By www.CentralBankNews.info South Korea’s central bank held its base rate steady at 2.50 percent and expects inflation to gradually rise in the second half of the year from last year’s low base while the economy continues to grow weakly and will be below its potential output for a “considerable time going forward” due to the slow recovery of the global economy.

The Bank of Korea (BOK), which cut rates by 25 basis points in May, said exports had generally been favorable while “indicators of domestic demand have alternated between improvement and worsening.”

The global economy is expected to continue its “modest recovery going forward” but the BOK considers the downside risks to growth to comprise “the possibility of an earlier-than-expected tapering off of US quantitative easing and a slowdown in Chinese economic growth, and to the implementation of fiscal consolidation in major countries.”

Just as in major international financial markets, Korea’s markets have been volatile in recent months with stock prices falling substantially due to outflows of foreigners’ investment funds and long-term market interest rates rising in concert with those of major economies.

“After having depreciated greatly, the Korean won has appreciated to a considerable extent,” the BOK said.

Following the Bank of Japan’s launch of a new more aggressive quantitative easing in early April, the won rose over 10 percent against the Japanese yen through late May, causing concern over the competitiveness of Korean exporters. But the won then reversed course until mid-June when it started rising again.

Compared with the start of the year, the won has risen almost seven percent against the yen, quoted at 11.33 per yen earlier today.

Korea’s headline inflation rate was steady at 1.0 percent in June from May, continuing a declining trend since mid-2011. The BOK targets inflation of 2.5-3.5 percent.

It’s Gross Domestic Product grew by 0.8 percent in the first quarter of this year from the fourth quarter of 2012 for annual growth of 1.5 percent. The BOK has forecast growth of 2.6 percent this year, up from last year’s 2.0 percent.

The Three Most Critical Drivers of Stock Prices

What drives stock prices? In this bull market, it’s the Fed, earnings and jobs.

Or, more specifically, it’s the size of the assets on the Fed’s balance sheet, Wall Street’s consensus estimate for earnings per share for the S&P 500 Index, and initial filings for unemployment benefits.

Amazingly, these three factors sport a 90% correlation with the weekly price swings in the S&P 500. And that’s been the case ever since the bull market began in March 2009, according to a recent analysis by Jeffrey Kleintop, Chief Market Strategist at LPL Financial.

But earnings represent the “most fundamental driver” of all, says Kleintop. And that’s music to my insecure ears, since I routinely tell you that stock prices ultimately follow earnings. Yet many of you still email me to say that you just don’t believe it. (What’s it going to take, people?!)

So why am I bringing any of this up? Because we’re at the onset of another earnings reporting season. And that means I have a brand-new opportunity to put my trusty earnings theory to the test.

Per tradition, aluminum giant, Alcoa (AA), kicked things off for us on Monday evening, beating expectations. But forget about Alcoa (go here to see why).

Instead, here’s the single most important data point we need to focus on to determine if stock prices will, indeed, head higher…

Introducing the Analyst “Error” Rate

When it comes to having an innate ability to make terrible predictions, Wall Street analysts stand right next to economists and weathermen.

According to the latest FactSet data, analysts collectively expect S&P 500 companies to report almost non-existent earnings growth of 0.7%.

If they’re right, the stock market is all but certain to suffer a setback. If they’re wrong – and earnings growth for the S&P 500 checks in higher – giddy up! This bull market is going to blast higher.

So what’s my prediction? Analysts are going to be spectacularly wrong. (And based on their past performance, the odds are in my favor. Just saying.)

Simply put, analysts are too darn pessimistic. They’re giving in to recent warnings about how the slowdown in China and other emerging markets could affect U.S. corporate profitability.

A fellow contrarian, Richard Bernstein, has my back. He recently told Morningstar’s Kevin McDevitt that “a lot of people don’t realize some of the best growth stories in the world right now are in the United States.”

Amen, brother! And those “people” include analysts.

For what it’s worth, Bernstein also adheres to the “stocks follow earnings” philosophy, saying that we’ve been in a primarily “earnings-driven market” ever since 2000. Maybe his faith in the doctrine will encourage a few of the holdouts among us to convert.

If not, the tale of the tape this quarter should do the trick. By that I mean, if stock prices march higher thanks to stronger earnings growth, nonbelievers won’t have a choice but to accept the theory as true.

