By www.CentralBankNews.info Romania’s central bank cut its policy rate by 50 basis point to 4.50 percent, the second cut in a row, saying its latest inflation report shows faster “disinflation in the period ahead, along with a pick-up in economic growth.” The rate cut was expected.

The new inflation report, which was approved by the bank’s board, will first be released on Aug. 7.

The National Bank of Romania (NBR) has now cut its rate by 75 basis points this year, the same as in 2012, said the latest data show that inflation is in line with the central bank’s previous forecasts and should fall within the bank’s target range once the effects of last summer’s supply-side effects fade.

Romania’s headline inflation rate was largely steady at 5.37 percent in June from 5.32 percent in May, above the bank’s target of 2.5 percent, plus/minus 1.0 percentage point. The NBR has forecast that inflation will fall to 3.2 percent by the end of the year.

Based on the EU’s HICP measure, inflation rose slightly to 4.5 percent in June from 4.38 percent in May.

Romania’s economy improved in the first quarter due to exports while consumption stalled and the dynamics of loans to the private sector remained in negative territory and the pass-through of the policy rate to interest rates on new corporate and household loans remains slow, the bank said.

Romania’s Gross Domestic Product expanded by 0.6 percent in the first quarter from the previous quarter for annual growth of 2.2 percent, up from 1.2 percent in the fourth quarter.

The NBR noted that volatility in investors’ risk appetite and persistent uncertainty surrounding economic activity in Europe and elsewhere “temporarily entailed wider fluctuations in the leu exchange rate,” largely repeating last month’s statement.

But a new precautionary agreement with international financial institutions and structural reforms should strengthen the economy’s resilience to external shocks, the NBR added.

Last week the International Monetary Fund and the European Union reached a 4 billion euro standby loan agreement with Romania that should help protect it from financial turmoil.

The Romania leu weakened in May but has been steady on the year, quoted at 4.42 leu to the euro today compared with 4.44 on Jan. 1, 2013.

Uganda holds rate, core inflation seen close to target

By www.CentralBankNews.info Uganda’s central bank held its central bank rate (CBR) steady at 11.0 percent, saying it was maintaining a neutral policy stance as core inflation over the next 12 months is forecast to remain very close to the bank’s 5.0 percent target.

The Bank of Uganda (BOU), which cut its rate by 100 basis points in June, said the the risks to inflation remain on the upside, as last month, with pressures from the domestic supply side, along with the prospect of higher oil prices due to geopolitical factors in the Middle East and North Africa.

“Demand pressures remain moderate and still do not pose a risk to the inflation outlook,” the bank said.

Headline and core inflation are likely to rise slightly in the next three to six months due to the impact of drought on food prices, but this is expected to be temporary and prices should then ease and stabilise around 5.0 percent.

Headline inflation rose to 5.1 percent in July from 3.6 percent and core inflation to 6.4 percent from 5.8 percent due to higher food prices, particularly prices of processed food, which is likely transitory.

Uganda’s economy is forecast to expand by 6 percent in the 2013/14 financial year, which began July 1, but downside risks to growth remain, the bank said.

A decline in private sector imports in the first six months of this year and a subdued pace of credit extension “suggests a softening of aggregate demand,” but a decline in lending interest rates to 22.6 percent in June from 27 percent last year should contribute to a rise in private sector investment and stronger growth in the later part of 2013/14.

Uganda’s Gross Domestic Product shrank by a quarterly 0.1 percent in the first quarter of 2013, but on an annual basis, GDP rose by 7.2 percent, down from 10.4 percent in the fourth quarter.

Climate Change Will Exacerbate Violence Around The World, Research Finds

Climate Change Will Exacerbate Violence Around The World, Research Finds (via Clean Technica)

Climate Change Will Exacerbate Violence Around The World, Research Finds (via Clean Technica)Climate change will exacerbate violence around the world, increasing levels of both personal violence and social upheaval, according to new research from Princeton University and the University of California–Berkeley. Throughout history, even slight…

Euro climbs on German PMI services data

The 17-nation currency euro made a slight rise against the US dollar on Monday, as the German PMI reports showed that the PMI in services from the country grew lesser than forecasted in July. While the currency is pushed by the disappointing US jobs data released on Friday.

Euro rose 0.08% to $1.3292 against the greenback as of 8:01am GMT, while it declined 0.46% to ¥130.74 against the yen at the same time. The German final services Purchasing Managers’ Index (PMI) remained at 51.3 in the month of July. The German’s PMI was expected to advance to 52.5.

