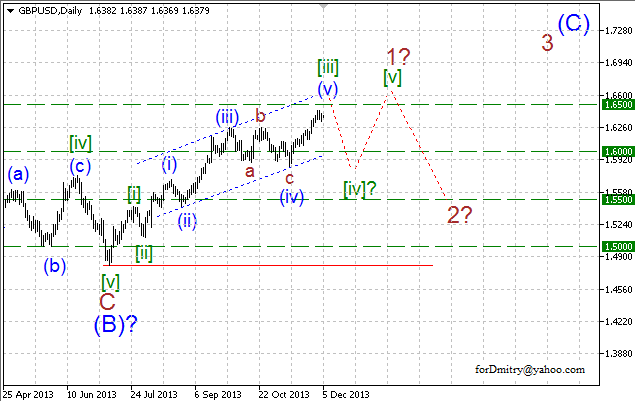

GBP/USD

Possibly, Pound is forming mid-term ascending trend inside large impulse (C). Right now, pair is finishing ascending impulse 1 of (C).

Probably, price is finishing ascending impulse [iii] of 1, which may be followed by descending correction [iv] of 1.

Possibly, price is completing ascending impulse [iii] of 1], which may be followed by descending correction [iv].

USD/CHF

Probably, Franc is forming large descending zigzag A-B-C of (5) of [C]. Right now pair is finishing its first part, descending diagonal triangle A of (5).

Possibly, Franc is forming diagonal triangle (a) of [v] of A of final descending zigzag [v] of A.

Probably, price is completing descending diagonal triangle (a) of [v], which may be followed by local ascending correction (b) of [v].

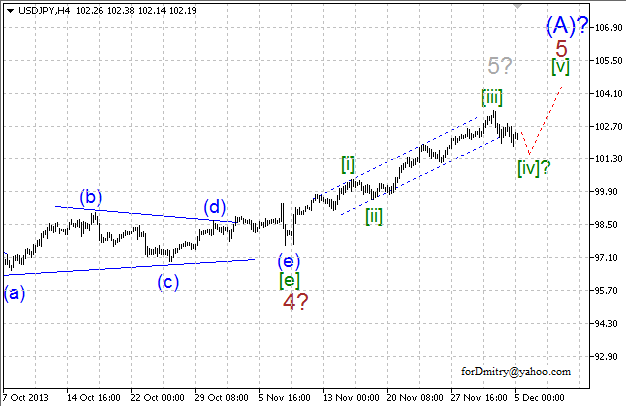

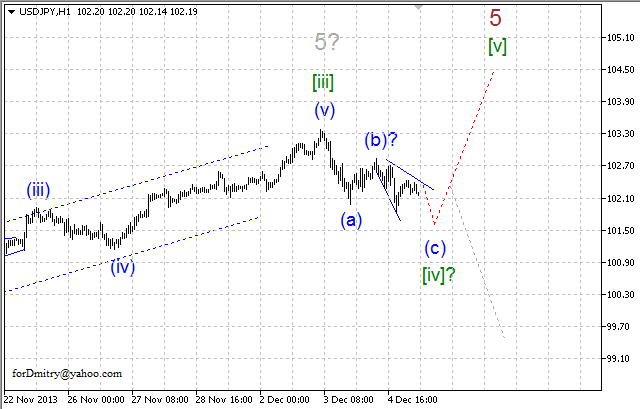

USD/JPY

Possibly, Yen is completing large ascending impulse (A). In this case, later pair is expected to start large descending correction (B).

Probably, pair is forming final ascending impulse 5 of (A). If it’s true, then right now price is forming descending correction [iv] of 5, after which ascending trend may continue.

Possibly, price is finishing local descending correction [iv] of 5 or its first part.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Keynote Speaker Series: Alexander Green Brings Back the American Dream

Our Publisher, Robert Williams, just sat down with The Oxford Club’s Investment Director, Alexander Green, to discuss his compelling new book.

Alex is one of the greatest minds in finance, as his track record proves.

The book, An Embarrassment of Riches, explores the tremendous advantages of living in our capitalistic society. And the timing couldn’t be better…

A recent poll suggests that 41% of people in the United States don’t believe in the American dream anymore.

With the strategies Alex lays out in this book, however, he’s bringing the dream back in a BIG way.

Indeed, as Alex says during the interview, the secrets revealed in the book can help anyone “achieve the financial independence that eludes so many people.”

We should certainly listen to what he has to say, too, since his portfolio’s performance is so impeccable.

In fact, the independent Hulbert Financial Digest has ranked Alex’s investment letter, The Oxford Communiqué, among the best-performing newsletters in the nation… For more than a decade!

Click on the image below to hear the interview in its entirety.

Ahead of the tape,

Louis Basenese

The post Keynote Speaker Series: Alexander Green Brings Back the American Dream appeared first on Wall Street Daily.