Bottom line: Analysts should have stuck to their March 31 prediction, which called for earnings growth of 4.2% for the quarter. As it stands now, the bigger their error, the higher we can expect the stock market to rally. Bet on it!

Ahead of the tape,

Louis Basenese

The post The Three Most Critical Drivers of Stock Prices appeared first on | Wall Street Daily.

Article By WallStreetDaily.com

Original Article: The Three Most Critical Drivers of Stock Prices

Fed hints no instant end to QE stimulus

According to the minutes released from the last Federal Reserve’s meeting , the Fed are not showing any signs of ending the bond-buying program as they need more signs of a stronger economy and an improved job market before proceeding with the cut back in the monthly $85 billion stimulus program .

However, the minutes released also showed the policy makers are still discussing and contemplating whether to end the bond-buying program by the end of 2013.

The minutes stated “many members indicated that further improvement in the outlook for the labor market would be required before it would be appropriate to slow the pace of asset purchases.”

Federal Reserve Chairman Ben S. Bernanke continued by highlighting the labor market is weaker than expected as the current unemployment rate is at 7.6%. The Fed Chief also highlighted the US dollar dropped 0.7% against the euro.

The Fed’s purchase of its monthly $85 billion in mortgage bonds and Treasuries , have kept the interest rate low, persuading people to purchase more properties to boost the economic growth .

Stocks rose as minutes from the Federal Reserve meeting were released, as the Standard & Poor’s 500 Index advanced 0.8 % to 1,661.40.

“It may well be sometime after we hit 6.5 percent before rates reach any significant level, so again, the overall message is accommodation. There is some prospective, gradual and possible change in the mix of instruments, but that shouldn’t be confused with the overall thrust of policy which is highly accommodative,” Bernanke stated in the minutes.

The post Fed hints no instant end to QE stimulus appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Europe Shares falls; Italy’s credit rating lowers

Europe shares fell on Wednesday as the Standard & Poor’s lowered Italy’s rating to BBB’ , because of the predicted weakening of the economic prospects .

The EuroStoxx 50 dropped 0.27% to 2,657.00, while the French CAC 40 lost 0.16% to 3,844.60. The UK FTSE 100 gained 0.10% to 6,519.30, while in Germany the DAX index fell 0.19% to 8,042.50.

With predictions of the Italian economy heading towards another quarter of high unemployment and contraction, the Prime Minister Enrico Letta suspended a property tax payment.

“The rating action reflects our view of a further worsening of Italy’s economic prospects coming on top of a decade of real growth averaging minus 0.04 percent,” S&P said. “The low growth stems in large part from rigidities in Italy’s labor and product markets.”

Italy’s Gross Domestic Product (GDP) is predicted to edge down from its previous estimated fall of 1.4% to 1.9%, according to S&P.

Meanwhile, the International Monetary Fund (IMF) lowered its prediction for the global growth from 3.3% to 3.1, and changed its outlook for Europe prediction of 0.4% to 0.6%, according to reports released.

In Germany, the Consumer prices rose by 0.1% in June, with continuous rising every month since May when it rose 0.4%. Annually the prices increased by 1.8%, according to reports released by the Federal Statistical Office.

In France, the industrial production fell by 0.4% month-to-month since May, compared to previous month’s growth of 2.2%, according to the National Institute for Statistics and Economic Studies.

With Italy still struggling with the economy, Italy’s industrial production rose by 0.1% in May, according to data from the National Institute for Statistics.

Italy is expected to auction the treasury bills with a target of 9.5 billion euros.

The post Europe Shares falls; Italy’s credit rating lowers appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Red Alert: Why This Stock Market Rally is a Trap

Yet again the markets are zooming around on the back of comments from our fearless leader Ben Bernanke.

First, the release of the minutes from the last FOMC meeting managed to confuse just about everyone with their opaqueness. Some people think this, others think that, so all up we might do this or that at some point in the future.

As a result, the stock market gyrated up and down and closed scratching its head.

But then Ben got on the pulpit and started to wax lyrical about the difference between tapering Quantitative Easing and raising interest rates. Bernanke said that even if unemployment did fall to his target of 6.5% it wouldn’t definitely mean that he would start raising rates from that point.

