One of my favorite scenes in Martin Scorsese’s The Departed is the exchange where Jack Nicholson asks Leonardo DiCaprio what a nice kid like him was doing in the South Boston projects. “And if I can slander my own environment, it makes me sad, this regression.”

Unfortunately, I find myself asking the same question about my profession at times. If I may slander my environment a little, it makes me sad to see people trust their financial security to the fickle whims of the stock market. At best, it is a cold game of chance, and at worst—as the debacle of the Facebook ($FB) IPO showed—it’s a game that has been rigged against them.

To be sure, there are ways to mitigate the worst risks of stock market investing. Never buy or sell on a “hot tip” unless you’ve done your homework first and have reason to trust the source. Avoid microcap and penny stocks with anything other than your “play money.” If you use an investment advisor or money manager, make sure they use a reputable third-party custodian, lest you fall victim to a Bernie Madoff-style Ponzi scheme.

Getting more into my areas of expertise, focus on dividends, though beware of chasing high dividend yields. Focusing on dividends and cash flows offers a degree of safety that a buy and hold (and pray) strategy can never offer, and you can realize a respectable cash return even in a down market.

But the best way to avoid taking unnecessary risk in the capital market is to refrain from putting your entire life savings into it. Make sure that a significant chunk of your net worth and current income come from outside the traded markets.

This might sound like odd advice coming from a man who earns his living investing in the capital markets, but it is the only sound advice.

Think about it for a minute; what did your grandparents do? Before the democratization of the stock market through mutual funds and 401k plans, people still invested their savings. They still accumulated wealth, but they were more creative in how they invested it.

Let me throw out an example. My grandfather owned a small warehouse and shop floor in Fort Smith, Arkansas. The rents generated from that property alone were sufficient to cover my grandmother’s modest retirement needs after he passed away. He would have never left her financial security hanging on something as fragile as a 4% withdrawal rate from an index fund. (Ironically, given the theme of this article, his stock and bond portfolio ended up throwing off a lot more income than his warehouse, but he had no way to know that ahead of time.)

I’ve written before about rental houses as an investment (see “Here’s the catalyst for a housing rebound”), and I would like to reiterate that recommendation today. I know of no other legal investment that allows for both tax free current income (technically “tax deferred” for you accountants out there) and capital appreciation that will likely at least keep pace with inflation and allows you to do it all with borrowed money.

Yes, I know. Home prices are falling. Americans are broke. There’s an enormous backlog of foreclosed properties that have to be worked off. All of this is true.

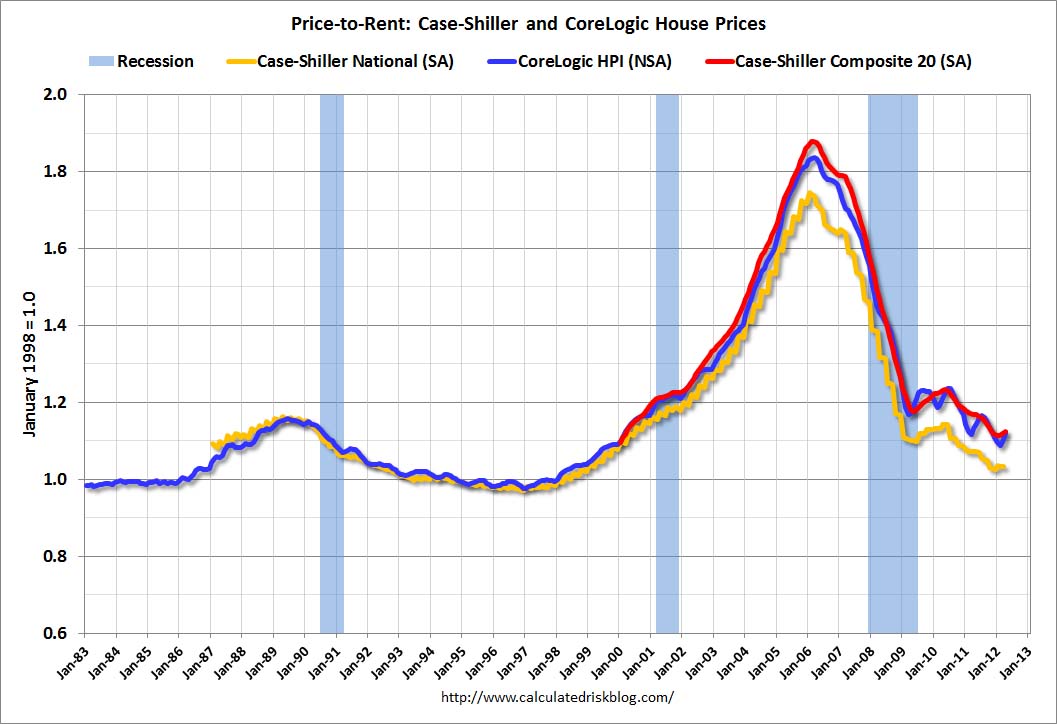

But it is also true that new construction has been close to nil in recent years even while the population has grown and that mortgage rates—even for rentals—are at low levels most of us never dreamed possible. Nationally, the price-to-rent ratio has fallen to levels not seen in well over a decade, and in many markets it is far cheaper to buy than rent.

{kind=link}

On balance, it would seem that flattish prices would be more likely than large declines in most areas, but that is not really the point. I’m not recommending you buy-and-hold the Case-Shiller Housing Index (sadly, there were ETFs to track this for a while; thankfully, they folded). I recommending you put on a good pair of walking shoes and that you look around for a handful of rental properties that you can reasonably expect to rent out at a profit after allowing for debt service and expenses.

To clarify, I’m not recommending you quit the stock market altogether. There is money to be made for those with the patience and emotional temperament for it, and stocks—like rental real estate—can be fantastic generators of cash income.

But they shouldn’t be the only asset you own, and you shouldn’t bet your retirement on capital gains that may never come.

If you liked this article, consider getting Sizemore Insights via E-mail. This article first appeared on MarketWatch.

No related posts.