Article By WallStreetDaily.com

Original Article: Keynote Speaker Series: Alexander Green Brings Back the American Dream

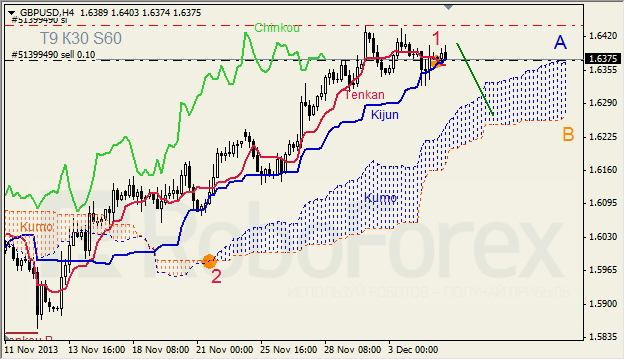

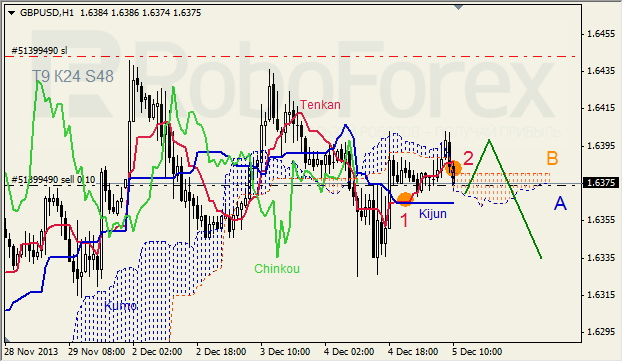

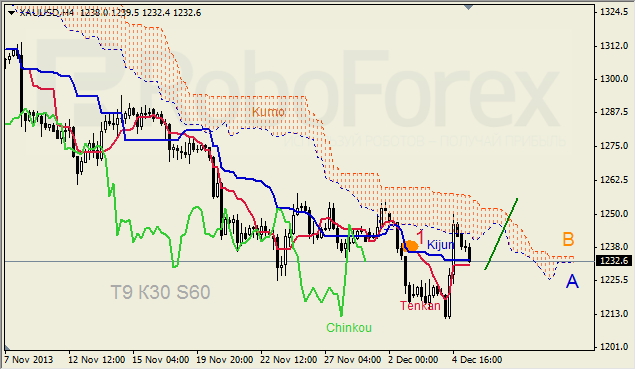

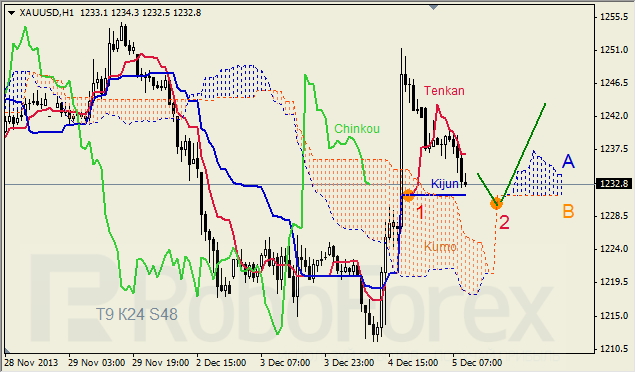

Ichimoku Cloud Analysis 05.12.2013 (GBP/USD, GOLD)

Article By RoboForex.com

Analysis for December 5th, 2013

GBP/USD

GBPUSD, Time Frame H4 – Indicator signals: Tenkan-Sen and Kijun-Sen intersected and formed “Dead Cross” (1); Senkou Span B is directed upwards, other lines are horizontal. Ichimoku Cloud is going up (2), Chinkou Lagging Span is close to the chart, and price is on Kijun-Sen. Short‑term forecast: we can expect attempts to stay inside Kumo.

GBPUSD, Time Frame H1 – Indicator signals: Tenkan-Sen and Kijun-Sen intersected below Kumo Cloud and formed “Golden Cross” (1); all lines are horizontal. Ichimoku Cloud is very narrow and continues going down (2); Chinkou Lagging Span is on the chart, and price is inside Tenkan-Sen – Kijun-Sen channel. Short‑term forecast: we can expect support from Senkou Span A – Kijun-Sen, and growth of the price.

GOLD

XAUUSD, Time Frame H4 – Indicator signals: Tenkan-Sen and Kijun-Sen intersected below Kumo Cloud and formed “Dead Cross” (1); all lines are horizontal. Ichimoku Cloud is very narrow and still going down, Chinkou Lagging Span is below the chart, and the price is on Kijun-Sen. Short‑term forecast: we can expect attempts to stay above Kumo.