The stock market was closed at this stage, so the futures markets took off like a rocket on the back of these dovish comments from the king. But I have to ask. Why? What has changed?

Selling Pressure is Brewing for the Stock Market

The answer is nothing.

Basically Bernanke wanted everyone to know that it was going to be a long time until he raises interest rates.

The minutes from the FOMC are hinting loud and clear that tapering is on the table and it’s coming soon.

If they do start to taper then bond yields are going to continue rising. They have already spiked by over 1% in the last few months. That’s a huge move in the yield curve and it’s not going to stop because Bernanke has promised not to raise interest rates for the foreseeable future.

Did anyone think he could possibly start raising rates soon?

The other interesting thing to note is that the stock market has been rallying for months on the back of falling interest rates. The dividend yield on stocks was looking tempting when 10 year US Treasury bonds were yielding only 1.6%.

With bonds now yielding about 2.6%, a 2% dividend yield on stocks isn’t looking so great. If tapering does get started and yields continue to rise then the stock market should come under selling pressure.

But for now everyone is cheering his words. Not actions, not fundamentals – but words.

What a world we live in.

So how far can this market rally go, and when should we start to look for opportunities to get short for the next leg down?

ASX 200 Daily Chart

I’m going to give you a detailed technical view of the ASX 200 and where I see it going from here.

I realise how confusing it can be reading a technical analysis view of a chart because there are so many moving parts and squiggly lines rushing all over the place. I will be as clear as possible in my analysis.

I am using the terms L1, L2 and H1, H2 to describe the lower (L1,L2) and upper (H1,H2) bounds of the ranges that I make all of my calculations from.

The POC1 and POC2 terms relate to the Point of Control of each distribution in the chart, which is the midpoint between L1-H1 and L2-H2.

On the 16th of May (the day after the high was reached), I wrote to you and said:

‘Our stock market has traded in a pretty tight range for years. The gravity of the point of control at 4,700 is very strong and I would expect to see us revisiting that level at some point.

‘The first thing I need to see is a close under the 15th March high of 5,163. From there we should see a retest of 5,025-5,040. If the market can’t hold above that level then we’ll be re-entering the major long term range and we could expect to see a pretty quick trip to 4,700.’

The sell-off in late May and early June was certainly quick and we saw the retest of 4700 as expected.

From there we went into a sideways distribution (L2-H2), which has been shaking both the bulls and the bears out of their positions.

The interesting thing to note is that prices found support in an area which was 0.618 (Fibonacci level) outside of the upper range.

The Trap for Share Traders

The way to think about that is that prices are still under the gravitational influence of the POC1 even though prices have broken below L1.

Most share traders would think that prices have ‘broken out’ of that upper range when prices fell below L1.

The fact is that even though prices may be below the extremity of the range they can easily reverse course and re-enter the range. That’s why I call them ‘distributions’ and not ‘ranges’. A range sounds concrete, whereas a distribution is more fluid.

Distributions form because traders place ‘stop losses’ outside the extremity of the range, so the thing that will stuff up the most people is a ‘widening distribution’ that shakes everyone out of their position before the market is ready to have its real move.

Before the real move occurs though, you will often see a return to what I call the Point of Control. It acts as support or resistance, and then prices will shoot higher or lower out of the distribution and start trending again.

The rally from the lows at 4632 could possibly be a move such as this. The POC1 sits at approximately 5025, so we may see the ASX 200 rally all the way to that level. That is the upper bound of my ‘sell zone’ in the chart.

The lower bound of my sell zone is the bottom of the L1-H1 range at 4883. We have already busted above that level in the last few days.

So I am currently on red alert looking for potential selling opportunities.

The line at 5100 which is the ‘possible extent of rally’ in the chart, is the 76.4% retracement of the whole sell off from 5250.

Not many people look at the 76.4% retracement zone, but it is well worth keeping an eye on because the market will often reverse in that zone.

So I’ll let the market cheer Bernanke’s empty words, but I’ve got my eyes on some concrete levels where I believe we will find resistance. On the first signs of a reversal I will be jumping on board some short positions to ride the next leg down.