The final services PMI for Spain made a slight rise from previous record of 47.8 in June to 48.5 in July. While the Italian services PMI advanced to 48.7 in July, from previous record of 45.8 in June, according to reports from the Markit Economics.

In France, the services Purchasing Managers’ Index (PMI) edged up to 48.6 in July from previous record of 47.2 in June. The service sector activity advanced to the highest in 11 months in the month of July.

The below-forecasted US jobs data showed that it’s most likely that the Federal Reserve’s won’t begin to taper its quantitative easing program anytime soon.

The unemployment rate fell by 0.2% to 7.4%, slightly below the estimated record of 7.5%.

On Wednesday, the US central bank concluded after the two-day policy meeting that the key rate would remain the same at 0.25% and would continue its $85 billion monthly asset purchases.

The post Euro climbs on German PMI services data appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Asian stock market decline;China services data climbs

The Asian stock market started the first day of the trading week in red, first time in three days as the Japanese shares led the decline on a stronger yen after the U.S. jobs data showed below-forecast data on Friday. The Chinese shares and European index futures advanced, while in Australia and Japan, bonds rallied with gold.

The disappointing figures from the below-forecast workforce data showed that the US economy is still at a slow recovery growth, which is not strong enough for the Federal Reserve to start scaling back on the monetary stimulus programme.

The Japanese benchmark Nikkei 225 declined 1.44% to 14,258.04, while the Topix index dropped 0.89% to 1,185.53. Hong Kong’s Hang Seng slightly advanced 0.20% to 22,234.98, while the Chinese mainland Shanghai Composite rose 0.80% to 2,045.71.

The South Korean Kospi index fell 0.37% to 1,916.22, while the Australian S&P/ASX 200 decreased by 0.15% to 5,109.30.

The US released the disappointing non-farm payrolls data on Friday, as the figures were below expectations and indicated the US economy added around 162,000 jobs in the month of July, below the forecasted 185,000.

The report showed that the unemployment rate fell by 0.2% to 7.4%.

The figures from the report failed to push the Asian stocks, while the US stocks, such as the Dow and S&P 500 were at a high record, while bonds rallied and the US dollar declined.

The stock market in China opened in green on Monday, as the Chinese service sector was seen in the expansion territory in the month of July. Reports from HSBC Holdings Plc and Markit Economics measured business activities in services resulted to 51.3 in July.

The Chinese government survey showed accelerated expansion from 53.0 from June to 54.1.

The post Asian stock market decline;China services data climbs appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Central Bank News Link List – Aug 5, 2013: China central bank move indicates tightening bias

By www.CentralBankNews.info Here’s today’s Central Bank News’ link list, click through if you missed the previous link list. The list comprises news about central banks that is not covered by Central Bank News. The list is updated during the day with the latest developments so readers don’t miss any important news.

- China central bank move indicates tightening bias (WSJ)

- Romania seen lowering rates for second month in new easing cycle (Bloomberg)

- Bank of Israel ‘functioning normally,’ policy maker Gronau says (Bloomberg)

- Mark Carney to unveil ‘pre-commitment’ on interest rates (The Telegraph)

- BOK to freeze rate again in August: analysts (Yonhap)

- Israel’s Netanyahu lampooned for failing to fill top central bank job (Reuters)

- SBP may push up interest rates in the monetary policy (Pakistan Observer)

- Egypt’s interest rate cut a welcome first step: analysts (Ahramonline)

- www.CentralBankNews.info

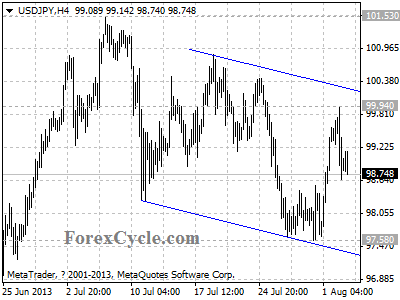

USDJPY is now in uptrend from 97.58

USDJPY is now in uptrend from 97.58, the fall from 99.94 is likely correction of the uptrend. Another rise to test 101.53 key resistance is possible after correction, a break above this level will indicate that the long term uptrend from 75.57 (Oct 31, 2011 low) has resumed, then the following upward movement could bring price to 110.00 zone. Initial resistance is at the upper line of the price channel on 4-hour chart, fail to break above the channel resistance will suggest that the pair remains in downtrend from 101.53, one more fall to 96.00 to complete the downward movement is possible.

Provided by ForexCycle.com

When Should You Sell Your ‘Loser’ Stocks?

Take $1.1 billion, invest it in a business, and then wait 20 years.

Now, take that same business and sell it for…just $70 million.