XAUUSD, Time Frame H1 – Indicator signals: Tenkan-Sen and Kijun-Sen intersected below Kumo Cloud and formed “Golden Cross” (1); all lines are horizontal. Ichimoku Cloud is going up, Chinkou Lagging Span is above the chart, and price is inside Tenkan-Sen – Kijun-Sen channel. Short‑term forecast: we can expect support from Kijun-Sen – Senkou Spans A and B, and growth of the price.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

No ‘Too Big To Fail’ in Mining Sector Opens Opportunities for Value Investors: Mike Niehuser

Source: Special to The Gold Report (12/4/13)

Mining stocks may have moved from a bear market to a place where they are becoming contrarian plays, says Mike Niehuser, founder of Beacon Rock Research, opening opportunities for value investing. With the concept of “Too Big To Fail” unknown in the mining world, the field of companies is shrinking, making room for potential winners. In this interview with The Gold Report, Niehuser warns that companies need more than good projects and cash to outperform their peers and details a dozen miners that should be on the radar of investors.

The Gold Report: We are coming to the end of 2013, and you’ve been busy visiting projects and attending conferences. What are some themes you see in metals and resource stocks?

Mike Niehuser: It is clear that following the PDAC Convention last spring, conferences seem to be down in numbers of attendees and participating companies, probably a result of challenges raising money or running out of money. But it feels as if we have moved from a feeling of fear of what’s to come to an acceptance of how to move forward. What is interesting to me about the recent Metals & Minerals Investment Conference in San Francisco is that the commentators all seem to be reaching the same conclusion but with different words. It’s similar to several people witnessing a traffic accident; the result is plain to see, but the way it happened can be perceived quite differently.

TGR: Are you referring to mining stocks?

MN: There seems to be a definite consensus that we are at a bottom for mining stocks, but the question nobody dares to touch is how long it will last. Exeter Resource Corp. (XRC:TSX; XRA:NYSE.MKT; EXB:FSE) had a nice little chart in its corporate presentation going back to 1983 for small-cap mining stocks. It showed bottoms lasting a couple of years prior to 2000, with greater volatility, in 2008, for example. I’m thinking we may be in for a couple of years that could be positive. This would imply that we have moved from a bear market to the place where mining stocks are becoming contrarian plays. I suspect this is how we begin to move off the bottom. I don’t see an immediate massive sector rotation back into mining stocks, but this is fine for me because it favors company selection and value investing.

TGR: That seems optimistic. How do you know that?

MN: There are a few success stories out there that have appreciated. Companies still get rewarded for results, they just need to be material and faster than their cash burn rate. Also, appreciation generally follows companies with good capital structure and insider buying. All this is just basic value investing for those with the potential to deliver more than their peers. With a smaller field of companies, the market has already culled the herd, and 2014 could be a much better year. The sector and companies will be under pressure. This will provide further opportunities at year-end, especially with further declines in metal prices.

TGR: What do you see for metal prices?

MN: Certainly the Federal Reserve tapering, or reducing its bond buying, is getting all the attention, but I think this is misleading because the Fed is genetically predisposed to easy money in one form or another. I am shocked to see the velocity of money dropping like a rock. If you go to the Federal Reserve Bank of St. Louis’ website and look up the chart for the Velocity of M2 Money Stock, velocity is at the lowest level in more than 50 years. How we are not in a full blown depression can only be a result of ongoing bond purchases by the Federal Reserve, funding government largess.

Quantitative easing (QE) suppresses interest rates, which benefits those with access to capital markets like large corporations, and good luck to the rest of us. The drop in velocity is a rational response to the administration’s “fundamental transformation” that has increased uncertainty and led to holding higher cash balances. This causes deflation in the short run. When holders of cash are shaken seeing the value of their position eroded by QE, the horse will be out of the gate.

It is interesting that the leading economic indicators are positive, but this indicator is heavily weighted to low interest rates. So, in effect, the Federal Reserve is grading its own papers. With the appointment of the new Fed chair I don’t anticipate any changes in QE. If you pulled QE out in 2013, we probably would have negative growth over the last four quarters.

I don’t like QE because it is a Keynesian mechanism based on the premise that individuals are subject to animal spirits, or, in effect, are stupid. This is offensive to me. I would prefer what Friedman suggested for a passive monetary policy that didn’t try to trick consumers and investors, but trusted their individual judgment for consumption and investment.

QE is like meth—it makes you feel warm and pretty out on the street. It allows you to steal from others without concern. QE redistributes wealth. It is the drug that enslaves the user and robs seniors of their independence and from receiving a fair return on their savings. It promises the young an education at an inflated price, it places an extra burden on the productive and it destroys the middle class. If you want to see who is getting rich, go to Washington to see how the dealers are doing.

TGR: So should the Federal Reserve end QE right now?

MN: If the economy is as strong as the stock market is telling us, why not? The antidote for QE is reality, stable money. It doesn’t have to be a gold standard, but just some stability to stop manipulating the money supply. It’s become insider trading by the government. Look to the pilgrims, they lost everything and learned to adapt and they survived. So can we. Of course, I am an optimist.

TGR: So where do you see gold prices going in the near term?

