One of the buzzwords at this week’s Australian Petroleum Producer and Explorer Association (APPEA) conference is ‘Shale’.

And specifically, shale gas.

If you’re not familiar with it, shale gas is gas that’s trapped within deep shale rock formations. Until recently, it was almost impossible to recover this gas.

But technological advances mean natural gas companies can now access this gas. To the extent that it’s now revolutionizing the energy world right before your eyes.

The US Shale Gas Story

Nowhere has it had a bigger impact than in the United States. Less than 10 years ago, the US faced an energy crisis. Today they have more natural gas than they know what to do with.

Based on what I’ve heard this week at the ‘oil and gas show’, Australia has a chance to follow the same path. And that could be great news for you, if you get in early…

Shale gas already makes up 30% of the US gas supply. By the end of the decade, it could reach 50%.

The rapid success of shale gas exploration and production means cheap natural gas for the US. Really cheap!

Just four years ago, gas was USD$14 per million British thermal units (mmBtu). Last month, it fell below USD$2 mmBtu. This cheap energy can make life tough for the producers, but is a gift for the US economy.

The benefits go beyond affordable heating, transport, and more competitive manufacturing. It also creates jobs.

According to J. Michael Jaeger, the CEO of BHP Billiton Petroleum, ‘the unconventional energy sector has been responsible for 600,000 new jobs in recent years, and this is set to increase to 850,000.’

And by his estimates, the sector adds USD$100 billion to the US economy each year.

But this American energy revolution didn’t come easy.

In North America between 2008 and 2011, explorers drilled 15,000 shale gas wells. That takes a lot of investment, a lot of time and a lot of risk.

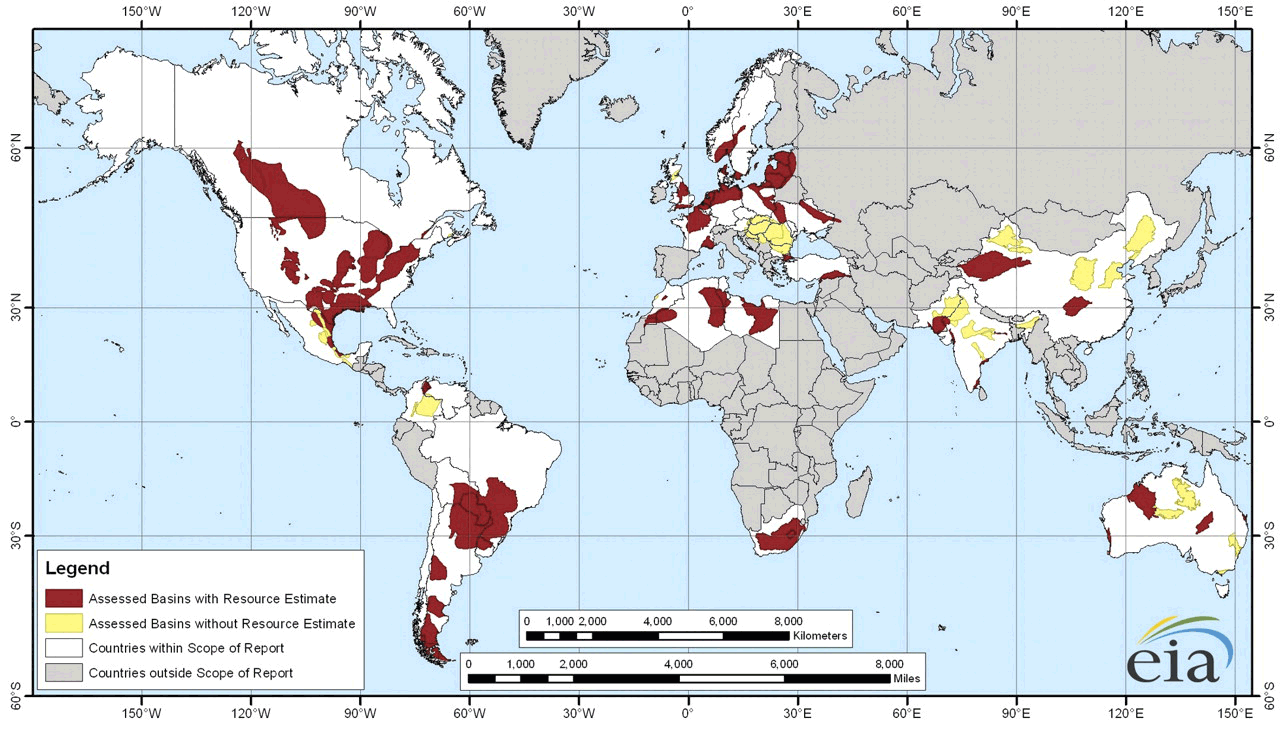

Abundant Shale Gas Basins

But, as you can see on the map below, you’ll find shale basins all over the world. Canada, Brazil, Argentina, South Africa, Europe, China, and of course…Australia.

But in the time the North Americans drilled 15,000 wells and ensured cheap gas for decades to come, how much progress has the rest of the world made?

Less than 100 wells drilled.

So Australia has a lot of catching up to do. But it’s making tracks.