That’s a loss of 93.6%.

But this is more than just a big financial loss.

It’s also a terrific example of how a healthy, thriving and growing business can quickly become almost completely obsolete…

The transaction we mentioned above was the New York Times Company’s [NYSE: NYT] purchase of the Boston Globe newspaper in 1993 and the subsequent sale last week.

We’re sure that 1993 must have seemed like a pretty good time to buy a newspaper business.

OK, so circulation numbers for all newspapers in the US had fallen to 59.8 million in 1993 from 62.8 million in 1985. But the US had only just come out of a recession. Circulation numbers were bound to climb as the economy recovered.

And anyway, it was 1993; what was the alternative to newspapers? Surely not that new-fangled ‘internet thing’.

Newspapers Hit the Tipping Point

As it turns out, things would never get better for the newspaper business. Not only were newspapers losing readership to online news sources, but they were losing their major source of revenue – advertising.

After circulation declined steadily through the 1990s and into the 2000s, they finally began to fall of a cliff in 2004:

Source: Statista.com

For most of those 10 years we dare say the New York Times Company thought things would turn around. Just one small business initiative would stop the decline.

That didn’t happen. And to tell the truth it was never going to happen. Since 2003, circulation of the Boston Globe has declined by 38%. That’s roughly in line with the broader print industry.

In the 2000s the information revolution hit the tipping point. For the newspaper industry it was in 2003. After the boom and bust of the dotcom era, firms that used the internet could finally show they had a real business model.

It also happens that 2003 was when talk began about a stock market listing for the brash new internet search company, Google [NASDAQ: GOOG].

It finally listed in 2004 at USD$85 per share. It has barely looked back since. Today it trades for USD$906. That’s a 966% gain. In contrast, the New York Times Company traded for USD$41 in 2004. Today it trades for USD$11.93.

That’s a 71% drop.

Blindsided by the Internet

Where are we going with this?

Well, you can draw a few key lessons from the New York Times Company’s Boston Globe purchase – all of them relate to investing.

The biggest takeaway is that once a truly game-changing and revolutionary trend starts, it’s darn hard to stop it. Australian newspapers have fared just as poorly as US newspapers.

The situation is so bad they try to hide the declining print numbers by quoting combined print and digital numbers. But it’s not hard to do the math. The Sydney Morning Herald had a print circulation of 214,000 in 2004. Today it’s around 131,000.

Another key point is the damage to a dying business doesn’t always come from where you expect. Arguably it wasn’t just the declining readership that killed the newspaper business, but the falling ad revenue.

Think about it. Until the early 2000s, three main areas controlled the ad industry: TV, radio and print. They had an almost captive consumer.

But as consumers went online, the old media lost the captive consumer. Now, consumers may only spend several minutes a day (if that long) reading the Fairfax and News Ltd websites. The rest of the time consumers look at alternative news websites, blogs, social media websites, and others.

And because fewer people buy newspapers, advertisers have taken their business elsewhere. Newspapers have lost out to the likes of Google, Facebook [NASDAQ: FB] and eBay [NASDAQ: EBAY].

But there’s a more direct lesson for investors in the New York Times Company’s experience. And that’s one simple fact: if a bad business is a bad business then it’s usually better to get rid of it sooner rather than later.

Can Your Stock Recover, or is It a Loser?

It’s important to remember that, especially with stocks in your main blue-chip portfolio. Ask why you bought a stock. Most likely if it’s a blue-chip stock you bought it because you believed it could keep growing its business and perhaps keep growing its dividend.

If the company stops doing one or both of those things, then maybe it’s time to give up on it and look elsewhere. Of course, some companies can go through a rough patch or suffer lower sales and profits due to an economic recession.

If you think the downturn could be short term, then it may pay to hang on…or even buy more of the stock. But you should still review your analysis. There’s a chance the company’s industry is going through a seismic shift that will change its business for all time.

As we say, when the New York Times Company bought the Boston Globe in 1993, they must have thought they were smart for buying an established business with a loyal readership during a short term downturn.

That downturn turned out to be anything but short term, and 20 years later they’re selling out for a huge loss. It can be hard to admit you’re wrong with an investment. But when you’re saving for retirement you just can’t afford to follow that example by holding on to ‘loser’ stocks forever.

Cheers,

Kris+

From the Port Phillip Publishing Library

Special Report: The Sixth Revolution

Daily Reckoning: The Global Trend Towards Wealth Protection

Money Morning: Two Approaches to Investing…

Pursuit of Happiness: Learning to Avoid the Governments ‘Noble Wealth Trap’

Australian Small-Cap Investigator:

How to Make Big Money from Small-Cap Stocks

How to Get the Government to Pay for Your Retirement

The terms ‘cut the grass’ and ‘mow the lawn’ are different ways of saying the same thing.