MN: Who knows? We can expect gold to be lower in the near term. QE benefits Wall Street, big companies and government workers and beneficiaries. These consume rather than save. Velocity is dropping too fast for QE to keep gold prices up in the near term, especially with talk of tapering. It will be interesting to see who is buying this holiday season and how much, and what they have left at the end of the day. It will be interesting to watch consumer sentiment meet reality; it will be subtle.

TGR: What about investor sentiment for mining stocks?

MN: It appears that we are at a classic place where you know we are at the top when your barber is giving you hot stock tips, and we are near the bottom when they are plugging bitcoins over gold. Gold is real and has a history. What is important is that with year-end tax loss selling and with metal prices at or below advertised costs of production, there should be some real bargains. If we are near a bottom, this is when value investors become active, and this is the domain of the contrarian.

It is not enough to find companies with cash and good projects. You need a business that has a good aggressive management team working together with a realistic plan leading to success. This defines who survived the downturn and who will come out of it first. We have seen the losers, and now the winners are beginning to emerge. It will still take some time for them to get the recognition that they will need to earn. Good company selection is important to pick stocks with potential for appreciation, but a little sector rotation could make them look real smart. With an apparent reduction in active junior mining stocks, by definition, when sentiment reverses, it could be quite dramatic given a smaller roster of mining stocks.

TGR: With volatility in mining stocks don’t you feel investors hurt by the downturn will stay away?

MN: Investors may feel they have been lied to by companies and maybe a little bit by themselves. Rising prices never keep up with increasing expectations. The problem of course with mining is that miners seem to operate with costs of production up to the metal price. When expectations cool, metal prices stall and mines fail to meet earnings growth expectations, and investors look for someone to blame.

Nobody questions corporate decisions when stock prices increase, but they do question ethics when they decline. But this is why I love the mining sector: there is no Too Big To Fail here. If you don’t cut it, you fix it or you’re gone. There’s no subsidizing failure except by investors believing in good projects. This is why the sector could come roaring back. The only thing that can get in the way is government. This means the headwinds of higher taxes, regulatory corruption and career focused NGOs.

TGR: When do you think money might start moving back into the mining sector?

MN: It could start next spring, but I wouldn’t set my clock by it. At some point investors are going to see returns diminish in the broader market and will look for alternatives. They naturally will look for oversold areas for greater returns. This is optimistic. So my concern is that with QE we may see a shrinking class of contrarian retail investors that are the foot soldiers of a bull market. These investors have the greatest acuity for seeing value and have the greatest willingness to do their homework and to accept risk with a longer time horizon.

TGR: What have you seen and what do you like?

MN: For the most part sticking close to North America, to metals and jurisdictions I understand. I’m looking for companies with good prospects to positively surprise investors by improving production, reworking development plans or exploration potential, and special situations.

TGR: Let’s start with production.

MN: I recently visited the Grass Valley area of California and Virginia City, Nevada. Ever since I was a kid I loved Virginia City. I really like what Comstock Mining Inc. (LODE:NYSE.MKT) has done. The company has won over the community and local government, and brought the historic Comstock into production. Comstock should soon double the rate of production in 2014 to 40,000 ounces of gold annually, which should reduce the costs of production ahead of further declines in the price of gold. Should gold prices increase, the company should have cash for exploration. It appears to have a good geologic model with the potential to expand the resource. So there is both production and exploration upside.

I also visited North Bay Resources Inc.’s (NBRI:OTCBB) Ruby mine near Downieville, California. I saw the Ruby’s “globs” of gold when I was 15 years old looking through a National Geographic magazine. This is an interesting paleoplacer gold mine, which is now ready to commence production at a low cost. Both Comstock and North Bay’s mines are historic, which also interests me.

TGR: What about development-stage projects?

MN: Two big projects that I believe still have potential are in Alaska. Despite the Environmental Protection Agency’s handling of the Pebble project, Alaska is still viable. NOVAGOLD (NG:TSX; NG:NYSE.MKT) is divesting noncore assets and focusing on advancing Donlin Creek, arguably one of the world’s largest undeveloped gold deposits, which will benefit from an increase in gold prices.

Also, last July I visited International Tower Hill Mines Ltd.’s (ITH:TSX; THM:NYSE.MKT) Livengood project near Fairbanks. This project is now being optimized to work at lower prices and should benefit by an increase in gold prices. International Tower Hill Mines has an accomplished team that is local to the area or has a past history working at nearby Fort Knox. These projects are either on private land or designated for mining uses and are important to Alaska and the local communities they serve.

I also toured the Yukon in September. Alexco Resource Corp. (AXR:TSX; AXU:NYSE.MKT) in the Yukon recently suspended operations but is working to reopen as a considerably different project. The centrally located mill is expected to be fed by two additional large or high-grade silver mines, which should bring the mill to capacity. With increasing silver prices alongside gold, this will be a remarkably different mine. Alexco also has a unique environmental business, which will cover a lot of overhead until the mine reopens.