The Australian Shale Gas Story – Still in Early Stages

The market has embraced the shale story. Aussie shale stocks like Buru Energy (ASX: BRU) have gone up eight–fold in the last two years.

It’s an exciting start, but there’s still a long way to go for the Aussie shale industry.

And the best time to get in is before the industry becomes mainstream…before local explorers have drilled 15,000 wells.

My old pal, Australian Wealth Gameplan editor, Dan Denning knows this. Dan first wrote about shale gas in 2005.

This is what he wrote at the time:

‘If the U.S. government is eventually going to pump billions of dollars into the development of the shale industry, with the goal of national energy independence, I want to figure out who’s going to benefit the most…

‘…I’d rather be ahead than behind on the shale curve.’

He was ahead of the curve. Back then, the US produced less than two billion cubic feet (bcf) of shale gas per day.

This year the US is set to produce nearly 25 bcf of shale gas per day.

And last year he tipped a handful of Aussie stocks that he thought would benefit from the Aussie shale gas story.

But the real billion–dollar–question is, can we recreate North America’s success with shale gas, here in Australia?

We have the potential, but there are some big differences between Australia and the US.

Shale Gas With an Oil Kicker?

Research and Consulting Service, Wood Mackenzie, asked this question at the conference this week. The good news is they reckon it can be done.

The bad news is a number of stars need to align first.

First, explorers need to do much more drilling to see if the geology is right, and whether it’s possible to produce natural gas commercially.

Then there’s the issue of support services. It’s still a new game here, and, unlike in other resources sectors, we don’t have all the players, expertise and equipment to get the job done.

Remote locations, and the wet season, add an extra challenge.

We also need to ask the question — does Australia even need shale gas?

We have plenty of conventional natural gas already. Then we have the Coal Seam Gas industry, which is still growing, and now meets 40% of East Coast Australia’s natural gas needs. And, as I mentioned yesterday, the LNG industry is already set to triple production in the next six years.

So where does shale gas fit in to the Australian energy mix?

As with everything, it depends on the production cost. If it’s cheap enough, Australia can enjoy even more affordable natural gas, and could turn it into another export revenue stream.

But shale gas isn’t the only opportunity. The real money–spinner could be in ‘shale oil‘.

Shale Oil – ‘Liquid Rich’

They call shale ‘liquids rich’ when it contains oil. Oil is more profitable, and easier to export. Finding it in Aussie shale plays could help kick–start the development of a profitable Aussie shale industry.

The biggest opportunities for shale oil are in the Canning, Cooper and Georgina basins. They each have ‘liquids’ potential, but so far no–one has struck shale oil yet, only shale gas.

There’s a lot of Australian shale exploration planned this year. Joint ventures between small Aussie companies and giant overseas firms are drilling the better–known ‘Canning basin’ in WA and ‘Cooper Basin’ in South East QLD.

Drilling and hydraulic fracturing (fracking) is also taking place in the Georgina Basin in the Northern Territory, Gippsland in Victoria, and Galilee Basin in Queensland.

Back when the US shale boom was at this early stage, land was cheap.

Today, US shale acreage valuations are through the roof. Early investors in the right projects scored big.

This is probably why you see big players like Mitsubishi (TYO: 8058), BG Group (LON: BG), ConocoPhillips (NYSE: COP) and Hess Corp. (NYSE: HES) moving in early on the Aussie shale gas story.

And ConocoPhillips for one says it wants more.

With big companies getting in at the ground floor — and with so much focus on the sector at Australia’s largest oil and gas conference — it already looks like the shale sector is set to be Australia’s next resources boom.

Dr. Alex Cowie

Editor, Diggers and Drillers

Related Articles

The Conference of the Year "After America" DVD

APPEA – Day One at the Oil & Gas Show: Sand Dunes, Scuba Diving and Camels

Why Europe Will Ditch Green Energy

Tradervox (Dublin) – The FOMC minutes were released yesterday showing that some members still think quantitative easing might be required is the economy loses momentum due to turmoil in Europe or due to the inability of lawmakers in US to reach consensus on the budget. As a result the dollar retreated from its four-month high against the euro as yen declined against 16 of the most traded currencies as speculation of Bank of Japan added stimulus next week rose. According to BOJ governor Masaaki Shirakawa, the central bank is keen on supporting growth in the country.

Tradervox (Dublin) – The FOMC minutes were released yesterday showing that some members still think quantitative easing might be required is the economy loses momentum due to turmoil in Europe or due to the inability of lawmakers in US to reach consensus on the budget. As a result the dollar retreated from its four-month high against the euro as yen declined against 16 of the most traded currencies as speculation of Bank of Japan added stimulus next week rose. According to BOJ governor Masaaki Shirakawa, the central bank is keen on supporting growth in the country. Tradervox (Dublin) – The Canadian dollar has weakened to its lowest last seen in January after the European central bank indicated that it is going to reduce its lending to some banks in Greece to reduce its risk. Investors have taken this to mean that Greece might lose its position in euro zone which has caused risk aversion.

Tradervox (Dublin) – The Canadian dollar has weakened to its lowest last seen in January after the European central bank indicated that it is going to reduce its lending to some banks in Greece to reduce its risk. Investors have taken this to mean that Greece might lose its position in euro zone which has caused risk aversion.