Murray Dawes+

Editor, Slipstream Trader

From the Port Phillip Publishing Library

Special Report: Panic of 2013

Daily Reckoning: Why Natural Gas Could Save Us From an Impending Energy Crisis

Money Morning: Why Oil Could be the One Commodity to Defy the Doom…

Pursuit of Happiness: Make Sure You’re Not a Property Investing ‘Loser’

No End to QE to See

Federal Reserve Chairman, Ben Bernanke said this in a recent Bloomberg article:

‘“If you draw the conclusion that I just said that our policies — that our purchases will end in the middle of next year, you’ve drawn the wrong conclusion, because our purchases are tied to what happens in the economy,” he said. “If the economy does not improve along the lines that we expect, we will provide additional support.”‘

The market isn’t listening to what Bernanke says…it’s panicking. Just about everything got hit as a result. Equities, bonds, commodities, precious metals, all were slammed as the US dollar rallied. The Aussie dollar collapsed 2 cents…that’s a massive move in FX land.

The speculators got it wrong. They positioned for a soothing Bernanke statement. But they just got more of the same. That is, if the economy moves into a sustainable expansion, we cut out the asset purchases…if it falters, we’ll ramp them up.

That sounds pretty straightforward, but it led to a massive unwind of leveraged bets in anticipation of the beginning of the end of easy money.

Is it really though? The ‘end’ of QE might just be the thing that ensures it remains a part of the financial lexicon for years to come.

Why?

Well, bond yields are on the rise. The US 10-year bond yield, a benchmark for the global cost of credit, traded around 1.6% at the start of May. Following another sharp sell-off overnight, it’s now at 2.33%, the highest level in over a year.

In general, global market interest rates follow the lead of the US 10-year Treasury bond. So rising rates represent a tightening of monetary conditions in financial markets. Which means the US economy, for years heavily dependent on easy money, will come under pressure soon as higher interest rates begin to bite.

And if the US economy comes under renewed pressure, Bernanke won’t cut QE anytime soon. So no end to QE…long live QE!

But what if the US economy really is recovering? And what if this recovery DOES end QE sometime next year and then interest rates move back to normal in subsequent years?

Years of zero interest rates have robbed the system of real savings. In its place, the level of total debt has ballooned to keep up the façade of healthy and sustainable growth. And in the meantime, the structure (industry, incomes, employment, profits taxes etc) of the economy grows around this ongoing provision of cheap and easy money.

If you try to take it away, the economy will fall in a heap. That shouldn’t be a big deal but we’re talking about the world’s largest economy, and consumer of last resort here. The US’ ongoing propensity to consume more than it produces is made possible by easier and easier money.

As money becomes cheaper, debt levels grow to fund consumption. The whole economic structure of the world economy grew out of this falling US interest rate/rising debt/excess consumption model.

You think we’re going to get out of it easily? You think the Fed can all of a sudden put an end to this multi-decade trend without major problems?

Throw in the world’s second largest economic zone, (Europe) which is in the throes of its own painful structural adjustment…and the world’s second largest economy, China, which is about to experience what it’s like when a credit bubble goes bust, and…well, Houston, we have a problem.

So if QE can’t really end, where to from here?

If confidence in the Fed and Bernanke is receding, then liquidity will soon follow. One of the most beneficial impacts of QE is that it instils confidence. Confidence creates liquidity which creates asset price inflation.

In the Q&A following the press conference, someone asked about sharply rising bond yields over the past few weeks, and how that reconciles with the Fed’s view that it’s the stock of assets it holds on its balance sheet that determines yields.

Bernanke responded ‘we were puzzled by that‘, and then tried to explain it away by citing other factors like potential optimism about the outlook for the economy (optimism not shared by any other asset class, by the way).

When you admit to being puzzled by the effects of the largest monetary experiment in history, which you implemented, it’s a confidence drainer. And with confidence goes liquidity.

Greg Canavan+

Editor, The Daily Reckoning Australia

[Ed Note: To read more of Greg’s in depth macro-economic analysis, click here to subscribe to the free daily e-letter The Daily Reckoning.]

From the Archives…

The Power of Low Interest Rates Coming to the Aussie Market

5-07-2013 – Kris Sayce

S+P 500 Downtrend Looms? Counting Down The Days…

4-07-2013 – Murray Dawes

Here’s Your Six-Point Stock Buying Checklist

3-07-2013 – Kris Sayce

Are the Credit Rating Agencies at it Again?