TGR: What exploration projects do you think deserve a look?

MN: Nevada is a good place to start. At the Metals & Minerals Conference I sat down with Premier Gold Mines Ltd. (PG:TSX). I have not visited its projects, but the company is known for work done in Ontario and is expecting results on its project in Red Lake. Investors should keep an eye on its Cove project in Nevada. It is brownfields exploration but Premier is looking at it in a whole new way. If the company is right, it could be one of the biggest discoveries in Nevada in some time. Premier also has about $80 million ($80M) in cash, which is very interesting.

There are a number of interesting projects in the Cortez Trend in Nevada. NuLegacy Gold Corporation (NUG:TSX.V; NULGF:OTCPK) has a highly prospective Iceberg oxidized gold project near Barrick Gold Corp.’s (ABX:NYSE) Cortez Hills mine, and even closer to Barrick’s 14 million ounce (14 Moz) 4+ gram/ton gold discovery. NuLegacy recently amped up its exploration team and raised enough cash to complete a 70% earn-in on the Iceberg gold project by December 2015.

Rye Patch Gold Corp. (RPM:TSX.V; RPMGF:OTCQX) also has targets in the area. Rye Patch recently settled with Coeur Mining Inc. (CDM:TSX; CDE:NYSE) on its claims on its Rochester project. Rye Patch has about $9M in the bank, and the royalty settlement is estimated at about $32M in total. Rye Patch should start receiving payments next April. The company has a 2–3 Moz gold deposit near Rochester and has picked up additional prospective land. Shares of Rye Patch are cheap.

TGR: Is Rye Patch one of your special situations?

MN: It was, but the settlement is in the past. It now has a resource, exploration upside and cash.

An interesting special situation is the acquisition of High Desert Gold Corp. (HDG:TSX.V) by South American Silver Corp. (SAC:TSX; SOHAF:OTCBB). High Desert shareholders get 0.275 share of South American. The new company will have $13M in cash, High Desert’s Gold Springs project on the Nevada-Utah border and South American Silver’s giant Escalones copper project in Chile. The company will probably joint venture Escalones and focus exploration at Gold Springs, which is a district-size property with exploration upside on both sides of the Nevada-Utah border. South American will also split out its litigation with Bolivia over the nationalization of Malku Khota. These shares will also trade, and it appears that it has a good chance to collect.

TGR: Mexico has made changes to its taxation policies. Is that a concern?

MN: This is unfortunate because of a global theme of political risk concerning investors and the surprise on what had been a premier jurisdiction for mining. The net result is that it puts Mexico on par now with its neighbors, which is not necessarily something to brag about. One company that I mentioned in an earlierinterview, that I met with at the Denver Gold Forum, was Excellon Resources Inc. (EXN:TSX; EXLLF:OTCPK). I had visited the company’s mill under other ownership.

Excellon has a very high-grade silver deposit, not unlike a Mexican Alexco. Excellon recently successfully resolved issues and has rapidly increased cash flow, which is building its balance sheet, and several years of net operating losses to defer taxes. Depending on the rate of production, Excellon has 7 to 15 years of production and what appears to be an excellent exploration profile.

TGR: Anything interesting outside North America?

MN: Last September I visited Namibia with students from Oregon State. I love Namibia. We visited uranium, gold and fluorite mines and Namibia Rare Earths Inc.’s (NRE:TSX, NMREF:OTCQX) Lofdal heavy rare earth project. This project has not gotten the visibility it deserves because the company has not yet produced a preliminary economic assessment. Namibia Rare Earths has, along with Northern Minerals Ltd. (NTU:ASX), a heavy rare earth resource in xenotime, which is the only mineral in hard rock that has commercially recovered rare earths. Consequently, Namibia Rare Earths, being primarily heavies, has the highest basket price for contained minerals, contained within a well-defined resource with excellent expansion opportunity.

Namibia Rare Earths recently reported steady progress on its metallurgical test work, which appears to build upon its credibility in locating a qualified joint venture partner. Metallurgical work is less expensive than exploration, and with about $10M in the bank, the company is well positioned.

TGR: Are rare earths on their back right now?

MN: While rare earth prices and company stocks are down, I believe this is a stage where, when enthusiasm wanes, heavy rare earth projects will be distinguished from the lights, and a few winners among the 300+ rare earth projects will emerge.

I also spoke to Tasman Metals Ltd. (TSM:TSX.V; TAS:NYSE.MKT; TASXF:OTCPK; T61:FSE) at the Metals & Minerals show. Tasman has one of the largest rare earth projects. It has low political risk, being located in Sweden, and close to end users. I have not visited the project but it is clearly located in an area with a long mining history, and with excellent infrastructure it presents the option for a low capital-cost project, which is appealing to investors. Tasman, like other developing rare earth projects, is focused on metallurgy, and investors should watch for progress in 2014.