So it is with ‘franking credit’ and ‘dividend imputation’. Both describe the tax treatment applied to company dividends paid to shareholders.

Prior to 1987, company dividends were subject to double taxation e.g. Company made a profit of $1,000 and paid 30% company tax ($300). The shareholder received the dividend (after tax profit) of $700.

But then the $700 was subject to the shareholder’s personal income tax rate. Let’s assume their personal tax rate was 40% ($280 tax). Of the initial $1,000 profit, the government received taxes totaling $580 and the shareholder $420.

The introduction of the imputation system (franking credit) lowered the shareholder’s tax burden. In effect shareholders receive a tax credit for the company tax paid on the dividend. Franking credits represent the tax the company has already paid on the earnings it has paid as dividends.

Using the same numbers in the above example, the tax treatment of a fully franked dividend is…

Company profit of $1,000 taxed at 30% company tax rate ($300).

The shareholder receives the after tax profit of $700. For tax purposes, the shareholder declares a grossed up (actual dividend plus company tax paid) dividend of $1,000.

Based on the shareholder’s personal tax rate of 40%, the tax payable is $400 minus the $300 company tax already paid. The shareholder’s net tax liability is $100. Under the imputation system, the $1,000 profit is split $400 to the government and $600 to the shareholder.

The above example is of a fully franked dividend – a profit taxed at 30% company tax rate.

An unfranked dividend is where company tax hasn’t been paid (due to losses, writedowns etc.). In this case the unfranked dividend is fully taxable in the hands of the shareholder.

The reason fully franked dividends are popular with self managed superannuation funds (SMSF’s) is the difference between the company tax rate and the tax rate paid by SMSF’s.

A super fund in the accumulation phase pays 15% tax on earnings and zero tax on earnings in pension phase.

The $1,000 grossed up dividend paid to a SMSF in accumulation phase would be taxed at 15% ($150). The SMSF gets to deduct the company tax credit ($300) and therefore get a refund of $150.

The SMSF in pension phase has a zero tax liability on the $1,000 grossed up dividend and would receive a full refund of the $300 company tax credit.

For example in the past 12 months Commonwealth Bank of Australia [ASX: CBA] has paid out a fully franked dividend of $3.61 per share. On the current share price of $73.80 this equates to a yield of 4.9%. When you add back the franking credit, the GROSSED up dividend is 7%.

That’s very attractive compared to most savings accounts.

In an environment of falling interest rates it’s easy to see why SMSF investors have eagerly chased companies paying fully franked dividends. However, chasing yield can be dangerous – especially if shares are at a premium. That extra few percent in income could come with a hefty capital cost if the market falls.

Prudent, value orientated investors know a tax effective income isn’t the basis for investing. The investment must firstly represent sound (and preferably, discounted) value. If the income stream has a ‘tax sweetener’ that’s a bonus.

The ability to access quality direct shares of your choosing is one of the main attractions for investors establishing an SMSF. A 7% income stream with minimum middleman costs (except for accounting and audit fees) lets investors keep the lion’s share of the income to fund their retirement goals.

With lower rates of return on capital, it’s not hard to see why the SMSF sector is one of the fastest growing in the financial services industry.

But be warned – the control, independence and lower cost structure afforded by having a SMSF comes with responsibilities. Step outside the rules and guidelines and you’ll most certainly feel the taxman’s wrath.

Over the coming weeks I’ll go into more detail on the do’s and don’ts of investing in a SMSF.

Vern Gowdie

Editor, Gowdie Family Wealth

From the Archives…

Is This the Spark to Send Australian Property Crashing?

26-07-2013 – Kris Sayce

Why it’s Deflation…Not Inflation, that’s Heading Our Way

25-07-2013 – Vern Gowdie

Why You Must Avoid This Big Investing Mistake…

24-07-2013 – Kris Sayce

The Dark Side of Technology: Part 2

23-07-2013 – Sam Volkering

The Dark Side of Technology: Part 1

22-07-2013 – Sam Volkering

Syria’s Assad bans foreign currency transactions

Syria’s Assad bans foreign currency transactions (via AFP)

Syria’s Assad bans foreign currency transactions (via AFP)Syrian President Bashar al-Assad issued a decree on Sunday banning the use of foreign currency in commercial transactions, state news agency SANA said. “It is prohibited to make payments, reimbursements, commercial transactions and any other commercial…