2-07-2013 – Kris Sayce

Why This Could be Another Great Year for Australian Stocks…

1-07-2013 – Kris Sayce

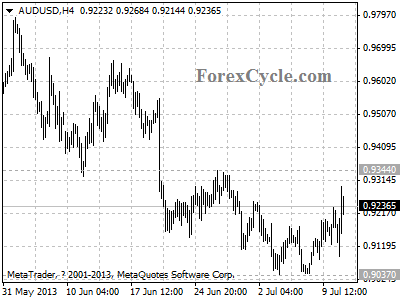

AUDUSD’s rise from 0.9037 extends to 0.9297

AUDUSD’s upward movement from 0.9037 extends to as high as 0.9297. Further rise to test 0.9344 resistance is still possible, as long as this level holds, the rise could be treated as consolidation of the downtrend from 1.0582 (Apr 11 high), another fall towards 0.8500 is still possible after consolidation. On the upside, a break above 0.9344 key resistance will suggest that the downtrend from 1.0582 had completed at 0.9037 already, then the following upward movement could bring price back to 0.9800 zone.

Provided by ForexCycle.com

Brazil raises rate for third time this year to 8.50 %

By www.CentralBankNews.info Brazil’s central bank raised its benchmark Selic rate by another 50 basis points to 8.50 percent, as expected, to help bring inflation under control.

It is the third consecutive rate rise by the Central Bank of Brazil, which has now raised rates by a total of 125 basis points this year. Last year the central bank cut rates by 375 basis points as economic growth fell.

The decision by the central bank’s monetary committee, known as Copom, was unanimous and the decision was not accompanied by a bias toward its next move.

“The Committee considers that this decision will contribute to bringing inflation toward a decline and ensure that this trend will continue next year,”the central bank said in a brief statement.

Brazil’s inflation rate rose to 6.7 percent in June from 6.5 percent, above the central bank’s target of 4.5 percent, plus/minus two percentage points.

The central bank has forecast inflation of 5.7 percent this year and 5.3 percent in 2014.

Brazil’s Gross Domestic Product rose by only 0.6 percent in the first quarter from the fourth quarter for annual growth of 1.9 percent, up from 1.4 percent in the previous quarter.

Is Gold going to Rally Back to 1300$ per Ounce?

Article by Investazor.com

Chart: GOLD, H4

As it looks now, in our opinion, the answer would be not yet. The FOMC meeting minutes showed that there are more members that agree with the tapering of the Quantitative Easing program, but it wasn’t specified the date for the start of the tapering. The speculated date was September this year, but it seems that the Federal Reserve has to see whether the unemployment rate is heading to 7%.

After the Minutes the dollar lost some ground, gold rallied to 1265$ per ounce but didn’t stay too much there. In less than an hour Ben Bernanke will have a speech and the investors will keep their eyes and ears focused on what the Fed’s chairman is going to say.

From the technical point of view, the price of gold encounter a good resistance area at 1268.00 level, that was tested 2 more times in the past 3 weeks, and could not pas. The bounce off 1265$ might mean that the pressure is still on the downside, even though it can be spotted an Ascending Triangle price pattern on the chart.

To wrap it up, during the speech of Bernanke we will look at the support 1243.30 and resistance 12568.45 key levels. Under the support the targets will be 1220.00, 1200.00 and 1180.00, while above resistance the price targets would be 1302.45 and 1350.00.

The post Is Gold going to Rally Back to 1300$ per Ounce? appeared first on investazor.com.

Tajikistan cuts rate by 40 bps due to lower inflation

By www.CentralBankNews.info Tajikistan’s central bank cut its refinancing rate by 40 basis points to 6.1 percent in light of a decline in inflationary pressures and the impact of external factors.

The National Bank of Tajikistan, which last cut its rate by 30 basis points in August last year, also said in a statement from July 9 that the rate cut should make implementation of monetary policy more effective and lead to a decline in average interest rates on loans in the banking system.

Tajikistan’s inflation rate eased to 5.6 percent in May from 5.9 percent in April while its Gross Domestic Product expanded by an annual 7.3 percent in the first quarter of 2013, down from a pace of 7.5 percent in the previous quarter.