TGR: Thank you for taking the time to join us.

Mike Niehuser is the founder of Beacon Rock Research, LLC, which produces research for an institutional audience and focuses in part on precious, base and industrial metals, oil and gas and alternative energy. Previously a vice president and senior equity analyst with the Robins Group, he also worked as an equity analyst with The RedChip Review. He holds a bachelor’s degree in finance from the University of Oregon.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) The following companies mentioned in the interview are sponsors of The Gold Report: Comstock Mining Inc., NOVAGOLD, International Tower Hill Mines Ltd., Premier Gold Mines Ltd., NuLegacy Gold Corporation, Rye Patch Gold Corp., Excellon Resources Inc., Namibia Rare Earths Inc. and Tasman Metals Ltd. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

2) Mike Niehuser: I or my family own shares of the following companies mentioned in this interview: Comstock Mining Inc., Alexco Resource Corp., High Desert Gold Corp., South American Silver Corp. and Namibia Rare Earths Inc. I personally am or my family is paid by the following companies mentioned in this interview: Alexco Resource Corp., North Bay Resources Inc. and Namibia Rare Earths Inc. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

3) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2013 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8999

Fax: (707) 981-8998

Email: [email protected]

Analysts Reduce their Forecasts for Gold

Several analysts have recently cut their predictions for gold, providing dire forecasts for the future of the precious metal.

Individuals who want to make money by trading the commodity might benefit from being aware of this information. These market experts have lowered their predictions for gold at a time when the commodity has been having a rough 2013. The metal has suffered a precipitous slide that began earlier this year, and resulted in the precious metal falling into a bear market in April, after it plunged more than 20 percent from the all-time high that it rose to in 2011 amid significant economic turmoil.

In the following months, gold continued to trend lower. In June, it dropped below $1,200 per ounce, which represented its lowest price in almost three years. While the metal than managed to enjoy some appreciation and erase some of the losses it incurred, gold is still down sharply in 2013.

Markets predict further declines for gold

After the rough time that the commodity has had this year, several analysts have predicted that gold will continue to experience declines moving forward. Precious-metals strategists at UBS recently forecast that in 2014, the asset will have an average value of $1,200 an ounce, according to Barron’s. This amount compares to the prior forecast of $1,325 per ounce. In a report, two key market experts explained the various factors that will serve to push the precious metal lower next year.

Brian MacArthur and Joshua Wardell of the major financial services firm have asserted that the low risk aversion of global investors, “the reduction of tail risks” and a strong economy will all create a situation whereby “safe havens like gold will become even more unfashionable up ahead.”

Various factors could push metal lower

“With the market now increasingly refocusing on QE-tapering, gold has resumed its downward trend,” they wrote. “Together with weak underlying sentiment, as evidenced by the disappointing price performance even in the face of bad news such as tensions in Syria and the US government shutdown and given constrained Indian demand under the current regulatory framework, UBS believes the recent downward pressure will continue and sees a lack of supporting catalysts.”

UBS was not alone in making bearish predictions for the precious metal, as Societe Generale analysts recently recommended that global market participants “go short” on the commodity since they predict that there will be “more pain for gold, with prices seen at $1,050 an ounce by the end of 2014,” according to MarketWatch.

The post Analysts Reduce their Forecasts for Gold appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

USDJPY pulls back from 103.37

Being contained by the resistance of 103.73 (May 22 high), USDJPY pulls back from 103.37 and breaks below the lower line of the price channel on 4-hour chart, suggesting that consolidation of the uptrend from 96.94 is underway. Sideways movement in a range between 101.50 and 103.37 would likely be seen over the next several days. Key support is at 101.00, as long as this level holds, the uptrend from 96.94 could be expected to resume, and one more rise towards 105.00 is still possible. On the downside, a breakdown below 101.00 will indicate that the upward movement from 96.94 had completed at 103.37 already, then the following downward movement could bring price back to 95.00 zone.

Provided by ForexCycle.com

Forget Bitcoin, This is the Real Future of Digtial Money…

We first mentioned Bitcoin in Money Morning about six months ago.

That was when technology analyst Sam Volkering joined the team.

Back then the price of a Bitcoin was around US$140 or something.

Today it’s US$1,200. It was even higher last week.

Is this the future of money? Not if you ask Sam. He thinks any business that accepts Bitcoin today would be mad. We’ll explain why below…

Yesterday afternoon we tuned in to watch a pre-release version of a Skype video call between Sam and our old pal Dan Denning.

The discussion was about Bitcoin, mainly what it is and how it works.

This is a key topic around our Albert Park office. The future of money is the subject of next year’s Port Phillip Publishing investment conference. We’ve titled the event World War D in honour of the seemingly unstoppable trend towards digital money.

Tap, Pay, Go – Easy

Your editor is entirely convinced that paper or plastic bank notes and metal coins will cease to exist within the next 10 years.

If you want to pay for something you’ll pay for it electronically. And that will mean for any and every transaction regardless of the amount.

Stop and think about it. If you’re like us you probably already pay for most things electronically. You’ve probably got an EFTPOS card or VISA or MasterCard debit card. And you’ve probably got a credit or charge card too.

When was the last time you used cash? And when you did we bet it wasn’t out of choice. We bet it was a small cash purchase. There’s even a chance you had to go out of your way to find an ATM in order to get the cash so you could pay for whatever you wanted.

What a waste of time.

We’ll admit something though. As much as we’re in favour of an all-electronic money system, we’ve been slow on the take-up in some respects. We’ve always signed for things when we’ve used a credit card.

How old fashioned.

We didn’t like the idea of using a PIN. Maybe it’s because we couldn’t bear the thought of needing to remember another darn number.

But of course, thanks to chip technology you don’t need to sign…and you don’t need a PIN. You just tap your card on the console and bingo, you’re done. We’ll admit something else – we love ‘tap and go’ transactions.

We can’t imagine why anyone would think that’s an innovation not worth having.

But that’s just the beginning of the shift to all-electronic money. We’ll explain the next stage shortly. First, let’s get back to Bitcoin and explain why Sam thinks any business would be nuts to accept it as a payment right now…

Too Volatile to Transact?

Australian businesses accept Australian dollars for good reason. They have a high degree of certainty that the dollars they accept today will be worth the same tomorrow or the next day when it comes to buying something (such as supplies) with those dollars.

That isn’t something you can necessarily say about Bitcoin. As Sam pointed out in his Skype call from London, Bitcoin is currently far too volatile for any business to accept as a method of payment.

The Bitcoin price has surged since the start of November from US$228 to today’s price of US$1,200. Now, if a business had accepted a Bitcoin in return for selling some goods a month ago that business owner would be pretty happy. He or she would have made five-times their money just on the appreciation of Bitcoin.

But as any financial advisor will tell you, prices can go down as well as up. So imagine if a business accepts a Bitcoin today as payment. What guarantee does the business owner have that the price will be the same tomorrow?

There is no guarantee. If the price collapsed tomorrow (say, back to US$228) before the business owner could cash in the Bitcoin for Australian dollars, the business owner would make a huge loss on the transaction.

As Sam points out in the Skype call, that kind of volatility would make it hard for any business owner to plan for the future if they didn’t have some idea about the future price of Bitcoins.

The Currency Wars End Game

Admittedly, you could say the same about any exchange rate. The Australian dollar has fallen over 10% over the past six months. That kind of price move makes it hard for Aussie businesses to plan for the future too.

The major difference is that at least the business owner knows the Australian dollar will be widely accepted today, tomorrow and most likely a year from now. Can anyone say with 100% conviction that the same is true for Bitcoin? No.

But that doesn’t mean we’re down on all digital currencies (to be honest, we’re not really down on Bitcoin either; we just don’t see it becoming a widely transacted digital currency).

Instead, we see a future where digital currencies are much more user friendly. We see a competitive market of free market currencies where you make transactions as easily – if not more easily – than you do today.

We see biometric technologies such as thumb scanning and iris recognition becoming the method of payment rather than a credit or debit card.

This isn’t something that will happen tomorrow, but it will happen. Digital money and ‘digital wallets’ are gaining acceptance among consumers. It’s only a matter of time before the State’s monopoly on money ends and a new era of private digital money begins.

Our guess is it will be a relatively peaceful transition. But we can’t guarantee that. That’s why our conference theme is World War D. The global currency wars are about to go to a whole new level.

Cheers,

Kris+

PS: The Early Bird discount for the World War D conference ends this Friday. To make sure you don’t miss out on the line-up of star speakers, including Dr Marc Faber and Jim Rickards, sign up here. Seating is limited and is sure to sell out soon.

From the Port Phillip Publishing Library

Special Report: The ‘Wonder Weld’ That Could Triple Your Money

The Coming Leap in Mass Transit

Have you ever had a humbling ‘foot in the mouth’ moment?

I sure have. It happened a couple of years ago when I first heard about a service, a smartphone app, aiming to fundamentally alter the taxi industry.

I was at a monthly dinner with a dozen venture capitalists and angel investors. After a few glasses of cabernet, when we were going around the table to talk about exciting or harebrained ideas we’d recently come across, I stood up to blast holes through this new taxi idea.

I ranted to my colleagues that the idea was impossible to execute and bound to fail. Trying to break into regulated markets like transportation, I said, is like sticking needles in your eye. And beyond that, in my mind, nobody would ever use or pay extra for a service like this – especially in places like New York City, where yellow taxis dot the road at all hours.

Fast-forward a few months to a bitterly cold and rainy night. I’d just ducked out of a steakhouse and was standing on the corner of 49th and Lexington Avenue, drenched, trying to hail a cab. The wind was howling, my loafers were soaked and there wasn’t an empty yellow cab in sight. Desperate, I pulled out my iPhone and clicked on the very same taxi app I’d verbally torn apart only a few months prior.

And what do you know: Within four minutes, my opinion of the product and the company changed.

Because within four minutes I was sitting in the back seat of a Lincoln Navigator, hot air blowing at me from my personally controlled vents. I’d been able to track the position of the car on my phone while I waited inside the warm, dry steakhouse, so I knew exactly when it would be at the curb. Sure, it cost a few dollars more than a yellow cab, but the overall experience was fantastic. Now I use the service constantly.

The service is Uber. And since the night of my foot-in-the-mouth remarks, the company has grown like a weed, making a huge dent in the taxi industry. In fact, the company recently raised over $250 million from Google at an eye-popping $3.5 billion valuation.

Given this company’s humble beginnings – and my initial scepticism – I’ve become open to the idea of small, private companies ‘disrupting’ (that’s geek-speak for fundamentally changing) regulated and public-sector industries.

In fact, there’s a company raising money on AngelList right now that’s looking to disrupt mass transit. In fact, it could become the ‘Uber of mass transit’…

From an Investor’s Perspective, the Opportunity is Huge

The top 20 US markets for mass transit cater to 2.2 billion riders per year. Even at a few dollars in revenue per ride, whoever succeeds in capturing this market could become a billion-dollar company.

The company I’m referring to on AngelList is called Leap Transit.

They launched a trial in San Francisco. Within four months, they registered over 4,000 members, provided rides to over 2,300 people, and are already generating revenue.

Based on the size of the market opportunity and the results of the test, the company attracted the attention of famed venture capital firm Andreessen Horowitz (early backers of Facebook and Twitter) as well as Ron Conway’s SV Angel fund (early investors in Google). They’re both investing in this round of financing.

Leap essentially operates its own fleet of buses, much like Uber operates a fleet of cabs. That might sound dull at first blush, but the way Leap leverages technology is downright innovative and exciting.

For one thing, there won’t be any standardised routes or schedules. The bus routes will be crowdsourced – meaning, the service will intelligently generate new routes based on riders’ pickup locations and destinations. So if you and dozens of other people live in the same area and are all headed downtown, the bus will automatically generate the most optimal route and pickup schedule.

And like Uber, Leap will allow you to check arrival times and track the current location of the bus right from your mobile phone. So no more wondering when your bus will arrive, wondering where it is or running to the stop in a panic.

On top of that, the buses have comfortable seating, air conditioning and free Wi-Fi, so you can work or relax while in transit. We believe Leap Transit has the makings of a successful company…and a successful investment.

The company is currently raising $2 million on AngelList and, as mentioned, already has some high-profile investors involved.

The valuation is $4 million. Given the opportunity size, the company’s progress so far and the skills of their management team, we believe that’s an attractive figure.

Wayne Mulligan,

Contributing Writer, Money Morning

Ed Note: The Coming Leap in Mass Transit originally appeared in The Daily Reckoning USA

Poland still sees steady rates at least until end-H1 2014

By CentralBankNews.info

Poland’s central bank, which earlier today maintained its reference rate at 2.50 percent, repeated that “interest rates should be kept unchanged at least until the end of the first half of 2014.”

The National Bank of Poland (NBP), which has cut rates by 175 basis points this year, also said Poland’s gradual economic recovery was likely to continue in coming quarters while inflationary pressures will remain subdued.

Last month the NBP pushed back any rate rise until at least until the end of the first half of next year from September’s statement that it would maintain rates at least until the end of this year. In July the central bank said its cycle of easing had ended after cutting rates by 225 points since November 2012.

Poland’s Gross Domestic Product expanded by a stronger-than-expected 1.9 percent annual rate in the third quarter, up from 0.8 percent in the second, as domestic demand rose, driven by rising consumption and a slight increase in investment while net exports had a lower positive contribution and inventories had a negative impact on GDP, the bank said.

Last month the Organization for Economic co-Operation and Development (OECD) raised its forecast for Polish growth this year to 1.4 percent from a previous 0.9 percent and its 2014 forecast to 2.7 percent from 2.2 percent. In 2012 Poland’s GDP grew by 1.9 percent.

In October there was a minor slowdown in the annual growth of industrial output and retail sales while construction and assembly continued to fall, albeit at a slower pace. Business climate indicators suggest a gradual recovery in coming quarters.

“The gradual improvement in economic conditions is accompanied by fading negative trends in the labour market,” the NBP said.

While Poland’s unemployment rate was steady at 13 percent in October from September and August, the number of employed people rose to 8.496 million in the third quarter, up from 8.490 in the second quarter.

“Demand and cost pressures in the economy remain low,” the central bank said, as headline inflation fell to 0.8 percent in October from 1.0 percent in September, well below the bank’s 2.5 percent target.

www.CentralBankNews.info